President's Note

Dear Friends,

Our younger generation is a major resource not only for the development of financial prosperity but also for social changes as well. Despite this, millennials often face hurdles on a daily basis, with their energies and capabilities not being channelized in the right direction. We in the Chamber have always advocated the importance of empowering our youth. In this context, last February, we organized a two-day certificate Workshop “The Last Mile – Eligibility to Employability” for the students to develop/polish their employability skills. The programme received a huge response from the student community. We now plan on taking this forward in a bigger and better way. The details of the same, once finalized will be sent to all of you. I urge you to get as many youngsters as possible to participate in this event which is scheduled for January 2020.

The Government’s approval of the Kerala Metropolitan Transport Authority Bill is a huge step towards regaining the lost glory of public transport and reducing today’s traffic congestion. We hope that this initiative will help bring about seamless mobility to increase productivity and prevent wastage of time and fuel.

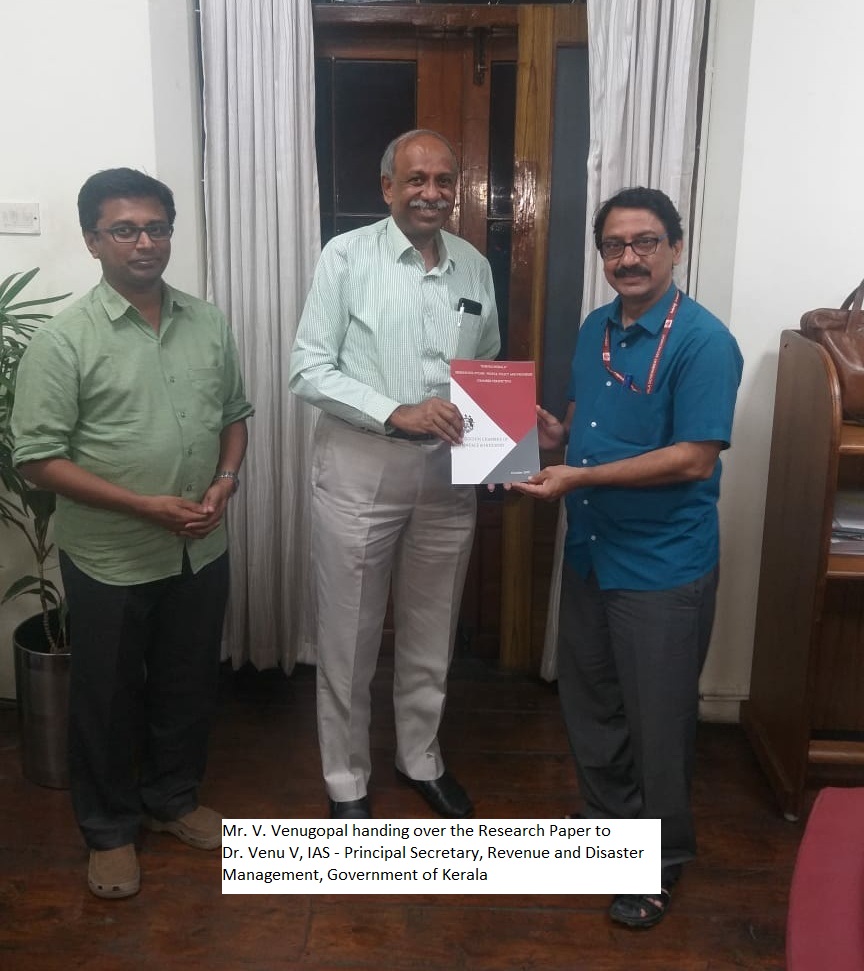

Last month, the Chamber published a Briefing book entitled “Rebuild Kerala’ – Seeking Solutions: People, Policy and Progress, Chamber Perspective which is aimed at supplementing the Government of Kerala’s Nava Keralam efforts towards a mission mode of development. I had the privilege of presenting the same to Mr. Tom Jos I.A.S, Chief Secretary, Government of Kerala and to Dr. Venu I.A.S, Revenue Secretary, Government of Kerala. It was a proud moment for the Chamber as our efforts and suggestions were well appreciated.

I am also happy to inform you that the Kerala Farmers’ Welfare Fund Bill 2019 passed by the State Assembly last week contains various suggestions that the Chamber had raised during the time of discussions.

The Chamber has also sent in a representation on the Draft Occupational Safety Code 2019.

Coming to this month’s activities, we started with the CEO Forum – Breakfast Meeting on the 1st of November. The Speaker for the meeting was Mr. Ravi Tennety Chief Executive Officer – Training and Skilling Division, Quess Corp Limited, Bangalore who spoke on the topic “Skilling – The Engine of the Economy.” The Forum discussed the relationship between skills and economic growth and how skill development could accelerate higher economic growth for the country. The session was well appreciated by all the attendees.

On the 8th of November, we organized a Half-Day Session on “GST – Upcoming Changes, Legislative, Legal and Other Updates.” The Speakers for the session were Mr. Kunal Wadhwa, Partner, Indirect Tax, PwC India, Bangalore, and Ms. Nisha Menon, Director, Indirect Tax, PwC India, Cochin. The purpose of the session was to provide the participants with a brief update on the proposed changes under GST and also shed some light on recent key amendments. The programme was attended by 70 participants from various organizations.

It has become increasingly clear in recent decades that lifestyle factors contribute significantly to the ever-growing bane of chronic diseases. To create an awareness about the impact of lifestyle on health, the Chamber conducted a Half-Day Session on “Lifestyle Diseases and Wellness Management” on the 26th November, in the Chamber Conference Hall. The Session was addressed by Dr. Sujith S R, CEO, Haya Wellness; Wellness Consultant and Nutrition Medical Specialist. The programme was attended by 35 participants from various organizations.

The last CEO Forum – Breakfast Meeting of this edition will be held on the 6th of December 2019 at Taj Gateway, Ernakulam. The Speaker at this session will be Dr. Jacob Varghese, Head of Orthopaedic Department, VPS Lakeshore, Kochi who will speak on “Joint Health & Safety – Maintenance and Preservation” and it’s Medical Tourism Potential for the State. I trust you will make use of this opportunity and attend the session.

