President's Letter

Dear Friends,

February has been an eventful month for the Chamber!

We started the month with the CEO FORUM Breakfast Meeting on Friday the 1st of February.

The Guest Speaker at the meeting was Prof. Abraham Koshy, Professor – Marketing, Indian Institute of Management, Ahmedabad who spoke on the “Bonsai Management Syndrome.”

In his talk, Prof. Koshy spoke about thought leadership and administrative leadership and how the former is the new strategy for corporate growth. Corporations that embrace thought leadership as a strategy for growth represent the essence of market leadership and change the rules of client management. He also explained the term ‘Bonsai Manager’ as one whose growth has not reached its potential due to his/her own acts of omission and commission. Prof. Koshy explained in detail the growth requirements for a Company viz. data collection, innovation, exploration, and results. He emphasized the importance of thinking ‘out of the box’ and also suggested that it is important not to be burdened by past successes since an organization needs to explore new opportunities in order to overcome the bonsai syndrome.

The Annual Post Budget Analysis on the Union Budget 2019-2020 was held on the 4th of February. The Lecture was delivered by Mr. Homi P Ranina, eminent Lawyer and Tax Expert from Mumbai. The event went off very well and we had almost 180 participants including students and industry representatives attending.

In his address, Mr. Ranina said that the last budget of the present Government has sought to lay down the road map for transforming the Indian economy by ushering an era of digitization, the fruits of which will be reaped in the coming years. The main thrust of the budget proposals is to continue fiscal consolidation and restrict the fiscal deficit of 2018-19 to the level of 3.4% of the GDP, with a promise that in the next fiscal 2019-20, the attempt would be to retain it at 3.4%, despite disbursement of Rs.75,000 crore on direct benefit transfers to marginal farmers.

India needs to be made the manufacturing hub of the world and this finds its imprint on the budget proposals by encouraging the spirit of entrepreneurship among millions of Indians by providing credit facilities and training programmes to hone the skills of young entrepreneurs. A road map has been chalked out for enhancing investments in key sectors and passing on the benefit of the growth process to the common man.

The gist of Mr. Ranina’s talk is given in this issue of the Newsletter for your information.

I’m also happy to inform you that the Chamber successfully conducted the 2 day – ‘The Last Mile- Eligibility to Employability’ Certificate Workshop on the 15th and 16th of February. I would take this opportunity to thank you all and the Members of the Executive Committee of the Chamber for the support and co-operation received. I would also like to thank the Workshop Sponsors’ – The Eastern Group of Companies (Principal Sponsor) and the Associate Sponsors, The Federal Bank Ltd., and CMRL for their generous support to this endeavour of the Chamber.

The Workshop was aimed at equipping fresh graduates / students hone their skills to become employable and to take-up good jobs.

The programme commenced with an Inaugural Session at which Mr. S Venkatesh, Management Board Member and President, Group HR, RPG Enterprises, Mumbai delivered the Inaugural Address. This was followed by a Panel Discussion moderated by Mr. Mark Antony Sequeira, Master Trainer & CEO – Maestro HR Pvt. Ltd. Chennai, on ‘Careers 2020 and Beyond – Your Way Forward.’ Mr. S Venkatesh, Prof. Dr. Radha Thevannoor, Group Director – SCMS, Cochin and Mr. K Harikumar, Managing Director, Travancore Cochin Chemicals Ltd., were the other panel members.

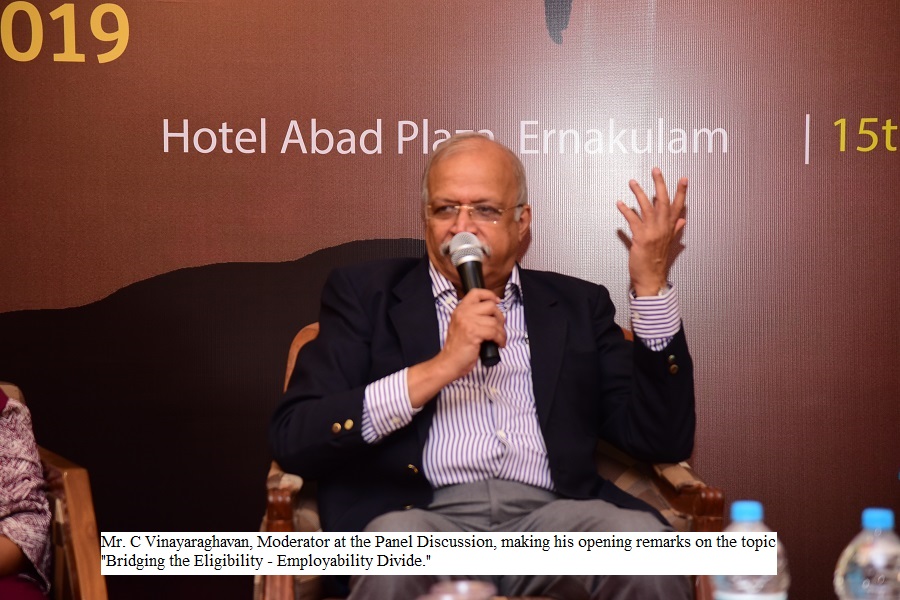

The second-day’s programme started off with a Panel Discussion on ‘Bridging the Eligibility Employability Divide.’ The Discussion was moderated by Mr. Vinayaraghavan, Former CEO, Harrisons Malayalam Limited. Mr. Vineeth P Mathew, DGM – HR & Training, Synthite Industries Pvt. Ltd., Ms. Rajasree R, HR Head, TCS, Kochi and Ms. Nisha Menon, Director, Tax – PwC India were the Panelists.

The session was attended by 80 students from 24 different educational institutions.

We propose to conduct this event annually henceforth.

On the 21st of February British Conservative MP Mr. Bob Blackman visited the Chamber to discuss business possibilities, especially in the field of health care and Ayurveda. He also spoke about Brexit, its pros and cons and the future of Great Britain.

Detailed reports on these events along with pictures are carried in this issue of Newsletter.

Friends, the next CEO Forum Breakfast Meeting will be held on the 1st of March 2019. Mr. Abraham Chacko, Former ED, Federal Bank Limited, Independent Director – Jana Holdings Ltd., will be the Speaker at the Session. He will speak on “Kerala and Singapore – A Similitude: The Way Forward”.

On the 15th of March we will be organizing a Workshop on “Marketing in the Age of IoT, AI, and Block Chain” at Hotel Abad Plaza, Ernakulam. The Speaker will be Mr. Arun James, Business Head – Outcome Infotech, Bangalore. The details of the programme are being sent to you separately.

The Cochin Chamber has more programmes and activities lined up for the coming months, details of which will be intimated to you in due course.

I trust that you will make use of these opportunities to the fullest.

Wishing you all the very best!

