President's Note

Dear Friends,

India has witnessed an alarming surge in Covid cases in recent weeks. On September 7, India overtook Brazil with 4.2 million confirmed cases to become the country with the second-highest number of confirmed cases in the world.

With more than 90,000 people succumbing to COVID-19 infection so far, India’s death toll is the third highest in the world after the US and Brazil. Since mid-August, India has been recording the world’s largest daily increases in coronavirus cases. In the second week of September, new COVID-19 cases averaged nearly 90,000 per day in India.

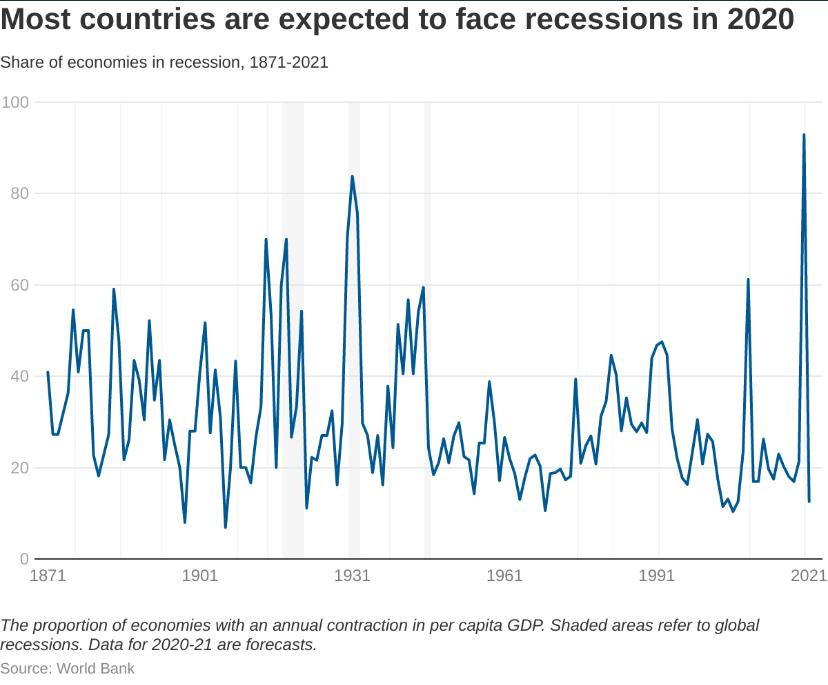

The pandemic has delivered an unparalleled economic blow to the country. The nationwide lockdown literally shuttered India’s $2.9 trillion economy. Economic activity came to a grinding halt in the country. As per official data released by the Ministry of Statistics and Programme Implementation, the Indian economy contracted by 23.9% in the April-June quarter of this fiscal year. This is the worst decline ever recorded since India started compiling GDP statistics on a quarterly basis in 1996.

India’s GDP contraction was worse than any of the world’s biggest economies. Except for China, most major economies witnessed GDP contraction in the April-June quarter of 2020, but India posted the steepest quarterly decline, far worse than the US (9.1%) and Italy (17.7%) ― two countries severely hit by the coronavirus pandemic. As the informal sectors of the economy have been worst hit by the pandemic, India’s GDP contraction during April-June could well be above the projected figures.

For the Indian economy, private consumption and investment are the two biggest engines for growth. During the first quarter of 2020, private consumption ― accounting for 59% of India’s GDP ― declined by 27%, while investments by private businesses fell by 47%. India’s net exports turned positive due to sharp compression in imports. Except for agriculture, all the major sectors of the economy were badly hit. Significantly, labour-intensive sectors such as construction, real estate, retail trade, transport and manufacturing contracted sharply during this quarter.

Business activity and consumption is expected to remain subdued in the coming months due to a continued rise in virus cases across the country and the contraction in the Indian economy could continue into the next three quarters. Economists, rating agencies and international financial institutions have revised their forecasts and their current projections show India’s GDP could contract in the range of 9% to 18% this fiscal year.

Economic recovery is expected to be slow and uneven with adverse consequences on output, employment and financial stability. Both private consumption and investment demand will take a long time to recover. The discretionary spending on non-essential goods has declined drastically due to rising unemployment and worries about likely job losses in the future. In the absence of domestic demand, businesses will not undertake fresh investments, which in turn would curb employment and overall economic growth. However, of late, few indicators (e.g., power consumption, passenger vehicle sales and e-way bills) are showing signs of revival in India after the government eased lockdown restrictions.

What is urgently needed are measures to spur domestic demand and to sustain investment. The primary focus should be on the informal sectors, micro, small and medium enterprises (MSMEs), the self-employed and casual workers that have been the worst casualty of the COVID-19-induced lockdown and subsequent disruptions.

The much talked about Labour Law Reforms are here. The Lok Sabha, has passed three new labour codes – the Industrial Relations Code Bill, 2020, Code on Social Security Bill, 2020 and the Occupational Safety, Health and Working Conditions Code Bill, 2020 – with a view to amalgamate 44 central Labour Acts into four codes, aimed at simplifying India’s labour laws, and improving the ease of doing business. The Code on Wages, which had proposed the universalisation of minimum wages, was cleared by Parliament last year.

The changes to the labour laws will provide operational freedom to employers, although provisions related to universal social security and guaranteed minimum wages may substantially add to their cost of hiring.

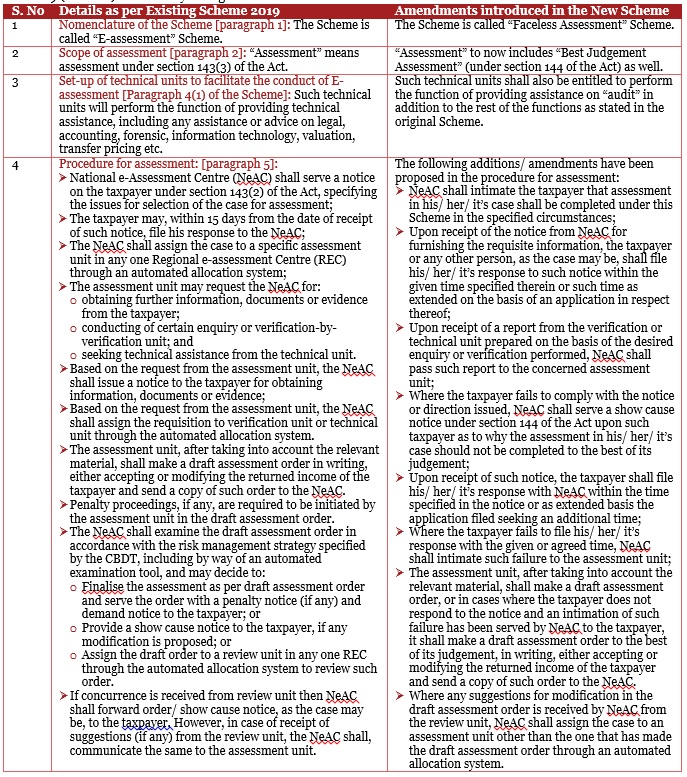

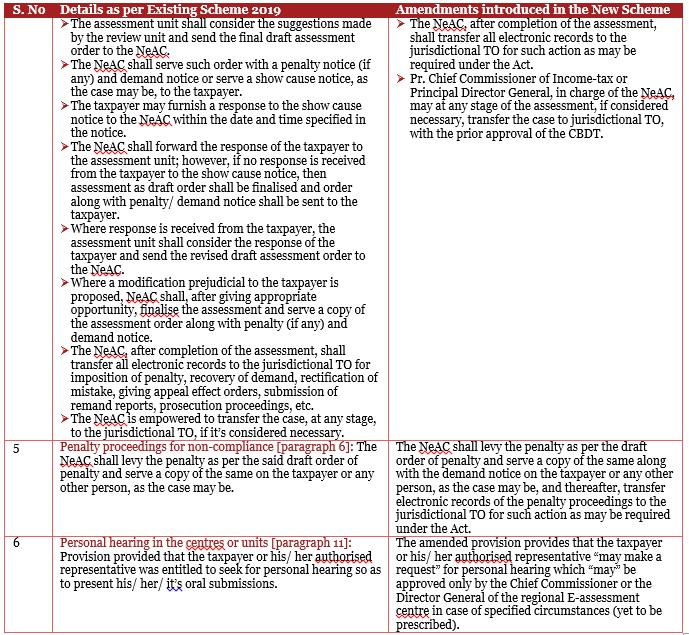

Coming to this month’s activities, we organised the Virtual CEO Forum Meeting on Saturday, 8th of August, 2020. Shri Ravindra Kumar I.R.S., Principal Chief Commissioner of Income Tax, Kerala Region was the Speaker at the meeting. He spoke on the “Faceless Assessment Scheme and the Tax Payers’ Charter”. He spoke about how faceless assessment and faceless appeals aim to eliminate physical interface between taxpayers and the tax authorities, thereby imparting greater efficiency and transparency to the assessment and appeal process. The program was well appreciated by all those who participated.

