President's Note

Dear Friends,

Since the very beginning, the Cochin Chamber has been involved in the advancement of several public causes in the State apart from its regular activities. We have always sought the progress of the business community and to making contributions to the society that we live in. In this context, the Cochin Chamber of Commerce & Industry has come out with a Briefing Book Entitled ‘Rebuild Kerala’ – Seeking Solutions: People, Policy and Progress, Chamber Perspective” which is aimed at supplementing the Government of Kerala’s Nava Keralam efforts towards a mission mode of development. This Report was released at the time of the CEO Forum Breakfast Meeting earlier this month.

This document, prepared by the Research Cell in the Chamber, is aimed at helping the prioritization of reforms in different fields to strengthen the foundations of the Nava Keralam establishment process.

The United Nations in its report Kerala Post–Disaster Needs Assessment (Floods and Landslides) August 2018 had suggested the need for a ‘broad policy framework’ which provides a coherent narrative and binds all the sectors to a common vision of Nava Keralam.

Our report is a step in this direction. The report is based on three pillars i.e. people, policy and progress, hence the title- Seeking Solutions- People, Policy and Progress, Chamber’s Perspective. We have listed 40 reforms

categorized under nine chapters relating to innovation, ease of doing business, agriculture, education, health, tourism, governance, environment, etc. The different Chapters explain the status quo and suggest interventions with the help of relevant resources and best practices. Our report emphasizes the need for upgrading the State’s industrial competitiveness, facilitating innovation and promoting participatory governance among other things. We have emphasized on the sustainable development aspect in every intervention we have suggested.

We hope to initiate a conversation with the Government on the need for structural reforms and to cooperate in facilitating the Nava Keralam process for a better tomorrow.

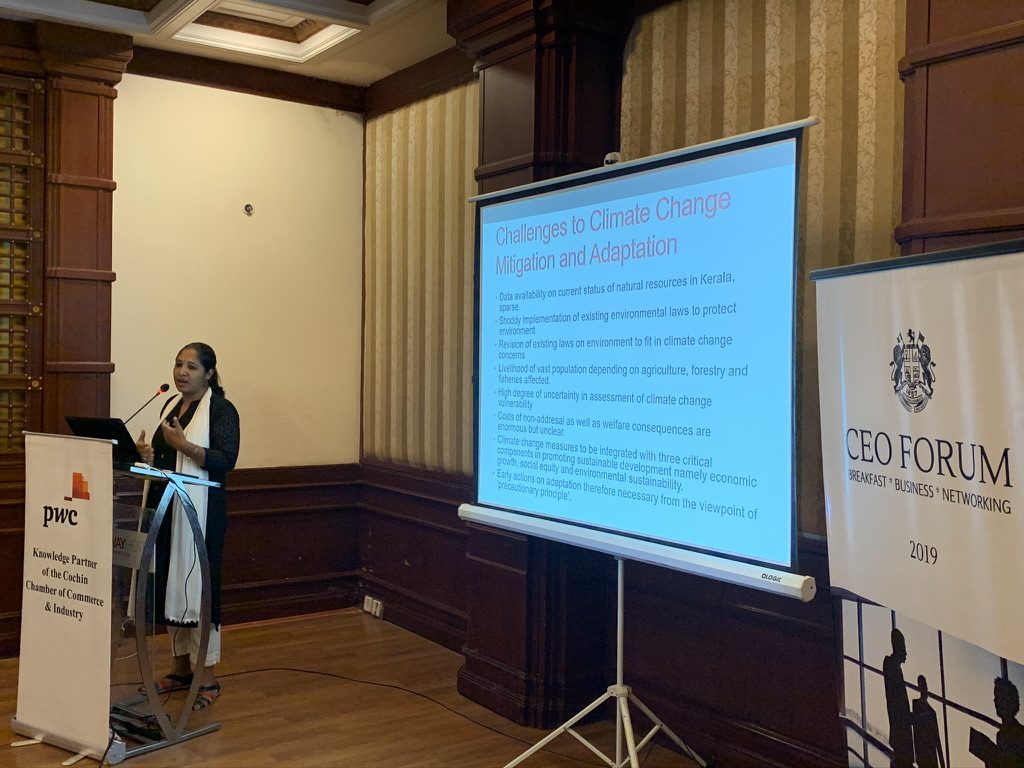

The 10th CEO Forum Breakfast Meeting was conducted on the 4th of October 2019. This time around, the Guest Speaker was Ms. Shyama Kuriakose, Senior Project Fellow (Environment Law), Vidhi Centre for Legal Policy, New Delhi who spoke on “Climate Change in Kerala – A Way Forward for Collective Action.” The Forum discussed the importance of recognizing climate change as an important factor and how to tackle the climate change problem at the larger level of discourse. Ms. Kuriakose insisted that for countries like India, the focus should be on ‘adaptation’, or measures taken to cope with the inevitable effects of climate change that has already happened, such as nasty storms, floods, and droughts. Using the example of the recent floods in Kerala, the forum discussed its impacts and the possible measures to reverse the potential damage.