V Venugopal

Trivia

Quote

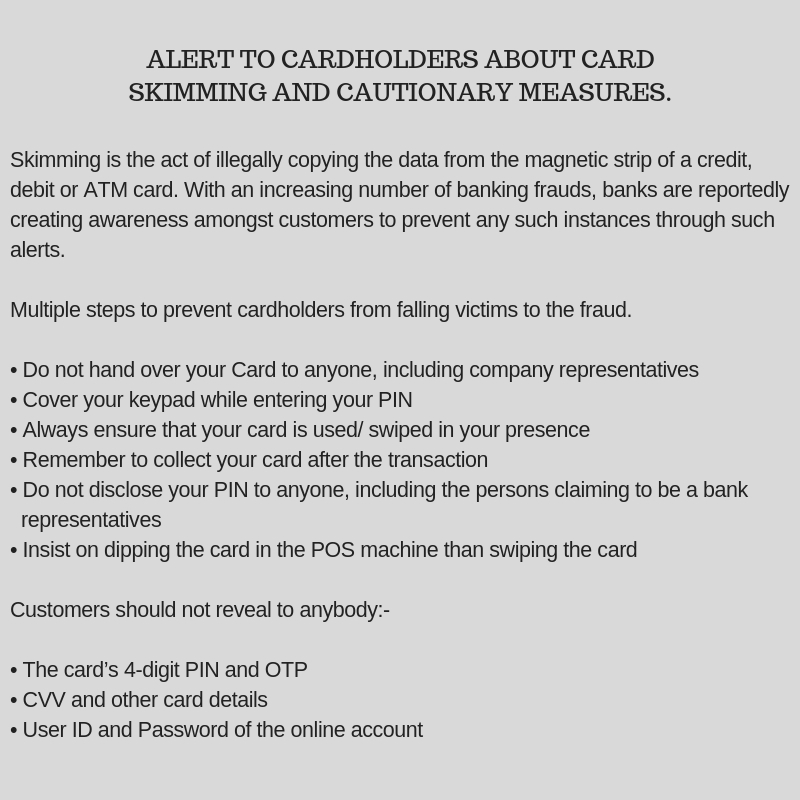

Alert to Cardholders

Recent Events

CEO FORUM 2019

Bonsai Management Syndrome | 01.02.2019

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s – 2nd Breakfast Meeting on Friday, 1st February 2019 at Taj Gateway Hotel, Ernakulam. The Guest Speaker at the meeting was Prof. Abraham Koshy, Professor – Marketing, Indian Institute of Management, Ahmedabad.

Calling the meeting to order, Mr. V Venugopal, President of the Chamber delivered the Welcome Address and introduced the Speaker of the day

Prof. Abraham Koshy’s talk was on the “Bonsai Management Syndrome.”

In his talk, Prof. Koshy spoke about thought leadership and administrative leadership and how the former is the new strategy for corporate growth. Corporations that embrace thought leadership as a strategy for growth represent the essence of market leadership and change the rules of client management. He also explained the term ‘Bonsai Manager’ as one whose growth has not reached its potential due to his/her own acts of omission and commission.

Prof. Koshy explained in detail the growth requirements for a Company viz. data collection, innovation, exploration, and results. He spoke on how data collection is a fundamental aspect for the growth of an organization and also the importance of having actual facts supporting a product’s success or failure rather than having mere opinions or expectations. He emphasized the importance of thinking ‘out of the box’ and also suggested that it is important not to be burdened by past successes since an organization needs to explore new opportunities in order to overcome the bonsai syndrome.

Prof. Koshy spoke about the control management of an organization and how micromanagement can damage efficiency. Controls should be goal oriented, he said. He specified the need for a shift from activity-based control to result-based control. He also explained the Pareto Principle, the 80/20 Rule and how 80% of the effects come from 20% of the causes.

Prof. Koshy shed some light on how an organization could identify the bonsai syndrome by measuring its growth over the years, from people development index and whether there is a spark of innovation.

Mr. Venugopal C Govind, Past President of the Chamber, presented a memento to Prof. Koshy.

Mr. K Harikumar, Vice President of the Chamber proposed the Vote of Thanks.

The interactive session concluded by 10 a.m with breakfast.

Annual Post Budget Analysis - 2019

04.02.2019

Gist of the speech delivered by Mr. H. P. Ranina, tax expert, at the Annual post Budget Analysis 2019

Mr. Piyush Goyal, the Finance Minister, had the unenviable task of framing his proposals in a difficult environment, both nationally and globally. The entire world economic order is facing the threat of lower growth, rising unemployment and unstable financial markets. India has also its share of worries despite the higher projected growth rate of 7.2% during the current financial year.

The last budget of the present Government lays down the road map for transforming the Indian economy by ushering an era of digitization, the fruits of which will be reaped in the coming years. The main thrust of his budget proposals is to continue fiscal consolidation and restrict the fiscal deficit of 2018-19 to the level of 3.4% of the GDP, with a promise that in the next fiscal 2019-20, he would attempt to retain it at 3.4%, despite disbursement of Rs.75,000 crore on direct benefit transfers to marginal farmers.

The vision of the Government to make India the manufacturing hub of the world finds its imprint on the budget proposals by encouraging the spirit of entrepreneurship among millions of Indians by providing credit facilities and training programmes to hone the skills of young entrepreneurs. A road map has been chalked out for enhancing investments in key sectors and passing on the benefit of the growth process to the common man.

For the first time, the Indian Government has made a serious attempt for providing social security coverage for workers in the unorganized sector. While these systems are in existence in all developed countries of the world, they were conspicuous by their absence in India. A pension scheme has been formulated whereby workers would be provided with pensionary benefits of Rs. 3,000 per month after reaching the age of 60.

The subsidy burden has been streamlined by overhauling the delivery system through direct transfer of cash benefits. This has been accomplished by using the banking system which has been made more inclusive as a result of Jan Dhan bank accounts being opened by almost 34 crore Indians who never had a bank account earlier. As a result, most of the international agencies had upgraded India’s economic growth potential and investor confidence has grown substantially in the last four years.

Initial steps are being taken to move towards the provision of basic universal income being guaranteed to the lowest level of Indian society. Small and marginal farmers who own cultivable land upto two hectares will be provided income support of Rs.6,000 per annum. The amount will be directly transferred into the bank accounts of beneficiary farmers. The total outlay on this programme is estimated at Rs.75,000 crore in a whole year. The Kisan Credit Card scheme is being extended to cover those who are involved in animal husbandry and in fisheries. They will also be given 2% interest subsidy on the loan availed through the scheme.

The Finance Minister has highlighted the fact that the banking sector has now been put on a stronger ground as a result of reforms being initiated, including the implementation of the Insolvency & Bankruptcy Code. An amount close to Rs.3 lakh crore has already been recovered by banks and creditors. The strategy of recognition, resolution, recapitalization and reforms has been successful. Public sector banks have been recapitalized to the extent of Rs.2.6 lakh crore. Amalgamation of banks have brought the benefits of economies of scale and improved access to capital which would reduce dependence on budgetary funding.

To sustain the basic needs of the common man, Rs.1,70,000 crore was spent in the current financial year to provide food grains at affordable prices. About 2.5 crore families have now been provided free electricity connections. The universal healthcare programme, Ayushman Bharat, will provide medical treatment to as many as 50 crore citizens.

To empower youth and promote self-employment opportunities, 15.56 crore loan applications have been sanctioned and Rs.7,23,000 crore have been disbursed. With job seekers becoming job creators, India has become the world’s second largest start-up hub. To help the small scale sector, loans are being sanctioned upto Rs.1 crore in the shortest possible time, and those units which are registered for the Goods & Services Tax will get a 2% interest rebate.

India is now leading the world in the consumption of mobile data which has increased by over fifty times in the last five years. The number of companies manufacturing mobiles and components has increased from 2 to 268. About 3 lakh common service centres employing around 12 lakh people are digitally delivering different types of services to citizens who are not computer literate. There is a proposal to make one lakh villages into digital villages over the next five years.

On the direct tax front, the Finance Minister has announced that persons having taxable income upto Rs.5 lakhs per annum will not have to pay tax because they will get a tax rebate under section 87-A of the Income-tax Act, 1961 upto a maximum of Rs.12,500. However, this benefit will not be available to those tax payers whose taxable income exceeds Rs.5 lakhs per annum.