The Ministry of Corporate Affairs (MCA) has announced a new format for the Statutory Audit of Companies. The MCA has notified Companies (Auditor’s Report) Order, 2020 on 25 February 2020 (CARO 2020). The order (CARO 2020) replaces the earlier order under Companies (Auditor’s Report) Order, 2016. In this connection the Chamber partnered with TiE, Kerala in organising a Virtual Meeting on the subject on Thursday, 10th September, 2020. Ms. Ruchi Rastogi – Partner, KPMG, India, Mr. Supreet Sachdev – Chartered Accountant, and Mr. Baby Paul – Chartered Accountant were the Speakers at the session.

On 17th September, the Chamber conducted an Online Session on ‘Latest Changes under Customs Law’. The Speakers at the session were Mr. Prabhakaran P M – Partner & Head of Kochi Office, Lakshmi Kumaran & Sridharan; Ms. Lakshmi Menon – Partner – Customs and International Trade Team, Lakshmi Kumaran & Sridharan; and Mr. Karthik Nair, Joint Partner – Kochi Office, Lakshmi Kumaran & Sridharan. The Webinar covered in detail, areas such as In bond Manufacturing, Faceless Assessment under Customs Law, and Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR).

On the 29th of September, we organised a Virtual Meeting on the “Consolidation and Codification of Labour Laws: A step towards a brighter future?” Ms. Devika A. Gadgil an Associate with AnB Legal, Mumbai was the Speaker on this occasion. The Meeting covered the backdrop of Indian labour laws, the importance of merging Labour Laws into a Code, Analysis of the legislation and its impact in the Indian business scenario etc.

The next CEO FORUM Virtual Meeting is scheduled for Saturday, 3rd October 2020. Dato Dr. Jai Mohan, Adviser to Nichi – Asia Center for Stem Cell & Regenerative Medicine, Malaysia has agreed to be the Guest Speaker at the Meeting and to speak on “Regenerative Medicine and Stem Cell Therapy”. I trust you all will attend this meeting.

The corona virus has contributed to the widespread adoption of face covers and masks and completely reworked social behavioural patterns. These are welcome changes that will serve us well for the future too when India continues to grapple with seasonal outbreaks. Let us all work together to ensure that we stay safe and healthy in the coming days.

V Venugopal

Quote

Trivia

Trivia

Trivia

Recent Events

CEO FORUM 2020 - Faceless Assessment Scheme and Tax Payers' Charter | 04.09.2020

The Cochin Chamber of Commerce and Industry conducted a Virtual CEO Forum Meeting on Saturday, 4th of September, 2020.

Shri Ravindra Kumar I.R.S., Principal Chief Commissioner of Income Tax, Kerala Region was the Speaker at the meeting. He spoke on “Faceless Assessment Scheme and Tax Payers’ Charter”.

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

Mr. Kumar said that the tax system in India has seen major reforms lately aimed at simplifying the tax structure, bringing in ease of compliance and reducing litigation. On August 13, 2020, the Prime Minister launched a platform for ‘Transparent Taxation- Honouring the Honest.’ The platform comprises three reforms:

faceless assessment, faceless appeals and the Taxpayers’ Charter. Faceless assessment and faceless appeals aim to eliminate physical interface between taxpayers and the tax authorities, thereby imparting greater efficiency and transparency to the assessment and appeal process. Mr. Kumar added that the objective is to make the tax assessments “seamless, painless and faceless’, where the physical interface is sought to be eliminated. It is expected that once successfully implemented, these changes will bring in transparency and objectivity in tax assessments, foster taxpayer’s trust and confidence, and boost voluntary compliance.

Mr. Kumar explained that under the new assessment scheme, the taxpayer and the tax official will not have any direct human interface. The entire assessment process will be divided into various units. The draft assessment will be done by one unit and this would be reviewed by a second unit and the final assessment will be done by yet another different unit. The allocation of cases to various units will also be automated under the Faceless Scheme of Assessment. This will create an anonymous system where the tax payer does not know who the tax assessing officer is as the function of assessment will be performed by various units and that too in the form of team and not an individual. This is a welcome step to ensure transparency, he said. The taxpayer will no longer be required to visit the Income Tax Office for assessment and appeals, he said.

As a major structural reform, the National e-Assessment Centre (NeAC) based in Delhi will now act as the single point of contact between the taxpayer and the tax department. It will facilitate and co-ordinate the proceedings in a centralized manner. At present, the exceptions to this scheme include cases of serious frauds, major tax evasion, search and seizure matters and international taxation cases, Mr. Kumar said.

Mr. Kumar said that during the Budget 2020 speech, the Finance Minister proposed to amend the provisions of the Income Tax Act, 1961 to authorise the CBDT to adopt a Taxpayers’ Charter with the objective of creating a tax system which will build trust between the taxpayer and the tax authorities. The Taxpayers’ Charter aims to treat taxpayers as honest individuals / entities and to provide them with fair and courteous treatment. It proposes to resolve issues in a time-bound manner and provide timely decisions to help taxpayers settle disputes without having to go through a long-drawn litigation process.

Concluding the meeting, Mr. Kumar said that the Taxpayers’ Charter also aims to provide complete and accurate information for tax compliance and endeavours to reduce the cost of compliance. On the other hand, the Taxpayers’ Charter expects the taxpayer to be honest and compliant in reporting all details to the tax authorities. As a good citizen, it will be the responsibility of the taxpayer to maintain accurate records, provide timely responses and make tax payments on time, he said.

Following this, there was a brief discussion wherein the Speaker clarified the issues raised by the participants.

The meeting ended with the Vice President of the Chamber, Mr. K Harikumar thanking everyone for having participated in the meeting.

Virtual Session on "Companies (Auditor’s Report) Order, 2020 (CARO 2020)" | 10.09.2020

The Cochin Chamber of Commerce and Industry partnered with TiE, Kerala in organising a Virtual Meeting on the Companies (Auditor’s Report) Order, 2020 (CARO 2020) on Thursday, 10th September, 2020 on the Zoom Platform.

Mr. Nirmal Panickar, Executive Director, TiE, Kerala welcomed the participants to the virtual meeting. The President of the Chamber Mr. V Venugopal introduced the Speakers at the meeting.

Ms. Ruchi Rastogi – Partner, KPMG, India, Mr. Supreet Sachdev – Chartered Accountant and Mr. Baby Paul – Chartered Accountant were the Speakers.

Mr. Sachdev said that CARO 2020 is a new format for issue of Audit Reports in the case of statutory audits of Companies under the Companies Act, 2013. CARO 2020 has included additional reporting requirements after consultations with the National Financial Reporting Authority (NFRA). NFRA is an independent regulatory body for regulating the audit and accounting profession in India. The aim of CARO 2020 is to enhance the overall quality of reporting by the company auditors, he said.

Mr. Sachdev explained that CARO 2020 is applicable for all statutory audits commencing on or after 1 April 2020 corresponding to the financial year 2019-20. The order is applicable to all companies which were covered by CARO 2016. Accordingly, the order applies to all the companies except One person companies, Small companies (Companies with paid up capital less than/equal to Rs 50 lakh and with a last reported turnover which is less than/equal to Rs 2 crore), Banking Companies, Companies registered for charitable purposes and Insurance Companies.

Mr. Sachdev said that the main objective behind CARO is to basically augment the overall quality of reporting by Company Auditors. CARO 2020 is anticipated to

build up accountability, faith and transparency to stakeholders of the Companies. CARO 2020 follows the same layout of provisions like CARO 2016 with an addition in reporting and modifying disclosures and increasing scope of an auditor.

Mr. Paul said that there will be stringent comprehensive reporting of loans or other borrowings. It requires the Auditor to report whether the Company is a declared wilful defaulter by any bank or financial institution or other lender. He further added that the Auditor shall have to assess the authenticity of the complaint, whether it has been resolved, whether reflected in financial statements which in itself require investigating into whistle blowing mechanism which in itself is a tedious task.

About the internal audit system, Ms. Rastogi said that the Auditor is required to report as to whether the Company has an internal audit system that is commensurate with the size and nature of its business. Though this point has been rightly included however it adds a layer of responsibility on the Statutory Auditor and also increases the chances of ego clashes due to segregation of audit and non-audit services.