As we continue to grow, we are working diligently to develop programmes and sessions which are insightful and relevant to our members and the business community. We are exploring new ways to work and build partnerships, creating a path for the Chamber to stay strong and grow into the future. We are also working on ways to improve member support and engagement. I encourage companies and business leaders to engage with us to experience the value that the Chamber has to offer to you and your business and make most out of your membership.

Wishing everyone the very best of this festive season!!!

V Venugopal

Quote

Obituary

Mr. George Paul – Vice Chairman – Synthite Industries Private Limited

Former Executive Committe Member of the Cochin Chamber, passed away on 26.11.2019

Recent Events

11th CEO FORUM Breakfast Meeting

Skilling - The Engine of the Economy | 01.11.2019

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s 11th Breakfast Meeting on Friday, 1st of November 2019 at the Taj Gateway Hotel, Ernakulam.

Mr. V Venugopal, President of the Chamber, delivered the Welcome Address and introduced the Speaker for the meeting.

Mr. Ravi Tennety, Chief Executive Officer – Training and Skilling Division, Quess Corp Limited, Bangalore spoke on “Skilling – The Engine of the Economy.” The forum discussed the relationship between skills and economic growth and how skill development could facilitate a higher growth in the economy.

Mr. Tennety said that a well-educated population, equipped with knowledge and skills is not only essential for economic growth, but is also a precondition for steady growth since it is the educated and skilled person who will benefit most from the employment opportunities. He also said that knowledge, skills, and technology are the backbone of our economy and we have to recognize these three elements as the key drivers to economic growth.

Mr. Tennety emphasized the fact that the secret to realizing the potential of an emerging superpower like India lies in understanding and steering through the complexities of its economy. While India’s large young workforce is a great resource, it isn’t being utilized optimally to power the nation’s growth. He said that 12 million are expected to join the labour market every year for the next 2 decades and 57% of the population is in working age (700 million) of which 500 million will need some form of vocational skills.

In the age of the Fourth Industrial Revolution and the ever-increasing shift towards automation and digitization, jobs demand familiarity and expertise in disruptive technologies. These skill requirements posing a challenge to young Indians and there is a huge mismatch between the demand and supply in terms of a skilled workforce. This is weighing the nation down and crippling its long-term economic growth prospects, he said.

Mr. Tennety explained the Skill Pyramid and presented a statistical report of opportunities in different sectors for people falling under different skill levels in the pyramid. He said that policies like NAPS should be promoted and significant resources should be allocated for skill development initiatives. He pointed out that the low industry participation in building skill capital and low investments in talent building need to be addressed immediately.

The Forum also discussed the supply and demand-side constraints like the unorganized sector, the agri-based economy, high rural population, parental pressures, demographic peer groups, lack of a premium on skills, low-cost structure, low career progression opportunity, low minimum wages and high urban cost of living, etc.

Mr. Bibu Punnooran, Executive Committee Member of the Chamber presented a Memento the Speaker.

Mr. K Harikumar, Vice President of the Chamber proposed the Vote of Thanks.

Meeting with the Chief Secretary & other Government officials

07.11.2019

The Cochin Chamber of Commerce & Industry has compiled a Research Paper entitled “Rebuild Kerala – Seeking Solutions – People Policy and Progress – Chamber Perspective” which the Chamber President Mr. V. Venugopal handed over to Mr. Tom Jose, IAS – Chief Secretary, Government of Kerala and the Revenue Secretary, Dr. Venu IAS at Trivandrum.

The document, prepared by the Research Cell in the Chamber, is aimed at helping the prioritisation of reforms in different fields to strengthen the foundations of the Nava Keralam establishment process.

The United Nations in its report Kerala Post–Disaster Needs Assessment (Floods and Landslides) August 2018 had suggested the need for a ‘broad policy framework’ which provides a coherent narrative and binds all the sectors to a common vision of Nava Keralam.

Our report is a step in this direction. The report is based on three pillars i.e. people, policy and progress, hence the title- Seeking Solutions- People, Policy and Progress, Chamber’s Perspective. We have listed 40 reforms categorised under nine chapters relating to innovation, ease of doing business, agriculture, education, health, tourism, governance, environment etc. The different Chapters explain the status quo and suggest interventions with the help of relevant resources and best practices. Our report emphasises the need for upgrading the State’s industrial competitiveness, facilitating innovation and promoting participatory governance among other things. We have emphasised on the sustainable development aspect in every intervention we have suggested.

We hope to initiate a conversation with the Government on the need for structural reforms and to cooperate in facilitating the Nava Keralam process for a better tomorrow.

Goods and Services Tax

Upcoming Changes, Legislative, Legal and other Updates | 08.11.2019

The Cochin Chamber of Commerce and Industry conducted a Half-Day Session on GST – Upcoming Changes, Legislative, Legal and other Updates on 8th November 2019 at Hotel Park Central, Kaloor.

Mr. Thomas Sebastian, Deputy Secretary of the Chamber, delivered the Welcome Address and introduced the Speakers for the session, Mr. Kunal Wadhwa, Partner, Indirect Tax, PwC India, Bangalore, and Ms. Nisha Menon, Director, Indirect Tax, PwC India, Cochin.

The purpose of the session was to provide the participants with a brief update on the proposed changes under GST and also shed some light on other key amendments. The programme was attended by 70 participants from various organizations.

The first half of the session covered e-invoicing, its purpose, and implementation and key updates under the e-invoice format. Ms. Menon explained the major changes in the e-invoice scheme, clarifications to be provided and key points for the seller and buyer. She also explained the new return framework in detail.

The second half of the session started with the normal monthly return process and the key steps to be considered while filing the same. Mr. Wadhwa explained the restrictions on the availing of ITC and the recent legislative and judicial updates. The session also covered the evaluation of customer support services and marketing support services in the context of intermediary services under GST. Mr. Wadhwa threw some light on the tax exposure on the account of deemed supply under GST and the legacy dispute resolution scheme.