Standard deduction for salaried employees has been increased by 25% from Rs.40,000 to Rs.50,000. The notional income in respect of self-occupied property is proposed to be exempted from the financial year 2019-20 to the extent of two self-occupied houses, instead of one at present.

For those who make taxable capital gains upto Rs.2 crore in a financial year, they will now be permitted to roll over these capital gains in two residential properties, if they so wish, to avail of the exemption under section 54. Upto the current financial year ending on 31st March, 2019, it was mandatory to invest the taxable capital gains only in one residential house. The new provision will help families who may want to have two houses by selling one, giving a boost to the real estate sector which currently has a large stock of unsold residential units.

Developers will also not have to pay tax for two years, instead of one year at present, if they hold on to unsold properties. Those builders who are undertaking affordable housing schemes will now get the benefit of tax exemption under section 80-IBA if their project is approved by 31st March, 2020.

For the fixed income earners, interest on bank deposits is currently exempt under section 80-TTA upto Rs.10,000. This is proposed to be increased to Rs.40,000 with effect from the financial year 2019-20. Where a person has rented out his property, he will not have to suffer deduction of tax at source so long as his rental income does not exceed Rs.2,40,000 per annum from the financial year 2019-20; currently, the exemption from withholding tax is given where the rental income is Rs.1,80,000 per annum or less.

Within the next two years, the Income tax Department will be totally digitized and all functions will become online. All returns will be processed in 24 hours from the time of filing and refunds will be issued simultaneously. All verification and assessment of returns selected for scrutiny will be done electronically in back offices without any personal interface between tax payers and tax officers. The number of tax returns filed during 2018-19 has gone up from 3.79 crore to 6.85 crore, resulting in substantial increase in tax collections. Almost 99.5% of income tax returns have been accepted by the tax department under the summary assessment scheme.

Some critics have called this an election budget. However, the voter is not going to be swayed by the sops which have been announced in the interim budget. What may weigh with the voters is the track record of this Government. Inflation has been down from 10.1% to 4.6% which is a creditable achievement. More than 15 lakh rural houses have been connected by all-weather roads.

Subsidized housing has been provided to 1.5 crore families. New electricity connections have been given to 2.5 crore families, and 6 crore LPG connections have been provided in rural homes. Around 19 crore families are eligible for subsidized life and accident insurance cover.

The Finance Minister has, at the end of his speech, set out the Vision of the Government for the decade ending 2030. The first dimension of this Vision is to complete the construction of the physical and social infrastructure of roads, railways, ports, inland waterways, urban transportation, hospitals and schools. The second Vision is to digitize the entire economy and create millions of jobs in the emerging ecosystem. The third limb is to make the Nation pollution free by ensuring use of electric vehicles, energy storage devices and solar energy.

Rural industrialization which would generate massive employment in smaller cities and towns is the fourth pillar of the Vision, whereby global manufacturing hubs will be set up in various sectors, including automobiles and electronics. The fifth and sixth limbs of the Vision are to provide safe drinking water to all Indians and clean up the rivers. Developing inland waterways will enhance the income potential of millions of citizens residing along the river banks as it is in advanced countries like Germany.

The seventh dimension of the Vision is to develop space programmes and to become the launch-pad for satellites which would be used by many countries of the world. The next Vision is to enhance farm productivity through modern agricultural practices and value addition and formulate an integrated approach for agro and food processing, packaging and maintenance of cold chains.

The ninth dimension is to create and support a robust health infrastructure and provide insurance coverage to all citizens. The ultimate goal of the Vision is to transform India into a minimum government, maximum governance Nation having a bureaucracy which is proactive, reform oriented and accountable to citizens.

If the broad parameters of this Vision are fulfilled by 2030, the full potential of the Indian economy will be realized, laying the foundation for India’s next phase of growth and development. While the Indian economy will grow from a 2.7 trillion dollar economy at present to a 5 trillion dollar economy by 2023, some international institutions have projected that by 2030 the Indian economy will be the second largest in the world after China, based on the purchasing power parity method of calculating the comparable size of economies.

The budget has been structured to meet the aspirations of most sections of society. Marginal farmers, unorganized sector workers and middle class families have been given benefits and incentives which were long overdue. Despite this being an interim budget, it lays the foundation for a full fledged programme to be implemented after the elections.

Most of the infrastructure projects will come to fruition and see the light of the day by 2023. This will lay the foundation for exponential growth which only China had achieved during the past decade. There is no doubt that India’s time has come to be in the league of the most advanced economies of the world, having surpassed even today both England and France.

The Last Mile - 2019

Eligibility 2 Employability | 15th & 16th February, 2019

Day-1

The Cochin Chamber of Commerce and Industry conducted a two-day Certificate Workshop ‘The Last Mile – Eligibility to Employability’ for ‘students’ on the 15th and 16th February 2019 at Hotel Abad Plaza, Ernakulam.

The Workshop was aimed at equipping fresh graduates / students hone their skills to become employable and to take-up good jobs.

Mr. V Venugopal, President of the Chamber delivered the Welcome Address.

The programme commenced with an Inaugural Session at which Mr. S Venkatesh, Management Board Member and President, Group HR, RPG Enterprises, Mumbai delivered the Inaugural Address. The Inaugural Session was followed by a Panel Discussion moderated by Mr. Mark Antony Sequeira, Master Trainer & CEO – Maestro HR Pvt. Ltd. Chennai, on ‘Careers 2020 and Beyond – Your Way Forward.’ Mr. S Venkatesh, Prof. Dr. Radha Thevannoor, Group Director – SCMS, Cochin and Mr. K Harikumar, Managing Director, Travancore Cochin Chemicals Ltd., the other panel members, shared their views on the rapidly evolving job landscape, the skills one needs to possess in order to succeed in the coming years and also how the push for entrepreneurship through schemes like Start-Up India is beginning to positively impact jobs and opportunities.

Mr. V Venugopal, President of the Chamber, Mr. C S Kartha, Past President of the Chamber, Ms. Vinodini Issac, Executive Committee Member, presented the Mementos to the Speakers.

The training sessions commenced with an assessment test to evaluate the students’ skills in timing, persuasion, analysis, and problem-solving. Later the students were divided into various teams and were given various scenarios to discuss and reach a logical conclusion and to present them. Mock interviews were conducted to help the students understand what is expected in a real job interview and to help them improve themselves.

Day-2

The second-day’s programme started off with a Panel Discussion on ‘Bridging the Eligibility Employability Divide.’ The Discussion was moderated by Mr. Vinayaraghavan, Former CEO, Harrisons Malayalam Limited. Mr. Vineeth P Mathew, DGM – HR & Training, Synthite Industries Pvt. Ltd., Ms. Rajasree R, HR Head, TCS, Kochi and Ms. Nisha Menon, Director, Tax – PwC India were the Panelists. They shared their views on how one needs to keep pace with next-generation technology skills, bridging the digital skill gap and how soft business skills like creativity, decision – making, interpersonal skills, leadership skills and time management will always be in high demand.

Following the Panel Discussion Mementos were presented to the Speakers.

The Student teams were given various activities to enhance their skills by completing the tasks assigned in the most efficient and effective way. Group Discussions were conducted, on various topics, to help the students improve their thinking process, communication skills, personality traits and the skills needed to contribute effectively to the goal accomplishment process. The students were evaluated on the basis of their communication skills, knowledge, listening skills etc.

Certificates of merit were awarded to the students who performed their best in the Mock Interviews and Group Discussions and also to the Best Team. Participation certificates were given to all students who attended the two day programme.

Mr. C.S Kartha, Past President of the Chamber, proposed the Vote of Thanks.

