President's Note

Dear Friends,

The Corona Pandemic has affected economies and stock markets across the globe adversely. However, the Indian Stock Markets have started growing and is currently the 2nd highest in the world at 76% growth from its lowest low in March. Favourable monetary policies, strong foreign capital inflows, and the certainty of the US elections are said to be some of the reasons behind the growth.

2021 also looks strong for the IPO Market. The data available shows that with only just 12 IPOs, we have managed to raise a whopping 25000 crores this year through initial share sale. Companies from a variety of sectors like, IT, Pharma, Telecom, international restaurant chains etc. have also joined the IPO market, which will hopefully ensure that this market will stay strong through the next year as well. This figure could increase as many other multinational companies are expected to enter our markets soon.

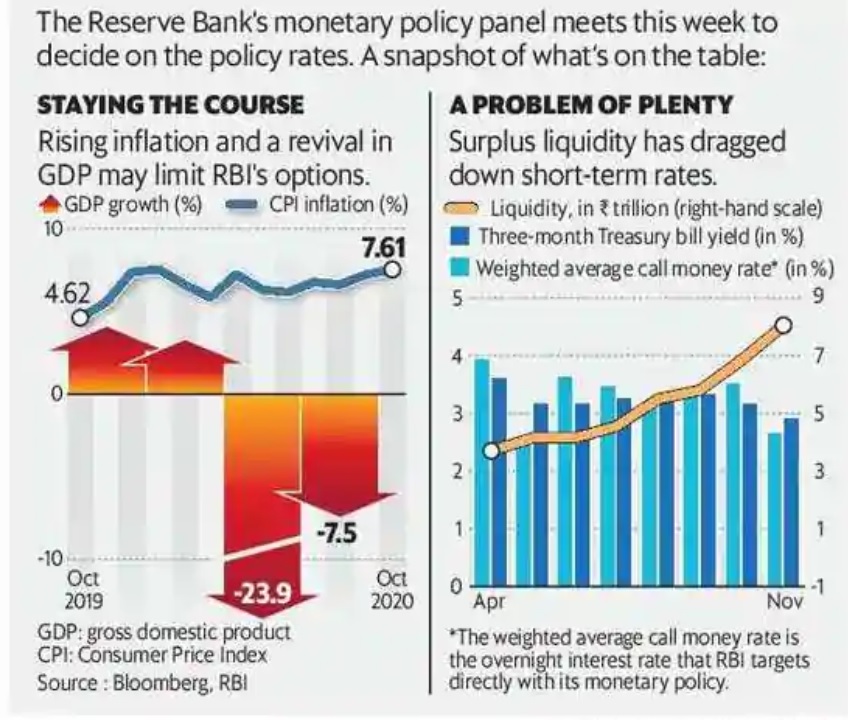

Given the circumstances, the Reserve Bank of India has decided to keep its policy rates unchanged. The RBI has been trying to ease the high inflation, which has been in the red for the last seven months and also to regulate economic growth. Retail inflation hit its highest in six and a half years at 7.6% last October due to the uncontrolled surge in food prices. We think we can now expect the RBI to put a hold on the rate cuts for the rest of the fiscal year as against what was expected earlier.

The Cochin Chamber has always been an advocate for the industry raising its concerns to the authorities. Off late we have submitted 3 representations raising different issues the details of which can be accessed elsewhere in this edition of the Chamber Voice.

As is customary we conducted our monthly CEO FORUM Virtual Meeting earlier this month. Mr. G. Vijayaraghavan, Founder CEO of Technopark and Former Member, Kerala State Planning Board was the Guest Speaker. He spoke on “Government & Business?” The session was a very interesting and thought-provoking one. A detailed report of this Session is carried in this Newsletter.

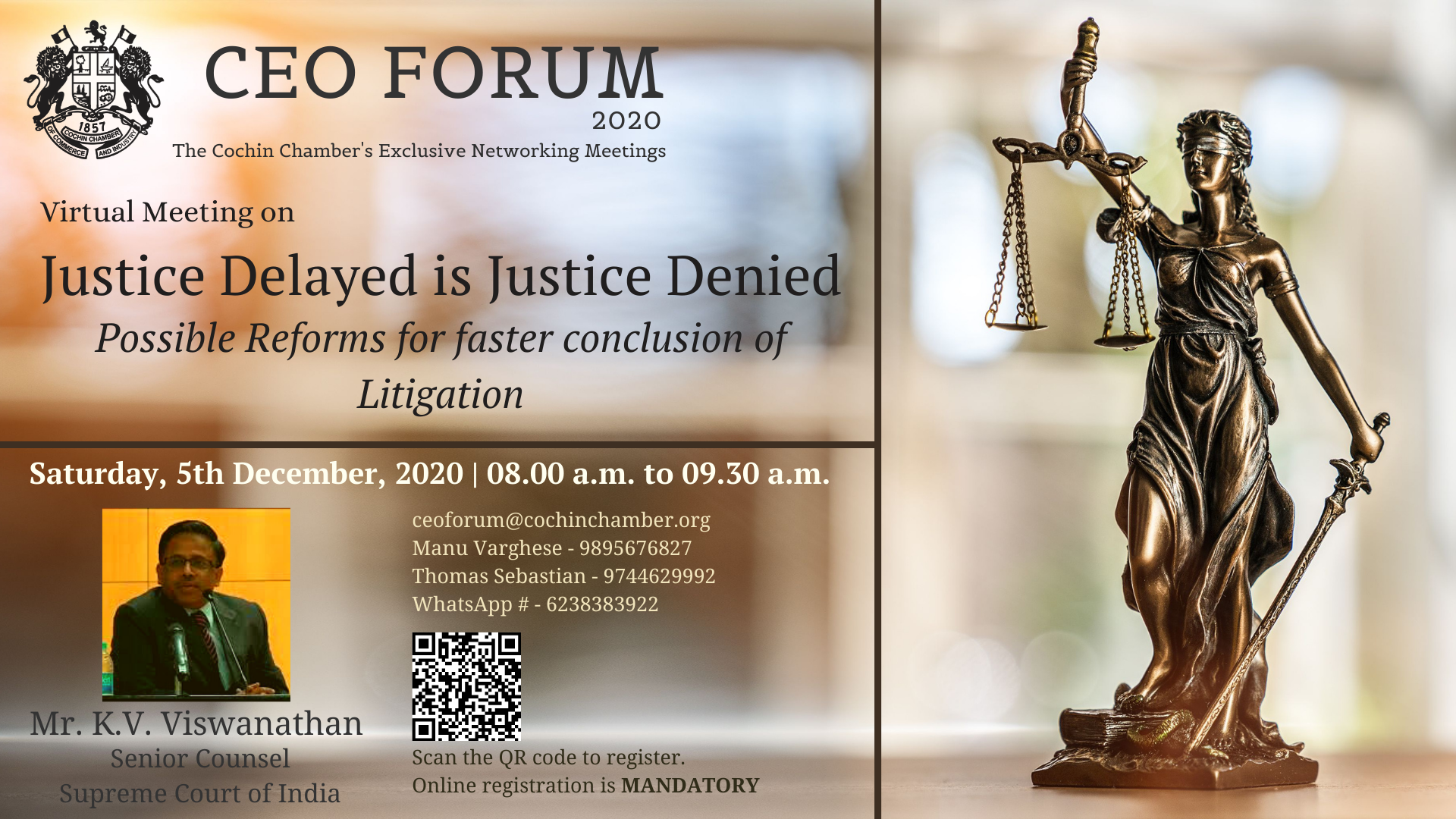

The next CEO FORUM meeting will be held on Saturday the 5th of December between 08.00 a.m and 09.30 a.m. Advocate. K. V. Viswanathan, Senior Counsel, Supreme Court of India is the Guest Speaker and will talk on “Justice Delayed is Justice Denied. ” This session too will be held online. I hope all of you will register to attend this session.

This will be my last letter to you as the President of the Chamber. On the 18th of December at the 163rd Annual General Meeting of the Chamber I will be demitting office after an eventful two years as President of one of the prestigious Chambers of Commerce in the country. It has been an honour serving this Chamber and I carry with me fond memories of my term as President. I take this opportunity to thank you all, the Members of the Chamber, the members of the Executive Committee and the Secretariat of the Chamber for the gracious and unstinting support and cooperation that I have received during my tenure as President.

Thank you and wishing you all the very best.

Venugopal

President

Quote

Trivia

Forthcoming Event

CEO FORUM 2020

Justice Delayed is Justice Denied - Possible Reforms for faster conclusion of Litigation

05.12.2020

The next CEO FORUM Virtual Meeting is scheduled for Saturday, 5th December 2020 from 8.00 a.m. to 9.30 a.m. on the Zoom platform.