Before concluding the session Mementos were presented to Mr. Wadhwa and Ms. Menon.

Mr. Manu Varghese, Deputy Secretary of the Chamber proposed the Vote of Thanks.

Lifestyle Diseases and Wellness Management

26.11.2019

The Cochin Chamber of Commerce and Industry organized a Half-Day session on “Lifestyle Diseases and Wellness Management” on 26th November 2019 in the Chamber Conference Hall, Willingdon Island.

Mr. V Venugopal, President of the Chamber delivered the Welcome Address.

Dr. Sujith S R, CEO, Haya Wellness; Wellness Consultant and Nutrition Medical Specialist was the Speaker at the session.

Dr. Sujith commenced the session by outlining the history of ‘bacteria,’ one of the earliest forms of life and a word that often brings about a sense of uneasiness in everyone. Dr. Sujith said that the number of bacterial cells in the body is commonly estimated at 10 times the number of human cells. Every coin has two sides, bacteria are essential for one to survive but there are some harmful forms of bacteria too. Humans and Bacteria need each other, he added.

The brain has a direct effect on the stomach and intestines. Dr. Sujith explained that a troubled intestine can send signals to the brain, just as a troubled brain can send signals to the gut. Therefore, a person’s stomach or intestinal distress can be the cause or the product of anxiety, stress, or depression since the brain and the gastrointestinal system are intimately connected. This is especially true in cases where a person experiences gastrointestinal upsets with no obvious physical cause. For such functional gastrointestinal disorders, it is difficult to heal a distressed gut without considering the role of stress and emotion, he said.

Dr. Sujith also explained the importance of the microbiome, and why it is the key to human health. A plethora of conditions, from obesity to anxiety, appear to be linked to the microbes inside every human.

The session covered the scientific hypothesis called the ‘thrifty gene’, which states that obesity in some human beings can be explained by the existence of a ‘thrifty gene’ that aids the storage of excess energy as fat. Zinc has a key role as a catalyst in a wide range of reactions and is, in fact, a catalyst for about 100 enzymes. It is important in the structure of the cell to transport proteins such as vitamins A and D. Dr. Sujith listed out the key roles Zinc performs in a human body viz. regulating gene expression; stabilizing cell membranes, helping to strengthen their defence against oxidative stress; participating in the synthesis, storage, and release of insulin; interacting with platelets in blood clotting; and influences thyroid hormone function.

The session also covered the importance of Vitamins C, D and K, signs of progesterone and estrogen deficiency, treatment of menopausal symptoms, etc. in detail.

On this occasion Medivision Scan & Diagnostic Research Centre conducted a free random Blood Sugar and Blood Pressure test for all the participants.

Mr. P S Menon, Executive Committee Member of the Chamber presented a Memento to Dr. Sujith and Mr. Bibu Punnooran, Executive Committee Member of the Chamber proposed the Vote of Thanks.

The session was attended by 35 participants from various member organizations.

Trivia

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

CBDT communicates its view on accumulated MAT credit and additional depreciation under the newly introduced lower tax rate regime

The Taxation Laws (Amendment) Ordinance, 2019 (Ordinance), which was promulgated on 20 September 2019 by the President of India, introduced section 115BAA of the Income-tax Act, 1961 which allowed domestic companies to opt for an alternative income-tax regime from financial year 2019-20. The key features of the alternative income-tax regime are as follows:

- Reduced income-tax rate of 22% (plus surcharge and cess) will be applicable;

- Certain exemptions, deductions, allowances (including additional depreciation) will not be available; and

- Minimum Alternative Tax (MAT) will not apply.

There is no time limit for companies to opt for the new tax regime; however, once adopted, it cannot be withdrawn.

- There were few open issues that emerged when interpreting the Ordinance for which the Government’s view was sought. Upon receipt of representations from various stakeholders the issues were examined and the following view has been expressed by the Central Board of Direct Taxes vide circular no. 29/ 2019 –

- Companies opting for the new tax regime will not be allowed to offset brought forward loss on account of additional depreciation.

- Given that MAT would not be applicable for companies opting for the new tax regime, they will not be allowed to utilise brought forward MAT credit.

- Companies having brought forward loss on account of additional depreciation or brought forward MAT credit, have the option to offset such loss and MAT credit under the tax regime existing prior to the promulgation of the Ordinance, and thereafter, opt for the new tax regime.

PwC comments: The above circular has put to rest any ambiguity in how the new tax regime will operate for these issues. Corresponding amendments to the Ordinance can be expected.

Gift of shares made by a company under an internal restructuring exercise not a “colorable device” – revision under section 263 rejected

The Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) holds transfer of shares of a company as “gift” by a taxpayer to its group company is not a colorable device. It rejected the Revenue’s contention that the taxpayer had resorted to circular transaction of transfer of shares to avoid capital gains tax.

In addition, the Tribunal quashed the Commissioner of Income-tax’s (CIT) revisionary order under section 263 of the Income-tax Act, 1961 (Act), as the Tribunal observes that the tax officer (TO) had made due enquiries during the assessment proceedings and the CIT was only trying to substitute its opinion, which cannot be done by exercising revisionary jurisdiction under section 263 of the Act

PwC Comments: Based on the facts and circumstances the Tribunal has re-iterated that the transfer of shares as “gift” by the taxpayer to its group company is not a “colorable” device.

Tribunal holds section 79 not applicable where the shareholder continues to hold 100%, although partly indirectly, post-amalgamation of the company having brought forward losses

The Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) in the case of the taxpayer held that the condition under section 79 of the Income-tax Act, 1961 (Act) for carry forward and set-off of loss, is said to be satisfied if the beneficial shareholders of the company during the year when the loss was incurred, directly or indirectly holds at least 51% shares in the said company during the year of set-off.

PwC Comments: This judgement reaffirms that the continuity of the ultimate beneficial ownership, and not immediate direct ownership, is required to satisfy the conditions of carry forward and set-off of losses under section 79 of the Act.