Following this, there was a brief discussion wherein the Speakers clarified the issues raised by the participants.

The meeting ended Mr. Panickar thanking everyone for having participated in the meeting.

Virtual Session on "Latest Changes under Customs Law" | 17.09.2020

The Cochin Chamber of Commerce and Industry organised an Online Session on ‘Latest Changes under Customs Law’ on Thursday, 17th September 2020 on the Zoom Platform.

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

The Speakers for this session were Mr. Prabhakaran P M – Partner & Head of Kochi Office, Lakshmi Kumaran & Sridharan; Ms. Lakshmi Menon – Partner – Customs and International Trade Team, Lakshmi Kumaran & Sridharan; and Mr. Karthik Nair, Joint Partner – Kochi Office, Lakshmi Kumaran & Sridharan.

Commencing the Session Mr. Karthik Mr. Nair said that to achieve the goal of a strong self-reliant India, Atmanirbhar Bharat Abhiyan has been initiated by the Government with encouraging slogans of ‘Vocal for Local’ and Make in India, Make for the World. With a view to promote manufacturing in India, Section 65 of the

Customs Act has been amended over a period of time to promote the initiative of manufacturing in-bond to an importer who can import raw materials and capital goods without payment of duty for manufacturing and other operations in-bond and export.

He further added that In Bond Manufacturing offers deferred import duty on capital goods as well as raw material or inputs used in bonded manufacturing. The import duty gets remitted if the finished goods are exported. However, if the finished goods are cleared in the domestic market, the import duty on raw material used becomes payable, but without any burden of interest. The Session covered in detail the Nuances of bonded manufacturing, types of beneficiaries, benefits of bonded manufacturing, procedure for clearance of manufacture and capital goods, accounts and records maintenances and open issues and challenges in bond manufacturing.

Mr. Prabhakaran, in his talk, gave the participants an overview of the Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR). He said that the Ministry of Finance has issued the Customs Rules, 2020 effective from 21st September, 2020 which prescribes various obligations and guidelines, for claiming the origin based Customs duty exemptions and concessions. The Webinar covered in detail the Declaration in the BoE, Information on Origin of Goods, Claim of preferential rate of duty under a Trade Agreement, Responsibility of Importers, and Verification by Customs Authority.

Speaking at the session Ms. Lakshmi Menon said that an importer is now required to do due diligence before importing the goods to ensure that they meet the prescribed originating criteria. A list of minimum information that the importer is required to possess has also been provided in the rules along with general guidance. Also, an importer would now have to enter certain origin related information in the Bill of Entry, as available in the Certificate of Origin. The new Rules will support the importer to correctly ascertain the country of origin, properly claim the concessional duty and assist Customs authorities in smooth clearance of legitimate imports under FTAs. The new rules would strengthen the hands of the Customs in checking any attempted misuse of the duty concessions under FTAs, she said.

To promote the ease of doing business, CBIC has implemented faceless assessment which is similar to the e-assessment (faceless assessment) under Income Tax law in a phased manner, Ms. Menon said. Presently, it has been launched in Bangalore and Chennai Customs Zones and will be extended to all airports, ports, inland container depots throughout India by the end of the year. As a major structural reform, the National e-Assessment Centre (NeAC) based in Delhi will now act as the single point of contact between the taxpayer and the tax department. It will facilitate and co-ordinate the proceedings in a centralized manner. The webinar examined the objectives and aspects of the Scheme of Assessment proposed to be undertaken through the Customs Automated System.

Following this, there was a brief discussion wherein the Speaker clarified the issues raised by the participants.

The meeting ended with the Deputy Secretary of the Chamber, Mr. Manu Varghese, thanking everyone for having participated in the meeting.

Virtual Session on "Consolidation and Codification of Labour Laws" | 29.09.2020

The Cochin Chamber of Commerce & Industry organised a Virtual Meeting on the “Consolidation and Codification of Labour Laws: A step towards a brighter future?” on the 29th of September, 2020. Ms. Devika Gadgil – ANB Legal, Mumbai was the speaker for this Session.

In the article below Ms. Devika gives a clear analysis of the Consolidation and Codification of the Labour Laws, the background, the process and its implications.

Article

Most of the countries in the world including India have faced the issue of an archaic labour law system, which is plagued with problems in terms of multiplicity of labour laws, discrepancies in different legislations, etc. India’s labour legislations consisted of over 100 State legislations and 44 Central legislations, covering a plethora of aspects. However, there has always been a dire need to simplify and consolidate the labour statues in India with a view to streamline the legislations.

In 2019, the Ministry of Labour and Employment introduced 4 Bills to consolidate 29 Central legislations regulating the following aspects: (i) Wages, (ii) Industrial Relations, (iii) Social Security, and (iv) Occupational Safety, Health and Working Conditions. The Code on Wages, 2019 was passed by the Parliament in 2019; however, the three remaining Bills were referred to the Standing Committee. The Bills were re-introduced in the Lok Sabha as on September 19, 2020 and were passed by the Rajya Sabha as on September 23, 2020. However, the Bills have faced strong opposition from certain sections and the effectiveness of the Bills from the perspective of striking a balance between the demands of the workforce and ensuring ease of doing business for the Companies remains debatable.

SCOPE

The present article analyses the three Codes and discusses the various key features and the implications therein. Section I discusses the backdrop and the need for consolidated legislations in India. Section II deals with the Industrial Code, 2020 and analyses the various key features, major amendments and the practical implication thereunder. Section III analyses Occupational Safety, Health and Working Conditions Code, 2020 and discusses the changes and their implications in depth. Section IV deals with the Code of Social Security, 2020 and analyses the various key features and the implication thereunder.

ANALYSIS

Section I: Backdrop and need for consolidated Labour Statues in India

As discussed above, most of the countries in the world struggle with obsolete labour laws and have felt the need to update the same. India has over 100 State legislations and 44 Central legislations, which makes the compliance process a lot more complicated.

The labour codes were adopted on the recommendations of the Second National Commission on Labour (“NCL”) in 2002. The Second NCL found existing legislation to be complex, with obsolete provisions and inconsistent definitions. With a view to improve ease of compliance and ensure uniformity in labour statues, the NCL recommended the consolidation of labour legislations into broader groups such as (i) industrial relations, (ii) wages, (iii) social security, (iv) safety, and (v) welfare and working conditions.

The Government introduced 4 Codes in Parliament which consolidated 29 labour statues. The following were the key factors which led to the consolidation and codification of the labour legislation in India:

- The need to replace old & primitive labour statues and upgradation of the legislations

- Expansion of scope of the legislations along with inclusion and streamlining of the unorganized sector

- Ensuring efficiency and ease of compliance

- Removal of discrepancies in the existing Central and State legislations

- Ensuring effective implementation of the legislations

The Code on Wages, 2019 was passed by Parliament in 2019. However, the other three codes were reintroduced after the Standing Committee Report.

Section II: The Industrial relations Code, 2020

A) BACKGROUND OF THE CODE

The Industrial Code, 2020 plays a crucial role in amalgamating and combining the 3 major laws governing the employee-employer relationship. The legislation provides for a broader framework to protect the rights of workers to form unions, to minimise the friction between the employers and workers and to deal with settlement of industrial disputes. The Code replaces and consolidates the following three statues: (i) the Trade Unions Act, 1926; (ii) the Industrial Employment (Standing Orders) Act, 1946; and (iii) the Industrial Disputes Act, 1947.

B) ANALYSIS

The Code Bill has introduced many amendments which have altered the practical implications of the various legislations.

1) Key Definitions

a) "Industrial Dispute"

The following are few of the key definitions which have been amended by the Code Bill:

The definition of industrial dispute has been amended to include disputes arising out of discharge, dismissal, retrenchment or termination of workers thereby expanding the scope thereunder.

b) "Worker"

The definition of the term worker has been expanded to include working journalists as defined in clause (f) of section 2 of the Working Journalists and other Newspaper Employees (Conditions of Service) and Miscellaneous Provisions Act, 1955 and sales promotion employees as defined in clause (d) of section 2 of the Sales Promotion Employees (Conditions of Service) Act, 1976. Further, the definition classifies persons employed in a supervisory role drawing less than INR 18,000/- per month under the definition. The limit has been revised from INR 6,500/- per month as specified under the Industrial Disputes Act, thereby bringing more workers under its ambit.

c) "Fixed Term Employment"

The concept has been defined to include the engagement of a worker on the basis of a written contract of employment for a fixed period. Thus, all the fixed term employees are entitled to receive benefits as normal workers except retrenchment benefits. The fixed term employee will also be eligible for gratuity subject to the condition that they render service under the contract for a period of one year.

d) "Employer"

The term employer has been amended to include ‘contractor’, ‘legal representative of deceased employer’ etc.