The session, attended by 80 students from 24 different educational institutions concluded by 6:30 p.m with a team photo shoot.

Visit of the British MP Mr. Bob Blackman to the Cochin Chamber

21.02.2019

The Cochin Chamber of Commerce and Industry hosted Conservative British Member of Parliament Mr. Robert (Bob) Blackman on the 21st of February, 2019 in the Chamber Conference Hall, Willingdon Island.

Mr. V Venugopal, President of the Chamber welcomed Mr. Blackman to the Chamber.

Mr. Blackman said that the purpose of his visit was to discuss business possibilities, especially in the field of health care and Ayurveda. Brexit and its possible fallout was also part of the discussions.

Mr. Blackman explained the reasons for Britain wanting to leave the European Union and the benefits that will accrue after Brexit. He said that 17.4 million people had voted to leave the Union in a referendum conducted in 2016. According to the Lisbon treaty, both the sides will get two years to agree to the terms of the split. He also mentioned the fact that the process was started in 2017 and Britain is scheduled to leave on 29th March 2019 regardless of whether there is a deal with the Union or not. He also said that the UK will be free to conduct trade all around the world, after Brexit, which will be advantageous for them.

Mr. Blackman agreed with suggestions made that the UK visa and immigration policies needed to be liberalised and promised to take up the issue with the British Foreign Office on his return to the UK.

Mr. V Venugopal, President of the Chamber presented a Memento to Mr. Blackman and thanked him for his visit.

Mr. Blackman was accompanied by his wife Nicole Blackman.

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

Deduction under section 80-IC on profits of an eligible undertaking to be computed ignoring losses of other eligible undertakings

Recently, the Chandigarh bench of the Income-tax Appellate Tribunal (Tribunal) has inter alia held that deduction under section 80-IC of the Income-tax Act, 1961 (the Act) is allowed with respect to the profits earned by the taxpayer from “eligible undertakings” without setting off the losses from other eligible undertakings. This is held in view of the provisions under section 80-IC(7) of the Act being “undertaking-specific”, unlike section 80-IA(5) of the Act, which is “business-specific.”.

PwC comments: There are plethora of judgements (both favorable and unfavorable) on the issue relating to computation of deduction under Part C of Chapter VIA of the Act. In the present ruling, the Tribunal has done a threadbare analysis of the provisions of sections 80AB, 80HHC, 80-IA(5) and 80-IC(7) of the Act. The Tribunal has observed that while section 80-IA(5) includes all “eligible undertakings” carrying out “eligible business”, the term “business” is to be substituted with “undertaking” for the purpose of section 80-IC(7) of the Act. This is a welcome ruling as the profits and losses of each undertaking should be considered separately without clubbing for computing the deduction under section 80-IC of the Act.

TO cannot reject the method of valuation of shares adopted by the taxpayer for purposes of section 56(2)(vii b) but can look into the reasonableness of data used

In a recent ruling, the Bangalore bench of the Income-tax Appellate Tribunal (Tribunal) held that while determining the fair market value (FMV) of shares under section 56(2)(viib) of the Income-tax Act, 1961 (the Act) read with Rule 11UA of the Income-tax Rules, 1962 (the Rules), the taxpayer is responsible for substantiating the reasonableness of the projections used for the discounted cash flow (DCF) method. Further, the Tax Officer (TO) can scrutinize the valuation report and opt for a fresh valuation. However, it was clarified that the valuation should be as per the methodology opted by the taxpayer.

PwC comments: The valuation as per the DCF method involves the estimation of multiple variables, which can change based on assumptions. Hence, taxpayers need to maintain documentation to substantiate the reliability of the estimates considered in valuation as per the DCF method.

While the Tribunal has clarified that the tax authorities cannot change the method of valuation adopted by the taxpayer, it has also considered that the tax authorities have the right to question the projections used in the valuation.

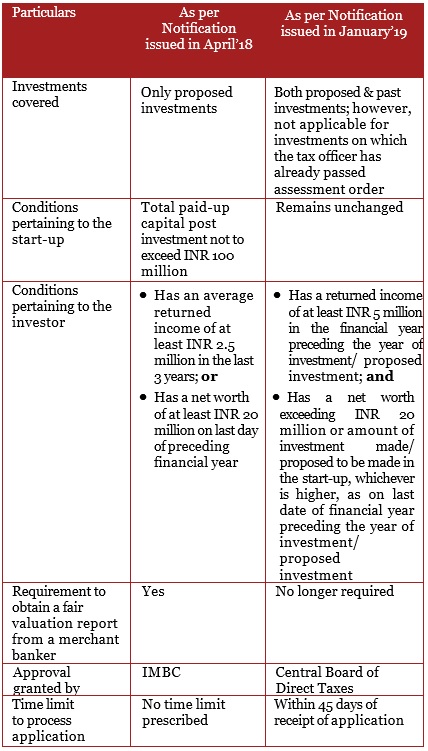

Government amends procedure for seeking exemption from section 56(2) (viib) for start-ups

Section 56(2) (vii b) of the Income-tax Act, 1961 (the Act) is applicable in case of issue of shares at a premium by a company in which the public are not substantially interested. The excess of share issue price over the fair market value of such shares, computed in accordance with prescribed methodology, is subject to income-tax.

The section further provides for specific carve-outs, which include class or classes of persons as may be notified by the Central Government. In 2016, the Government notified start-ups to be exempted from the applicability of provisions of section 56(2) (vii b) of the Act if such start-ups are recognized by the Inter-Ministerial Board of Certification (IMBC) under the Department of Industrial Policy and Promotion as eligible for such exemption.

On 11 April, 2018 the Government issued a notification[1] to provide for a procedure to grant exemption to registered start-ups. To make such a procedure more attractive and time bound, the Government issued another notification on 16 January, 2019. The amendments to the procedure are as follows:

DIPP Notification No. G.S.R. 364(E) dated 11 April, 2018

An entity is considered a start-up if –

- In existence, for up to 7 years (up to 10 years for those in the biotechnology sector);

- Turnover is less than INR 250 million; and

- Is involved in innovation/development/ improvement of products or processes or services or with high potential of employment/ wealth generation, subject to the entity not being formed by splitting up or reconstruction

Regulatory

Changes to the ECB Framework

As a part of the monetary policy announcement in December 2018, the Reserve Bank of India (RBI) indicated rationalization and consolidation of all borrowing and lending guidelines applicable to cross border transactions. The RBI notified revised regulations and has now issued a circular explaining the revised framework for External Commercial Borrowings (ECB) and rupee (INR) denominated bonds.

Some of the key highlights of the new ECB framework are as follows:

- 4-tier structure (Track I, II, III, and INR denominated bonds) replaced with two-tier structure (Foreign Currency loans and INR loans).

Tracks I and II under the existing framework are merged as “Foreign Currency (FCY) denominated ECB”. Track III and INR denominated bonds frameworks are combined as “INR denominated ECB

- List of eligible borrowers and eligible lenders have been significantly expanded.

- Borrowers: All entities eligible to receive Foreign Direct Investment (FDI) can borrow under the ECB framework ·The list of eligible borrowers shall include the following:

- Registered entities engaged in micro-finance activities, viz., registered not for profit companies, registered societies/ trusts/ cooperatives and Non-Government Organizations (permitted only to raise INR ECB).

- Port Trusts, units in SEZ, SIDBI, EXIM Bank.

Further, the term “Indian Entity” is defined under FEMA 3(R) to mean a company incorporated in India or a Limited Liability Partnership (LLP) formed and registered in India.

- Lenders:

- All lenders (including in case of transfer of ECBs) should be resident of Financial Action Task Force (FATF) or International Organization of Securities Commissions (IOSCO) compliant country. Multilateral and Regional Financial Institutions, where India is a member, also eligible.