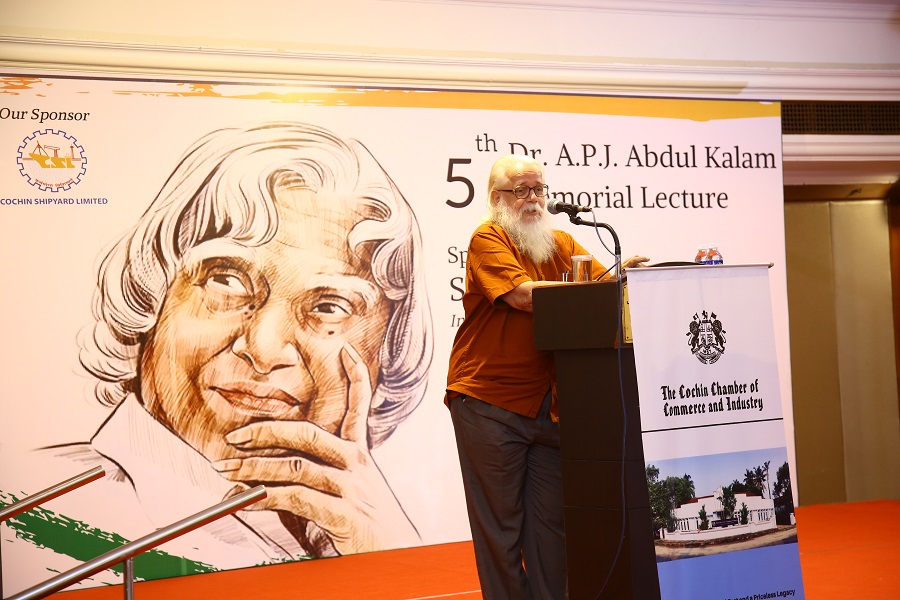

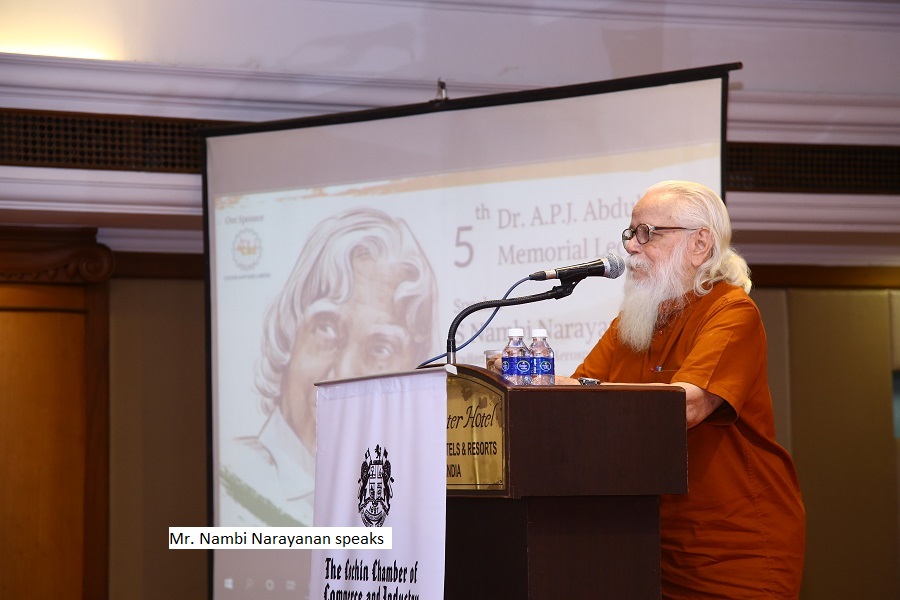

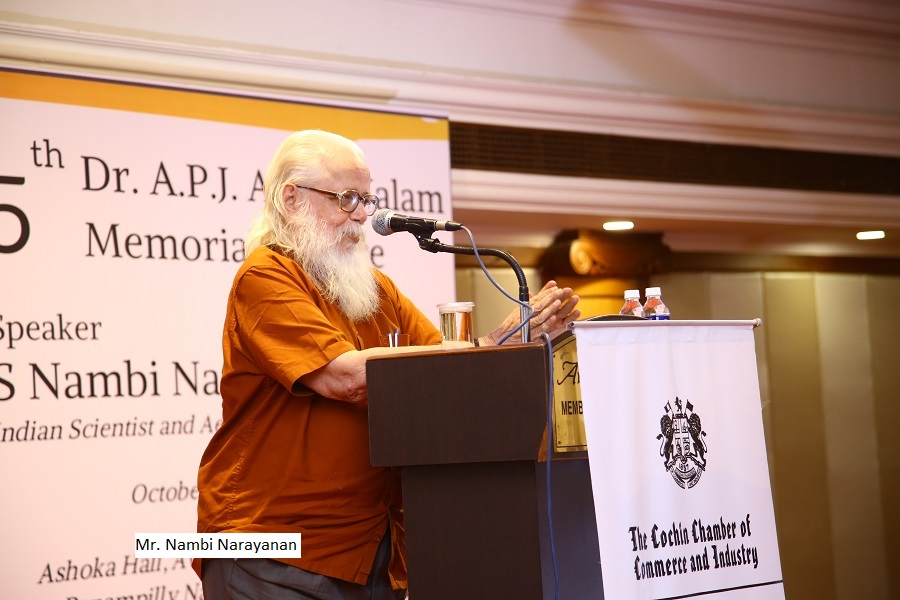

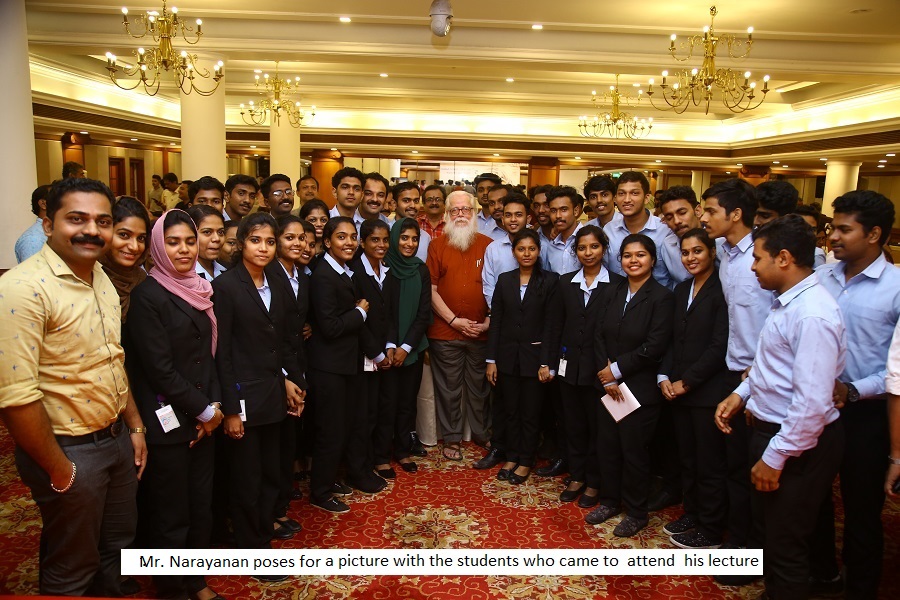

The Chamber conducted the 5th Annual Dr. A.P.J Abdul Kalam Memorial Lecture on the 18th of October 2019. Renowned Indian Scientist and Aerospace Engineer Mr. S Nambi Narayanan was the Guest Speaker on the occasion. It was an honour for the Chamber to have hosted such an eminent personality. We could not have asked for a better person to deliver the Lecture this year.

In his address, Mr. Nambi Narayanan spoke about the Rocket Engineering Division (RED) which Dr. Kalam headed. He said that Kalam was a person of great abilities who could think in ways which no one else could and outlined the story of the Dreamer 2 rocket which was Dr. Kalam’s dream. He also spoke on the international scenario concerning space technology and where we stand today.

The programme was attended by over 200 people including seniors in the Industry and Students from different institutions.

Detailed reports along with pictures of these programmes are carried elsewhere in this issue of this Newsletter.

The 11th Breakfast Meeting under the aegis of the Chamber’s CEO Forum 2019 will be held on Friday, the 1st of November 2019. The Speaker at this Session will be Mr. Ravi Tennety, Chief Executive Officer – Training and Skilling Division, Quess Corp Limited, Bangalore who will speak on “Skilling – The Engine of the Economy.”

There is an increased focus from the Government’s side on curbing tax evasion and bringing in more transparency to the entire GST system. The new return formats and e-invoicing are expected to trigger a huge shift in the way GST compliances are carried out and would also have a great impact on the IT systems.

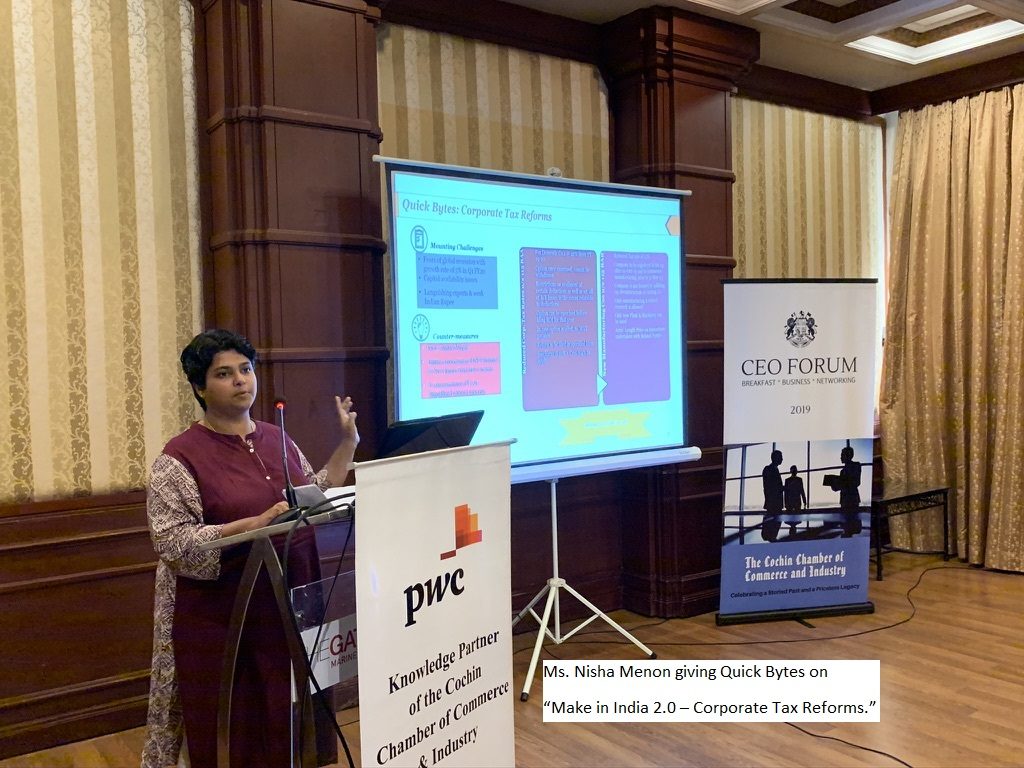

In thus connection, the Chamber will be organizing a Half-Day Session on GST – Upcoming Changes, Legislative, Legal and other updates on the 8th of November 2019. The Speakers for this Session will be Mr. Kunal Wadhwa, Partner, Indirect Tax, PwC India, Bangalore, and Ms. Nisha Menon, Director, Indirect Tax, PwC India, Cochin. I trust that all of you will make use of these opportunities in the best possible manner.

We are in the process of scheduling various programmes for the coming months. The details of the programmes, once finalized, will be shared with you all in due course.

Wishing you all the very best of this Diwali Season!

V Venugopal

Quote

Advertise here!!

Recent Events

10th CEO FORUM Breakfast Meeting - 2019

Climate Change in Kerala: A Way Forward for Collective Action | 04.10.2019

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s 10th Breakfast Meeting on Friday, 4th October, 2019 at the Taj Gateway Hotel, Ernakulam.

Mr. V Venugopal, President of the Chamber, delivered the Welcome Address and introduced the Speaker for the meeting.

Ms. Shyama Kuriakose, Senior Project Fellow (Environment Law), Vidhi Centre for Legal Policy, New Delhi spoke on “Climate Change in Kerala: A Way Forward for Collective Action” in the light of the natural calamities that ravaged Kerala for two consecutive years.

The Forum discussed the importance of recognizing climate change as an important factor and how to tackle the climate change problem at the larger level of discourse.

Ms. Kuriakose said that the latest reports on the impact of global warming from the Intergovernmental Panel on Climate Change has warned that without substantial cuts in carbon dioxide emissions, the world will reach the threshold of 1.5°C warmer than preindustrial levels as early as in 2030. The increased flood risks are alarming, especially their impact on vulnerable populations with low coping and adaptive capacities.

In particular, floods can have a long-run impact on health which in turn will deteriorate human capital, a key driver of sustainable development, she said. Using the example of the recent floods in Kerala, the Forum discussed its devastating impact and the possible measures to reverse the potential damage.

Ms. Kuriakose listed out the aftermaths of climate change namely alteration of hydrological cycles, increased frequency of tropical cyclones, rise in communicable diseases, physical damage to infrastructure and resultant costs etc.

Ms. Kuriakose also spoke on the UNFCC, the Convention which acknowledges the vulnerability of all countries to the effects of climate change and their special efforts to ease the consequences, especially in developing countries. One of the three Rio Conventions, the UNFCCC’s ultimate objective is to achieve the stabilization of greenhouse gas concentrations in the atmosphere at a level that would prevent dangerous interference with the climate system, she added.

Ms. Kuriakose insisted that for countries like India, the focus should be on ‘adaptation’, or measures taken to cope with the inevitable effects of climate change that has already happened, such as nasty storms, floods and droughts. The goal of mitigation is to avoid significant human interference with the climate system, and stabilize greenhouse gas levels in a timeframe sufficient to allow ecosystems to adapt naturally to climate change, whereas the goal of adaptation is to reduce the vulnerability to the harmful effects of climate change, she said.