Advances by a subsidiary, as a business venture on profit share basis, for strategic investments to be made by the holding company not dividends under section 2 (22) (e)

The Indore bench of the Income-tax Appellate Tribunal (Tribunal), while dealing with the issue of deemed dividend, held that the amount received as loan/ advance from a subsidiary for making further strategic investments will not be covered under section 2(22)(e) of the Income-tax Act, 1961 (Act). In addition, in view of peculiar facts of the case, the Tribunal held that for calculating the amount of deemed dividend, the opening balance of accumulated profits needs to be considered

International Tax

Based on specific facts, capital gains on sale of shares in an Indian company, carrying on real estate business, held not taxable under India-Spain tax treaty

Recently, the Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) held that capital gains on sale of shares in Indian real estate companies are not taxable under Article 14(4) of the India-Spain Double Taxation Avoidance Agreement (tax treaty), since such companies were engaged in the business of real estate development and not in the business of holding real estate assets as investments. The Tribunal also observed that merely because a company deals in real estate development, it does not imply that it consists principally of immovable properties. Further, the Tribunal held that gains arising on foreign exchange transactions shall not be taxable as “other income” under Article 23 of the India-Spain tax treaty.

PwC Comments: The Tribunal’s ruling has laid down that merely holding shares in a company engaged in real estate development would not lead to taxation in the source country, i.e. country in which the immovable property is located. The quantum of stake held by the taxpayer and whether assets of such company comprise 50% or more from immovable property needs to be factored while determining the taxability under the tax treaty.

Transfer Pricing

CBDT amends rules for computation of interest in case of secondary adjustment

Background

Rule 10CB of the Income-tax Rules, 1962 (Rules) was introduced for the purpose of computation of interest income pursuant to secondary adjustment provisions introduced in section 92CE of the Income-tax Act, 1961 (Act). The Central Board of Direct Taxes (CBDT) has now amended Rule 10CB of the Rules vide notification dated 30 September 2019. A summary of the latest amendment is as follows.

Clarification on “excess money”

The above notification has replaced the words “excess money” with the words “excess money or part thereof” in Rule 10CB. This appears to be made pursuant to the amendment vide Finance (No.2) Act, 2019, which had introduced similar language in section 92CE of the Act.

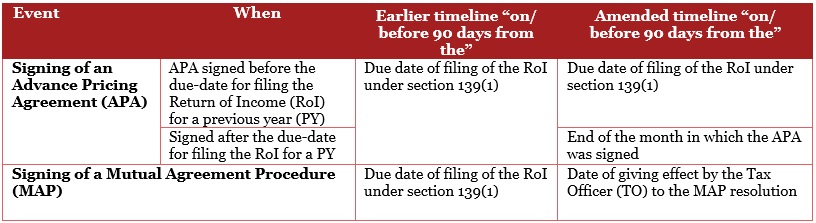

Time limit for determining the 90 days

The notification has amended the time limit for repatriation of money as follows:

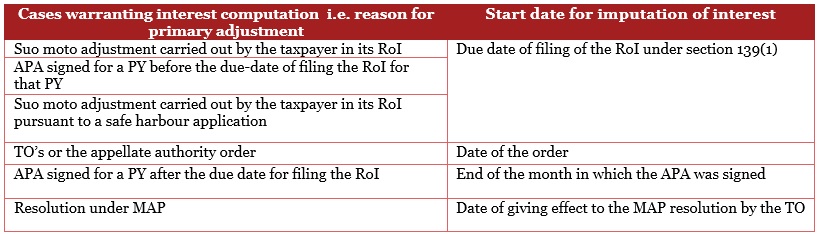

Start date for computing interest

The newly inserted sub-rule (3) to Rule 10CB of the Rules prescribes the start date that needs to be considered for computation of interest, in the absence of repatriation of such excess money or part thereof:

Clarification on rate of exchange

The newly inserted explanation to Rule 10CB provides that the rate of exchange for the calculation of amount of international transaction in foreign currency should be Telegraphic Transfer buying rate as on the last day of the PY.

PwC Comments: While the notification relaxes the timeline for repatriation of money in case of secondary adjustment on account of APA and MAP, it prescribes that in absence of repatriation within a timeline of 90 days, the interest shall be payable from day one, i.e., without considering the 90 days’ timeline available for repatriation of money. The notification has been issued at an opportune time considering that the due-date for filing is approaching fast and would provide the taxpayers with much needed clarity while adhering to the regulations.

Indirect Tax

GSTN issues advisory enabling online refund processing system, with disbursal by a single authority

The Goods and Services Tax Network (GSTN) has issued an advisory for the implementation of an online refund processing system on the GST portal, with disbursal by a single authority. The manual filing of refund applications through Form GST RFD 01A is being disabled.

The highlights of the newly implemented online refund processing system are listed below.

- The application processing and all communication relating to refund between the Tax Officers (TO) and the assessee will be online on the portal.

- The refund amount will be disbursed by an accredited bank of the Central Board of Indirect Taxes and Customs (CBIC) through the Public Financial Management System after validation of the assessee’s bank account.

- The assessee will receive communications on the progress of the refund over emails and SMSs.

- Input tax credit (ITC)/ cash shall be auto re-credited to the electronic credit ledger/ cash ledger if a deficiency memo is issued or the TO identifies an inadmissible ITC. The former scenario would require the filing of a fresh application.

- Form GST RFD 01A has been disabled on the portal. However, assessees shall be able to view the status of the refund claims filed previously in Form GST RFD 01A on the GST portal.

PwC Comments: The Government had introduced the manual filing of refund applications because of the non-availability of the online refund module on the GST portal. Thus so far, the State Governments as well as Central Government were involved in the process of disbursal of refund claims, which posed certain challenges. This revised model is a welcome move, considering the hardships that assessees encounter in obtaining disposal of refund claims within a reasonable time. Further, it is expected that the end-to-end online processing of refund applications would facilitate the Government’s policy objective of introducing online assessments. This step seeks to implement the objectives contained in the newly inserted section 54(8A) of the CGST Act, 2017, in line with the statutory amendments sought to be introduced in the Budget 2019-20.