2) Key Provisions

The Code Bill has introduced a few concepts and further amends multiple provisions related to strikes, trade unions, negotiations, constitution of authorities, etc.

a) Fixed Term Employment

The Code Bill incorporates certain provisions with regard to protection of the fixed term employees. The fixed term employees would be eligible to receive all the statutory benefits available to a permanent worker proportionately according to the period of service rendered by the employee. The same shall be applicable even if the period of employment does not extend to the qualifying period of employment as required in the statute. Further, fixed term employees will be eligible to receive gratuity on completion of one year of service under the contract. Thus, the Code Bill now extends protection to a wide array of employees.

b) Provisions related to strikes

The Code Bill states that no person employed in an industrial establishment shall go on strike, in breach of contract without giving to the employer notice of strike, within 60 (sixty) days before striking; or (b) within 14 (fourteen) days of giving such notice. Such a notice is to be shared with the Conciliation Officer within 5 (five) days from the date of the notice. Further, during the pendency of the arbitration proceedings or conciliation proceedings, the employees are not permitted to strike. Under the Industrial Disputes Act, the provision pertaining to notice period for strikes/ lock-out was applicable only to public utility services; however the same has now been extended to all establishments Thus, the concept of “flash strikes” is not permitted under the Code Bill.

c) Lay Off, Retrenchment and Closure

The Code Bill has increased the threshold employee-limit for prior Government permission for retrenchment, lay-off and closure. The Code Bill states that any factory, mine or plantation, as defined under section 72 of the Code Bill, employing more than 300 workers on an average per working day in the preceding twelve months needs to obtain prior permission of the appropriate Government for retrenchment, lay-off or closure. The appropriate Government is only permitted to increase this threshold limit of 300 workers. It must be noted that establishments of a seasonal character or in which work is performed only intermittently do not fall under this ambit.

In the event the appropriate Government does not communicate the order granting or refusing to grant permission to the employer within a period of sixty days from the date on which such application is made, the permission applied for shall be deemed to have been granted as applied for on the expiration of the said period of sixty days.

d) Threshold limit for framing of Standing Orders

Standing Orders are required to be framed in relation to the matters specified in the first schedule of the Code Bill such as the classification; attendance; condition for leave, paydays; termination of employment or suspension; redressal mechanism, etc. The Code Bill increases the threshold limit from 100 workers to 300 workers for compliance by industrial establishments for adoption of standing orders.

e) Negotiation Council

The Code Bill introduces a provision for recognition of a Negotiation Council. Under the Code Bill, a sole Union will be the negotiation agent with the management of the establishment. If there were more than one registered trade union of workers functioning in an establishment, the trade union having more than 51% of the workers as members would be recognised as the sole negotiating union. In case no trade union is eligible as sole negotiating union, a Negotiating Council will be formed consisting of representatives of Unions that have at least 20% of the workers as members The Code Bill further states that no Trade Union of workers shall be registered unless at least 10% of the workers or 100 (one hundred) workers, whichever is less, engaged or employed in the industrial establishment or industry with which it is connected are the members of such Trade Union on the date of making of application for registration. Thus, there is ambiguity pertaining to the solution in the event trade unions have more than 100 member workers but no single union fulfils the limit of 20% for formation of a negotiation council.

f) Voluntary Reference to Arbitration

Due to the amendment in the definition of industrial disputes, disputes arising out of discharge, dismissal, retrenchment or termination of workers can also now be referred to arbitration.

g) Limitation Period

The limitation period for filing of industrial dispute by the employee has been reduced to 2 years instead of 3 years as specified under the Industrial Disputes Act.

The Code Bill also provides for provisions pertaining to constitution of industrial tribunals and national tribunals, provision for re-skilling funds, etc.

g) Limitation Period

The limitation period for filing of industrial dispute by the employee has been reduced to 2 years instead of 3 years as specified under the Industrial Disputes Act.

The Code Bill also provides for provisions pertaining to constitution of industrial tribunals and national tribunals, provision for re-skilling funds, etc.

C) THE LOOPHOLES

The Code Bill has been drafted in an exhaustive manner however; there are certain issues and loopholes which need to be addressed.

a) The Code Bill restricts the ability of workers to go on strikes or lock-outs

b) Restrictive conditions pertaining to formation of a Negotiation Council might affect the negotiation power of the workers and the trade unions, which might result in unequal bargaining

c) The change in the threshold limit of workers from 100 to 300 with regard to lay-off, retrenchment and closure might have an adverse impact on the workers since the establishments do not need to obtain any prior permission as discussed

d) The non-applicability of standing orders to establishments with less than 300 workers also might have an adverse impact on the workers due to lack of a proper and effective model standing policy for governing the relationship between the employer and the

Section III: The Occupational Safety, Health, and Working Conditions Code, 2020

A) BACKGROUND

The Occupational Safety, Health and Working Conditions Code, 2020 consolidates and amends 13 laws governing occupational safety, health and working conditions of the persons employed in an establishment. It was introduced with an object to impart flexibility in adapting technological changes and dynamic factors, in the matters relating to health, safety, welfare and working conditions of workers. The Code replaces and consolidates the thirteen statues such as the Factories Act, 1948; the Mines

Act, 1952; the Contract Labour (Regulation and Abolition) Act, 1970; the Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Act, 1979; etc.

B) ANALYSIS

The 2020 Code Bill has amended the scope of the provisions dealing with the working conditions, health and safety of the workers and has attempted to create an inclusive legislation which would extend these rights to a wide array of workers.

1) Key Definitions

The following are few of the key definitions which need to be analysed:

a) The definition of “Factory” has been revised and threshold limit of employees is now 20 in case of use of power and 40 in cases without power and has specifically excluded, hotels, restaurants, eating places, Electronic Data Processing Units or Computer Units etc.

b) The definition of “Employer” has been amended to expand the scope to contractor, legal representative of a deceased employer, etc.

c) The definition of “Employee” has been incorporated and includes person doing any skilled, semiskilled or unskilled, manual, operational, supervisory, managerial, administrative, technical or clerical work for hire or reward.

d) The definition of the term “Worker” has been amended and now includes any person who is employed in a supervisory capacity drawing wage exceeding eighteen thousand Rupees per month or an amount as may be notified by the Central Government from time to time.

e) The definition of “Inter-State Migrant Worker” has been amended to include self-employed workers and has been subject to a ceiling wage threshold of INR 18,000/- per month.

f) The definition of “Contract Labour” has been modified and includes inter-State migrant worker but excludes part-time employee, regularly employed on mutually accepted standards of the conditions of employment and entitled to periodical increment and social security benefits.

2) Key Provisions

The Code Bill has introduced a few concepts and further amends multiple provisions related to contract labour, inter-state migrant workers, working hours, etc.

a) Contract Labour

The definition of contract labour has been expanded in the manner stated above and the Code Bill states that the laws pertaining to contract labour shall be applicable in every establishment with 50 or more contract labour. Further, the code states that contract labour cannot be utilized in the areas of “core activities.” The term “core activities” refers to the activity for which establishment is set-up subject to certain specified exclusions.

The Code Bill further imposes restrictions and liabilities on the employer as well as the contractor. The Contractor needs to obtain a license in the manner as specified under the Code Bill for supplying or engaging contract labour in any establishment or undertaking or executing the work through contract labour. The employer shall be prohibited from employing contract labour through a non-licensed contractor. Further, the contractor is not permitted to charge directly or indirectly, in whole or in part, any fee or commission from the contract labour.

The Code Bill imposes a liability on the principal employer to provide welfare facilities provided to the normal employees or workers specified under the Section 23 and 24 of the Code Bill, such as the providing canteens, rest rooms, drinking water, first aid etc. In the event the contractor fails to make payment of wages within the prescribed period or makes short payment, then, the employer shall be liable to make payment of the wages in full or the unpaid balance due, as the case may be, to the concerned contract labour employed by the contractor.

b) Inter-State Migrant Workers

As stated above, the definition of the term inter-state migrant worker has been expanded to include self- employed migrant workers. The following are few of the benefits have been extended to the inter-state migrant workers under the Code Bill: (i) option to avail the benefits of the public distribution system either in the native state or the state of employment, (ii) availability of benefits available under the building and other construction cess fund in the state of employment, (iii) insurance and provident fund benefits available to other workers in the same establishment (iv) suitable working conditions (v) journey allowance.