Ms. Kuriakose said that adaptation planning and investments must include the private sector as it can mobilize financial resources and technical capabilities, leverage the efforts of governments, engage civil society and community efforts, and develop innovative climate services and adaptation technologies.

Ms. Nisha Menon, Director – Tax, PwC India gave ‘Quick Bytes on Make in India 2.0 – Corporate Tax Reforms.

Mr. V Venugopal along with the Research Team of the Chamber presented a Research Report “Rebuild Kerala – Seeking Solutions – People, Policy and Progress, Chamber Perspective” which advocates sectoral reforms in different fields to strengthen the foundations of the ‘Nava Kerala’ establishment process.

Ms. C S Kartha, Program Committee Chairman presented a Memento to Ms. Kuriakose.

Mr. K Harikumar, Vice President of the Chamber proposed the Vote of Thanks.

5th DR. A.P.J. ABDUL KALAM MEMORIAL LECTURE

18.10.2019

The Cochin Chamber of Commerce & Industry conducted the 5th Dr. A.P.J. Abdul Kalam Memorial Lecture on Friday the 18th of October, 2019, in Ernakulam.

Renowned Indian Scientist and Aerospace Engineer Mr. S Nambi Narayanan was the Speaker on the occasion.

The programme commenced with a Welcome Address by the President of the Cochin Chamber of Commerce & Industry, Mr. V Venugopal.

Mr. V Venugopal welcomed the audience and gave a brief introduction about the Cochin Chamber and the connection that the Cochin Chamber had with Dr. Kalam and why this Memorial Lecture series was started in the year 2015. Later in his address, Mr. Venugopal cited various examples that highlighted the qualities of Dr. Kalam which made him the ‘Peoples President’and the idol that he is today for the people of India. He also introduced Mr. Nambi Narayanan to the audience.

In his address Mr. Nambi Narayanan spoke about the Rocket Engineering Division (RED) which Dr. Kalam headed in the early days. He said that Kalam was a person of great abilities who could think in ways which no one else could. He outlined the story of the Dreamer 2 rocket which was Dr. Kalam’s dream. Failures never dampened Kalam’s spirits. For him failures were only a reason to try ever harder. Dr. Kalam was a man who thought ahead of his times, preparing for eventualities that seemed far-fetched at that time. Even though his thoughts and ideas that appeared vague and unattainable to his colleagues, they were actually the first steps to where ISRO is today. Dr. Kalam was an inspirational leader, humble to the core and affectionate to even those who did not agree with his ideas.

Mr. Narayanan then outlined his work on the Liquid Propulsion Technology in the early days. He also spoke about the international scenario with regard to space technology and where we stand today. Mr. Narayanan also outlined the strides taken by other countries like the US, Russia etc. in space technology advancements. The US is planning to put a man on the moon once again by 2024 and China plans to do so by 2030. Deep space exploration has caught the imagination of various countries….. moon landings, Mars exploration etc. However, Mr. Narayanan was of the firm view that no one country can do the job alone. He was of the view that countries need to collaborate in space exploration so as to manage technologies and funding issues. He said that in this scenario, an organisation like the Asian Space Agency which he is promoting, will be highly useful in this endeavour. India has the potential to reach outer space with the excellent technology and infrastructure that we have. The potential is huge and needs to be tapped. India cannot afford to be left behind. We need to push forward.

Thereafter, Mr. Narayanan answred the questions raised by people in the audience.

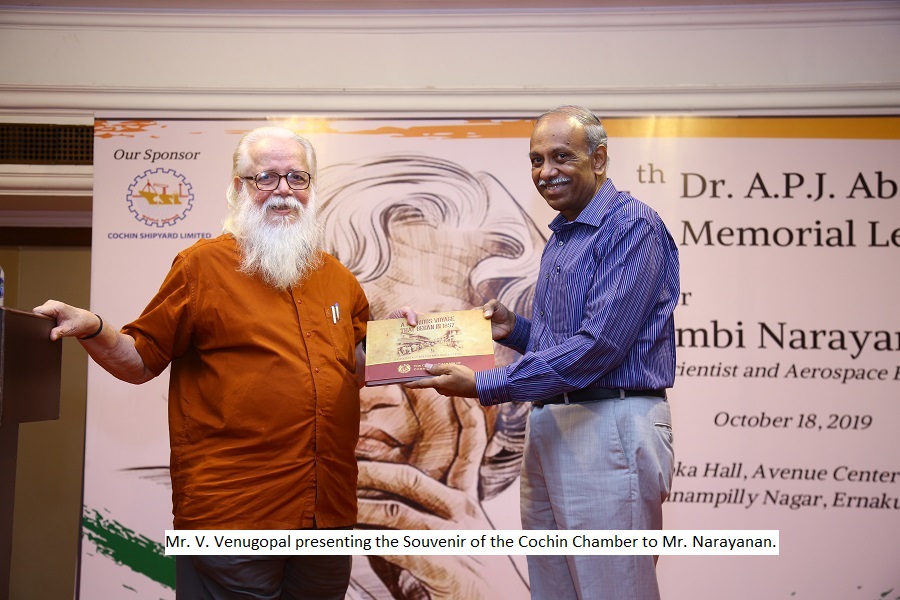

Mr. V. Venugopal, President of the Cochin Chamber of Commerce & Industry Presented a Memento to Mr. Nambi Narayanan.

Mr. K. Harikumar, Vice President of the Cochin Chamber delivered the Vote of Thanks and concluded the 5th Dr. A.P.J. Abdul Kalam Memorial Lecture.

Executive Committee Members 2019-2020

At the 162nd Annual General Meeting of the Cochin Chamber held on 27th of September, 2019, the following persons were elected to constitute the new Executive Committee for the year 2019-2020.

Mr. V. VENUGOPAL : PRESIDENT

Vice President – Legal,

Harrisons Malayalam Ltd.,

Mr. K. HARIKUMAR : VICE-PRESIDENT

Managing Director,

The Travancore-Cochin Chemicals Ltd.,

Mr. P.M. VEERAMANI : COMMITTEE MEMBER

Senior Partner,

RGN Price & Co.,

Mr. BIBU PUNNOORAN : COMMITTEE MEMBER

Director,

Medivision Scan & Diagnostic Research Centre Pvt. Ltd.,

Mr. P.S. MENON : COMMITTEE MEMBER

Managing Director,

Tropicana Logistics Private Limited.,

Mr. C.S. KARTHA : COMMITTEE MEMBER

Managing Partner,

Karthas Shipping Solutions

Ms. VINODINI ISSAC : COMMITTEE MEMBER

Managing Director,

Team One Advertising Company Pvt. Ltd.,

Mr. S.P. KAMATH : COMMITTEE MEMBER

Executive Director,

Amalgam Foods Limited.,

Mr. PRASAD K. PANICKER : COMMITTEE MEMBER

Executive Director-Refinery,

Bharat Petroleum Corporation Ltd.,

Mr. GULSHAN JOHN : COMMITTEE MEMBER

Managing Director,

Nedspice Processing India Private Ltd.,

Mr. DINESH P. THAMPI : COMMITTEE MEMBER

Vice President & DCH – Kerala,

Tata Consultancy Services

Mr. PRAVEEN THOMAS JOSEPH : COMMITTEE MEMBER

Chief Executive Officer,

India Gateway Terminal Pvt. Ltd.,

INDIA RANKS 63 IN WORLD BANK'S DOING BUSINESS REPORT. INDIA IMPROVES RANK BY 14 POSITIONS

The World Bank released its latest Doing Business Report (DBR, 2020) today on 24th October 2019. India has recorded a jump of 14 positions against its rank of 77 in 2019to be placed now at 63rdrank among 190 countries assessed by the World Bank. India’s leap of14 ranks in the Ease of Doing Business ranking is significant considering that there has been continuous improvement since 2015 and for the third consecutive year India is amongst the top 10 improvers. As a result of continued efforts by the Government, India has improved its rank by 79 positions in last five years [2014-19].

The Doing Business assessment provides objective measures of business regulations and their enforcement across 190 economies on ten parameters affecting a business through its life cycle. The DBR ranks countries on the basis of Distance to Frontier (DTF), a score that shows the gap of an economy to the global best practice. This year, India’s DTF score improved to 71.0 from 67.23 in the previous year.

India has improved its rank in 7 out of 10 indicators and has moved closer to international best practices (Distance to Frontier score). Significant improvements have been registered in ‘Resolving Insolvency’, ‘Dealing with Construction Permits’, ‘Registering Property’, ‘Trading across Boards’ and ‘Paying Taxes’ indicators. The changes in seven indicators where India improved its rank are as follows:

The important features of India’s performance this year are:

- The World Bank has recognized India as one of the top 10 improvers for the third consecutive year.

- Recovery rate under resolving insolvency has improved significantly from 26.5% to 71.6%.

- The time taken for resolving insolvency has also come down significantly from 4.3 years to 1.6 years.

- India continues to maintain its first position among South Asian countries. It was 6th in 2014.