Shri K.V. Viswanathan, Senior Counsel, Supreme Court of India has agreed to be the Guest Speaker and to speak on *“Justice Delayed is Justice Denied – Possible Reforms for faster conclusion of Litigation”. *

There is No Registration Fee for the members of the Cochin Chamber.

Others may register for the programme by clicking here.

CCCI - Ease of Doing Business Information Survey

The Kerala Government has constituted a Committee of Secretaries vide Order dated 7th October 2020 as Phase 1 of exercising minimum regulatory compliance on businesses. The Cochin Chamber of Commerce & Industry wishes to contribute quality policy inputs to the Government to improve Ease of Doing Business in the State.

Questionnaire on Business Information Survey (click on the link given to view the same)

We request you to send your valuable inputs by filling the above Questionnaire and kindly co-operate with us.

Recent Event

CEO FORUM 2020

Government & Business?

06.11.2020

The President of the Chamber, Mr. V. Venugopal commenced the meeting by welcoming the Speaker for the day Mr. G. Vijayaraghavan and the participants to the 11th CEO FORUM Meeting.

In his welcome address, Mr. Venugopal pointed out some concerns pertaining to the Government doing business, the continuity of CEOs in Public Sector Companies etc. He also introduced the Speaker Mr. Vijayaraghavan to the participants as Founder CEO of Technopark and Former Member, Kerala State Planning Board.

Mr. Vijayaraghavan, in his address, thanked the Chamber and the President for inviting him to be the Speaker at the Session and for allowing him to express his views on the topic – Government and Business. He then briefly introduced the topic of the session and main aspects that he will cover.

In his introductory remarks, Mr. Vijayaraghavan emphasised that the purpose of a Government is Governance including Social Welfare activities, upliftment of people who need support in the Society etc. A Government’s mandate does not include doing business. He touched upon the differences between a Bureaucrat and a Politician, corruption in Kerala, and the expectations from the Society at large. Mr. Vijayaraghavan explained why the Central Government is now backing out of businesses which they were earlier a part of. He said that there is no need for a Government to be involved in any sort of Business undertaking which is not profitable. He cited the example of KTDC holding a lot of properties across the State which isn’t making money and is actually a burden on the Government. “Such properties could have been done up much better if someone actually owned them other than the Government,” he said.

Mr. Vijayaraghavan said that the main problem with the Government running a business or a particular property is that no one really owns it. He said that everyone who works in the Government-owned business thinks that the money they spend belongs to the Government and fails to realise that it actually is the people’s money which is spent. Mr. Vijayaraghavan painted a vivid picture of how Governments run businesses and how the real state of affairs of these businesses is revealed at the time of the audit.

Corruption in these Government undertakings runs deep he said even though claim are laid to say that it is all for the benefit of the general public and the State.

Mr. Vijayaraghavan added that it now appears that the whole idea of a Government is to cater to specific groups of people, their accomplices and the powers that be.

Towards the end of his session, Mr. Vijayaraghavan highlighted the importance, role and responsibility of the Media in our society. The problem with Media these days is that, they are all behind their ratings and viewership, and for this every news channel’s priority is sensationalizing even the smallest of matters, he said. Mr. Vijayaraghavan suggested that the Chamber conduct yearly sessions with the Media, bringing them together to discuss matters of concern, eradicating corruption in the Media, and to explain to them what is expected of them by a society that is literate and discerning as is the case in Kerala.

Concluding his session, Mr. Vijayaraghavan said that the right thing to do is to achieve a balance whereby the Government sector and the Private Sector work together in such a manner as to leverage the best of both sides. This approach will focus more on the development of the society and the State, he said.

Following Mr. Vijayaraghavan’s address Member CEOs of the Chamber raised several questions, expressed views and discussed the current state of affairs in Kerala and how we can jointly work to remedy the situation.

Mr. K. Harikumar, Vice-President of the Chamber delivered the Vote of Thanks.

The session was attended by 30 people.

Articles

“Chronic diseases create large adverse – and underappreciated – economic effects on families, communities and countries. In 2005 alone, it is estimated that India will lose 9 billion dollars in national income from premature deaths due to heart disease, stroke and diabetes (reported in international dollars to account for differences in purchasing power between countries). These losses are projected to continue to increase: cumulatively, India stands to lose 237 billion dollars over the next 10 years from premature deaths due to heart disease, stroke and diabetes.”

Chronic diseases in many instances do not occur alone e.g. diabetes occurs as the only condition in 48% of cases, with one other condition in 30% of cases and with two or more conditions in 24% of cases. This adds to the complexity of management as well as to the costs of providing care. The prevalence of chronic diseases increases with increasing age as seen with ischaemic heart disease, stroke, diabetes, cancer, osteoarthritis, Alzheimer’s disease, etc. The increasing burden of chronic diseases reflects to some extent the failure of public health measures to prevent their development as well as the lack of medical treatments to cure these diseases. As a result, there has been a move to explore alternate therapies including stem cell therapy. While there is increasing evidence for benefit, there remains the need for large scale controlled studies to validate their effects on health outcomes. There also exists the need to ensure such therapies are administered in proper clinical settings by ethical and trained practitioners.

Stem cells are undifferentiated biological cells that can differentiate into other types of cells and can also divide in self-renewal to produce more of the same types of stem cells to maintain their population. They therefore act as a repair or renewal system. Stem cells persist through life in our human tissues, replacing cells lost to homeostatic turnover, injury and disease. Stem cell number and function decline with age. Such age-related changes in the population of stem cells may contribute to some of the diseases of aging. Human cells replicate a limited number of times before entering a senescence phase with arrest of the cell cycle. The accumulation of aged or damaged cells negatively impact the stem cell function of our organs causing organ dysfunction and degeneration resulting in the features of aging and aging-related diseases.

Dato Dr. Jai Mohan

While there are different types of stem cells, it is mesenchymal stem cells that are mainly used in therapy. Sources of mesenchymal stem cells include bone marrow, dental pulp, adipose (fat) tissue, umbilical cord blood and umbilical cord tissue, amniotic fluid and menstrual blood. When the source of stem cells is the individual being treated, treatment is called autologous. When the source is another individual, the treatment is allogeneic. Rejection is not a problem with mesenchymal stem cells. Stem cell therapy can be used in regenerative medicine (promote the reparative response of diseases, dysfunctional or injured tissues) or as an alternative to organ transplant (to address organ shortage or long waiting lists).

The list of conditions for which stem cells have been administered are numerous. It has been especially popular in the treatment of osteoarthritis, spinal injury, myocardial infarction, heart failure, diabetes mellitus, critical limb ischaemia, autism, alopecia, liver disease, renal failure, autoimmune diseases, etc. A full list can be obtained from www.clinicaltrials.gov which lists the clinical trials that are being or have been conducted world-wide and the results where available. There are many medical journals which publish the results of stem cell clinical trials as well as good reviews of outcomes.

There is evidence that the benefits may not be due to stem cells replacing damaged or aged cells but due to the cytokines, growth factors, angiogenic factors and extracellular vesicles that are secreted by stem cells (“the paracrine effect”). These raises the possibility of using these factors without using stem cells. Such conditioned media are already being used in aesthetic practice.

A newer development has been the discovery of exosomes which play a role in cell-to-cell communication. These exosomes are membrane-bound packets produced by cells. They are about the size of a virus each and contain proteins, lipids, DNA, RNA, miRNA and a host of other substances. Exosomes have been shown to contain numerous disease-associated cargos such as those associated with Alzheimer’s disease, Parkinson’s disease and amyotrophic lateral sclerosis. Exosomes have been suggested to be propagators of neurodegenerative protein spread and may be a key to management of these neurodegenerative conditions. In addition, there is evidence to suggest that tumour-derived exosomes play critical roles in cancer. Exosomes and their cargos may serve as cancer prognostic markers, therapeutic targets or even as anticancer drug‐carriers.

It must be emphasized that the use of stem cells, conditioned media and exosomes still require much more research and should be cautiously in proper clinical settings.

India is on the verge of enacting its all-important Personal Data Protection Bill, 2019 (‘PDP Bill’), currently pending before the Parliamentary Standing Committee. Apart from this, the Government has also floated two other possible reforms that stem from the PDP Bill i.e., Non – Personal Data Governance Report, 2020 (‘Report’ / ‘NPD Governance Report, 2020’) and the Health Data Management Policy (‘Health Policy’). All of the above however, have a common and central theme that keeps the citizen at the hilt – Consent.