The Central and the State Governments shall maintain the data base or record, for inter- State migrant workers, electronically or otherwise in such portal and in such form and manner as may be prescribed by the Central Government. The migrant worker shall register himself as an inter-State migrant worker on such portal on the basis of self-declaration and Aadhaar. Further, a social security fund shall be established by the appropriate Government for the welfare of unorganized workers.

c) Single Registration

The Code Bill provides single registration for an establishment instead of multiple registrations resulting in a centralized database

d) Employment of Women

Women workers will be entitled to be employed in all establishments for all type of work and will be permitted to work at a night-shift, with their consent. If the appropriate Government considers employment of women in certain establishment dangerous for their health and safety, such Government may in the prescribed manner, require the employer to provide adequate safeguards prior to the employment of women for such operation.

e) Safety Committee

The appropriate Government may, by general or special order, require any establishment or class of establishments to constitute a Safety Committee in a prescribed manner.

f) Constitution of National and State Occupational Safety and Health Advisory Boards

The Central Government shall constitute a National Occupational Safety and Health Advisory Board to discharge the functions as specified under the Code Bill and to advise the Central Government on the matters such as framing of rules, implementation of provisions, issues of policy etc. The State Government shall constitute a Board to be called the State Occupational Safety and Health Advisory to advise the State Government on such matters arising out of the administration as may be referred to it by the State Government.

The Code further also deals with various provisions such as rights of the employees, welfare facilities, appointment of inspectors, etc. in detail.

C) ANALYSING THE LOOPHOLES

The Code Bill creates a mechanism for the protection and safety of the workers. However, there are certain areas which need to be considered:

a) The Code Bill bars Civil Courts from hearing any matters under the Code Bill. In the event where persons are aggrieved by the orders of authorities, the Code Bill provides for an Administrative Appellate Authority to be notified. However, it does not provide a judicial mechanism for hearing disputes under the Code Bill.

b) The 2019 Code Bill requires the contractors to pay a displacement allowance to inter-state migrant workers at the time of their recruitment, which was equivalent to 50% of the monthly wages. However, the same has not been retained in the 2020 Code Bill.

c) The Code Bill increases the threshold for coverage of factories and establishments employing contract workers. This has restricted the applicability of the Code Bill from a perspective of extension of benefits under the Code Bill to the workers employed in such establishments.

Section IV: The Social Security Code, 2020

A) BACKGROUND

The Social Security Code, 2020 consolidates and amends 9 statues governing social security with the objective of ensuring universal social security and consolidating the statues relating to social security with the goal of extending social security to all employees and workers either in the organised or unorganised or any other sector The Code replaces and consolidates the nine statues such as the Employees’ State Insurance Act, 1948; the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952; the Maternity Benefit Act, 1961; the Payment of Gratuity Act, 1972, the Unorganised Workers’ Social Security Act, 2008, etc.

B) ANALYSIS

The Code Bill has introduced key concepts such as a gig worker, platform worker and extended the benefits to the unorganised workers, etc.

1) Key Definitions

The following are the key definitions that need to be considered:

a) “Gig worker” means a person who performs work or participates in a work arrangement and earns from such activities outside of traditional employer-employee relationship

b) “Platform work” means a work arrangement outside of a traditional employer employee relationship in which organisations or individuals use an online platform to access other organisations or individuals to solve specific problems or to provide specific services or any such other activities which may be notified by the Central Government, in exchange for payment

c) “Platform Worker” refers to person engaged in or undertaking platform work

d) The definition of “Inter-State Migrant Worker” has been amended to include self-employed workers and has been subject to a ceiling wage threshold of INR 18,000/- per month.

1) Key Amendments

The following are the major amendments introduced via the Code Bill:

a) Concept of Gig Worker, Platform Workers and Unorganised Workers

The concept of gig worker and platform worker recognizes the work arrangement outside of a traditional employer-employee relationship, thus extending the applicability of the Code Bill and the benefits thereunder to a wide range of workers.

The Code mandates that the Central Government and State Government should frame a scheme for the welfare of unorganised workers in relation to the subjects prescribed under the Code Bill. The Code Bill states that the schemes for gig workers and platform workers may be funded through a combination of contributions from the Central Government, State Governments, and Aggregators. Every unorganised worker, gig worker or platform worker shall be required to be registered under the Code provided that the person has completed 16 years of age and shall be required to be registered under the Code via his/her Aadhar number. Further, there are various benefits such as helpline facilitation extended to the class of workers. A social security fund shall also be set up by the Central Government for social security and welfare of the unorganised workers, gig workers and platform workers.

b) Benefits under the EPF Scheme, ESIC and Gratuity

The Code Bill states that all establishments with 20 or more employees fall under the purview of EPF. In the earlier Act, the same was applicable only to establishment included in the schedule with 20 or more employees. The contributions paid by the employer to the fund shall be ten per cent. of the wages for the time being payable to each of the employees (whether employed by him directly or by or through a contactor), and the employee’s contribution shall be equal to the contribution payable by the employer in respect of him and may, if any employee so desires, be an amount exceeding ten per cent. of the wages, subject to the condition that the employer shall not be under an obligation to pay any contribution over and above his contribution payable under the Code Bill. Further, the Code Bill incorporates a limitation period of 5 years for initiation and 2 years for conclusion of enquiries.

With regard to the ESI, all establishments with 10 or more employees other than a seasonal factory will fall under the purview of the provisions. The Code Bill extends the benefit to Gig Workers, Platform Workers, Unorganised Worker and Plantation workers.

As per the Code Bill, gratuity is payable if the employee has served a continuous period of five years and fixed term employees will be paid on a pro rata basis. However, the same shall be three years in case of working journalists.

c) National Social Security Board and State Unorganised Workers Board

The National Social Security Board has been constituted for the purposes of the welfare of unorganised workers and also gig workers and platform workers under the provisions of the Code Bill.

d) Exemption during Pandemic

The Central Government may defer the application of the provisions of the Code for a period of three months in the event of a national disaster, pandemic or endemic.

B) ANALYSING THE LOOPHOLES

The Code Bill has surely introduced new concepts and has upgraded the legislations while codification. However, there are a few concerns which have not been addressed by the Code Bill:

a) The recommendation of the Standing Committee on implementation of an integrated social security system has not been taken into consideration while drafting the 2020 Code Bill. Integrated social security coverage is required to avoid deprivation of basic needs of workers

b) There is discrepancy pertaining to the extension of gratuity benefits to fixed term employees under the provisions of the Social Security Code, 2020 and Industrial Relations Code, 2020. The Social Security Code, 2020 states that in the case of fixed term employment, the employer will pay gratuity on a pro rata basis. However, the Industrial Relations Code, 2020 states that the fixed term workers will be eligible for gratuity only after they complete a one-year contract. Therefore, whether a fixed term employee with a contract of lesser than one year will be entitled to gratuity under the Code on Social Security, 2020 needs to be determined since the two legislations reflect different provisions on gratuity for fixed term workers

c) The Code Bill does not provide for common minimum mandatory entitlements across States for construction and unorganised workers to enable portability as per the recommendations of the Standing committee.

CONCLUSION

The idea of consolidation and upgradation has been the subject of discussions since the year 2002 after the report of the Second National Commission on Labour. The main objective has been to replace and update the obsolete and archaic labour laws in India along with ensuring ease of compliance. Effective labour laws are not only important with a view of protecting the rights of the workers but are also crucial from the perspective of ensuring ease of doing business in the country. The four labour codes were introduced on similar lines and keeping the same objective in mind. There are certain loopholes and issues in the Codes which need to dealt with and clarified keeping in mind the best interest of the workers and employees. The provisions of the code need to ensure that there is no adverse impact on the rights of the workers and the codes are an aid to them rather than an obstacle.

The Labour Codes are surely a step towards development and reformation. The Codes have brought in multiple amendments and introduced various concepts which will help in broadening the applicability of these regulations thereby creating all- inclusive legislations. Various protections and rights have now been extended to a plethora of workers and employees. Multiple authorities have been introduced under the Codes thereby creating mechanisms for the purpose of dispute redressal, advisory and compliance services, etc. The consolidation of these codes and the employer friendly policies introduced under the codes will surely have a positive impact on the index of ease of doing business in India thereby ensuring a boost for industry and the economy. It will also promote investments into the country.

The efficiency of the Labour Codes will depend on the effective implementation of the same. Thus, it is crucial to ensure that the true intent of the legislation is being achieved by striking the perfect balance between protection of the workers on one hand and interest of the employer on the other.

INTRODUCTION

With the objective of reducing any undue claims made by importers while importing certain goods, the Finance Minister Smt. Nirmala Sitharaman during the Budget Speech, 2020, stated that reformations shall be brought into the Trade Agreements with respect to the Rules of Origin. The same has been implemented by introduction of Section 28DA in the Customs Act, 1962 and further by notifying a set of Rules namely Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (hereinafter referred to as “CAROTAR”) by the Central Government.