Introduction of retrospective amendment to CGST Rules to specify the last date to avail ITC and imposition of credit restrictions where invoices are not uploaded in GSTR-1

The CGST Rules, 2017 (Rules) have been amended by notification no. 49/2019- CT dated 9 October 2019. The key amendments are as follows:

- Rule 61 of the Rules has been amended retrospectively with effect from 1 July 2017 to notify that the return furnished in Form GSTR-3B would be considered as a return specified in section 39(1) of the CGST Act, 2017 (Act). The assessee would not be required to file Form GSTR-3 where returns are required to be filed in Form GSTR-3B.

- Input tax credit (ITC) availed by a registered person on invoices that have not been uploaded by the supplier in its Form GSTR-1, shall be restricted to 20% of the eligible credit available in respect of the invoices that have been uploaded by a supplier in its Form GSTR-1.

- An amendment has been made to Rule 91 of the Rules to enable the Central Government to disburse refunds for claims made to both the Central and State Governments, under a consolidated payment advice, in case of provisional refunds.

- The due date for filing Form GST TRAN-1 has been extended to 31 December 2019 (previous due date being 31 March 2019). For Form GST TRAN-2 where an assessee is filing declaration in Form GST TRAN-1 in accordance with Rule 117(1A) of the Rules the due date has been extended to 31 January 2020 (previous due date being 30 April 2019).

PwC Comments:

- The amendment to Rule 61 of the Rules seeks to nullify a recent judgment of the Gujarat High Court by post facto notifying that Form GSTR-3B is the return required to be filed under section 39(1) of the Act. In the aforesaid judgement, the High Court had held that the Press Release dated 18 October 2018, clarified that the last date for availing ITC relating to invoices issued during July 2017 to March 2018 would be the last date for filing return in Form GSTR-3B for the month of September 2018 (later extended to March 2019), as invalid. This is because the High Court viewed Form GSTR-3B as an interim arrangement, which did not tantamount to a monthly return under section 39 of the Act, being Form GSTR-3.

- The implication was that the time limit of availing ITC for financial year 2017-18 would be pegged to the date of filing the annual return (i.e. 30 November 2019), and not the due date of filing Form GSTR-3B for September 2018, which was 20 October 2018 (later extended to 23 April 2019). The current amendment seeks to restate the potential entitlement of assessees to avail ITC in respect of any GST invoice issued in financial year 2017-18 until 23 April 2019.

- In addition, this amendment has been introduced retrospectively from 1 July 2017. Consequently, ITC unclaimed until 23 April 2019 but subsequently claimed based on the Gujarat High Court judgment, may now suffer challenges. It will be interesting to see if such a step to retroactively alter rights relating to ITC is challenged at a constitutional forum.

- Further, the amendment introducing the 20% limit on availing ITC on unreported invoices would add to the compliance burden and require monthly vendor invoice reconciliation. The assessee would have to ensure that availment of ITC on unreported invoices does not exceed 20% of eligible credit of the reported invoices.

Article

‘Compromise and Arrangements’ – An Avenue to revive a Corporate Debtor in a pending Liquidation Proceeding?

Introduction

Sections 230 to 232 of the Companies Act, 2013 (Act) provides for ‘Compromise and Arrangements.’ The said provision allows for compromise and arrangements between i) the company and its creditors or any class of them, ii) the company and its members or any class of them. With the implementation of the Insolvency and Bankruptcy Code (IBC) in 2016, a primary issue afflicting the minds of the companies was whether an application for ‘Compromise and Arrangement’ was allowed either between the company and the creditors or between the company and its members, whilst pendency of liquidation proceedings under IBC. This was settled by the National Company Law Tribunal (‘NCLAT’) by way of decisions in S.C. Sekaran v. Amit Gupta & Ors (Company Appeal (AT) (Insolvency) Nos. 495 & 496 of 2019) and Y. Shivram Prasad v. S. Dhanapal & Ors. (Company Appeal (AT) (Insolvency) No.224 of 2018). These two decisions directed the liquidators to first take steps under Section 230 of the Act. The Adjudicating Authority, if required, would pass an appropriate order. Only on failure of restoration, the Adjudicating Authority and the liquidator would first proceed with the sale of the company’s assets, and if not, sell the company in part and in accordance with the law.

Recently, another important question that came up for consideration related to implications of Section 29A of the IBC and the provisions relating to Compromise and Arrangements under the Act. Section 29A of the IBC provides for a list of persons who are ineligible to be a resolution applicant under the Act. The said list includes, a) an undischarged insolvent, b) wilful defaulter, c) a promoter who is in control of a corporate debtor and is classified as a non-performing asset, etc. Having said the above, the provisions under the Act do not provide for any class or list of members who are debarred from filing an application for Compromise and Arrangements. Thus, there arose some uncertainty as to whether individuals barred under Section 29A of the IBC could file an application for Compromise and Arrangements under Section 230 of the Act. The said ambiguity has now been settled by the NCLAT in its latest order dated 24th October 2019 passed in the case of Jindal Steel and Power Limited v. Arun Kumar Jagatramaka & Gujarat NRE Coke Ltd (Company Appeal (AT) No. 221 of 2018). This NCLAT judgement and its implications have been analysed in this article.

Facts and Issues Raised

Jindal Steel and Power Limited (Appellant) is an unsecured creditor of Gujarat NRE Coke Ltd., (corporate debtor) while Mr. Arun Kumar (1st Respondent) was its promoter. The 270-day period for acceptance and implementation of a resolution plan under the IBC had lapsed, thereby prompting liquidation of the corporate debtor by the National Company Law Tribunal, Kolkata. The said liquidation process was challenged by the 1st Respondent before the NCLAT. In the meanwhile, the 1st Respondent had filed an application for Compromise and Arrangement under Sections 230 – 232 of the Act before the National Company Law Tribunal, Kolkata. By virtue of order dated May 15, 2018, the Tribunal at Kolkata accepted the application for Compromise and Arrangement filed by the 1st Respondent. Thereafter, the Appellant had filed the present appeal against the order passed by the Tribunal at Kolkata and the following questions were framed for adjudication before the NCLAT:

- Whether in a liquidation proceeding under IBC, the scheme for Compromise and Arrangement can be made in terms of Sections 230 to 232 of the Act?