Given the effects and after effects of the pandemic, it has become increasingly important for organizations and entities to ensure that data is protected and preserved. The role and obligation of a Data Fiduciary has only been on the rise and will continue to rise for a foreseeable period. But why does this create issues? Consent, as some might say, is the mole in this entire drama that may unfold once the law is enforced. What is it about consent that makes this legislation tricky?

Consent is the baseline for data protection. The law provides for consent to be taken, preferably at every stage i.e., collection, storage, processing etc. It is left to one’s interpretation if consent needs to be taken at every stage or whether just one consent will suffice. The Data Principal (citizen) has complete power and right of data and can, at any point, refuse / withdraw consent.

In this article, we have tried to analyse the various consent requirements across different legislations i.e., General Data Protection Regulations (GDPR) in EU, the Sri Krishna Committee Report, PDP Bill, the Report / NPD Governance Report, 2020 and the Health Policy.

General Data Protection Regulation (GDPR):

Consent is defined under Article 4 (11) of the GDPR which means “any freely given, specific, informed and unambiguous indication of the data subject’s wishes by which he or she, by a statement or by a clear affirmative action, signifies agreement to the processing of personal data relating to him or her.”

Consent is an essential ground for processing the data and protecting it, though, not the only one. There are several other grounds for processing such data which include: contract, legal obligations, vital interests of the data subjects, public interest and legitimate interest as stated under Article 6(1) GDPR.

Consent to that end poses itself as an onerous obligation on organizations, with Data Fiduciaries really getting written consents from data principals for use, sharing and processing of data. This Consent must be free, specific, informed and unambiguous. Consent cannot be coerced or must not be given under any form of undue influence since such a Consent would be invalid to say the least.

The effect of the above is that the data principal must be fully informed about the identity of the Data Fiduciary (be it controller or processor of data) and the usage of the data i.e., where it is stored, what is capable of happening to his data, where it is used and what are the results of such usage. The Data Principal must also be in a position at any point, to withdraw Consent from storage, usage or controlling of his data. It is also the responsibility of the Data Fiduciary to ensure that this withdrawal is hurdle-free and does not carry additional or carry on obligations. At this juncture, all data that is stored, processed or used by the Data Fiduciary and belongs to the Data Principal, must be returned at once to the Data Principal without any delay. If the Data Principal chooses to inform the Data Fiduciary to delete the data that was with the Data Fiduciary, the Data Fiduciary must be obliged and give a confirmation to the Data Principal immediately after deletion. Article 13(2)(f) of GDPR provides for the responsibility of the Data Fiduciary when automated decision making is involved. The Data Fiduciary must inform the Data Principal about the possible outcomes that could be encountered by them.

It must however be noted that it is not mandatory for the Data Fiduciary to seek Consent in physical form alone – it can also be done electronically. Further, Consent for or on behalf children and adolescents has been listed as a separate category. This places an additional Consent requirement on the Data Fiduciary for any person under the age of 16 years. It is essentially a consent from the parent of such an individual. This is a flexible age limit that can be modified as per law.

Srikrishna Committee Report:

The Srikrishna Committee Report follows suit from the GDPR, in terms of what constitutes Consent and the compliance requirements under the heading ‘Consent’. The Committee Report then highlights that Consent can be both manual and automated. The Committee Report then goes on to explain that Consent is nothing but the person’s expression towards autonomy on the data provided by her / him.

The Committee Report states that there are two (2) advantages of seeking consent i.e., (i) it respects user anonymity and (ii) creates liability on part of the Data Fiduciary. However, Consent alone is not completely sufficient to protect data. Therefore, additionally, the Data Principal must be aware at the time of Consent about the nature of storage, control and use of such data. Two (2) other aspects that that have been covered in the report relate to ‘child’s consent’ and ‘safeguards for processing of sensitive personal data’. Of course, like every rule, there are exceptions like ‘legitimate State interest.’ Under this exception, Consent is not required to be obtained from the Data Principal.

The Data Fiduciary seeks Consent by way of a ‘notice’ which communicates terms and conditions of the Data Fiduciary. The individual has the freedom to provide her / his Consent. The Committee Report suggests tentative contents which must be part of the notice which is given to the Data Principal. The reason being that such a notice must not be onerous on the Data Principal and places an obligation on the Data Fiduciary at all points. The suggestions are as under:

- Collect and display only the reasonable amount of data required, in the terms and conditions;

- A clear notice explaining in detail, all the contents to which Consent is needed;

- Any harmful or erroneous clauses in the contract, that may be overlooked by the Data Principal, must now be specifically highlighted and consented to by the Data Principal;

- Affirmative consent is received;

- Give the Data Principal an option of accepting / denying certain conditions.

The Contract Act, 1872, requires all the conditions for a valid Consent to be fulfilled, which include: free, informed, clear, specific and capable of being withdrawn. These conditions must not be misunderstood to be applicable for all the scenarios and all the types of Consent.

Consent for Sensitive Personal Data: Consent in so far as ‘sensitive personal data’ is concerned needs to be obtained ‘explicitly’. The Consent must be informed i.e., the purpose for which data is being taken and the nature of storage and use. The individual must also be given the opportunity to specify as to what information to use and process and what not to. Hence, merely ticking the ‘I agree’ box will not be considered ‘explicit consent’. The details and affirmations sought for by the Data Fiduciary must clearly be visible on the screen in simple comprehensible language for the Data Principal to give Consent. At the same time, the permission sought must not be so elaborate so as to vex the Data Principal and coerces them to give Consent.

The Committee Report also mentions that a ‘Consent Dashboard’ must be created by Data Fiduciary, to keep an effective track about the number of times an individual gives Consent. The same has not been reflected in the PDP Bill, 2019. This Dashboard can be accessed both by the Data Fiduciary and the Data Principal cutting out on the aspect of ‘consent fatigue’.

Data protection of minors – parental consent for minor’s usage of internet applications of websites: This requirement has been borrowed from the GDPR and emphasises the parent’s consent towards minor’s usage and the terms and conditions. The same is reflected in the PDP Bill, 2019 under Chapter IV, Section 16, which provides for personal data and sensitive personal data regarding minors. The Data Fiduciary must process the personal data of the child in the manner which would protect the rights and the interest of the child. Before processing the data, the age has to be verified and parent or guardian’s consent must be taken.

PDP Bill, 2019:

Consent under Section 3(10) read with Section 11 of the PDP Bill, 2019, must be given by the Data Principal at every stage of the process i.e., collection, storage, use, processing and transfer to any third party. Such a Consent, as stated above in the Committee Report, will not be valid unless it is free, informed, specific, explicit, clear and capable of being withdrawn. The purpose for seeking such information and the use of it must be made clear. No supplementary or add on obligations must be added to the Consent as a condition. The burden of proof falls on the Data Fiduciary to establish that Consent was freely given by the Data Principal for a particular term or condition.

Under Chapter III of the PDP Bill, 2019, data can also be processed without consent under Section 12 which include (i) exercise of any function of the State, (ii) legal proceedings i.e., processing of personal data to comply with any law, order, or judgment of courts or tribunals, (iii) to respond to a threat / emergency.

Further, Section 12(f) provides an exception wherein processing of personal data may be done without any consent of the users, in case of “breakdown of public order”. Section 14 provides for another exception wherein personal data may be processed without consent for “reasonable purposes”. The illustrative list of “reasonable purposes” tentatively includes “prevention and detection of any unlawful activity including fraud”, “whistle blowing”, “mergers and acquisitions”, “network and information security”, “credit scoring”, “recovery of debt”, “processing of publicly available personal data” and “the operation of search engines”.

Lastly, the ‘right to be forgotten’ is an essential feature of the PDP Bill, 2019. At any point, the Data Principal can request any and all information to be wiped out from the Data Fiduciary’s systems and networks. This is not a request – it is a mandatory feature. The Data Fiduciary will not have an option to reject this application – they are under an obligation to follow through with this request.

NPD Governance Report, 2020:

India is the first country to regulate and seek consent for the use and processing of the non-personal data. Non-personal data refers to all data that is not personal data or sensitive personal data. The ambit of non-personal data has further been diluted down to sensitive non-personal data, non-sensitive non-personal data and community non-personal data. Various principals regarding anonymization and de-anonymization, have been quoted to understand the schematics behind governance of the non-personal data.

In so far as Consent for sharing, storing, processing of non-personal data are concerned, there are multiple stages of a cycle where the individual needs to provide Consent which include when the data is collected, stored, processed and shared, including uploading and downloading of data. The Data Principal will also have the liberty to choose what data needs to be anonymized and what data can remain de-anonymised. Appropriate standards of protection are needed for anonymisation of data, in order to protect it from the threat of re-identification.