The intention of CAROTAR is to put a stop to dumping of products especially from China, being re-routed through countries that have a Free Trade Agreement with India. CAROTAR supplements the certification provided to importer under the respective Trade Agreements they form a part of.

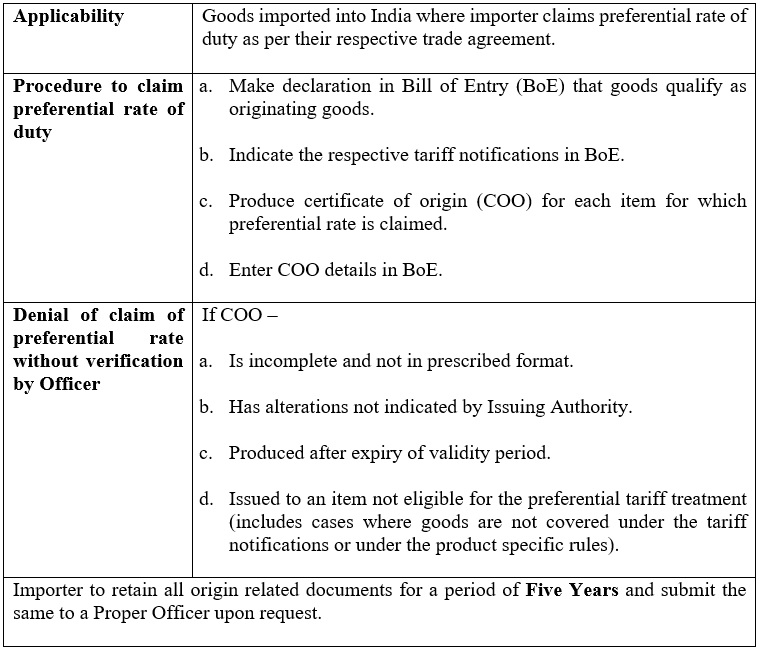

PREFERENTIAL RATE OF DUTY

Any importer importing goods, in general, is required to provide documentation to validate the origin of the imported good. Those importers who are part of any Trade Agreement are permitted to claim a preferential rate of duty under which the said imported goods may be imported.

Section 4 of the Customs Tariff Act, 1975 differentiates the circumstances under which a standard rate and a preferential rate of duty is levied on imported goods. It states that a standard rate of duty shall be levied on goods imported, unless the importer claims for the product to be produced or manufactured in a preferential area, as declared by the Central Government by way of Notifications, making it eligible for preferential rate of duty.

In order to receive preferential treatment every importer must make a specific claim for preferential rate for imports and must make sure the goods are produced or manufactured in such preferential area.

LAW AT PRESENT

Section 28DA of the Customs Act, 1962 was inserted by way of Section 110 of the Finance Act, 2020. It describes the procedure regarding claim of preferential rate of duty and states that any importer making a claim for such preferential rate of duty, must make a declaration that the specified goods qualify for preferential rate and furnish such information as per the Rules provided.

Further, the Proper Officer can seek further information if not satisfied with the details provided and in case the importer fails to provide the same, further verification may be sought.

CAROTAR, 2020

Prior to introduction of the aforesaid Section, the aspect of Certificate of Origin was regulated by Instruction No. 31/2016 –Cus dated September 12, 2016 issued by the Central Board for Indirect Taxes and Customs (‘CBIC’) regarding the implementation of Rules of Origin under Free or Preferential Trade Agreements and the verification of the preferential Certificates of Origin. The said Instructions, in detail, discussed the verification process of the signatures and seals present in the origin certificates and in various other cases.

This Instruction was superseded by the Circular No. 38/2020 – Cus in 2020 issued on August 21, 2020 which detailed the guidelines regarding the implementation of section 28DA of the Customs Act, 1962 and CAROTAR, 2020.

CAROTAR was notified by way of Notification No. 81/2020 – Customs (N.T.) and came into force from September 21, 2020. Key points detailed in the said Rules have been briefly laid down below. The same shall come in handy for any importer claiming a preferential rate of duty:

Details to be provided by Importer:

Information and further documentation may be sought by the Officer if he has reason to believe that the origin criteria have not been met. The procedure for the same is as follows-

Verification Request

- Request for verification of COO may be made by the Officer where –

i) there is a doubt regarding the authenticity of the COO if there is a mismatch of signature or seal with the specimen received from exporting country.

ii) COO criterion has not been met.

iii) verification is undertaken on a random basis. - Timeline followed for verification –

i) As per respective trade agreement, or

ii) In the absence of such agreement, 60 days from date of request. - Upon initiation of verification process –

i) Preferential Tariff Agreement shall be suspended till conclusion of the verification.

ii) Officer may provisionally assess and clear the goods, upon request of importer, only if importer furnishes a security amount equal to the difference between the duty provisionally assessed and the preferential duty claimed. - On temporary suspension, the Officer may inform the Issuing Authority of such development and seek information regarding the origin of the goods. On production, if the Officer is satisfied with the same, he may restore the Preferential Tariff treatment.

- Upon receiving the requisite information within the timeline, the Officer shall conclude the verification within 45 days of receipt of information, or the extended period as permitted by the Principal Commissioner or Commissioner of Customs.

- Any request for verification to be made within five years from the date of claiming preferential rate.

Rejection of Identical Goods –

- In case goods imported do not meet the origin criteria as per the Rules prescribed for every Trade Agreement, the Principal Commissioner of Customs or the Commissioner of Customs may, without further verification, reject prior claims of preferential rate for identical goods imported by the same exporter or producer.

- The Commissioner may restore the preferential tariff treatment on identical goods with prospective effect, after it is demonstrated by way of documents, that the manufacturing or other origin related conditions have been modified by the exporter or producer so as to fulfill the origin requirement as per the Rules prescribed for every Trade Agreement.

In situations where there is non-compliance of CAROTAR by the importer, the Authority shall have the power to confiscate the disputed goods and temporarily suspend the preferential tariff treatment.

Additionally, in case of any conflict between a provision of CAROTAR and a provision of the Rules notified for every Trade Treatment, the provision of the Rules of that said Trade Agreement shall prevail to the extent of the conflict.

ISSUES THAT PERSIST

There still persists a mandatory requirement for an importer in India to demonstrate a minimum of 35% of value addition that have been made on goods by the exporting country. Importers in India may face difficulty in trying to prove the genuineness of the Certificate of Origin obtained. The uncertainty of the importer must also be kept in mind, since they are merely going by the exporter’s declaration provided.

Additionally, with the requirement of providing the origin related documents to the Customs Authorities when sought for, the same may cause a challenge since such exporters may be reluctant to share their commercial or confidential information with the Authorities.

CONCLUSION

The Government has their heart in the right place by implementing CAROTAR strictly in order to avoid any kind of violation and malpractice. A huge obligation, however, is cast upon the importer to maintain documentation with respect to the origin of the said imports with utmost care.

Chamber Vlog & GST Web Series

To view all the videos in the Chamber Vlog series and other informative contents from the Chamber, please go to the Cochin Chamber’s YouTube Channel.

The most recent ones are added to the video players below. We will keep uploading new and relevant content for our members and the industry in general.

Kindly share these videos with your networks and subscribe to our YouTube Channel for more informative content.

3 Years of GST

Part - 1

3 Years of GST

Part - 2

3 Years of GST

Part - 3

Chamber Vlog - 19

Evolution of Title Deeds: Bamboo to Digital

Tax and Regulatory Updates from PricewaterhouseCoopers

Regulatory

Companies (Acceptance of Deposits) Rules, 2014 amended to provide relaxation of acceptance of deposits by start-ups

The Ministry of Corporate Affairs (MCA) has amended the Companies (Acceptance of Deposits) Rules, 2014 (Deposit Rules) prescribing certain relaxations for deposits received by start-up companies.

Exemptions for “start-up company”

The MCA has amended the Deposit Rules in the following manner:

- Earlier, the Deposit Rules had prescribed that an amount received by a start-up company via a convertible note will not be considered as deposit if it is convertible into equity shares or repayable within a period not exceeding five years from the date of issue. Now, with this amendment, this time period of conversion or repayment has been increased to ten years, thereby, enabling a start-up company to raise money with a longer tenure.

In addition, the concept of “start-up company” for the purpose of the above clause, has been changed and is now to be recognized in accordance with the notification issued by the Department for Promotion of Industry and Internal Trade.