- If permissible, whether the promoter is “eligible” to file application for Compromise and Arrangement, (who is ineligible under Section 29A of the IBC), to submit a ‘Resolution Plan’?

Reasoning and Judgement of the Tribunal:

- The NCLAT held that applications under Section 230- 232 of the Act, are allowed in circumstances wherein the company is in a liquidation proceeding under the IBC. The Tribunal laid emphasis on the findings of their own decisions in C. Sekaran v. Amit Gupta & Ors (Company Appeal (AT) (Insolvency) Nos.495 & 496 of 2019) and Y. Shivram Prasad v. S. Dhanapal & Ors. (Company Appeal (AT) (Insolvency) No.224 of 2018). Both these orders drew their reasoning from the observations made by the Hon’ble Supreme Court in the landmark case of Swiss Ribbons Pvt. Ltd. & Anr. v. Union of India & Ors. ((2019) 4 SCC 17) wherein it was held:

“…..the primary focus of the legislation is to ensure revival and continuation of the corporate debtor by protecting the corporate debtor from its own management and from a corporate death by liquidation. The Code is thus a beneficial legislation which puts the corporate debtor back on its feet, not being a mere recovery legislation for creditors.”

- Similarly, the observations of the Hon’ble Supreme Court in the case of Meghal Homes Pvt. Ltd. v. Shree Niwas Girni K.K. Samiti & Ors. ((2007) 7 SCC 753) were also taken into consideration while adjudicating the said matter. The Hon’ble Supreme Court in the said case analysed Section 391 of the erstwhile Companies Act, 1956 (now Sections 230 to 232 of the Companies Act, 2013) and held:

“…..Section 391(1)(b) gives a right to the liquidator in the case of a company which is being wound up, to propose a compromise or arrangement with creditors and members indicating that the provision would apply even in a case where an order of winding up has been made and a liquidator had been appointed.”

- Thus, in the greater interest of the corporate debtor, an application for ‘Compromise and Arrangement’ under Sections 230 to 232 of the Act filed during the liquidation process under the IBC, is said to be maintainable.

- In so far as Issue (2) is concerned, the NCLAT cited the case of Shivram Prasad (Supra) which emphasised and reiterated the observations made by the Hon’ble Supreme Court in the Swiss Ribbons (Supra) wherein it was held that the “primary focus of the legislation is to ensure revival and continuation of the corporate debtor by protecting the corporate debtor from its own management and from a corporate death by liquidation”.

- Thus, NCLAT held that an individual barred by Section 29A of the IBC, is not eligible under Sections 230 to 232 of the Act, to file an application for ‘Compromise and Arrangement’. The order of the Tribunal at Kolkata which had allowed for such an application by the 1st Respondent was therefore quashed, since he was barred under Section 29A of the IBC to propose any resolution plan.

Takeaways and Highlights of the Judgement

- The judgement clears the air on the eligibility of promoters to regain control of the company through the ‘Compromise and Management’ route available under the Act.

- The judgement also clarifies that an application for ‘Compromise and Arrangement’ under the Act is allowed even during the pendency of liquidation proceedings under the IBC.

- Similarly, the judgement settles the law that any person barred under Section 29A of the IBC, is not eligible to file an application for ‘Compromise and Arrangement’ under Sections 230-232 of the Act.

Prashanth S Shivadass

Advocate and Founder,

Shivadass & Shivadass (Law Chambers)

From the Research Wing....

- The Chamber submitted a representation to the State Government on changes required in the Kerala Shops and Commercial Establishment Act, 1960.

- The Chamber submitted comments on the Draft Social Security Code 2019 circulated by the Ministry of Labour (Government of India).

- The Chamber submitted comments on The Occupational Safety, Health and Working Conditions Code, 2019 circulated by the Parliamentary Standing Committee on Labour.

Policy Development Corner

- The Union Cabinet approval for strategic disinvestment in five PSUs— Bharat Petroleum Corporation Limited, Shipping Corp of India, Container Corporation of India (Concor), THDCIL and NEEPCO.

| PSU | Nature of disinvestment |

| Bharat Petroleum Corporation Ltd. (BPCL) | a) disinvestment of Government of India shareholding of 53.29%

b) transfer of management control |

| Shipping Corporation of India Ltd. (SCI)

|

a) disinvestment of Government of India shareholding of 63.75%

b) transfer of management control |

| Container Corporation of India Ltd. (CONCOR)

|

a) disinvestment of Government of India shareholding of 30.8% (out of 54 8% equity presently held by the Government of India)

b) transfer of management control |

| Tehri Hydro Development Corporation India Limited (THDCIL)

|

a) disinvestment of Government of India shareholding of 74.23% in THDCIL

b) transfer of management control to an identified CPSE strategic buyer, namely, NTPC. |

| North Eastern Electric Power Corporation Limited (NEEPCO)

|

a) disinvestment of Government of India shareholding of 100% in NEEPCO

b) transfer of management control to an identified CPSE strategic buyer, namely, NTPC.

|

Click here for more details about the strategic disinvestment of CPSEs.

2. The Kerala Legislative Assembly approved the Kerala Metropolitan Transport Authority (KMTA) Bill 2018. This law, if implemented properly, will be a game changer in addressing the perpetual traffic problems in Kerala.

3. The Kerala Government issued new guidelines for promoting the ease of doing business at the local self-governance level. Help desks are to be established in villages to facilitate a hassle-free experience to prospective entrepreneurs .

4. The Ministry of Corporate Affairs has invited comments on the report of the Company Law Committee. Click here to read the Report. Submit your inputs to [email protected] by 25th November 2019.

5. Comments invited on Draft Consumer Protection (Mediation) Regulations, 2019. Submit inputs to [email protected] by 13th December 2019.