Health Policy:

As the name suggests, the Health Policy is applicable to all the entities as mentioned under it, which include (i) all entities and individuals who have been issued an ID under this Policy; (ii) health care professional, including but not limited to doctors or health practitioners, nurses, laboratory technicians, and other healthcare workers; (iii) governing bodies of the Ministry of Health and Family Welfare, the National Health Authority, (iv) Health Information Providers, etc. Since the Health Policy deals largely with sensitive personal data of an individual, the Consent framework is intended to be robust and dynamic, keeping in mind the kind of data that will be shared by an individual.

Chapter III of this Policy provides for the Consent Framework. Data Fiduciaries can collect and process personal and sensitive personal data with valid consent. The purpose for collection and processing of such data will be limited. Consent can be obtained via electronic means or physically, either directly from the user or via a consent manager.

The Policy gives full control and decision-making power to the Data Principal with respect to the manner in which the data has to be collected, stored and processed. It further provides for the Data Fiduciaries to incorporate appropriate technological means to prevent security breaches and to guarantee the integrity of access permissions given by Data Principal.

All data that is stored in the database cannot be accessed by all the health service providers. Only the relevant part of the Data Principal’s information will be disclosed to the concerned health care worker. Example: if the pharmacist is accessing to the Data Principal’s data, he can only view that part of the entire database, which consists of the prescription prescribed by the doctor and nothing else.

Conclusion:

Data is increasingly taking centre-stage across almost all economic sectors around the world. Consent has constantly been the fulcrum of any such regime. The responsibility and accountability completely lies of the data fiduciary for protecting the privacy of the individual. The bill, currently pending before Parliament is gaining mainstream momentum in India. Organizations and Individuals are both worried and excited about the new law. It will be important to see the manner in which this law unfolds and the way Courts interpret this law.

The contents and comments of this document do not necessarily reflect the views/position of Shivadass and Shivadass (Law Chambers) but remain solely of the author(s). For any further queries or follow up, please contact [email protected].

Chamber Vlog & Web Series

To view all the videos in the Chamber Vlog series and the Chamber Web Series, please go to the Cochin Chamber’s YouTube Channel.

The most recent ones are added to the video players below. We will keep uploading new and relevant content for our members and the industry in general.

Kindly share these videos with your networks and subscribe to our YouTube Channel for more informative content.

Chamber Vlog - 21

Creating a new Online Market

Chamber Vlog - 20

Role and Persona of a Modern Marketer

Web Series

Consolidation & Codification of Labour Laws

Web Series

3 years of GST

Tax and Regulatory Updates from PricewaterhouseCoopers

Relaxations in visa and travel restrictions for foreign nationals travelling to India

The Ministry of Home Affairs issued revised guidelines on 21 October 2020 providing relaxations in visa and travel restrictions for foreign nationals and Overseas Citizen of India (OCI) card holders.

The key highlights of the relaxations are as follows:

1) The following categories of foreign nationals are permitted to enter India by water routes or by flights, including flights operated under the ‘Vande Bharat Mission’, air bubbles (bilateral air travel arrangements) or by any non-scheduled commercial flights, as allowed by the Ministry of Civil Aviation –

A) All OCI and Person of Indian Origin card holders;

B) All foreign nationals, including their dependents, who hold an appropriate category of dependent visa.

2. All existing visas except electronic visas (being tourist, medical, business visas), which remained suspended, shall stand restored with immediate effect.

3. If the validity of such visas has expired, the foreign national will be required to obtain a fresh visa of an appropriate category to travel to India. The application for obtaining the relevant visa will have to be made electronically on indianvisaonline.gov.in and it will be necessary to adhere to the process along with documentation, as prescribed by the relevant Indian Mission or visa processing agency.

4. Foreign nationals who do not fall under point number 1, above, but are required to visit India for the following purposes will be granted an appropriate category of visa upon making an application with the relevant Indian Mission/ Post for –

A. A family emergency – Single entry ‘X-Misc’ category of visa may be issued for an appropriate period.

B. Medical treatment in emergencies – Medical visa or medical attendant visa for an appropriate period may be issued.

5. Any Indian national holding any type of visa of any country is permitted to travel from India, provided there is no travel restriction for the entry/ transit of Indian nationals to the relevant jurisdiction(s). It will be the responsibility of the relevant airline to undertake necessary checks on the travel restrictions applicable for Indian nationals intending to travel to a particular country, before issuing a ticket/ boarding pass to such travelers.

6. Travelers will have to adhere to quarantine and other health related guidelines, as prescribed by the Ministry of Health and Family Welfare.

PwC comments As commercial international airspace in India remains suspended until 30 November 2020, organisations may want to explore travel options for their mobile population via the ‘Vande Bharat Mission’ or the ‘air bubble’ arrangements that India continues to enter with several countries. Applicants may have to factor any additional lead time (possibly arising due to backlog in the processing of applications) that may be added to the typical visa processing timelines for obtaining relevant Indian visas to travel to India. In addition to the standard documents required to apply for a relevant Indian visa, applicants may be required to furnish additional documentation, specifically required by the Indian Mission/ Posts or the visa processing agencies, if any, considering the pandemic, for obtaining a fresh Indian visa when filing a fresh visa application. While the electronic visa application process has commenced in most jurisdictions, applicants may still face practical challenges in lodging applications, especially in jurisdictions where local authorities are yet to relax restrictions due to lockdowns.

The Patents (Amendment) Rules, 2020

The Government of India published the Patents (Amendment) Rules, 2020 (Rules), in the Gazette of India on 20 October 2020 bringing into effect these Rules from the aforementioned date. The amended Rules aim to simplify the manner of furnishing information pertaining to commercial working of patents in India.

Key changes under the Rules are as follows:

- Form 27, containing details of the commercial working of patents, may now be filed within six months after the end of the financial year, instead of within three months from end of the calendar year, as required earlier.

- Instead of providing exact details of quantum and value accrued to the patentee through manufacturing and import into India, patentees are now permitted to mention approximate value and revenue accrued.

- A single form may be filed in respect of multiple patents, provided all of them are related patents, wherein the approximate revenue or value accrued from a particular patented invention cannot be derived separately from the approximate revenue or value accrued from related patents, and all such patents are granted to the same patentee.

- The requirement of declaration by the patentee to disclose whether public requirement has been met, partially met or not met, has been deleted.

The amended Form 27 also clarifies the following:

(i) Every patentee and licensee has to file Form 27 separately; and

(ii) If a patent is granted to two or more persons, they may file a single Form 27 jointly.

Liberalisation of OSP Guidelines

Recently, the Ministry of Communications, Department of Telecommunications (DoT) has issued the revised Other Service Provider (OSP) Guidelines (Revised Guidelines). These Revised Guidelines aim to significantly improve the ease of doing business for the Information Technology industry including Business Process Outsourcing (BPO)/ IT-enabled Services (ITeS) sectors, by reducing the compliance burden.

The Revised Guidelines have removed registration requirements and excluded entities providing non-voice-based services from the ambit of the OSP guidelines.

The key changes as per the Revised Guidelines are summarised below:

Key revised definition

- Authorised Telecom Service Providers Provisioned Virtual Private Network (VPN), means a network formed by the interconnection between OSP centres using leased circuits/ Multi-protocol Label Switching VPN (MPLS VPN), etc., from authorised licensees, for data transfer among the OSP centres.

- OSP is an Indian company, registered under the Indian Companies Act, 2013, or a Limited Liability Partnership (LLP) registered under the LLP Act, 2008, or a partnership firm, or organisation registered under the Shops and Establishment Act or a legal person providing voice-based BPO services.

- OSP centre means the infrastructure of an OSP at a location in India.

- Point of Presence (PoP) is a location where OSP places equipment, such as Private Automatic Branch Exchange (PABX), Interactive Voice Recording System, etc., to act as an extension of its OSP centre for collecting, converting, carrying and exchanging the telecom traffic related to its services.

No registration and approval requirement

- The requirement of obtaining OSP registration from the DoT and approval for sharing infrastructure has been removed.

Special dispensations outlined

- Permissibility to OSPs for the collection, conversion, carriage and exchange of the Public Switched Telephone Network (PSTN)/ Public Land Mobile Network/ Integrated Services Digital Network traffic over virtual private network such as National Private Leased Circuit, MPLS VPN interconnecting different OSP centres.

- Permissibility to carry the aggregated switched voice traffic from their PoP in a foreign country to their OSP centre in India over leased line/ MPLS VPN.

- Interconnectivity of two or more domestic and international OSP centres of the same company or group of companies is permitted

- Interconnectivity between OSP centres belonging to different OSP companies is now permitted.

- OSP may also operate by sharing infrastructure and adopting centralised EPABX (i.e. distributed architecture of EPABX).

- The requirement of furnishing any bank guarantee has been removed.