- Earlier, the Deposit Rules had prescribed that the restriction on the maximum amount of deposits accepted or renewed by a company from its members will not apply to a private limited company that is a start-up, for five years from the date of its incorporation. Now, pursuant to the current amendment, this time period has been extended to ten years from the date of incorporation of the private company, which is a start-up.

PwC comments: These amendments provide relaxation of acceptance of funds by start-up companies, thereby, allowing them some more headroom to raise funds without attracting the provisions of Deposit Rules and the compliance thereunder.

Amendments widening the scope of CSR activities under the Companies Act, 2013

The Ministry of Corporate Affairs has amended the Companies (Corporate Social Responsibility Policy) Rules, 2014 (CSR Rules) and Schedule VII of the Companies Act, 2013 vide Gazette Notifications dated 24 August 2020, widening the scope of corporate social responsibility (CSR) activities by including Research and Development (R&D) activities for new vaccines, drugs and medical devices related to COVID-19 in collaboration with the institutes mentioned in Schedule VII.

Following amendments are made in the Companies (Corporate Social Responsibility Policy) Rules, 2014

- A proviso has been added to the definition of “CSR Policy,” stating that a company engaged in R&D activity of new vaccines, drugs and medical devices in its normal course of business may undertake R&D activity for new vaccines, drugs and medical devices related to COVID-19 for financial years 2020-21, 2021-22 and 2022-23 subject to the following conditions:

- such R&D activities shall be carried out in collaboration with any of the institutes or organisations mentioned in item (ix) of Schedule VII of the Companies Act, 2013; and

- the details of such activity shall be disclosed separately in the annual report on CSR included in the Board’s Report.

- In Rule 4(1) of the CSR Rules, the words “excluding activities undertaken in pursuance of its normal course of business” are omitted.

- In Rule 6(1) of the CSR Rules, the first proviso, which states, “Provided that the CSR activities does not include the activities undertaken in pursuance of normal course of business of a company”, has been omitted.

Following amendments are made in Schedule VII of the Companies Act, 2013

- The list of activities for CSR expenditure has been expanded. Contributions to incubators or R&D projects in the field of science, technology, engineering and medicine, funded by the Central Government or State Government or Public Sector Undertaking or any agency of the Central Government or State Government shall also be counted towards CSR.

- Contributions made to autonomous bodies established under the Department of Pharmaceuticals and AYUSH will also be considered as CSR contributions.

PwC comments: These amendments will help increase the permissible avenues of CSR contributions and will encourage corporates to channel CSR funds towards R&D activities for developing new vaccines, drugs and medical devices related to the cure of COVID-19.

Transfer Pricing

CBDT publishes detailed guidance on MAP

The Central Board of Direct Taxes (CBDT) recently published detailed guidance (Guidance) on the Mutual Agreement

Procedure (MAP). The Guidance is a follow-up on the recent amendments to Rule 44G of the Income-tax Rules, 1962 (Rules) and the omission of Rule 44H of the Rules, which were notified a few months ago, and which dealt with the procedure for filing an application for and giving effect to a MAP. At several instances, the Guidance echoes the mandate of Rule 44G of the Rules and also the requirements of the amended Form No. 34F [which have been effective from the date of the notification, i.e., 6 May 2020, and apply to all MAP cases pending with the Competent Authorities (CAs) of India as on such date].

The CBDT has issued the Guidance for the benefit of taxpayers, tax practitioners, tax authorities, and CAs of India and tax treaty partners of India.

The Guidance has been essentially published in response to the recommendations proposed by the MAP Peer Review Report on India (Stage 1) undertaken pursuant to the OECD’s BEPS Action Plan 14, which is a minimum standard agreed to be implemented under the OECD’s BEPS Project. This Action Plan has been endorsed by the G-20 countries of which India is also a part. The MAP Peer Review report had recommended that the countries implementing Action 14 should publish clear rules, guidelines and procedures on access to and use of MAP.

While several aspects of the Guidance have been largely followed in practice, there are other aspects that are new. Our focus here is largely on such new aspects that emerge from this Guidance, which are particularly relevant from a taxpayer’s standpoint (and are over and above the provisions of Rule 44G of the Rules and the requirements of Form No. 34F).

2. KEY NEW ASPECTS EMERGING FROM THE GUIDANCE

2.1 Time limit for making a MAP application before the CAs

In most Double Taxation Avoidance Agreements (tax treaties) of India, the time limit for making an application for MAP is within three years from the first notification of the action giving rise to double taxation. Limited number of tax treaties have a time limit which is not three years. Wherever it is so, it is expected to be changed to three years as per the minimum standard outlined in the final report of the BEPS Action Plan 14 and also the subsequent recommendation contained in the MAP Peer Review report.

Observation: The CBDT has clearly expressed its intention to align the time limit provided in all the tax treaties for submitting the MAP application to three years, either through the Multilateral Instrument (MLI) or through bilateral negotiations with the tax treaty partners.

However, where the time limit is more than three years, the Guidance seems to contradict the provisions of the MLI. Based on a reading of the MLI provisions on MAP, if a covered tax agreement provides for a time limit of more than three years – then, there will be no change in this timeframe as a result of the MLI coming into force. The three-year timeframe would be substituted only in those covered tax agreements where the time limit is shorter than three years. Therefore, to this extent, the Guidance seems to be conflicting with the MLI.

2.2 Time frame for resolving a MAP case

As per Rule 44G of the Rules, the CA in India shall “endeavor” to arrive at a MAP resolution within an average time period of twenty-four months (which is also in line with the MAP Peer Review report). In this regard, the Guidance categorically clarifies that the commitment is not to resolve MAP cases within such timeframe but “endeavor” to do so.

Further, the Guidance also states that the period of twenty-four months is to be computed from the “start date” of a MAP case. However, the Guidance further clarifies that since most MAP cases before the CAs of India arise from a MAP application made by a non-resident taxpayer before the CAs of other countries or specified territories (tax treaty partners), the “start date” is determined by the other CAs. If the CAs of India receive intimation of MAP cases from the CAs of the tax treaty partners much beyond the “start date” – that would result in delaying the endeavor to resolve such MAP cases within twenty-four months.

Observation: The CBDT has distinguished between “commitment to resolve MAP cases” versus “commitment to endeavor to resolve MAP cases” within twenty-four months. While this was quite apparent from Rule 44G of the Rules, by highlighting this distinction in the Guidance the CBDT seems to have been extra cautious in this regard.

Moreover, the CBDT has also explained a practical challenge and an uncontrollable reason for a possible delay beyond twenty-four months from the “start date”. However, such a delay as contemplated by the CBDT may not arise because of the definition of “start date” as provided in OECD’s jurisdiction wise MAP statistics for India , as per which the start date “for MAP cases which are invoked by the other Competent Authority, is the date of receipt of MAP invocation letter from the other Competent Authority in the office of the Competent Authority.”

2.3 Access to MAP, although negotiation curtailed in certain circumstances

The Guidance has stated that, in certain circumstances, access to MAP would be provided, however, the Indian CAs would not negotiate any outcome other than that already agreed/ concluded under such circumstances.

These circumstances are as follows:

a) Unilateral Advance Pricing Agreement (UAPA): For a concluded UAPA , the Indian CAs would rather request the CA of the foreign jurisdiction to provide for correlative relief but would not change the terms and conditions of the UAPA. However, in situations where the UAPA negotiation is in-process, the Indian CAs would allow access to MAP but they would not process such MAP cases until the UAPA is concluded.

Observation: For a concluded APA, this position of the CBDT was, in essence, articulated way back in CBDT’s initial guidance on APAs (i.e., in the publication titled “Advance Pricing Agreement Guidance with FAQs”). This seems rational because providing a parallel MAP benefit for a transaction covered by a concluded UAPA may tantamount to CAs of India agreeing to undertake negotiation vis-à-vis their own initially agreed positions – and clearly, any other outcome in any such negotiation would be self-contradictory.

However, a question that may arise is as to how would a concluded UAPA, coupled with a MAP access for correlative relief, be different from a bilateral APA. Although a bilateral APA has a much wider scope than only granting a corresponding relief, the Guidance does not seem to address this aspect.

b) Safe Harbour: When an Indian or foreign taxpayer applies for safe harbour provisions (as applicable) on its international transactions, and the return of income is accepted by the tax authorities of India9, then the Indian CAs would rather request the CAs of the tax treaty partners to provide for correlative relief. However, they would not change the arm’s length price of the international transactions covered under the safe harbour provisions.

Observation: There seems to be an apparent conflict with Rule 10TG of the Rules, as per which, a taxpayer applying safe harbour provisions would not be entitled to invoke MAP at all, whereas the Guidance does provide access to MAP at the outset, but with the added condition that the arm’s length price of the international transactions covered under the safe harbour provisions would not change.