- Individuals are eligible only in following cases –

In their capacity as foreign equity holders to the borrower;

or

- If they are subscriber to bonds/ debentures listed

- Foreign branches/ subsidiaries of Indian banks –

- FCY ECB – Permissible (except FCY convertible bonds and FCY exchangeable bonds);

- INR ECB – Permissible to only participate as arrangers/ underwriters/ market-makers/ traders for INR denominated bonds issued overseas

(Underwriting for issuances by Indian banks not permitted)

- De-linking of Minimum Average Maturity Period (MAMP) from ECB Amount

- ECB raised by manufacturing companies (up to US$ 50 million per financial year) – One year;

- ECB from foreign equity holder (for working capital purposes, general corporate purposes or repayment of INR loans) – Five years;

- Others – Three years.

The call and put option, if any, shall be exercisable only after completion of minimum average maturity

- Late Submission Fees (LSF) introduced.

Non-payment of LSF will be treated as contravention of reporting provision and shall be subject to compounding

Sector-wise borrowing limits consolidated into a single threshold.

A single borrowing limit of US$ 750 million or equivalent per financial year has been set under the automatic route.

PwC Comments: Expansion of list of ECB borrowers to cover all entities eligible to receive FDI (including LLPs in eligible sectors) and expansion of list of ECB lenders to cover all entities that are resident of IOSCO and FATF compliant jurisdictions are significant steps towards liberalization of the ECB framework. This liberalization should give a further boost to the RBI and Government’s efforts towards attracting capital inflows into the economy.

Indirect Tax

CBIC issues notifications and orders to give effect to the decisions taken in 31st GST Council meeting and issues clarificatory circulars

The Central Board of Indirect Taxes and Customs (CBIC) has issued various notifications and orders to give effect to the decisions taken at the 31st GST Council meeting. CBIC also issued multiple circulars to clarify various issues. The gist of the developments are as follows –Amendments introduced through ‘removal of difficulty’ orders

- Extension in the due date for availing input tax credit (ITC) in respect of any invoice, where supply has been made during financial year 2017-18 and the details of which have been uploaded by the supplier (by March, 2019), has been extended to the due date for furnishing the monthly return for the month of March, 2019. Further, suppliers are also allowed to rectify any error or omission in respect of details of outward supply disclosed earlier till the date of submission of return for the month of March, 2019.

- Extension of due date for submission of annual return and reconciliation statement along with GST audit report to 30 June, 2019.

Amendments which do not impact rate of tax

- Extension of the due date for submission of Form GSTR 3B for the period July, 2017 to February, 2019 for newly migrated assessees to 31 March, 2019. Further, the due date for submission of Form GSTR 1 for the (6) quarters July, 2017 to December, 2018 and for the (20) months July, 2017 to February, 2019 for such newly migrated assessees will be 31 March, 2019

- The key amendments to the GST Rules are as under:

- A person who is required to collect tax in a State, where it does not have a physical presence, can obtain registration in that State by mentioning the details of its principal place of business located in another state.

- Withdrawal of the requirement of disclosure of challans in Form GST ITC 04, in case of the goods sent from one job worker to another.

- Removal of the requirement of affixing signature or digital signature on invoice or a bill of supply or consolidated invoice or any other document issued by an insurer or a banking company or financial institution, including non-banking financial companies or ticket issued by a passenger transport company, if the respective document is issued in accordance with the provisions of the Information Technology Act, 2000.

- For claiming refund of accumulated credit in case of inverted duty structure, the term ‘relevant period’ has been defined to mean the same as for refund claim of accumulated credit by exporters, i.e. the period for which the claim has been filed.

- A new rule has been inserted to bar a person who has not filed returns for two consecutive periods from generation of e-way This rule will be effective from a date yet to be notified.

- Forms GST RFD-01 (refund application), GST RFD-01A (refund application), GSTR9 (annual return) and GSTR 9A (annual return) and GSTR 9C (reconciliation statement and GST audit report) have been substituted with revised formats.

- For the persons who have not submitted Form GSTR 1 (return for outward supplies) for the periods July, 2017 to September, 2018 who now submit Form GSTR 1 for these periods, between 22 December, 2018 to 31 March, 2019, the late fee payable for such delay is waived.

- For delayed submission of Form GSTR 3B (periodical return) from the month of July, 2017 onwards, the late fee which is in excess of INR 25 per day (under CGST Act, 2017) has been waived. In case, Central GST payable under the return is nil, the late fee in excess of INR 10 per day (under Central GST Act, 2017) has been waived. Further, in cases where the returns in Form GSTR 3B for the period July, 2017 to September, 2018 has not been filed and is filed between 22 December, 2018 and 31 March, 2019 the late fee will be completely waived.

- For the persons who have not submitted Form GSTR 4 (return for composition dealers) for the periods July, 2017 to September, 2018 and submit Form GSTR 1 for these periods between 22 December, 2018 to 31 March, 2019 the late fee payable for such delay is waived.

- The due date for submission of Form ITC 04 (return for movement of goods to/ from job worker) for the period July, 2017 to December, 2018 has been extended to 31 March, 2019.

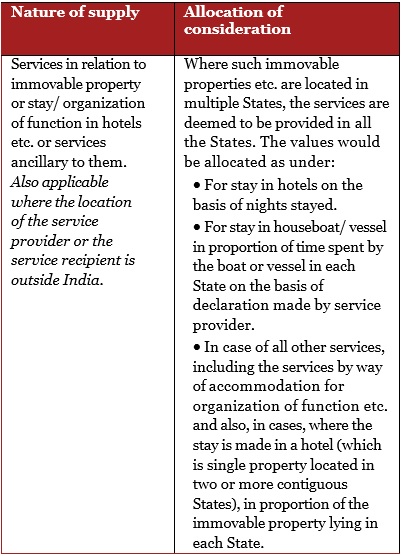

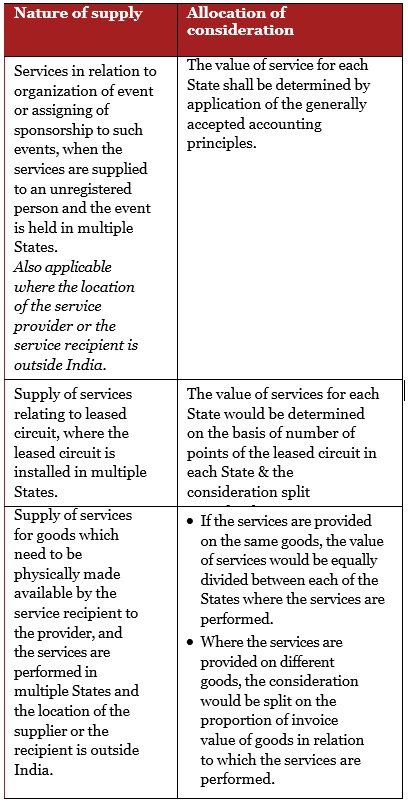

- The Integrated GST Rules, 2017 have been amended. The major amendments are as under:

- In case of advertisements over internet, the rules have been amended to provide a deeming fiction that such services are provided all over India.