- Interconnection of remote agent to the OSP centre/ resources is permitted.

- An OSP having multiple centres may obtain an internet connection at a centralised location, and this internet can be accessed from other OSP centres using lease circuits/ MPLS VPN.

Work-from-home

- OSP may also operate as work-from-home (WFH) and work-from-anywhere (WFA) in India.

- WFH and WFA shall be treated as extended agent position/ remote agent of the OSP. The remote agent is also allowed to work from any place within India. However, OSP shall be responsible for any violation related to toll bypass.

Sharing of infrastructure for OSP centres

- OSPs are allowed to share common EPABX for international OSP centre, domestic OSP centre and PSTN lines for office use, subject to the OSP ensuring that there is no bypass of the network of the Authorised Telecom Service Providers.

- Distributed architecture of EPABX (main EPABX at a centralised location and media gateways at individual OSP centres) for OSP centres across India is permitted, where the EPABX is owned by the OSP. However, the OSP is required to preserve the Call Detail Records (CDRs) for all the voice traffic carried using the EPABX. The CDRs shall be segregated for each media gateway.

- OSPs are permitted to interconnect with the same company or the same group of companies for internal communication and for its operations.

Other key considerations including security conditions

- Bypass of licenced International Long-Distance Operator and National Long-Distance Operator should not occur.

- EPABX at foreign location in case of international OSP is now allowed, subject to compliance with the requirements of relevant provisions of Indian laws, including applicable data privacy laws. The OSPs would also be required to maintain copies of the CDRs and system logs in storage at any of its OSP centres in India.

- OSPs are required to preserve the CDRs for all the voice traffic carried using the EPABX (segregated for each media gateway) and the timestamp in the CDRs in the system of the OSP should be synchronised with the Indian standard time. It should be possible to view the CDR data along with details of the agent manning the position by remote login to the CDR machine/ server.

- The location of the EPABX and the client’s data centre, in case of domestic OSPs, needs to be within India.

- In case of EPABX installed at locations other than the OSP centre, the remote access of all call data records, access log, configurations of EPABX and routing tables shall be made available on demand by the authority/ law enforcing agencies from at least one of the OSP centres.

- The OSP shall extend support to the authority in tracing any nuisance, obnoxious or malicious calls, messages or communications transported through its equipment and network.

PwC comments The liberalisation of the OSP Guidelines is a significant step in reducing the onerous compliance requirements on the BPO/ ITeS sectors under the erstwhile guidelines

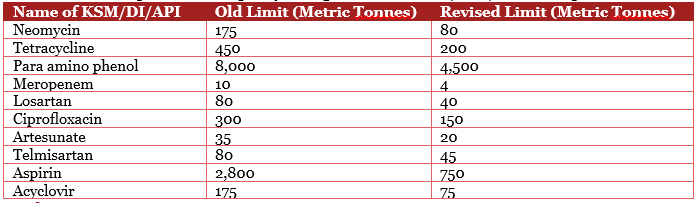

Revised guidelines – PLI Schemes for manufacturing of bulk drugs and medical devices

Further to the guidelines issued by the Ministry of Chemicals and Fertilizers, Department of Pharmaceuticals (Department) in July 2020, the Department has recently issued revised guidelines on 29 October 2020 in relation to both the Production Linked Incentive (PLI) Schemes to promote domestic manufacturing of medical devices and bulk drugs (Active Pharmaceutical Ingredients/ Key Starting Materials/ Drug Intermediates), in order to liberalise threshold requirements and provide clarifications on certain aspects. The revised guidelines supersede the guidelines previously issued by the Department on 27 July 2020.

The key changes as per the revised guidelines are discussed below:

Guidelines for PLI Scheme for promotion of domestic manufacturing of critical Key Starting Materials/ Drug Intermediates/ Active Pharmaceutical Ingredients in India

Timelines

Last date for application filing – extended from 23 November 2020 to 30 November 2020.

Incentive

Incentive to be provided on the sale of products – requirement with respect to ‘domestic’ sales has been removed.

Committed investment

- Minimum threshold investment prescribed under the Guidelines for PLI Scheme for promotion of domestic manufacturing of critical Key Starting Materials (KSM)/ Drug Intermediates (DIs)/ Active Pharmaceutical Ingredients (APIs) in India (guidelines for bulk drugs) has been deleted, and the concept of ‘Committed investment’ has been introduced. Relevant changes to this effect have been made throughout the guidelines for bulk drugs, such as changes to the definition of greenfield investment and net worth requirement, etc.

- The term ‘Committed investment’ has been defined to mean the amount of fresh investment as defined in the guidelines for bulk drugs that the applicant shall commit by declaration at the time of application.

- The requirement in relation to furnishing corresponding multiplier of Committed investment vis-a-vis increased commitment of minimum annual production capacity stands deleted.

Production thresholds

Minimum annual production capacity changed for few KSMs/ DIs/ APIs, are provided in the below table.

Bank Guarantee

The amount of bank guarantee that is required to be furnished by the selected applicants has been revised. Further, conditions under which such bank guarantee can be invoked has been deleted. It has also been clarified that a separate bank guarantee will be required to be submitted by the applicant for each such eligible product.

Guidelines for PLI Scheme for promoting domestic manufacturing of medical devices

Timeline

- Last date for application filing – extended from 23 November 2020 to 30 November 2020.

- Tenure of the PLI Scheme increased by one year from financial year (FY) 2026-27 to FY 2027-28.

Committed investment

- Minimum threshold investment prescribed under the Guidelines for the PLI Scheme for promoting domestic manufacturing of medical devices (guidelines for medical devices) has been deleted, and the concept of ‘Committed investment’ has been introduced. Relevant changes to this effect have been made throughout the guidelines for medical devices, such as change in definition of greenfield investment and net worth, etc.

- The term ‘Committed investment’ has been defined to mean the amount of fresh investment as defined in the guidelines for medical devices that the applicant shall commit by declaration at the time of applying under the PLI Scheme.

- Net worth requirement at the time of making application has been aligned with the requirement of Committed investment, and the specific requirement of INR 0.18bn net worth has been eliminated.

Incremental sales

- The threshold for the minimum incremental sales of manufactured goods has been reduced.

- It has been clarified that for the purpose of computation of incentive, the sale of eligible product means the sale of the eligible product manufactured by the applicant in the greenfield project approved and set up under the guidelines for medical devices.

Bank Guarantee

The amount of bank guarantee that is required to be furnished by the selected applicants has been revised. Further, conditions under which such guarantee can be invoked has been deleted. It has also been clarified that a separate bank guarantee will be required to be submitted by the applicant for each such eligible product.

PwC comments By issuing these revised guidelines, the Department has clarified various provisions of the existing guidelines and liberalised certain threshold requirements

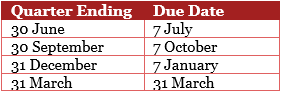

The Equalisation Levy (Amendment) Rules, 2020

The Central Board of Direct Taxes (CBDT) has amended the Equalisation Levy Rules, 2016 by Notification to align with the scope/ provisions of the Equalisation Levy (EL) expanded vide Finance Act 2020 w.e.f. 1 April 2020.

Background

In line with the Organisation for Economic Co-operation and Development’s Base Erosion and Profit Shifting project to tax e-commerce transactions, India had introduced EL at 6% on consideration paid or payable to a non-resident (NR) for online advertisement services w.e.f. 1 June 2016.

India expanded the provisions of EL, w.e.f. 1 April 2020, to include consideration received or receivable for e-commerce supply or services made or facilitated by an NR e-commerce operator (NR ECO) at the rate of 2%.

EL is required to be deposited by NR ECOs on a quarterly basis as follows:

Notified Rules

The CBDT has notified the EL (Amendment) Rules, 20207 (Rules), which suitably amend the EL Rules, 2016 dealing with the procedural framework for compliances and the appeals process to be followed for such levy. The amended Rules are effective from 28 October 2020. The relevant amendments are as follows:

Note

- Obtaining a Permanent Account Number (PAN) – unique tax identification number in India is mandatory to furnish Form No. 1 or filing of Appeal with the CIT(A) and the Tribunal. Further, it appears that the authorised person verifying the statement also has to furnish a PAN at the time of verification.

- The Form No. 1’s schema also allows the taxpayers to claim refund of EL discharged.

Tribunal holds dividend distribution tax payable by a company is subject to maximum rate in the relevant tax treaty

Facts

The taxpayer, an Indian company, is a 100% subsidiary of a German company. During the course of appellate proceedings, the taxpayer raised an additional ground of appeal before the Delhi bench of the Income-tax Appellate Tribunal (Tribunal), on the issue of extending the benefit of the applicable Double Taxation Avoidance Agreement (tax treaty) qua the rate of tax on the payment of dividend to the shareholder, as against the dividend distribution tax (DDT) rate currently applied.