(Source : PIB, GoI)

Chamber in the News

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

Taxation Laws (Amendment) Ordinance, 2019

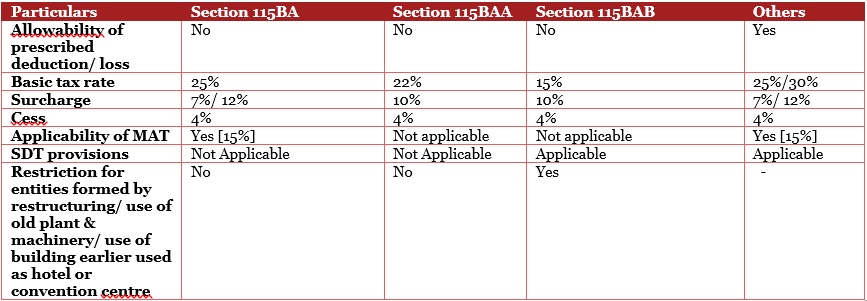

The Government promulgated the Taxation Laws (Amendment) Ordinance 2019, announcing key changes to corporate tax rates in the Income-tax Act, 1961 (Act). While existing domestic companies have been provided an option to pay tax at a concessional rate of 22%, new domestic companies set up on or after 1 October 2019, and commencing manufacturing before 31 March 2023, would have the option to pay tax at 15%2. However, the reduced tax rates come with consequential surrender of specified deductions/ incentives. No minimum alternate tax (MAT) would be applicable in either of these options. Companies that do not opt for the concessional tax rates will continue to enjoy the benefit of such specified deductions/ incentives, and where applicable, be subject to MAT at 15%

> Tax applicable for certain domestic companies [section 115BAA]

- Any domestic company has an option to pay tax at 22%, subject to the following conditions:

– The total income is computed without claiming prescribed deductions or set-off of loss [See computation mechanism].

– The option needs to be exercised within the prescribed time for filing the return of income (ROI) under section 139(1) of the Act for assessment year (AY) 2020-21 or subsequent AYs. - Once exercised, such option cannot be withdrawn for the same or subsequent AYs.

(with effect from AY 2020-21)

> Tax rate applicable for certain domestic manufacturing companies [section 115BAB]

Any domestic manufacturing company has an option to pay tax at 15%, subject to the following conditions:

- The total income is computed without claiming prescribed deductions or set-off of loss [See computation mechanism].

- Such company- Is incorporated on or after 1 October 2019, and commences production on or before 31 March 2023

– Is not formed by splitting up or reconstruction of business already in existence (exception provided for undertaking formed as a result of re-establishment, reconstruction or revival of business referred to in section 33B of the Act)

– Does not use plant and machinery previously used for any purpose in India and no depreciation has been claimed on the same (relaxation up to 20% allowed).

– Does not use any building previously used as a hotel or convention centre.

– Is not engaged in any business other than the manufacture or production of an article or thing and research in relation to or distribution of such article or thing manufactured or produced by it. - The option needs to be exercised before the due date as per section 139(1) of the Act for furnishing the first of the return of income for any previous year starting from AY 2020-21 or subsequent AYs.

- Once exercised, such option cannot be withdrawn for the same or subsequent AYs.

- Provisions similar to section 80IA(10) of the Act are made applicable for transactions between connected parties which has the effect of producing more than ordinary profit that might be expected to arise.

- Domestic transfer pricing provisions under section 92BA of the Act is being made applicable to such transactions. The corresponding amendment has been made in section 92BA of the Act to consider such transactions as specified domestic transactions (SDT) in order to bring it within the ambit of transfer pricing provisions.(with effect from AY 2020-21)

> Minimum Alternate Tax [section 115JB]

- Companies exercising the option under sections 115BAA or 115BAB of the Act have been excluded from the applicability of MAT.

- Tax rate under section 115JB of the Act has been reduced from 18.5% to 15%.

> Surcharge rates specified for sections 115BAA or 115BAB –

- For the purpose of advance tax the applicable surcharge rate on incomes chargeable to tax under sections 115BAA or 115BAB of the Act shall be at 10%.

> Amendments to existing section 115BA

- Corresponding amendments made to section 115BA of the Act to provide that it would apply to companies other than those mentioned in sections 115BAA and 115BAB of the Act.

- For a person exercising option under section 115BAB of the Act, the option under section 115BA of the Act may be withdrawn.

> Grandfathering of buy-back tax [section 115QA]

Tax on buy-back of shares (being shares listed on a recognised stock exchange) not applicable for shares for which the public announcement was made before 5 July 2019.

> Amendments on applicability of the enhanced surcharge rates on certain incomes

- The surcharge rate of 25%/ 37% introduced by the Finance (No.2) Act, 2019, shall not apply to capital gains arising on sale of equity share in a company or a unit of an equity oriented fund or unit of business trust referred to in sections 111A or 112A of the Act.

- The enhanced surcharge rate of 25%/ 37% shall also not apply to the income of foreign institutional investors (FIIs) from securities as referred to in section 115AD of the Act.

Computation mechanism: Prescribed manner of determining total income for the purpose of section 115BAA or section 115BAB

The total income of the company should be computed:

- Without claiming deduction under the following provisions:

- Section 10AA of the Act relating to SEZ.

- Additional depreciation allowance under section 32(1)(iia) of the Act.

- Section 32AD of the Act – Deduction for investment in new plant and machinery in notified backward States.

- Section 33AB of the Act –Tea/ coffee/ rubber development allowance.

- Section 33ABA of the Act – Site restoration fund.

- Sections 35(1) (ii), (iia), (iii) and 35(2AA), (2AB) of the Act – certain scientific research expenditure.

- Section 35AD of the Act – Deduction in respect of expenditure on specified business.

- Section 35CCC of the Act – Expenditure on agricultural extension project.

- Section 35CCD of the Act – Expenditure on skill development project.

- Deduction under Part C of Chapter VIA other than section 80JJAA of the Act (deduction in respect of employment of new employees).

- Without set-off of any loss carried forward from an earlier year to the extent that such loss is attributable to any of the deduction mentioned above. However, it would be deemed that full effect of the loss has already been given and no further deduction would be allowed for such loss in future.

- By claiming depreciation other than additional depreciation under section 32(1)(iia) of the Act determined in such manner as may be prescribed.

Snapshot:

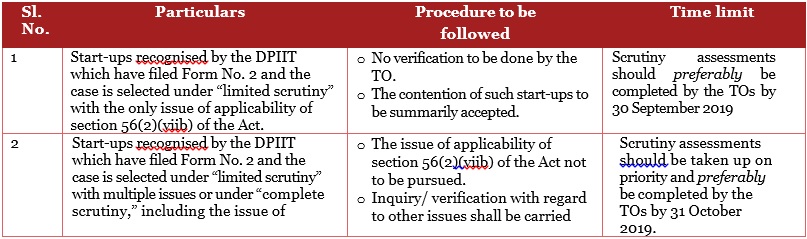

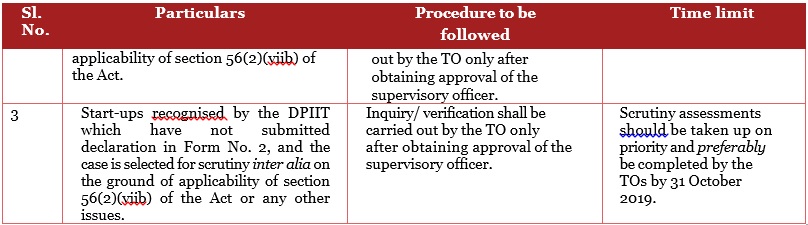

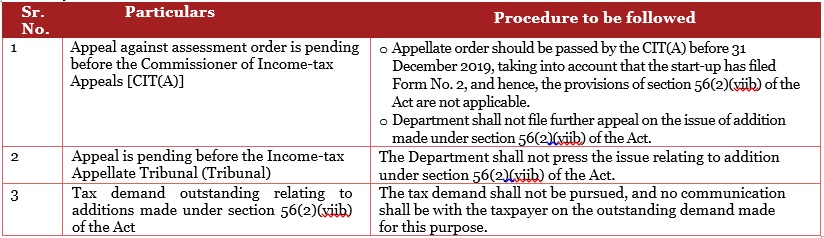

CBDT circular regarding assessment of start-ups

Section 56(2)(viib) of the Income-tax Act, 1961 (Act) provides that when a closely held company issues its shares at a premium, the excess of the share issue price over the fair market value of such shares, computed in accordance with the prescribed methodology, shall be subject to income-tax.

The Department for Promotion of Industry and Internal Trade (DPIIT), vide notification, and the Central Board of Direct Taxes (CBDT), vide notification (issued in pursuance of the DPIIT’s notification), have laid down that the provisions of section 56(2)(viib) of the Act shall not apply to any consideration received by a start-up company from a resident, if such company fulfils the conditions mentioned in para 4 of the notification issued by the DPIIT and files the prescribed declaration.

However, during assessment proceedings, Tax Officers (TO) are challenging the valuation of shares in relation to the funding received by start-ups. Scrutiny notices under sections 143(2)/ 147 of the Act have been issued before the issue of the DPIIT notification, or in many instances, even afterwards, challenging the applicability of section 56(2)(viib) of the Act to start-ups, which are pending disposal.

To provide a hassle-free environment for start-ups, the Finance Minister has made a series of announcements in her budget speech and thereafter. To give effect to those announcements, the CBDT issued various circulars/ clarifications in the last one month, and finally issued a consolidated circular in this regard followed by a Press Release. These circulars deal with matters relating to assessment of start-ups, time limit for completion of their pending assessments, procedure for addition made under section 56(2)(viib) of the Act in the past assessment, outstanding income tax demands and constitution of start-up cell

> Assessment procedure and timeline for completion

The procedure laid down in the circulars for proceedings under the Act are as follows:

> Procedure for addition made under section 56(2)(viib) of the Act in the past assessment and outstanding tax demand

Para 6 of the DPIIT’s notification restricted the benefit of notification and consequent exemption to start-up companies, wherein addition under section 56(2)(viib) of the Act has not already been made in the assessment order, before the date of issue of the said notification. This restriction caused difficulties to start-up companies where the TOs had already made such addition before 19 February 2019. The CBDT, vide circular, has relaxed para 6 and clarified that the notification will also be applicable to such start-up companies, provided the taxpayer has subsequently submitted a declaration in Form No. 2 that it fulfils the requisite conditions. The CBDT issued another press release on 10 August 2019, providing a combined clarification/ guidelines discussed in the circulars issued on 7 August and 9 August 2019 (as discussed above).