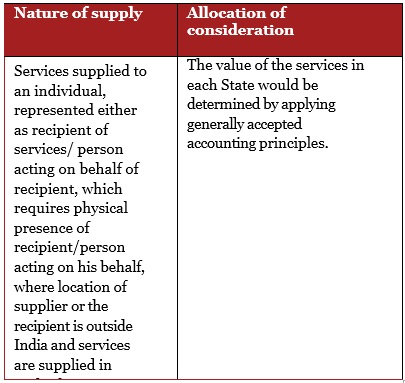

- The value of supply of service attributable to different States, when the services are supplied/ performed in multiple States and a consolidated consideration is charged, any break up for services supplied in an individual State, will be as under:

Circulars issued, clarifying various issues

- A circular is issued, providing various topical clarifications as under:

– Penalty under section 73(11) of the Central GST Act, 2017 is not applicable in case of delayed filing of Form GSTR 3B returns as such penalty pertains to non-payment of tax. However, penalty for delayed payment of tax under section 125 of the Central GST Act, 2017 is applicable.

- In case of revision of prices, after the appointed date, of any goods or services supplied before the appointed day, which requires issuance of any supplementary invoice, debit note, credit note, the rate as per the provisions of the Central GST Act, 2017 will be applicable.

- The provisions of tax deduction at source under section 51 of the Central GST Act, 2017 are applicable only to such authority or board or any other body set up by an Act of Parliament or a State legislature or established by any Government in which 51% or more participation by way of equity or control is with the Government.

- Taxable value for the purposes of GST shall include the amount of tax collected at source (TCS) under the provisions of the Income-tax Act, 1961 since the value to be paid to the supplier by the buyer is inclusive of the TCS.

- A circular is issued providing clarification on export of services in cases, where a service exporter has outsourced portion of the service contract to a person outside India. It has been clarified that:

– In such case, two supplies take place; one from Indian service exporter to the end client, and another from outsourced service provider to Indian service exporter.

- The Indian service exporter will be required to pay GST under reverse charge on services received from the outsourced service

- If the full consideration for the services as per the contract is not received in convertible foreign exchange where the end client directly pays the outsourced service provider, even that portion of the consideration would be treated as receipt for exports if Reserve Bank of India has permitted retention of part of consideration outside India and the Indian service exporter has paid Integrated GST on consideration paid to outsourced service provider under reverse charge.

- A circular is issued providing clarification on various issues relating to refund. The major clarifications are as under:

– While submitting the refund application, it was previously required that the copy of the refund application and the supporting documents were required to be physically submitted to the jurisdictional tax officer. Now such documents can be uploaded on the common portal.

- In case of refund of accumulated credit due to an inverted duty structure, the refund would be granted irrespective of applicable tax rates on the various inputs (whether higher or lower or equal to the rate applicable on output supply).

- The assessee to get interest on delayed refund on the refund amount immediately starting from the date after expiry of 60 days from the date of receipt of application (ARN) till refund has been actually credited to the bank account of the claimant

- Where the refund application has been electronically submitted and the ARN is generated on the common portal before the issuance of this circular but the application has not been received by the jurisdictional office (except refund of excess balance in electronic cash ledger), the refund claims of less than INR 1,000 should be rejected and the amount re-credited to the electronic credit ledger. In case of refund claims for amounts more than INR 1,000 the claimant should be sent an electronic mail communication to submit the application to the jurisdictional office within 15 days of receipt of the mail, failing which, the refund application would be dismissed and the amount debited would be re-credited to the credit ledger. In case of refund applications of excess balance in electronic cash ledger, the amount debited in the electronic cash ledger may be re-credited if there are no liabilities in electronic liability register. The amount should be re-credited, even though the return in Form GSTR 3B for the relevant period has not been filed

- The credit of an invoice for previous period, which is claimed in subsequent period, should be considered for the purpose of computing eligible refund for the period for which such credit has been

- The credit of any inputs used in the business and for making taxable (including zero rated) supplies should be considered as net ITC for refund, and ITC claimed as inputs on items such as stores and spares (including charged off to revenue and not capitalized), packing materials, material purchased for machinery repairs, printing and stationery items should be considered for refund if such credit is otherwise eligible.

- The refund of tax paid on input services and capital goods would not be available in case of claim of refund of accumulated credit due to inverted duty structure

- A circular is issued, clarifying the applicable rate of tax and classification of various goods. One of salient clarifications was that any inter-State movement of goods for provision of service on own account by a service provider, where neither transfer of title in such goods nor transfer to a distinct person is involved, does not constitute a supply of such goods and it is clarified that any movement on own account would not be liable to GST.

- A circular is issued, clarifying the issues arising from Central GST (Amendment) Act, 2018 on section 140(1) of the Central GST Act, 2017 dealing with carry forward of credit balances. The clarifications are as under:

- The closing balance of CENVAT credit pertaining to service tax can be carried forward as legislative intent was not to disallow service tax as transition CENVAT credit

- The expression “eligible duties” under section 140(1) of the Central GST Act, 2017 does not refer to the condition regarding goods in stock or to a condition regarding inputs and input services in transit. It has also been decided not to notify clauses 28(b)(i) and 28(c)(i) of the Central GST (Amendment) Act, 2018 (dealing with linking carry forward of closing balance of credits as per returns with various conditions) to avoid such linkage

- The eligible duties which are allowed to be carried forward under section 140(1) of the Central GST Act, 2017 would only cover the duties listed as eligible duties in sr. nos. 1 to 7 of explanation 1 to section 140 of the Central GST Act, 2017 and eligible duties and taxes as listed in sr. nos. 1 to 8 of explanation 2 to section 140 of the Central GST Act, 2017

- No transition credit of cesses, including cess collected as additional duty of customs under section 3(1) of the Customs Tariff Act, 1975 will be allowed

PwC Comments: The Council had issued a number of amendments, some of which, were not announced at the time of the 31st GST Council meeting. The amendment in Integrated GST Rules, determining the place of supply where a service straddles multiple States is prospective in nature and it would be interesting to see the approach adopted by the authorities for the past period. The further simplification of refund procedures, doing away with physical submission of application and various supporting documents is welcome, and will lead to reduction in procedural aspects. Parties claiming refund of compensation cess as exporters will need to review the classifications and their impact on past claims which are still unprocessed. Further, the clarifications regarding carry forward of CENVAT credit of service tax etc. clear the apprehension of the industry regarding potential challenge to carry forward of service tax credits etc. on the basis of language as drafted. However, the clarification prohibiting the carry forward of the credit of the cesses may see judicial challenge from the industry.

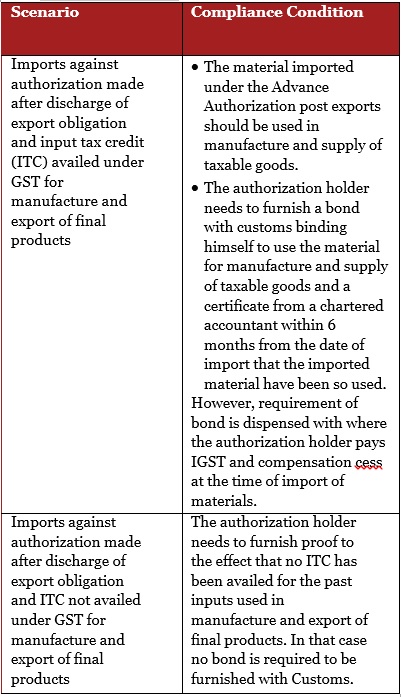

Sector Government removes the pre-import condition for Advance Authorization, extends exemptions of IGST and compensation cess for specified deemed exports.

Earlier, no integrated GST (IGST) and compensation cess exemptions were available for imports under advance authorization for deemed exports. However, these elements of customs duties were exempt for imports under advance authorization for physical exports, subject to the pre-import condition.

Pre-import condition contemplated that raw material imported under advance authorization is physically incorporated in the final products manufactured in India, which is then exported. Thus, disputes were raised in cases where the authorization holder imported raw material after exporting the final products.