Apart from this apparent conflict, in principle, it seems rational to not provide the benefit of negotiation under MAP for a transaction to which safe harbour provisions have already been applied and accepted, as this would tantamount to CAs of India agreeing to undertake negotiation vis-à-vis pricing outcomes that have already been provided to be arm’s length by the CBDT itself – clearly that would contradict CBDT’s position.

c) An order issued by the Income-tax Appellate Tribunal (Tribunal): There could be instances where the Tribunal

passes an order in respect of the same disputes that are also being examined under MAP. As per the Guidance, in such situations, since the Tribunal is an independent statutory appellate body, which is outside the administrative jurisdiction of the Indian tax authorities; and is the highest fact-finding body on tax matters, the CAs in India shall not deviate from the orders of the Tribunal for the relevant year where the dispute is decided on merits (this would apply even if the Tribunal order is passed after a MAP is concluded, but before it is implemented). In such cases, the CAs of India would request the CAs of the tax treaty partners to provide correlative relief. However, this does not apply to Tribunal orders setting aside the matters for being adjudicated afresh.

Observation: This has been a contentious matter in the past between the CAs of India and taxpayers that are already in the MAP process or are applying for MAP. Practically speaking, the CAs of India have been following this stance, which now also forms part of the Guidance. In the past, taxpayers have been contending that since MAP is an alternate tax dispute resolution mechanism available to taxpayers under the tax treaty, whereas any resolution by the Tribunal would be under domestic law – the latter should not override or curtail the former, and hence, a Tribunal verdict should not prevail over a MAP outcome. However, the CBDT’s perspective on this matter seems quite apparent from the Guidance, which is in essence, to keep the Executive body of the Government of India (i.e., the office of the CAs of India in the instant case) distinct from its Legislature/ Judiciary (i.e., forums like the Tribunal), and to keep them both within their respective domains and realm of powers.

It should be noted that this position would apply only on a year-to-year basis, i.e., a Tribunal order of, say Year 1 cannot impact the MAP proceedings of say Year 2 – the impact, as articulated in the Guidance, can only be on the MAP proceedings of Year 1.

Overall observation: A question that may arise is, if the negotiation cannot eventually go beyond what has been agreed/concluded in all the above circumstances, then, what could be the purpose of providing access to MAP at all in the first place. Notably, the purpose seems to have been coded in the Guidance itself, which is to obtain correlative relief from the CAs of the tax treaty partners, which can happen only through a MAP.

2.4 Denial of access to MAP

The Indian CAs can deny access to MAP in the following situations:

a) in case of delay in filing of MAP application by the taxpayer, i.e., beyond the expiry of the stipulated time period;

b) if the Indian CAs reach a conclusion that the objection raised by the taxpayer on the action taken by tax authorities is not justified – however, before reaching such a conclusion, the Indian CA should discuss this with the taxpayer and the CAs of the tax treaty partners;

c) in case of incomplete MAP applications/ documents/ information – the Guidance stipulates that a time period of 30 days shall be provided for remedying the errors/ defects in the MAP application, and a time period of 90 days shall be provided for submitting additional information/ documents;

d) where issues sought to be covered under the MAP application have already been either: (i) settled, or (ii) have been admitted, or (iii) are under examination by the Income-tax Settlement Commission or the Authority for Advance Rulings; or

e) in case of issues that are purely governed by India’s domestic law and arise due to implementation of India’s domestic legal provisions.

2.5 Multilateral MAP

In addition to the bilateral MAP process, in some cases (subject to certain conditions), the CAs of India can participate in multilateral MAP discussions with more than one tax treaty partner. Multilateral MAP cases shall involve similar processes on a multilateral basis amongst the CAs concerned, as are followed in a bilateral MAP case (such as exchange of position papers, negotiations, finalisation of mutual agreements, etc.). However, a multilateral MAP case shall be executed in the form of a series of parallel bilateral MAP cases.

Observation: Practically, multilateral MAPs are not common. However, they are just as feasible under tax treaty provisions as are bilateral MAPs. With the supply chains of a multinational group spread across the globe, and particularly with the OECD’s Pillar 1 and Pillar 2 projects on the anvil, there is an increased likelihood of a dispute impacting multiple countries, in which case, a multilateral MAP (besides a multilateral APA) would be the way forward.

2.6 Downward adjustment in a MAP settlement

The CAs of India are required to adhere to the provisions of section 92(3) of the Income-tax Act, 1961 (Act) in respect of adjustments made by Indian tax authorities. This implies that in a MAP negotiation the Indian CA cannot accept an outcome that results in a downward adjustment of the income declared by the Indian taxpayer in its return of income for the relevant year (returned income). However, in respect of MAP cases involving adjustments made by the tax authorities of other countries, the Indian CA may go below the returned income of the Indian taxpayer.

Observation: Adherence to the provisions of section 92(3) of the Act in respect of MAP cases involving adjustments made by Indian tax authorities, is also in effect mandated under Rule 44G(5) of the Rules. However, this sub-rule is silent on any such mandate in respect of MAP cases involving adjustments made by tax authorities of other countries. The Guidance has, however, clarified that a downward adjustment may be made in such cases. Quite apparently, this stands in contradiction to the provisions of section 92(3) of the Act. However, the Guidance has stipulated so, possibly to facilitate a level-playing and equitable negotiation that does not reach a “dead-end”, which may not have been possible to achieve in such cases if the Indian CAs were to be bound by section 92(3) of the Act.

2.7 Coverage

a) The Guidance stipulates that taxpayers will be able to opt for MAP even in situations where the Indian tax authorities have applied domestic anti-abuse provisions.

Observation: This was one of the recommendations provided under the MAP Peer Review report. As per this report, in order to protect taxpayers from arbitrary application of anti-abuse provisions in tax treaties and in order to ensure that CAs have a common understanding on such application, taxpayers should have been given access to MAP. Access to MAP was also considered important to avoid cases in which the application of domestic anti-abuse legislation is conflicting with the provisions of a tax treaty.

b) The Guidance also specifically provides that where obligation to deduct tax at source on payment made by an Indian entity to a non-resident entity is enforced by an order passed under section 201 of the Act and the same is disputed by the non-resident entity, MAP access will be provided to such non-resident entity. However, such action being purely under the domestic law and the order under section 201 of the Act not being an order determining any tax on income, the MAP discussion will be taken up only after the assessment order is passed in the case of the non-resident taxpayer.

Observation: The Guidance provides a two-level access to MAP for the non-resident taxpayer – (i) level one: based on an anticipated event of double taxation that could arise from the order under section 201 of the Act; and (ii) level two: the MAP will be negotiated only when an assessment order has been passed in the case of the non-resident. It is peculiar that access to MAP is given to a non-resident taxpayer based on an order under section 201 of the Act which is passed on a resident taxpayer. However, such a MAP would not be concluded unless an assessment of the non-resident is completed pursuant to such order under section 201 of the Act. Thus, even if a non-resident files a MAP application based on the order under section 201 of the Act (level one), the same could become infructuous, if the non-resident’s return is not selected for assessment.

Further, section 201 of the Act does not provide a time-limit for completion of the proceedings with respect to transactions with the non-resident. In that case, if a proceeding under section 201 of the Act is initiated beyond the time limit for regular assessment in respect of the non-resident, then no relief could be sought under MAP.

3. OTHER IMPORTANT ASPECTS

The aspects listed below have been practically followed in the past, but are now incorporated as part of the Guidance:

- Recurring issues: The Indian CAs may resolve cases involving recurring issues based on the same principles as were adopted in a prior MAP resolution. However, they cannot prevent tax authorities from making adjustments which are not in line with prior MAP resolutions in case of the same taxpayer and with respect to the same issues.

Observation: A specific mention of this in the Guidance may, to some extent, erode the persuasive value of a MAP resolution that taxpayers may often rely on in proceedings before tax authorities.

- Interest and Penalties: These are to be administered under the domestic laws and hence, the Indian CAs do not have any mandate to consider these issues. Where the amount of interest and penalties are linked to the quantum of income, such interest and penalties shall be varied in the same proportion as the variation in the quantum of income due to a MAP resolution, in accordance with the domestic law

- Secondary Adjustments: The Indian CAs would be obligated to make secondary adjustments part of the MAP resolution in respect of cases pertaining to financial year 2016-17 or thereafter. ● Bilateral and Multilateral APAs: In respect of issues for which a bilateral or multilateral APA application has already been filed and accepted, MAP applications on the same issues for the same years should not be made by taxpayers