However, there remained an open question regarding the procedure to be followed in matters pending before appellate authorities/ stay of demand, which has been addressed by the latest combined circular issued by the CBDT.

In addition to providing these much-awaited and necessary clarifications, to redress grievances and address various tax related issues in the case of start-ups, the CBDT has constituted a start-up cell. The latest consolidated circular contains the details and contact numbers of the members.

PwC comments: The above circulars are a welcome step and in line with the Finance Minister’s assurance in her budget speech of special administrative arrangement for assessments of start-ups and to redress their grievances. Not only does this provide relief to eligible start-ups under scrutiny on the applicability of section 56(2)(viib) of the Act, but also to non-eligible start-ups to the extent that scrutiny shall be carried out after obtaining requisite approval.

Central Government notifies E assessment Scheme laying down procedure for electronic assessment

The Central Government, in its endeavour to eliminate face-to-face interaction between taxpayers and Tax Officers (TO), has notified the E-assessment Scheme, 2019 (scheme) which shall come into force on the date of its notification in the official Gazette. The scheme attempts to almost eliminate human interface and lays down a detailed step-by-step procedure for e-assessments. The Government has taken a step towards achieving its objective of faceless, speedy, hassle-free and fair conduct of assessment proceedings. The scheme discusses the setting up of e-assessment centres, various units (assessment, verification, technical, etc.) and lays down a procedure to carry out assessments seamlessly

> Scope of the scheme

The assessment under the scheme shall be in respect of territorial areas, persons, income or cases as specified by the Central Board of Direct Taxes (CBDT). The scheme is applicable on all assessments under the Act, except search cases and income escaping assessment.

> E-assessment centres

A National E-assessment Centre (NEC) shall be setup at Delhi to carry out the assessments in a centralised manner. The NEC shall have the jurisdiction to make assessments in accordance with the provisions of the scheme. Regional e-assessment Centres (REC) would be setup, as and when considered necessary by the CBDT, to facilitate the conduct of e-assessments in the region controlled by the Principal Chief Commissioner of Income-tax.

> Setting up of different units

The scheme discusses the setting up of the following units to facilitate the conduct of e-assessments:

- Assessment units: Its functions include identification of points or issues to determine liability (including refund) under the Act, seeking information/ clarification and analysing the material furnished by the taxpayer.

- Verification units: To perform functions of verification, which include enquiry, cross verification, examination of books of accounts, witnesses, recording of statements and other functions that may be required for verification purposes.

- Technical units: To perform functions of technical assistance or advice on legal, accounting, forensic, information technology, valuation, transfer pricing, data analytics, management or any other technical matter, which may be required in a particular case.

- Review units: To perform the functions of review of draft assessment order, which include checking whether the relevant and material evidence is on record, relevant points of facts and law are duly incorporated, issues on which addition or disallowance is made has been discussed, applicable judicial decisions have been considered and other such functions necessary for review purposes.

The scheme further states that all the communications among the above units, or with the taxpayer, or any other person for making assessment, shall be routed through the NEC.

> Procedure for assessment

The procedure for making assessment under the scheme is as follows:

- The NEC shall serve a notice to the taxpayer under section 143(2) of the Act, specifying the issues for selection of the case for assessment;

- The taxpayer may within 15 days, from the date of receipt of notice, submit the response to the NEC;

- The NEC shall assign the case to a specific assessment unit in any one REC through an automated allocation system;

- The assessment unit may request the NEC for:

– Obtaining further information, documents or evidence from the taxpayer;

– Conducting certain enquiry or verification by verification unit; and

– Seeking technical assistance from the technical unit. - Basis the request from the assessment unit, the NEC shall:

– Issue a notice to the taxpayer for obtaining information, documents or evidence; or

– Assign the requisition to verification unit or technical unit (as requested by the assessment unit) through the automated allocation system. - The assessment unit, after taking into account the relevant material, shall make a draft assessment order in writing, either accepting or modifying the returned income of the taxpayer and send a copy of such order to the NEC.

- Penalty proceedings, if any, are required to be initiated by the assessment unit in the draft assessment order.

- The NEC shall examine the draft assessment order in accordance with the risk management strategy specified by the CBDT, including by way of an automated examination tool, and may decide to:

– Finalise the assessment as per draft assessment order and serve the order with a penalty notice (if any) and demand notice to the taxpayer; or

– Provide a show cause notice to the taxpayer, if any modification is proposed; or

– Assign the draft order to a review unit in any one REC through the automated allocation system to review such order. - If concurrence is received from review unit then NEC shall forward order/ show cause notice, as the case may be, to the taxpayer. However, in case of receipt of suggestions (if any) from the review unit, the NEC shall, communicate the same to the assessment unit.

- The assessment unit shall consider the suggestions made by the review unit and send the final draft assessment order to the NEC.

- The NEC shall serve such order with a penalty notice (if any) and demand notice or serve a show cause notice, as the case may be, to the taxpayer.

- The taxpayer may furnish the response to the show cause notice to the NEC within the date and time specified in the notice.

- The NEC shall forward the response of the taxpayer to the assessment unit; however, if no response is received from the taxpayer to the show cause notice, then assessment as draft order shall be finalised and order alongwith penalty/ demand notice shall be sent to the taxpayer.

- Where response is received from the taxpayer, the assessment unit shall consider the response of the taxpayer and send the revised draft assessment order to the NEC.

- Where a modification prejudicial to the taxpayer is proposed, NEC shall, after giving appropriate opportunity, finalise the assessment and serve a copy of the assessment order with a penalty (if any) and demand notice.

- The NEC, after completion of the assessment, shall transfer all electronic records to the jurisdictional TO for imposition of penalty, recovery of demand, rectification of mistake, giving appeal effect orders, submission of remand reports, prosecution proceedings, etc.

- The NEC is empowered to transfer the case, at any stage, to the jurisdictional TO, if it considers this necessary.

- Appeal against the assessment order passed by NEC under this scheme shall lie before the Commissioner (Appeals) having jurisdiction over the jurisdictional TO.

> Penalty proceedings for non-compliance

In case of non-compliance of any notice, direction or order issued under the scheme, a penalty procedure is specified for the same in the scheme.

> No personal appearance

- A taxpayer in not required to appear personally or through an authorised representative in relation to any proceedings under this scheme before any tax authority, NEC, REC or units set up under the scheme.

- If a taxpayer has been given the opportunity of being heard, he or his authorised representative, are entitled to make oral submissions before the tax authority in any unit under the scheme. However, such hearing shall be conducted through video conferencing, including the use of any telecommunication application software that supports video telephony.

- The CBDT shall establish suitable facilities for video conferencing so that a taxpayer is not denied the benefit of this scheme, merely because the taxpayer does not have access to video conferencing.

PwC comments: The scheme focuses on transiting to a faceless, paperless, speedy and fair conduct of assessment. Considering the volume of data and transactions, the implementation of the scheme may be juxtaposed to the technical feasibility of carrying such voluminous data. Accordingly, its effective and seamless implementation is of utmost importance to achieve the desired objectives. Further deliberation on issues such as jurisdiction of NEC vis-à-vis the TO, process of how draft assessment order vis-à-vis Dispute Resolution Panel directions would work, etc. may be required. Opportunity of personal hearing through video conference would need robust submission and strong explanations to justify taxpayer’s standpoint in limited number of opportunities and avoid last minute surprises.

ITAT holds section 50C not applicable where partner contributes land as capital to a partnership firm

Recently, the Chennai bench of the Income-tax Appellate Tribunal (Tribunal) held that section 50C of the Income-tax Act, 1961 (Act), requiring substitution of actual consideration with stamp duty value in certain cases, would not apply in case of transfer of land by a taxpayer-partner as his capital contribution to the partnership firm. The Tribunal held that such contribution is squarely covered under section 45(3) of the Act. Further, the Tribunal ruled that the provision of section 45(3) of the Act was exhaustive and that it did not confer any power on the Tax Officer (TO) to adopt a different consideration from what is recorded in the books of accounts of the partnership firm.

PwC comments: The Tribunal ruling has reiterated the rule of interpretation that special provisions prevail over general provisions. The ruling lays down that a TO cannot compute gains basis the revalued amount applying the provisions of section 50C of the Act when the law very clearly provides that the computation is to be done in a certain manner as per section 45(3) of the Act. Whilst the Tribunal has not discussed this, the said ruling is in line with the Mumbai bench of the Tribunal’s ruling in the case of M/s Amartara Private Limited which laid down that with respect to asset contributed by a partner in a partnership, the value recorded in the books of accounts of the firm would be deemed to be the full value of consideration for computation of capital gains in the hands of the partner.