To address the issue of ‘pre-import’ and provide impetus to ‘deemed export’ supplies, the Government of India through notifications dated 10 January 2019 amended the Foreign Trade Policy and corresponding customs notifications, effected below changes:

- Removal of the condition of pre-import to avail exemption from IGST and compensation cess with prospective effect, subject to the authorization holder complying with below key conditions, in respect of duty exempted imports made after discharge of export obligation:

- Exemption of IGST and compensation cess has also been extended to deemed exports:

Imports under Advance Authorization are now exempt from IGST and compensation cess for making supplies under following deemed exports categories

- Supply of goods by a registered person against Advance Authorization.

- Supply of capital goods by a registered person25 against Export Promotion Capital Goods Authorization

- Supply of goods by a registered person25 to an Export Oriented Unit

PwC Comments: The removal of ‘pre-import’ condition will address the issue faced by trade since October 2017 and provide required relief to the authorization holders. However, as the amendment is prospective, there would not be any relief in case of pending disputes. Further, as the exemption under the scheme is presently available till 31 March 2019, the relief extended would be for a limited period

Upcoming Events

CEO FORUM 2019

Kerala and Singapore - A Similitude: The Way Forward | 01.03.2019

The 3rd Breakfast Meeting under the aegis of the Chamber’s CEO FORUM 2019 will be held on Friday, the 1st of March 2019 between 8.00 am and 10.00 am at the Anchor Hall, Taj Gateway Hotel, Marine Drive, Ernakulam.

The Speaker at this Session will be Mr. Abraham Chacko, Former ED, Federal Bank Ltd. and Independent Director, Jana Holdings Ltd., Bangalore who will speak on ‘Kerala and Singapore – A Similitude: The Way Forward.’

Workshop

Marketing in the Age of IOT, AI and Blockchain | 15.03.2019

Organizations today are staring at a ‘Disruption’ in the way they work brought about by a generational shift in computing. Disruptive technologies such as Blockchain, Artificial Intelligence (AI), Machine Learning and the Internet of Things (IoT) are driving continuous business transformation. The marketing landscape, especially the Marketing Technology (MarTech) landscape has also witnessed a tremendous upheaval. Newer technologies have ‘democratized’ marketing by enabling lean marketing teams to understand customers better, produce captivating content, and orchestrate meaningful engagement; all without engaging the traditional big advertising agencies.

The Cochin Chamber of Commerce & Industry is organising a Full Day Workshop on “Marketing in the Age of Internet of Things (IOT), Artificial Intelligence (AI) and Blockchain” on Friday, 15th March 2019 at Vantage Point, Hotel Abad Plaza, M.G. Road, Cochin. The session is scheduled from 9 am to 5 pm.

Mr. Arun James, Business Head, Outcome Infotech, Bangalore will be the Faculty for the Workshop.

This one-day interactive event will help Business Heads, CMO’s and Senior Marketing Professionals to embark on a technology driven Marketing Transformation journey by introducing them to the MarTech landscape, and equipping them to calibrate the right marketing stacks based on their unique requirements.

Chamber going Digital

Exclusive EXIM Statistics

Advertise with us

Chamber Blogs!

Employability Quotient

This is an age where most employers use online tools to find keywords and filter the numerous resumes mailed to them by job applicants. So it is a common practise now among the job seekers to include words like “adaptability, teamwork and cognitive skills. The list varies depending on the applicant. Many job applicants might follow this practice simply because the job description demands it. There are others who would like to add these words so that their resumes stand out. Gone are the days when an employer used to assess the candidate merely on subject knowledge. Today’s competitive world witnesses many candidates performing equally well when their subject knowledge is put to test. It is in this scenario that companies are increasingly looking for skills specific to the job or general job skills in a candidate. Interviewers even ask the applicants to cite examples to prove these skills. In short, the employer is actually looking for a candidate, who will fit the role well and is job ready. These additional skills are what are termed – Employability Skills. In a swiftly changing employability landscape, these are the skills that set the job applicants apart from the others as they walk out of that Board Room after attending an interview.

Employability skills or “soft skills” are the key to workplace success. Employability skills are a set of skills and behaviours that are necessary for every job. These skills allow you to

- Communicate with co-workers

- Find solutions to problems at the workplace

- Understand your role within the team

- Make significant and responsible decisions

- Take charge of your own career Employers value employability skills because they are linked to how you get along with co-workers and customers, your job performance, and your career success. Some of the essential employability skills would be;

Foundational skills

- Being organized and punctual

- Reliable and with a positive attitude towards work

- Effort and perseverance

- Time management and accuracy

Interpersonal Skills

- Friendly and Polite

- Respect for supervisors and co-workers.

- Responds appropriately to customer requests

- Asks for feedback

Communication Skills - Read and understand written materials

- Listen, understand and ask questions

- Follow directions

- Express ideas clearly when speaking or writing

Problem Solving and Critical Thinking

- Accepting of change

- Willingness to start, stop and switch duties.

- Works calmly in busy environments

- Starts tasks without prompting

Teamwork

- Comfortable working with people of diverse backgrounds

- Sensitive to other peoples’ needs

- Takes responsibility for own share of work

- Contributes to team goals

Ethics and Legal Responsibilities

- Takes responsibility for own decisions and actions

- Understands and follows Company rules and procedures

- Honest and trustworthy

- Acts professionally and with maturityProfessional Skills

- Career development by learning new skills and taking on different projects.

- Leadership skills like coaching and mentoring others, willingness to take risks etc.

Economic growth results in job creation. In this context, India is currently focussing on skilling people. Our aim is to become the future Skill Capital of the world and the Government is leaving no stone unturned to achieve this goal. Being a nation with the youngest population, with more than 62% of its population in working age group of 15-59 years, and more than 54% of its total population below 25 years of age, it appears to be an attainable goal. Recent skill initiatives such as National Skill Development Mission, Amendment in the Apprentices Act etc. are examples of Government’s intention to move in this direction. Today’s job market and in-demand skills are hugely different from the ones that existed 10 or even 5 years ago. And, the pace of change is only set to accelerate in the days to come. New jobs require new skills. Building a skilling system to match the new requirements, a system that responds well to business needs, while opening opportunities for all is the need of the hour. Transforming the way employers invest in their workforce and use the skills of their employees can help meeting new skill requirements.

The survey done for India Skills Report 2018 focuses on future skills requirement and results show that AI & Robotics are leading the next gen jobs along with others. The survey clearly highlights that nearly 50% of the applicants appearing for the interview either do not meet the skills requirement or may possess skills only to meet the basic requirement of employers. It is estimated that the Indian workforce will increase to approximately 600 million in the year 2022 from the current 473 million. As the workforce will increase by about 27 percent during this period the overall composition of the unorganized sector and organized sector will slightly change from 92 percent and 8 percent today, to 90 percent and 10 percent by 2022. The major forces impacting these shifts are that of globalization, the expanding domestic Indian market and adoption of exponential technologies, like AI, Robotics, and IOT by Indian corporates. Advances in robotics, artificial intelligence, and machine learning are ushering in a new age of automation, as machines match or outperform human performance in a range of work activities, including ones requiring cognitive abilities. The other interesting aspect is that while only 5 percent of the activities performed today can be automated fully, almost 60 percent of current activities have at least 30 percent constituent activities that can be automated. This implies that more job activities will be fundamentally altered by automation than completely automated. This essentially means that people will continue to work alongside machines to produce the growth in per capita GDP to which countries around the world aspire. This wave of automation will result in a slew of new age jobs. These new age roles demand different skill sets from that of the existing labour force. Some examples of such roles are Data Scientist, 3D Printing, Digital Marketing, Cyber Security Specialist, Block Chain Architect etc. When one looks at potential jobs being created due to automation, the early indicators suggest that more jobs will be created in sectors aided by automation than the sectors creating automation solutions themselves. As estimated in the World Economic Forum ‘future of jobs’ report, in India the overall employment outlook is of strong growth in consumer and professional services industries while it suggests moderate growth in basic infrastructure, energy and mobility. The same report indicates that people in the information and communication technology industry are likely to be re-skilled. As per the Report, cognitive abilities such as creativity, logical reasoning and problem sensitivity, will be required in jobs in 2020. According to the India Skills Report 2018, Bangalore, Chennai, Indore, Lucknow, Mumbai, Nagpur, New Delhi, Pune and Tiruchirappalli are the cities with a high employability rate. Andhra Pradesh, Delhi, Gujarat, Karnataka, Kerala, Madhya Pradesh, Maharashtra, Punjab, Tamil Nadu and Uttar Pradesh are the States with high employability rates. Kerala tops the charts in skills like Emotional Intelligence and Self-determination.