6. Important bills listed for introduction, discussion and passing in the Parliament (Winter Session -18th November to 13th December )

| Bill | Purpose |

| The Taxation Laws (Amendment) Bill, 2019 | To encourage fresh investment, stimulate growth, create fresh job opportunity in the economy, stabilize the Capital Market and increase inflow of money in to Capital market. |

| The Prohibition of Electronic Cigarettes (Production, Manufacture, Import, Export, Sale, Distribution, Storage and Advertisement) Bill, 2019. | To prohibit the production, manufacture, import, export, transport, sale, distribution, storage and advertisement of e-cigarettes and like devices, considering the highly addictive nature of nicotine safety concern of flavours in combination with nicotine and other psychoactive substances; risk of use of other psychoactive substances through these devices; initiation of nicotine or psychoactive substances by non-smokers, especially adolescents and youth, dual use of e-cigarettes and conventional cigarettes, scant scientific evidence for use of e-cigarettes as effective tobacco cessation aids; threat to country’s tobacco control efforts; hindrance in achieving the targets envisaged under Sustainable Development Goals, National Monitoring Framework for Prevention and Control of Non-communicable Diseases and National Health Policy, 2017. |

| The Companies (Second Amendment) Bill, 2019 | To move certain amendments in the Companies Act, 2013 to decriminalize the offences and facilitate ease of doing business and ease of living.

|

| The Competition (Amendment) Bill, 2019 | To carry out certain essential Structural changes in the Governing Structure of the CCI, changes to substantive provisions to address the needs for new age markets and to expend the activities of the Commission across India by opening Regional Offices. |

| The Insolvency and Bankruptcy (Second Amendment) Bill, 2019 | For including a Chapter a Cross Border Insolvency. |

| The Anti-Maritime Piracy Bill, 2019 | To enact domestic anti maritime piracy legislation in line with United Nations Convention on the Law of the Sea (UNCLOS) to provide the necessary legal frame work within country for prosecution of persons for piracy related crimes committed on high seas beyond the territorial jurisdiction of India. |

| The International Financial Services Centres Authority Bill, 2019 | To provide for the establishment of the International Financial Services Centre Authority to regulate and develop a market for financial services in International Financial Services Centres in India. |

| The Industrial Relations Code Bill, 2019 | To amalgamate the following laws: -1. The Trade Unions Act, 1926.2. The Industrial Employment (Standing Orders) Act, 1946.3. The Industrial Disputes Act, 1947

|

| The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2019 | The Bill seeks the amendment Section 7 of the MSMED Act, 2006. As per the existing provisions under this section, the micro, small and medium enterprises are defined on the basis of investment in plant and machinery. Proposed new criterion is based on annual turnover. Under the proposed definition, an enterprise will be defined as a micro enterprise if its annual turnover does not exceed Rs. 5 crore; as a small enterprise if its annual turnover is more than Rs. five crore rupees but does not exceed Rs 75 crore, and as a medium enterprise if the annual turnover is more than Rs. 75 crore but does not exceed Rs 250 crore. |

| The Recycling of Ships Bill, 2019 | To provide legal framework for implementation of Hong Kong convention |

Detailed tentative list of business available here

Letter to the Chief Minister of Kerala...

The Chamber has written to the Chief Minister of Kerala, requesting his attention with regard to a few issues in the latest Amendments on the “Kerala Shops and Establishments Act, 1960.” The letter sent to the Chief Minister is reproduced below for information.

Mr. Pinarayi Vijayan

Honourable Chief Minister

Government of Kerala

Trivandrum

Sir,

Subject: Amendments required in the Kerala Shops and Commercial Establishment Act, 1960

The Cochin Chamber of Commerce and Industry, established in the year 1857, has completed 162 years of service to the region’s commerce, industry and trade. This Chamber, one of the oldest in the country, is a Promoter Chamber of the Associated Chambers of Commerce and Industry of India (ASSOCHAM), New Delhi, the oldest national Chamber in the country. The activities of the Chamber have undergone several changes over the years in keeping with the changing times and needs so as to provide prompt and effective services to its membership and the business community at large. Since the very beginning, the Chamber has been involved in the advancement of several public causes in the State apart from its regular Chamber activities. History tells us that the setting up of the Cochin Port was a result of active inputs from the Cochin Chamber. In recent times the Chamber has also played a significant role in the conceptualization of the Cochin International Airport and promoting the idea in its early stages. Though we are a Chamber of Commerce in the traditional sense, we have always been looking out for ways to reinvent ourselves and make relevant contributions to the society that we live in.

We take this opportunity to appreciate the Government’s initiative in facilitating the ‘right to sit’ through its landmark The Kerala Shops and Commercial Establishments (Amendment) Act, 2018 passed on 5th December 2018 by the Kerala Legislative Assembly. The move was well appreciated by civil society organisations and the public at large. However, there are some issues relating to the Shops and Establishments policy framework that requires urgent attention and intervention:

1) Permission for 24*7 Shopping

Section 10(2) of the Kerala Shops and Commercial Establishment Act, 1960 permits the Government by general or special order, to fix the time at which any establishment or class of establishments shall be opened or closed in any local area.

The Tamil Nadu Government vide G.O (Ms).No. 60 dated 28th May 2019 permitted all Shops and Establishments to keep open their establishments open for 24/7 all days of the year for a period of three years with effect from the date of publication of the notification.

A similar notification under section 10(2) will help boost retail trade and our tourism potential.

2) Prescribing minimum number of employees for registration

In Kerala, all shops and commercial establishments have to be registered under the Act irrespective of the number of workers.

Recent amendments in states like Gujarat (Gujarat Shops and Establishments Regulation of Employment and Conditions of Service Act, 2019), Maharashtra (Maharashtra Shop and Establishment Regulation of Employment and Service Condition Act 2017), Tamil Nadu (Tamil Nadu Shops and Establishments Amendment Act, 2018) etc. have set 10 employees as the benchmark requiring the employer to seek license and registration under this Act.

The Kerala Government could consider providing relief to the establishments employing less than ten workers.

3) Renewal of registration

Section 5 A (5) of the Kerala Shops and Commercial Establishment Act, 1960 prescribes one year validity to the registration certificate granted under this Act requiring the employers to renew the certificate on a yearly basis.