Bombay High Court directs waiver of section 234C interest payable by the resulting company; observes profit cannot be anticipated till approval of the demerger Scheme

The Bombay High Court in the case of the taxpayer held that the Principal Commissioner of Income-tax (PCIT) committed a serious error in rejecting the application for waiver of interest under section 234C of the Income-tax Act, 1961 (Act). The High Court accepted that the taxpayer was eligible to claim benefit provided in the Central Board of Direct Taxes (CBDT) circular – 2006

PwC comments: This is a welcome decision by the High Court, which allows waiver of interest on the basis of the CBDT circular and impliedly provides precedence, allowing credit of tax paid by the transferor company to the transferee company.

AAR holds shareholders liable to tax on capital gains arising on conversion of company into LLP; rejects ‘no transfer’ argument

Recently, the Authority for Advance Ruling (AAR) while dealing with the taxability in the hands of the shareholders, on conversion of a company into an Limited Liability Partnership (LLP) held that:

- Conversion of equity shares into partnership interest resulted in transfer under the provisions of the Income-tax Act, 1961 (Act);

- Computation provision under section 48 of the Act is capable of working out the capital gains arising in the hands of the shareholders; and

- Even if the value of a partner’s interest in the LLP is equal to the value of a shareholder’s interest in the company, it does give rise to taxable capital gains in the hands of the shareholder

PwC comments: The AAR ruling comments on various litigative areas relating to the taxability of shareholders on conversion of a company into LLP when the conditions prescribed under section 47(xiiib) of the Act are not met. This ruling distinguishes Texspin judgement and other rulings to clarify that those decisions were applicable to conversion of a company into an LLP but not to the shareholders or partners. It is ruled that conversion shareholding into LLP interest constitutes extinguishment of rights in the hands of the shareholders, and hence, would amount to transfer under section 2(47) of the Act.

One needs to carefully understand the findings of the AAR and also consider earlier decisions of other authorities and its impact on the taxability in the hands of shareholders on the conversion of a company into an LLP in future.

Supreme Court holds supporting manufacturer cannot take benefit under section 80HHC on export incentives

In a recent decision, a three-judge Bench of the Supreme Court held that a supporting manufacturer receiving export incentives in the form of duty draw back (DDB), duty entitlement pass book (DEPB), etc., is not entitled to deduction under section 80HHC of the Income-tax Act, 1961 (Act), at par with a direct exporter. Earlier, a division Bench of the Supreme Court had referred the matter to a larger Bench, considering the disagreement with existing judgements on this issue.

PwC comments: This decision clearly states that a direct exporter and a supporting manufacturer cannot be treated at par for the purpose of deduction under section 80HHC of the Act. This Supreme Court decision settles the issue and may be relevant even in the on-going litigation matters before the appellate forums.

International Tax

CBDT raises revenue effect threshold for issue of lower or nil withholding tax certificate in case of non-resident taxpayers

The Central Board of Direct Taxes (CBDT), vide Instruction required administrative approval for issuance of a certificate under section 197 of the Income tax Act, 1961 if the amount of tax foregone exceeded INR 5m in Delhi, Mumbai, Chennai, Kolkata, Bengaluru, Hyderabad, Ahmedabad and Pune stations, and INR 1m for other stations. The above thresholds created various administrative and systemic difficulties under the newly introduced online application process. This led to significant challenges and delays in non-resident taxpayers obtaining withholding orders. The CBDT, vide Office Memorandum, has now increased the threshold of tax foregone that require prior approval of the Commissioner of Income-tax (International Taxation) [CIT-IT] to INR 100m.

Accordingly, the threshold of tax foregone for CIT-IT approval is now raised from the erstwhile INR 5 m/ INR 1m (as the case may be) to INR 100m for all the applications of non-resident taxpayers, across stations, either pending as on date, or filed hereafter.

PwC Comments: The increased thresholds should expedite the issuance of Section 197/ 195 certificates to non-resident applicants.

Tribunal considers factual matrix; holds Cyprus entity beneficial owner of interest for purposes of the tax treaty

Recently, the Mumbai bench of the Income-tax Appellate Tribunal (Tribunal), while dealing with the concept of “beneficial ownership” in the context of interest income earned by the taxpayer from an Indian entity held that:

- The taxpayer has “dominion and control” over the interest income earned from the Indian entity.

- The taxpayer was not constrained by any contractual, legal or economic arrangement with any other third party and was free to utilise the interest income on its sole and absolute discretion.

- The fact that the investment was funded through shareholder loan and capital does not affect the “beneficial ownership/ status” of the taxpayer.

- The taxpayer is the beneficial owner of the interest income and will be taxed as per Article 11 of the Double Taxation Avoidance Agreement (tax treaty) between India and Cyprus at 10%

PwC comments: This ruling provides some clarity on how ‘beneficial ownership’ could be determined in case of investment holding companies. The ruling would also strengthen claims for lower withholding tax certificates for Cyprus companies which were hereto being denied by the tax authorities on the basis that they were not ‘beneficial owners’ of these investments.

Regulatory

Liberalization of foreign investment norms in select sectors

In line with the Cabinet’s announcements on easing foreign direct investment (FDI) norms on 28 August 2019, the Department for Promotion of Industry and Internal Trade (DPIIT) has issued a notification liberalizing foreign investment norms for four sectors (Single Brand Retail Trading (SBRT), contract manufacturing, coal mining and digital media), by issuing Press Note 4 (2019 Series) to amend the FDI Policy, issued vide Consolidated circular 2017 dated 28 August 2017.

The key provisions of Press Note 4 are as listed below.

> Single Brand Retail Trading

- All procurements made from India by the SBRT entity for that single brand will be counted towards local sourcing, irrespective of whether the goods procured are sold in India or exported.

- Sourcing of goods from India for that single brand for global operations can be done directly by the entity undertaking SBRT, its group companies or indirectly through a third party under a legally tenable agreement.

- Removal of year-on-year incremental sourcing requirement.

- The Government has permitted companies to undertake SBRT through online platforms prior to opening brick and mortar stores, subject to the condition that the SBRT company opens brick and mortar stores within two years from the date of start of online retail.

- Computation of five year cumulative period for compliance with the mandatory 30% local sourcing norms will be applicable from commencement of SBRT business, i.e., opening of first store or start of online retail, whichever is earlier.

> Contract manufacturing

- The Government has permitted 100% FDI under automatic route in contract manufacturing through a legally tenable agreement, irrespective of the arrangement whether on Principal-to-Principal or Principal-to-Agent basis.

- Therefore, such entity is now freely permitted to sell to all customers, whether on Business-to-Consumer (B2C) or Business-to-Business (B2B) basis, under automatic route. Also, the sale can be through any format i.e. online as well as offline.

> Digital media

- The Government has allowed 26% FDI under the government route for uploading/ streaming of news and current affairs through digital media.

> Coal mining

- The Government has permitted 100% FDI under the automatic route for sale of coal, coal mining activities, including associated processing infrastructure, which would include coal washery, crushing, coal handling and separation.

- The aforesaid changes will take effect from the date of notification under the Foreign Exchange Management Act, 1999 (FEMA).

PwC Comments: By issuing this Press Note, the Government has liberalised and rationalised foreign investment norms for SBRT, contract manufacturing, coal mining, and digital media sectors, by easing out the policy conditions and increasing the foreign investment limit. The changes will come into effect from the date of notification under FEMA.

High Court holds that wage ceiling applicable only for Indian employees for PF contribution is not discriminatory

In a recent communication, the Employees Provident Fund Organisation (EPFO) circulated a copy of a Bombay High Court decision to its zonal, regional, and district offices for their information.

In this decision, the Bombay High Court has dismissed the petition filed by the individual. The petition challenged the ceiling of the Provident Fund (PF) contributions being applicable only to Indian employees and not to “international workers” under the Employees’ Provident Funds Scheme, 1952 (the PF Scheme), thus making it discriminatory in nature.

PwC Comments: This decision establishes that “international workers” is a special category of employees, separate from Indian employees, and hence, governed by special provisions, different from Indian employees. Therefore, there is no discrimination on the applicability of special provisions as against Indian employees. The EPFO shared the above Bombay High Court decision with its field officers and asked them to refer this judgement. This may apply to cases where the employer argues why “international workers” should contribute on a wage ceiling higher than INR 15,000 per month while Indian employees are entitled to contribute on a wage ceiling of INR 15,000 per month. This is particularly relevant for expatriate employees who are generally equalised with regard to their social security arrangements, and a higher contribution in India increases the cost of the arrangement. However, the PF authorities may counter this argument by applying this judgement.

Indirect Tax

GST Council reduces tax rates, relaxes filing of annual returns for small taxpayers and defers new return system

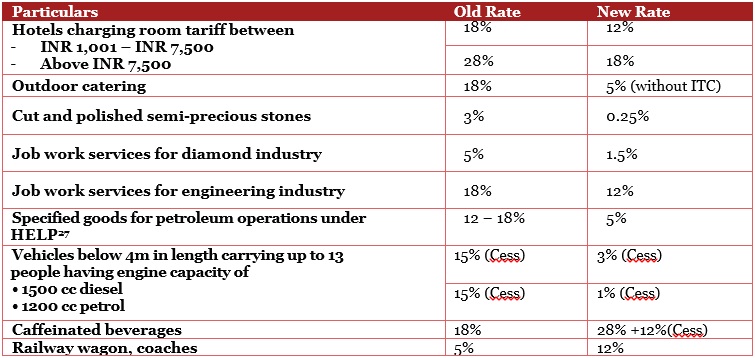

The GST Council, in its thirty seventh meeting, approved various proposals which includes relaxing of the filing of annual returns for MSMEs, deferment of the new return systems and withdrawal of a recently issued circular on post-sales discount on an ab initio basis. Further, the GST Council reduced rates on various goods and services, which will be effective from 1 October 2019, while also increasing rates on certain items on an exceptional basis, in addition to introducing various procedural improvements. The major decisions by the GST Council are summarised as follows:

> Change in rates

> Exemptions

The following goods and services are proposed to be exempted:

- Storage and warehousing of food items.