Tribunal’s ruling

The Tribunal admitted the additional ground of the taxpayer, considering the decision of the Delhi High Court wherein a similar issue was raised by way of an additional ground of appeal.

On merits of the issue, the Tribunal first analysed whether the incidence of tax on dividends is a liability on the company or the shareholder. In this regard, the Tribunal has noted the following:

- The Bombay High Court in the case of Godrej and Boyce Manufacturing Co. had held that DDT is a tax ‘on the company’ and not ‘on the shareholder’.

- However, the genesis of charge for levy of income-tax under section 115-O of the Income-tax Act, 1961 (Act) lies in section 4 of the Act, which provides for charge of income-tax on the total ‘income’ of a person. As per section 2(24) of the Act, ‘income’ includes dividends.

- The term ‘tax’ as defined under section 2(43) of the Act includes additional income-tax levied under section 115-0 of the Act and it is a tax on income, which includes dividends.

- Based on an examination of the memorandum to the Finance Bills of 1997, 2003 and 2020, the Tribunal observed that the levy of DDT on the payer company was merely for administrative convenience to reduce the compliance burden and not based on legal necessity. It also observed that the levy of DDT is for all intent and purposes, a charge on dividend.

Accordingly, the Tribunal held that the economic burden of DDT falls on the shareholders rather than on the company, as the amount of distributed profits available for shareholders stand reduced to the extent of the DDT.

With regard to the applicability of the beneficial provisions of the tax treaty, the Tribunal observed that sections 4 and 5 of the Act are subject to the provisions of section 90 of the Act, which provides for the applicability of the provisions of the Act to the extent they are more beneficial than those contained in the applicable tax treaty.

- Relying on the Supreme Court’s decision in the case of Azadi Bachao Andolan, the Tribunal held that in case of any inconsistency between the provisions of the Act and the tax treaty, the tax treaty provisions shall prevail.

- Relying on the Delhi High Court’s decision in the case of New Skies Satellites, the Tribunal held that a statutory amendment under the Act cannot override the tax treaty provisions. Accordingly, the tax rate provided in the tax treaty in respect of dividend taxation should prevail over those prescribed under the Act, as far as they are more beneficial to the taxpayer.

- The liability of the company to discharge such tax as DDT would not be a relevant consideration for the purpose of applying the rates set out in the tax treaty and thus, the beneficial provisions of the tax treaty would also apply to the DDT provisionAccordingly, the Tribunal held that the concessional rate specified under Article 10 of the India-Germany tax treaty would apply in this case, and remanded the issue back to the Tax Officer (TO) to factually examine the applicability of other clauses of Article 10 of the tax treaty, dealing with the presence of permanent establishment in India for the beneficial owner of dividend in light of the documents filed by the taxpayer in support of its claim for the first time before the Tribunal.PwC comments: This is a welcome ruling as this has been a contentious issue for taxpayers over the years. As opposed to the ruling of the Mumbai bench of the Tribunal in the case of SGS India Private Limited, which merely remanded the issues to the TO for reconsideration without laying down any principle, the present ruling leaves no scope for ambiguity that the liability of tax on dividends would be subject to beneficial provisions of the tax treaty applicable to the shareholder. However, given that the Tribunal has only decided the matter in principle, and remanded the matter to the tax authorities for examination of fulfilment of conditions prescribed under the tax treaty, the test of ‘beneficial ownership’ would remain a critical aspect while claiming benefits under the tax treaty. More so, in the new regime where the DDT has been substituted by a classical system of withholding tax by the Finance Act 2020, and tax needs to be withheld on the dividend paid to the shareholders based on the rate provided in the tax treaty, if the shareholder is a beneficial owner of the dividends.

Government issues FAQs on rules administering origin compliance in free trade agreements

To curb the rampant misuse of free trade agreements (FTAs), the Government of India (GoI) introduced section 28DA in the Customs Act, 1962, through section 110 of the Finance Act, 2020, effective from 27 March 2020.

Under this enactment, a key provision for monitoring the correct use of FTAs is implementing a legal onus on the importer of goods with respect to the declarations made on the Certificate of Origin (CoO), compliance with value-addition requirements by the overseas manufacturer in terms of Rules of Origin (RoO) notified for the FTAs, etc. The enactment further requires the importer to possess value-addition/ costing-related data for goods imported using an FTA from 27 March 2020. Simultaneously, it incorporates different types of

consequences, including a penalty for the inability to share requisite information with the Customs Authorities. Pursuant to the aforesaid enactment, the GoI on 21 August 2020, notified the procedural and compliance requirements for importers, processes and timelines for verification by the Customs Authorities, etc., in the form of the Customs (Administration of Rules of Origin Under Trade Agreements) Rules, 2020 (CAROTAR, 2020). This came into effect from 21 September 2020.

Basis inputs received in trade consultations and outreaches, the Central Board of Indirect Taxes and Customs has released a set of Frequently Asked Questions (FAQs) relating to CAROTAR, 2020. Below is a summary of the FAQs:

- The importer needs to possess basic minimum information prescribed under Form-I, relating to the description of the production process undertaken in the country of origin, manner in which the origin criteria is determined, treatment of packing materials, etc. However, an importer is not required to submit Form-I when filing the Bill of Entry (BoE). Although when Customs Authorities doubt the origin of the goods, they can seek details in terms of Form-I and documents from the importer.

- The details, as required in Form-I, focuses on process, and thus, if it is the same for identical shipments, and there is no change in the production process or manner of processing, then, the same set of information can be used in filing Form-I for identical goods covered under multiple BoE.

- If the importer is unable to furnish complete information as per CAROTAR, 2020 requirements, import will be allowed with preferential claim. However, in such cases, the origin-related information will be sought by the Indian Customs from the verification authorities in the exporting country.

- If the exporter fails to furnish the required information, the Customs Authorities will initiate the verification process with the exporting country and suspend the preferential benefit. The goods will be allowed clearance provisionally against a bond and security. Subsequent claims will be verified and will not be facilitated through the Risk Management System. Therefore, an importer is expected to ensure, to the best of his abilities, that it possesses the required information prior to import.

- There is no requirement to mandatorily seek inf8ormation on cost break-up or proprietary production process. In relation to ‘components which constitute value addition’, there is no requirement to provide exact figures. It is only necessary to disclose the description of major components taken into calculation of domestic value addition, e.g., material, labour, profit, etc.

- As the RoO includes the criteria that a non-originating good should have undergone the required transformation, e.g., at the sub-tariff heading level, the importer is required to know how this was met, e.g., through the process of distillation/ assembly of components/ stamping/ cutting etc. Therefore, the production process can be recorded briefly, clearly incorporating how it meets the prescribed originating norms. Hence, there is no requirement of an elaborate explanation of the ‘production process’ with technical details.

- The CAROTAR, 2020 does not prescribe any specific standard for supporting documents. It could range from an email communication from the exporter, informing of various origin-related details, to photographs of the production site, demonstrating the process that a good undergoes in the exporting country.

- The preferential tariff treatment cannot be denied on identical goods when it was denied for the previous consignment. Preferential tariff treatment can be denied without verification of origin because of noncompliance of procedures or conditions laid out in the FTA itself, such as expired validity period of CoO or incomplete CoO. In case of identical goods in subsequent cases, it can be denied if the RoO criteria as prescribed in the FTAs are not met.

- The obligation on the importer originates from domestic law and not from the trade agreements. However, the origin-related provisions of the trade agreements have been incorporated in the domestic law by notifying the RoO of each FTA. Hence, in the event of a conflict, the provisions RoO notified for each FTA shall prevail to the extent of the conflict.

PwC Comments: Companies currently availing benefit under FTAs or planning to use FTAs in the future need to assess value addition holistically and all other criteria set out in the RoO of the respective FTA under consideration read with requirements of CAROTAR, 2020. As the authorities will be seeking information/ documents as per CAROTAR, 2020 requirements to seek RoO compliance, any inability to comply with these requirements could potentially have an adverse impact on business in terms of disruption, denial of benefit, penal consequences, etc.

Mumbai bench of CESTAT lifts corporate veil to reject assessable value between two Indian subsidiaries of an overseas parent; holds that companies are artificially created to maintain lower selling price for payment of excise duty

Recently, the Mumbai bench of the Customs, Excise and Service Tax Appellate Tribunal (CESTAT) rejected the transaction value adopted for the payment of Central Excise duty in a sale transaction between two Indian subsidiaries of an overseas parent company. This decision has examined in detail the terms of arrangement between the parties and the past judicial decisions in the context of section 4 of the Central Excise Act, 1994 (Act), both, pre and post amendment of the valuation provisions in July 2000

Facts

- The taxpayer was engaged in manufacturing and production of two car models, as per the designs and specifications of their parent company in Germany. The taxpayer only sold these cars in India to the other subsidiary of its parent company (marketing subsidiary).