Internship is an opportunity for both employer and candidate to assess each other before getting into an actual employee-employer agreement. Being an employer, corporates have an opportunity to test the skills, train the intern and assess them before making him/her a full-time employment offer thus increasing their employability factor. Workplace gender diversity and equality should be included in the agenda for organizations across the globe especially in India where women’s participation in the workforce is decreasing at an alarming rate. The Government is making efforts to push this agenda and has taken several actions such as mandatory appointment of one-woman board member, increase in maternity leave from 12 weeks to 26 weeks, special funding scheme for women entrepreneurs etc. along with several others.

The Survey also states that every organization prefers an experienced and trained pool of candidates over fresh or inexperienced candidates for various reasons viz. the training effort (time & cost), productivity and opportunity cost etc. which in turn affects employability of fresh graduates applying for jobs.

Today digital technologies such as 3D printing, sensors, cognitive technologies, robotics, AI and the “Internet of Things (IOT)” are changing the way companies design, develop, and deliver almost every product and service. Analytics, Artificial Intelligence, Design (Software, Hardware, and Concept etc.), Research & Development and Robotics are the future job areas with Data Analytics and R&D emerging as areas of maximum scope. Domain Understanding, Adaptability and Positive Attitude were identified as the most preferred employability skills according to reports and the preferred sourcing channels of employers were Job Portals, Internal referrals and Consultants.

Interestingly, the Cochin Chamber had conducted a 2-day workshop called the “The Last Mile 2019- Eligibility 2 Employability” on the 15th and 16th of February 2019 for the students who are on the threshold of starting their careers. The programme was an effort to spread awareness among the students of the need to be job ready from day one by keeping abreast of the various changes in the employment requirements and making themselves employable in every sense of the word.

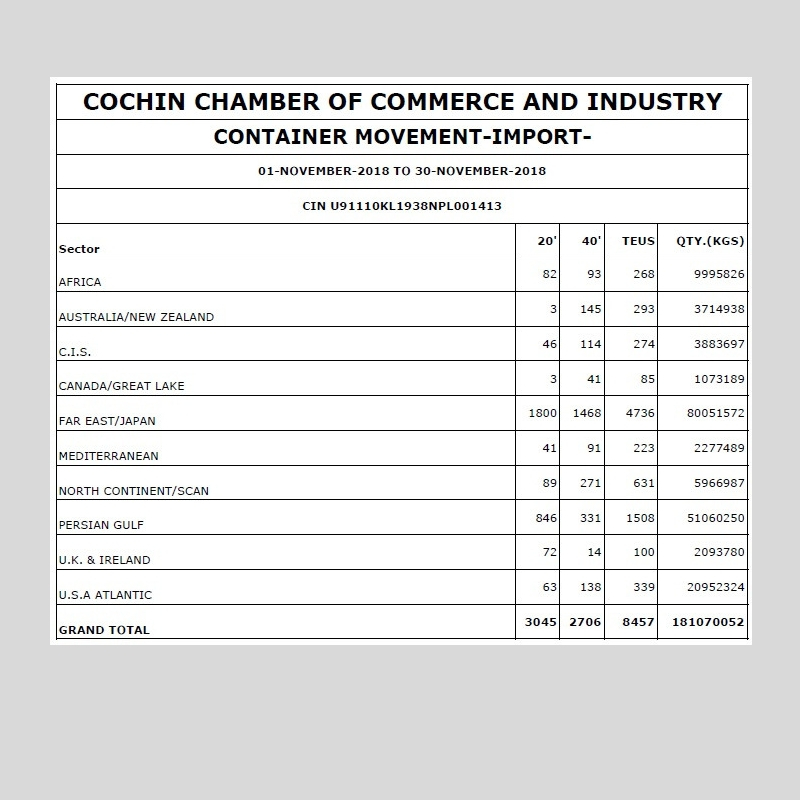

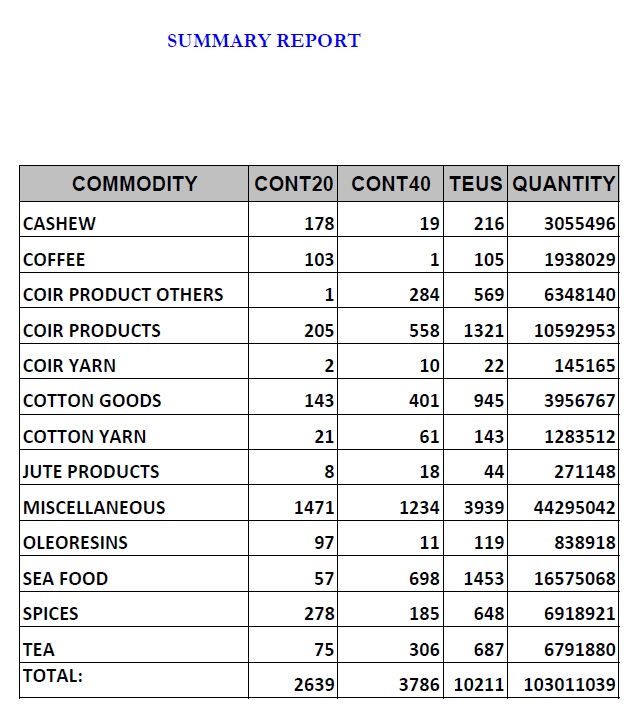

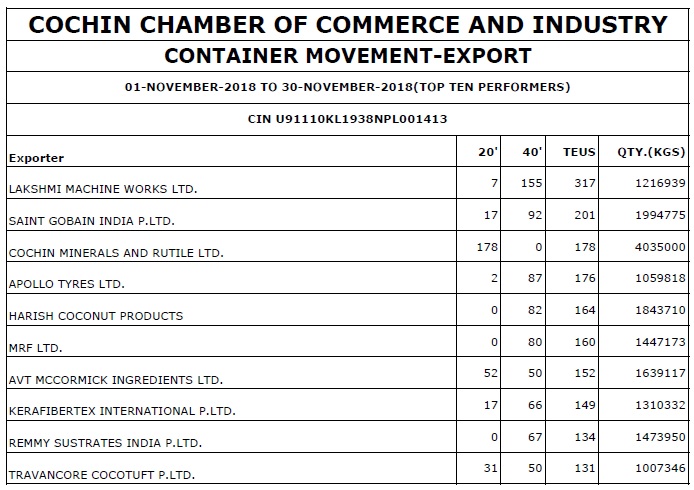

Exclusive EXIM Statistics - Sample Reports