- The current conditional exemption of export freight charges by air or sea has been extended until 30 September2020.

- Intermediary services provided to supplier of goods, when both the supplier and recipient are outside taxable territory.

- Supply to specified persons organising FIFA Women’s World Cup 2020 in India.

- Imports of silver/ platinum by specified nominated agencies, and its onward supply by such agencies to exporters of jewellery.

> Annual return

The Government has introduced relaxation in filing of annual returns for small taxpayers for financial years 2017-18 and 2018-19:

> Availment of input tax credit and new monthly return

- Statement of intent to impose restrictions on availing input tax credit in cases where the supplier has not furnished the details of outward supplies in time in Form GSTR 1.

- Implementation of new return formats has been postponed from October 2019 to April 2020. The due dates for furnishing Form GSTR 3B and Form GSTR 1 for the period October 2019 to March 2020 to be specified.

> Refund

- Circulars would be issued shortly introduced for uniformity in the application of law across all jurisdictions for the following processes:

- Procedure to claim refund in Form GST RFD-01A, subsequent to favourable order in appeal or any other forum.

- Eligibility to file a refund application in Form GST RFD-01A for a period and category under which a nil refund application has already been filed.

- Integrated refund system, with disbursal by single authority to be introduced from 24 September 2019.

> Post sale discount

Circular no. 105/ 24/ 2019-GST dated 28 June 2019, which provided an analysis of the tax treatment of various post sale discounts prevalent in the industry will be withdrawn on an ab initio basis. A revised circular is expected to be issued in the near future.

> Information Technology Enabled Services (ITES)

A clarification will be issued on when the supply of ITES may qualify as an intermediary, in supersession of circular no. 107/ 26/ 2019-GST dated 18 July 2019, to bring uniformity in the application of positions across all jurisdiction

> Miscellaneous changes

- Place of supply for R&D services provided by Indian pharma companies to foreign companies would be based on place of use and enjoyment of the service, i.e. location of service recipient.

- Registered authors will now have the option to pay GST on royalty received from publishers under forward charge.

- GST on securities lending services brought under the reverse charge mechanism at 18%; GST on such services prior to this change would be payable on a forward charge basis.

- Aerated drink manufacturers will not be eligible to avail the composition scheme.

- Last date for filing of appeals before the GST Appellate Tribunal to be extended, as the appellate bodies are yet to be made functional.

- Amendments to be made in the Central GST Act, Union Territory GST Act, and the corresponding State GST Acts in view of creation of Union Territories of Jammu & Kashmir and Ladakh.

- Committee of Officers to be constituted to examine the simplification of Forms for Annual Return and Reconciliation Statement.

- Aadhar to be linked with registration of taxpayers under GST and the possibility of making Aadhar mandatory for claiming refunds to be examined.

- To tackle the menace of fake invoices and fraudulent refunds, reasonable restrictions to be prescribed on passing of credit by risky taxpayers, including risky new taxpayers.

PwC Comments: The key decisions adopted by the GST Council have three key characteristics

* Firstly, they seek to ease the tax burden to bolster certain sectors in the economy, such as tourism, gems and jewellery and passenger transportation.

* Secondly, they are aimed at easing the burden of complex compliances on small taxpayers, allowing large taxpayers more time to prepare for new compliance formats and examine ways to further simplify annual compliances.

* Thirdly, tax woes faced by specific categories of exporters, such as ITES, R&D units (largely concerning the entitlement to refunds) have been sought to be addressed, which should improve the current experience.

From a systemic perspective, the withdrawal of certain clarifications (though welcome) may result in a degree of scepticism in the minds of the industry on future clarifications that are issued. The proposals to restrict input credits where vendors have not reported transactions in the GSTR1 and introduction of a system to flag “risky” taxpayers may cause concern in the industry. However, the displayed intent of the Government to ensure the adoption of common practices across the country by issuing administrative circulars on various issues needs recognition

Please note that the above analysis is based on press releases by the GST Council, which is a statement of intent. It will be necessary to analyse specific implications based on the actual notifications/ circulars issued in this regard.

Trivia

Advertise here!!

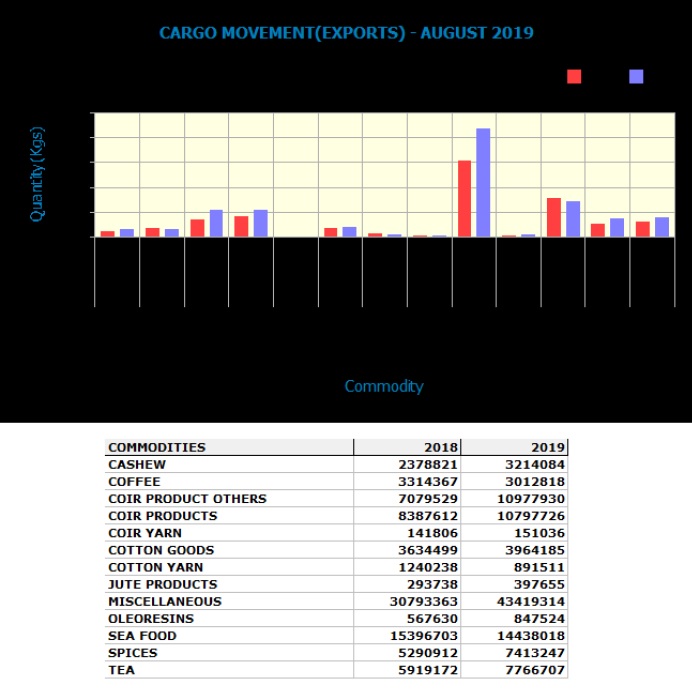

EXIM Statistics

From the Research Wing....

- The Chamber’s Research Report “Rebuild Kerala – Seeking Solutions – People, Policy and Progress, Chamber Perspective” which advocates sectoral reforms in different fields to strengthen the foundations of the ‘Nava Kerala’ establishment process, was released on the 4th October 2019.

- The Chamber’s Research Team is preparing a submission on the Draft Social Security Code 2019 circulated by the Ministry of Labour (Government of India).

Policy Developments Corner

1) The GST Council approved the standard of e-invoice at its 37th meeting held on 20th Sept 2019 and the same along with the scheme has been published on the GST portal. The GST Council has approved the introduction of ‘E-invoicing’ or ‘electronic invoicing’ in a phased manner for reporting of business to business (B2B) invoices to the GST System, starting from 1st January 2020 on voluntary basis. Click here for more details.

2) The Government vide GSR 776(E) dated 11th October 2019 amended the Schedule VII of the Companies Act. Companies can now fund Government sponsored incubators through the CSR mechanism. Click here to read the notification .

3) The Ministry of Health & Family Welfare has circulated the Prohibition on Electronic Cigarettes (Production, Manufacture, Import, Export, Transport, Sale, Distribution, Storage and Advertisement) Bill, 2019 for comments. Stakeholders can submit their comments to [email protected] latest by 8th November 2019.

Article

Amendment to Corporate Social Responsibility: Boon or Bane?

SHRADHA RAJGIRI - Advocate - Shivadass and Shivadass Law Chambers, Bengaluru

The Companies (Amendment) Act, 2019 was implemented on July 31, 2019 which replaced the Companies (Amendment) Second Ordinance Act, 2019 and brought along with it few essential changes.

A major change was made with regards to the framework of Corporate Social Responsibility (‘CSR’). Compliance to the said provisions have also been made mandatory. A default under the said provisions, amounts to imprisonment.

This article will explain the amendments made to the CSR provisions under Companies Act, 2013, and its ramifications.

Basics of CSR

CSR in India has always been viewed as a humanitarian activity. India is the first country to have enshrined the concept of corporate social responsibility into a law. In its core, as per the United Nations Industrial Development Organization, it is meant to be a ‘management concept whereby Companies integrate social and environmental concerns in their business operations and their interaction with the stakeholders’. It uses a unique “Triple – Bottom – Line Approach”[2] that aims to report the business’ impact on the environment and the people, and further helping in using the entity as a vehicle to balance the stakeholders’ interests.[3]

CSR was introduced under Section 135 of the Companies Act, 2013. Among various other provisions, the Government of India made it mandatory for a particular class of companies as per sub-section (1) of Section 135 of the Companies Act, to contribute a portion of their share of profits, for social activities through a dedicated procedure highlighted under Schedule VII of the Companies Act, 2013.[4]

Brief Explanation of the Amendments

The Amendments made with relation to CSR in the Companies (Amendment) Act, 2019 have been briefly been explained as under:[5]

1. Companies under the ambit of the amendment

All companies that have not completed three (3) after inception, but fall under any of the categories below, must contribute ‘2% of their average net benefit of the past three (3) years towards CSR:

- Companies that have a net worth of INR 500 Crores or more

- Companies having an annual turnover of INR 1,000 Crores or more

- Companies having a net-profit of INR 5 Crores or more

2. Transfer to unspent CSR Account

Companies must ensure that they retain amounts dedicated to on-going CSR projects only. Each CSR project must be chosen with due care, precaution and with adequate documentation and reasoning. When a Company decides to opt for a certain project, the funds that are required for such a project, must be utilized within that financial year. Within 30 days from the date of expiry of the said financial year, any remaining funds must be kept in a separate bank account, meant only for the purposes of expenditure for this project. It is from this particular account that the outflow for the ongoing project must be used in the following 3 years. If the amount in the CSR account isn’t used for any CSR activities within the following 3 years, at that point the amount will be transferable to the Funds referenced in Schedule VII.