- The marketing subsidiary is responsible for the promotion, advertisement, after sales support and distribution of the cars to the dealers. For this purpose, the taxpayer entered into a Service and Distribution Agreement with the marketing subsidiary. The marketing company also received reimbursement of a part of the marketing and sales promotion expenses from their parent company.

- The sale price between the taxpayer and the marketing subsidiary was attained by following the ‘Retail Minus method’, i.e., price after subtracting the marketing subsidiary’s margin from the retail sale price. The excise duty was paid on such sale price, treating it as the assessable value.

CESTAT’s ruling

The CESTAT held that the sale of cars by the taxpayer to the marketing subsidiary is not at arm’s length and the assessable value that the taxpayer declared was unacceptable. The following is a summary of the key observations and rationale by the CESTAT:

Mutuality of interest

- Both the taxpayer and the marketing subsidiary do not independently determine the value at which the taxpayer would transfer the cars to the marketing subsidiary. The ‘Retail minus’ method was used to arrive at the prices of cars. The prices were determined based on the planning rounds for the supplies/ deliveries of vehicles, held between the three parties. The documents and mails suggested that the parent company determined the price and dictated it to its two subsidiaries. The transfer value claimed to be the true transaction value was determined mutually between the two subsidiaries, which the parent company heads. The parent company made good any operating loss the taxpayer suffered.

- The taxpayer kept the cars manufactured in earmarked premises within its plant, after selling them to the marketing subsidiary. The sale of fully manufactured vehicles to the marketing subsidiary is after a defined area of control in the taxpayer’s premises, after which the taxpayer issues invoices in the name of the marketing subsidiary.

- This indicated a commonality of interest in marketing the cars and the distinction in functionality between the taxpayer and the marketing subsidiary had been created artificially, only with the intention to reduce the sale price, which has bearing on the amount of Central Excise Duty.

Lifting the corporate veil

- The two Indian subsidiaries are mere puppets in the hands of the parent company, who is the authority to determine and take decisions in relation to the production and sale of the vehicles in India.

- The parent company renders financial assistance to both the Indian subsidiaries to make them financially viable for their operation.

- In none of the cases relied upon by the Appellants during the course of arguments on appeal, has such an arrangement been considered.

- If the corporate veil is pierced, the entire operations of manufacture and sale of vehicles was throughout on account of the parent company. Referring to the Supreme Court’s decision, the CESTAT noted that when drafting the rules, lawmakers would not have envisaged such tri-partite arrangements, as in the present case. With multiplying business complexities, business models undergo changes and it is the bounden duty of the Courts and CESTAT to unearth and determine the real transaction, which should be taxed.

Valuation principle to be adopted

- The principles of determination of normal value and judicial exposition in respect of ‘normal value’ apply to ‘transaction value’, as held in Grasim Industries.

- The value claimed by the taxpayer to be the value as per section 4(1)(a) of the Act, does not stand to the test laid down by the Supreme Court in the case of Fiat India.

- The value that qualifies under section 4(1)(a) of the Act, can only be the value on account of sale at arm’s length, and not any value that is determined for the transfer/ clearance of goods.

- In the absence of value under section 4(1)(a) of the Act, the only route available to determine the value would be under section 4(1)(b) of the Act, through Rule 11 of the Valuation Rules, 2017. The value shall be determined using reasonable means consistent with the principles and general provisions and section 4(1) of the Act.

- By application of Rule 11 of the Valuation Rules, 2017, in case of transactions between related persons, it was held that the value has to be determined under Rule 9 of the Valuation Rules, 2017, i.e., on the basis of sale price, by the marketing subsidiary to the dealers.

- Benefit of cum duty price is available on the sale price of the marketing subsidiary to dealers.

Based on the above analysis, the CESTAT held that value of goods cleared by the taxpayer to the marketing subsidiary has to be determined on the basis of sale price by the marketing company to independent dealers, by treating the sale price as cum duty price.

The issue of valuation was always within the knowledge of the department, taken up in audit and part of the Comptroller and Auditor General of India report (CAG Report). As the issue was under discussion and the Revenue entertained the correctness of the valuation methodology as per the CAG report, change in opinion or insufficiency in enquiries made cannot be grounds for invoking an extended period of limitation. Penalties levied were set aside, as there was no suppression of facts and the issue involved the interpretation of statutory provisions.

PwC Comments: This is an important ruling that discusses the principles of valuation in a related party transaction involving ‘mutuality of interest’. The CESTAT has based it’s ruling on a detailed analysis of the terms of arrangement between the Indian subsidiaries and their foreign parent and various judicial precedents. This is a unique ruling in which the CESTAT has lifted the corporate veil on specific facts and circumstances and held that the manufacturing and marketing functions have been spilt artificially to obtain a lower assessable value. Revenue authorities will likely rely upon this ruling in similar situations to question the valuation adopted under the Central Excise laws. The analysis of mutuality of interest, control over pricing, etc., may also be considered in the context of determining the value of supplies between related persons in the GST law.

Madras High Court decides against carry forward of unutilised cess into GST

Recently, the Division Bench of the Madras High Court reversed the final order passed by the Single Judge. The High Court held that a taxpayer is not entitled to carry forward credit of unutilised and accumulated Central Value Added Tax (CENVAT) credit of the cesses (namely, Education Cess, Secondary and Higher Education Cess and Krishi Kalyan Cess, collectively referred to as cesses) and utilise them against any output liability under the goods and services tax (GST). Some of the key observations of the Madras High Court were as under:

Cess is not in the nature of a ‘duty’ or ‘tax’

- The purpose and collection of any cess remains distinct, as any cess amount collected, is liable to be spent for the avowed and dedicated purpose for which such imposition was made, unlike in the case of collection of taxes. Such distinction is a settled principle of law and the Supreme Court has upheld it in various decisions.

- The mere facility of taking credit of cess paid on input goods or input services to avoid the cascading effect on multiple transactions does not militate or alter the character of the levy in the nature of a cess.

Cesses were not subsumed under the GST law

- Only specified taxes and duties were subsumed under the CGST Act and no such subsumation can be concluded by way of inference.

- The transition of unutilised CENVAT credit could be allowed only in respect of taxes and duties that were specifically subsumed.

No entitlement to avail credit of cesses after their abolishment in 2015

- Merely the positive act of having ‘taken’ the amount of the cesses in the Electronic Credit Ledger through an accounting entry has no bearing on the issue of statutory entitlement of such credit.

- Any credit in respect of cesses after the levy itself has ceased, cannot be termed as ‘CENVAT credit’.

- No vested right is created in favour of the taxpayer to claim such transitional credit and set off against such output liability under GST.

- The question of their carry forward and utilisation has become purely academic once the levy of cesses itself ceased in 2015, and particularly, since the prohibition on the cross-utilisation of cesses against any duty of excise or service tax already existed.

Explanation 3 to section 140 of the CGST Act specifically excludes cesses

- Explanation 3 specifically excludes the cesses for the purpose of carry forward and set off under section 140 of the CGST Act, which is clearly applicable to gather the legislative intent behind such insertion by the Parliament.

- Explanation 3 has its own force and application and does not have a limited application in context of its linkage to Explanations 1 and 2 to section 140 of the CGST Act. Explanation 3 cannot be applied in a restricted manner only to the specified sub-sections of section 140 of the CGST Act mentioned in the Explanations 1 and 2 and shall apply to section 140 of the CGST Act as a whole.

Recourse cannot be taken under section 140(8) of the CGST Act

- Section 140(8) of the CGST Act and all Explanations to section 140 of the CGST Act are to be read harmoniously to give it a purposeful meaning for transitional credit available for set off against any output liability under the CGST Act.

- Sub-section (8) of section 140 of the CGST Act, as relied upon by the Single Judge, employs the phrase ‘allowed to take’. When contrasted with other sub-sections to section 140 of the CGST Act, which employ the phrase ‘entitled to take credit’, this reveals that the availment of such credit, vide the Electronic Credit Ledger and Form TRAN-1, does not guarantee any such right of utilisation independent of other subsections of section 140 of the CGST Act and at the cost of ignoring Explanation 3.

- It is impermissible to treat section 140(8) of the CGST Act as an independent or stand-alone code of regulations (governing only service providers holding centralised registration) and provide for separate entitlements therein.