States like Maharashtra amended their provisions to increase the period to ten years. The Odisha Government vide the Draft Odisha Shops and Commercial Establishments (Amendment) Rules, 2019 circulated on 13th June 2019 proposes to do away with the requirement to renew registration of shops and commercial establishments; registration will soon remain valid till revoked / furnishing of undertaking of closure.

Taking a cue from these developments, the Kerala Government should also consider increase the validity period of registration certificates to facilitate the ease of starting and doing business in Kerala.

The Chamber would be extremely pleased if the Government initiates a proper pre-legislative consultation for ideating and facilitating comprehensive changes to the Kerala Shops and Commercial Establishment Act, 1960. The process of consultation should be participatory so as to ensure the participation of relevant stakeholders including various trade, commerce, industry organisations and the public at large. These changes, if implemented properly, can facilitate and promote the Ease of doing Business in Kerala.

Thanking you and requesting your immediate and positive intervention in the matter.

Yours faithfully

V Venugopal

President

Forthcoming Events

12th CEO FORUM Breakfast Meeting

Joint Health & Safety - Maintenance and Preservation | 06.12.2019

The 12th Breakfast Meeting under the aegis of the Chamber’s CEO FORUM 2019 will be held on Friday, the 6th of December 2019 between 8.00 am and 10.00 am at the Taj Gateway Hotel, Marine Drive, Ernakulam.

Dr. Jacob Varughese, Head of Orthopaedic Department, VPS Lakeshore, Kochi will speak on “Joint Health & Safety – Maintenance and Preservation” and its Medical Tourism Potential for the State.

Joint preservation refers to the use of nonsurgical or surgical means to preserve a deteriorating joint in order to delay or avoid joint replacement surgery. The goal of preservation is to prevent injury, reduce inflammation and preserve cartilage. When it comes to maintaining your overall health and wellness, you may be surprised to figure out just how important your joints are when it comes to your total body wellness. This is even more true if you suffer from frequent bouts of acute back or joint pain or stiffness. If you experience chronic back pain or joint aches with no clear cause or reason, it is safe to say that poor joint health may be to blame. So what can you do to protect your joints and keep them healthy and working well?

Click on the Speaker profile to view the same.

Delegate Fee:

Member: Rs.1,500/- (incl. 18% GST)

Non-Member: Rs.1,750/- (incl. 18% GST)

Click here to register for the session.

CEO FORUM 2020 - 5th edition

03.01.2020

The 5th edition of the Cochin Chamber’s prestegious CEO FORUM Breakfast Meetings is set to commence on Friday the 3rd of January, 2020.

More details regarding this will be sent to you shortly.

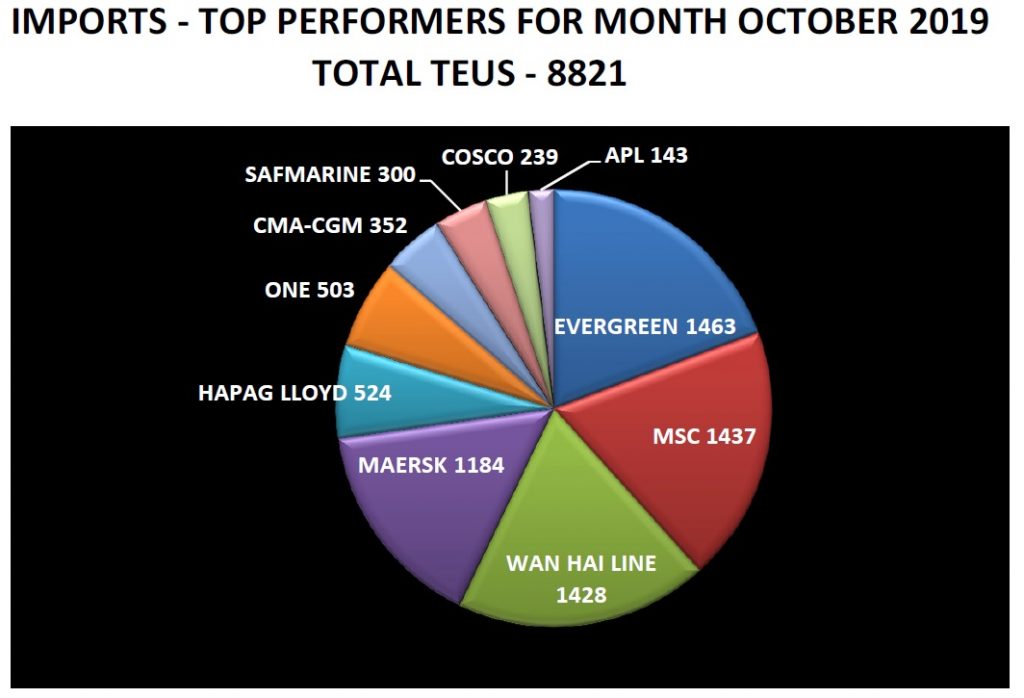

Exclusive EXIM Statistics

Statistical Reports on Exports and Imports through the Cochin Port.

The Cochin Chamber of Commerce and Industry publishes statistical reports on Exports and Imports through the Cochin Port on a monthly basis followed by a Consolidated Annual Report at the end of each calendar year. The reports on exports are classified as commodity wise and pertain to the following commodities:

- Coffee

- Tea

- Spices

- Cashews

- Cotton Goods

- Seafood and

- Coir and coir products

Details on all other commodities that do not fall under the above-mentioned heads are carried as the ‘Miscellaneous Report’. Customized reports will also be available according to customers requirement.

We have several members in the export/import fraternity subscribing to these reports on a monthly basis and from the feedback received they are immensely benefited by the same.

We are confident that our reports will be of help to your Company in staying one step ahead of your competitors in business. A sample of the report is attached herewith for your reference. Also attached is the ‘Subscription Form’ to enable you to subscribe to the report should you want to do so.

Should you have any queries please feel free to contact Ms. Archana (7025738447).

For more details, visit Export-Import Statistics

Sample Reports