3. Transfer to various Funds

Companies who fail to utilize the funds that were allocated towards CSR, must move such remaining funds to a fund, indicated under Schedule VII of the Act. Such remaining sum (or sum unspent), must be moved to an indicated fund above, within 30 days from the date of conclusion of the third (3rd) financial year.

4. Penalty for non-compliance

If Companies fail to conform with the provisions above and the amendment thereto, Companies will be liable to a penalty of a sum that will be more than INR 50,000 but less than INR 25 Lakhs. In addition, it recommends that each official of such non-compliant companies will be levied with a fine that is more than INR 50,000 but less than INR 5 Lakhs, or up to 3 years of imprisonment as punishment, or even both.

Industry in Distress

Prior to this amendment, the law simply required companies to highlight reasons for not spending the amounts set aside for CSR in their annual report at the end of the year. With the amendment however, a criminal penalty of three-year imprisonment for executives of Companies have been added for default of CSR obligations.[6]

Many corporate entities are in distress after the enactment of the Companies (Amendment) Act, 2019. Entities are of the opinion that such a penal imposition might be harsh on MSMEs, who lack an organized CSR department. They are also of the opinion that such a draconian provision of law might even be misused.

According to Finance minister Nirmala Sitharaman, the reason behind this amendment is to keep a check on Companies that try to get away from performing their responsibility. [7]

On the other hand, few Companies have come out in support of the amendment stating that such a judicial approach might unify CSR for the better.

Implementation put on hold

On August 23, 2019, the Finance Minister spoke with certainty and stated that the government would review the criminal provisions enacted through the amendment. The implementation of Section 21 of the Companies (Amendment) Act, 2019, therefore, dealing with the amendments to CSR have been put on hold. A Panel headed by Corporate Affairs Secretary, Injeti Srinivas, had made recommendations seeking to remove the provision relating to imprisonment while seeking to allow tax deduction on such expenditure. [8]

Some Companies, under the current regime, have received notices from the Ministry of Corporate Affairs, to show cause as to why action should not be taken against them for not utilizing the funds set aside for CSR. In this regard, the Finance Minister claimed that issuance of such notices would-be put-on hold for a certain duration.

On August 23, 2019, the Finance Minister reaffirmed that all CSR violations made, shall be treated only as a civil offence and not a criminal offence.[9]

Conclusion

Upon perusal of the amendment, it is too soon to decide the impact of this amendment. Though discussions regarding removal of penal provisions have spiraled to the Finance Ministry and the Minister herself has stated that there will be no criminal sanctions, Companies must aim to adhere to the CSR requirements.

Recommendations have been made through a Panel report[10] with alternatives to the criminal provisions by enhancing the penal amount by two to three times the default amount, with a cap of INR 1 Crore. The approach sought for is certainly lenient in comparison to the imprisonment provision.

It should be realised that CSR is not the main business of a company and imposing a criminal penalty on individuals of these Companies might result in tarnishing the image and reputation of such a Company. Instead of reaching for extremes, a middle ground must be sought for, which would balance the opinions of both the government and the industry.

References

[2] A form of accounting framework consisting of three factors: social, environmental and financial.

[3] Triple Bottom Line- Wikipedia, https://en.wikipedia.org/wiki/Triple_bottom_line

[4] India: Corporate Social Responsibility: Mandating Companies To Contribute Towards Society – http://www.mondaq.com/article.asp?article_id=305620&type=mondaqai&r=2&t=3

[5] CSR Amendments, 2019 – https://www.indiafilings.com/learn/csr-amendments-2019/

[6] CSR: Why make Charity Criminal? – http://www.indialegallive.com/viewpoint/corporate-social-responsibility-why-make-charity-criminal-70514

[7]Jail term for CSR violation makes firms anxious –

[8]Drop prison clause, give tax credit for CSR – https://timesofindia.indiatimes.com/business/india-business/drop-prison-clause-give-tax-credit-for-csr-panel/articleshow/70667503.cms

[9] CSR violations not to be treated as criminal offence, says Nirmala Sitharaman – https://www.indiatoday.in/business/story/csr-violations-not-to-be-treated-as-criminal-offence-says-nirmala-sitharaman-1590896-2019-08-23

[10] A report of the High Level Committee on the Corporate Social Responsibility 2018 dated August 7, 2019- http://www.mca.gov.in/Ministry/pdf/CSRHLC_13092019.pdf

Letter to the Cochin Port Trust

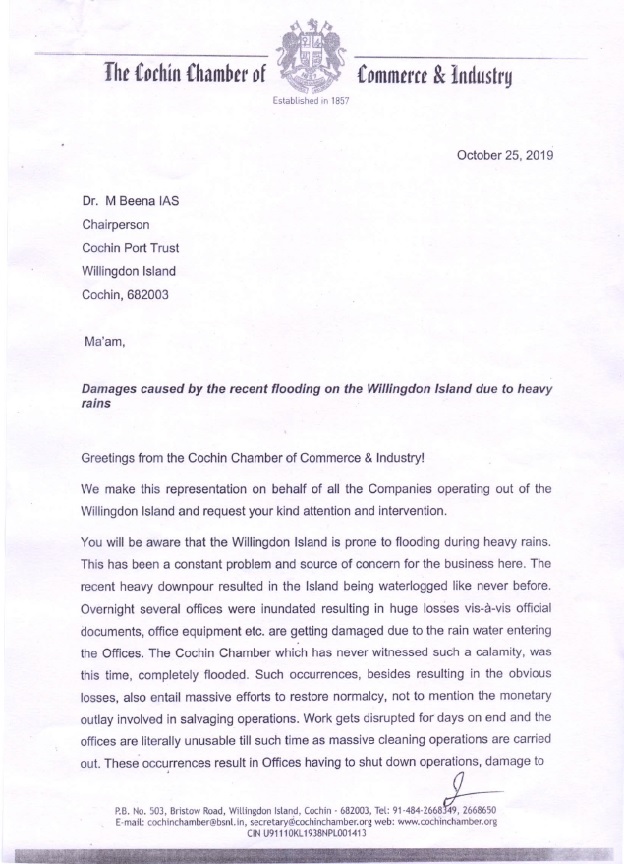

The Chamber has written to the Chairperson of the Cochin Port Trust requesting the Port to initiate measures to avoid the frequent flooding that occurs on the Island due to heavy rains. The President Mr. Venugopal also called on Dr. Beena IAS to impress upon her the need for an effective solution to this problem. The letter sent to the Port is reproduced below for information.

Upcoming Events

11th CEO FORUM Breakfast Meeting

Skilling - The Engine of the Economy | 01.11.2019

The 11th Breakfast Meeting under the aegis of the Chamber’s CEO FORUM 2019 will be held on Friday, the 1st of November 2019 between 8.00 am and 10.00 am at the Taj Gateway Hotel, Marine Drive, Ernakulam.

The Speaker at this Session will be Mr. Ravi Tennety, Chief Executive Officer – Training and Skilling Division, Quess Corp Limited, Bangalore who will speak on “Skilling – The Engine of the Economy.”

Click Here to reigster

Goods and Services Tax

Upcoming Changes, Legislative, Legal and other Updates | 08.11.2019

The Cochin Chamber of Commerce & Industry is organising a Half-Day Session on GST – Upcoming Changes, Legislative, Legal and other updates. The programme is scheduled for the 8th of November from 02.00 p.m. to 05.00 p.m. at Hotel Park Central, Ernakulam. Registrations open from 01.30 p.m.

The Speakers for this session will be Mr. Kunal Wadhwa, Partner, Indirect Tax, PwC India, Bangalore and Ms. Nisha Menon, Director, Indirect Tax, PwC India, Cochin.

About the Session

There is increased focus from the Government’s side on curbing tax evasion and bringing in more transparency to the entire GST system. With this objective in the backdrop, two major changes are on the anvil: The new return formats (where the primary thrust is on real time reporting of transactions and availment of credits to the extent the taxes have been paid by vendors) and e-invoicing. While the GST Council has approved the phase-wise implementation of e-invoicing for B2B transactions from 1 January 2020 onwards on a voluntary basis, the new GST returns are proposed to be introduced from April, 2020.

As a precursor to the above changes, the Government has already imposed restrictions on availment of input tax credit by recipients in cases credit details are not reflected in GSTR 2A of businesses

While the objective behind such changes seem reasonable, its implementation could be quite challenging for businesses. These changes are expected to trigger a huge shift in the way GST compliances are carried out and would also have a great impact on the IT systems. This session is aimed at providing a brief update on the above proposed changes and also shed some light on other key amendments and practical challenges that the companies might face in complying with the same.

List of topics that will be covered

A – Upcoming Changes in GST

– E-invoicing

– New Return Format.

B – Legislative Updates

– 20% ITC Restriction

– Retrospective amendment to CGST Rules on impacting last date to avail ITC;

– Recent Circulars

C – Legal updates

– Latest Case laws, AARs etc mainly focusing on ruling around services qualifying as ‘intermediary’ under GST

D – Other Updates

– Deemed supply provided by overseas entities with respect to brand, licenses, shared services, etc

– Key points under GST Audit

– LDRS.

Click Here to register

One-Day Session on Artificial Intelligence & Machine Learning

How to stay head in Business with the latest Tech and Tools | 29.11.2019

Registerations will open shortly…..