Input tax credit is in the nature of ‘concessions’ and not ‘entitlements’

- Reliance was placed on the Supreme Court’s decision in the case of Jayam and Co., wherein it was held that CENVAT credit or input tax credit is a concession or facility provided and not a vested right. Notwithstanding this principle, all statutory rights can be curtailed and regulated by conditions governing the availment of such rights.

- The provisions, viz., section 140 of the CGST governing transitional credit, also contain conditions that are required to be satisfied in relation thereto. Therefore, no conclusion on vested rights can be made in light of the same.

PwC Comments: The Division Bench of the Madras High Court upsets the position on carry forward credit of cesses, stating that credit is not a vested right but a concession, which is made available subject to the specified conditions being satisfied. The Court observed that cross-utilisation between cesses and duties/ taxes was not permitted prior to 1 July 2017 and the cesses were not subsumed into GST. The decision, while being well-reasoned and undertaking extensive analysis, does not address the validity of the retrospective insertion of Explanation 3 to section 140 of the CGST Act with effect from 1 July 2017, or the failure to make the same specifically applicable to sub-section (8) of section 140 of the CGST Act. While this decision holds that the unutilised credit cannot be transitioned to GST, the issue is open with regard to the lapse of unutilised credit (in the absence of a specific lapsing provision), and whether the taxpayer can claim refund of such credit.

CESTAT directs applications for refund of accumulated and unutilised credit of KKC to be kept in abeyance until the Supreme Court’s decision on the issue

Issue in brief

The issue before the Customs Excise and Service Tax Appellate Tribunal (CESTAT) in the instant excise appeal was, whether a taxpayer is entitled to refund of accumulated and unutilised credit of Krishi Kalyan Cess (KKC) appearing in the Central Value Added Tax (CENVAT) credit register, as the same cannot be utilised on account of implementation of Goods and Services Tax (GST).

CESTAT’s ruling

The Karnataka High Court, in the case of Slovak India Trading Co. Private Limited, had allowed refund of unutilised credit on closure of factory or business premises under Rule 5 of the CENVAT Credit Rules, 2017, stating that no express prohibition against granting of refund in such situations was created thereunder. The Karnataka High Court also relied on judgements relating to Modified Value Added Tax regime where such refund was allowed. Further, an appeal filed with the Supreme Court by the Union of India was dismissed, with the question of law being kept open. This decision was followed in a slew of decisions issued by various benches of the CESTAT and High Courts across India. Thereafter, the decision was also followed by the division bench of the Bombay High Court in the case of Jain Vanguard Polybutylene Limited.

The Larger Bench of the Bombay High Court, in the case of Gauri Plasticulture Private Limited considered the correctness of the Slovak India Trading decision, wherein the High Court held that cash refund under section 11B of the Central Excise Act, 1944 is not permissible when CENVAT Credit on inputs remains unutilised on account of closure of manufacturing unit or any generic inability to utilise input credit. It was held that one of the fundamental principles in a fiscal statute is that nothing can be read into its provisions that is expressly not provided. In other words, an implied meaning cannot be given, and this was incorrectly done by the Karnataka High Court in the Slovak India Trading decision. It was also observed that the appeal dismissed by the Supreme Court in the case of Slovak India Trading Private Limited is not a confirmation or approval of view and cannot be read as a declaration of law under Article 141 of the Constitution of India. An appeal against the decision passed by the Larger Bench of the Bombay High Court in the case of Gauri Plasticulture Private Limited is currently pending before the Supreme Court.

The CESTAT did not pass orders on merits since the Supreme Court is seized of the issue in the case of Bombay Dyeing & Manufacturing Co. Limited, and remanded the refund application to the original authority for de novo examination, once the issue is settled by the Supreme Court.

PwC comments The eligibility to claim refund of accumulated cess balances has been a subject of intense discussion and debate post introduction of GST, since the GST law restricts transition of such balances. Absence of a refund or set off mechanism results in expunging these cess balances, resulting in cost to the taxpayer. While the Ahmedabad Bench of the CESTAT has directed the officers to keep the refund application pending, the Division Bench of the CESTAT, Delhi in Bharat Heavy Electricals Limited, had upheld the grant of refund of accumulated credit of cesses (viz. Education Cess, Secondary and Higher Education Cess and KKC) following the Slovak India Trading decision. This decision may impact the approach of original or appellate authorities when dealing with such pending refund matters

Gujarat High Court upholds validity of amendments to Rule 96(10) of the CGST Rules, thereby denying rebate benefit to Advance Authorisation License holders

Recently, the Gujarat High Court upheld the amendments made to Rule 96(10) of the Central Goods and Service Tax Rules, 2017 (CGST Rules) vide Notification No. 54/2018-Central Tax dated 9 October 2018 (Amendment Notification), to the extent that it denies rebate (refund) to a person who has imported goods under an Advance Authorisation License (AA License). It held that the Amendment Notification is to be made applicable retrospectively with effect from 23 October 2017.

PwC Comments: Owing to the ambiguity around the applicability, a judgement clarifying the implications of the series of amendments in Rule 96(10) of the CGST Rules was most awaited. However, the High Court has observed that the issue of the Petitioner seems to be resolved to the extent of the Explanation being inserted in Rule 96(10) of the CGST Rules. The decision has not discussed other aspects such as the constitutional validity of amending notifications and the reason for denying the rebate benefit, which may have a huge impact on the industry. We will have to wait for decisions by other High Courts and the Supreme Court to deal with the constitutional validity of the amendments in greater detail and obtain further clarity on the issue.

Government issues additional clarifications on manufacturing and other operations in bonded warehouse

Background

To promote the ‘Make in India’ initiative and as a part of the Ease of Doing Business measures, in 2019, the Central Board of Indirect Taxes and Customs (CBIC) had notified the Manufacture and Other Operations in Warehouse Regulations (MOWR). The facilitation enables businesses to import raw materials and capital goods without paying duty for manufacturing and other operations in a bonded manufacturing facility for domestic market and exports.

The CBIC explained the modalities of the MOWR scheme through a circular.

On the basis of representations received from trade bodies on specific issues, the CBIC has clarified certain aspects regarding operations under the MOWR.

The following is a summary of the clarifications.

Job work for a CBW unit

The custom bonded warehouse (CBW) unit can send inputs for job work; however, it can send capital goods only for repair, against permission from the bond officer. The job work will be subject to the following conditions:

- Inputs will be first brought into the bonded warehouse and duly accounted for in the records.

- Co-relation to be established between goods sent out and received.

- Subject to MOWR, finished goods can be brought back or exported/ cleared to domestic tariff area (DTA) from the premises of job workers. The date of removal from job workers premises will be the deemed date of removal from the bonded warehouse.

- Scrap/ waste to be returned to the bonded warehouse or cleared from the job workers premises on payment of applicable duties.

- A bonded warehouse holds a goods and services tax (GST) registration; hence, the procedure and timelines as prescribed under the GST law for job work will be applicable for such removals and receipt.

- Records and accounts to be maintained in terms of MOWR.

Additionally, mould, jigs, fixtures, patterns, drawings, etc., can also be sent to the job workers’ premises subject to the proper accounting of such goods by the bonded warehouse, and they are used only for the bonded warehouse unit. It must follow procedure and timelines as per the GST law. Bond requirement will apply to the bonded warehouse unit and it must adhere to it, irrespective of removal of goods for job work.

CBW undertaking job work

As the bonded warehouse unit is a GST registrant too, it can undertake job work and maintain records of such activities in terms of the GST law. If it uses any imported inputs in such activity, it is necessary to pay the applicable customs duty on the clearance of job worked goods from the bonded warehouse to the DTA. However, it must pay no duty if the job worked goods are exported.

Procurement of goods from FTWZ by CBW

Since there is no restriction on sourcing of goods by the CBW unit and these units hold GST registration, which in any case, can procure goods from Free Trade Warehousing Zone (FTWZ)/ Special Economic Zone (SEZ). Hence, these units can procure inputs and capital goods from FTWZ/ SEZ by complying with the prescribed procedure.

PwC Comments: The operational flexibility extended to businesses in terms of duty deferment, interface with domestic market, etc., by the MOWR makes it a potential alternative vis-à-vis other options for undertaking manufacturing in India. The clarifications will hopefully address some concerns of these businesses and enable them to adopt the MOWR

CBIC issues additional FAQs on manufacturing and other operations in bonded warehouses

To promote the ‘Make in India’ initiative and as part of the Ease of Doing Business measure, the Central Board of Indirect Taxes and Customs (CBIC) had notified the Manufacture and Other Operations in Warehouse Regulations (MOOWR or Scheme) in 2019. The facilitation enabled businesses to import raw materials and capital goods without payment of duty for manufacturing and other operations in bonded manufacturing facilities for exports while allowing import duty deferral for the domestic market.