President's Note

Dear Friends,

The rapid and widening spread of the COVID-19, crumbling global economic outlook, falling oil prices, and financial market unrest has created severe and extensive economic and financial shocks. From call centres to hotels to airlines, India’s key services ventures have ground to a halt during the coronavirus outbreak, dragging the economy into perhaps its worst recession on record. Gross Domestic Product data estimates that India’s economy grew at its slowest pace in the last two years in the March quarter as the coronavirus pandemic weakened the already declining consumer demand and private investment sentiment.

Services emerged as the key employment growth engine before the crisis hit, with the sector even outperforming agriculture and industrial expansion when the economy was slowing last year. Unlike manufacturing-heavy economies like China and South Korea, in India, the services sector accounts for 55% of Gross Domestic Product and the slump in output has had ripple effects on jobs and economic growth.

The lockdown though has forced businesses offering services like food delivery, hotel bookings and real estate to cut jobs in recent weeks. The tourism industry is non- existent and is expected to witness an unprecedented scale of job losses. Currently 60% of branded hotels in India are shuttered while the remaining 40% are operating with less than 10% of revenues. India has allowed businesses to begin gradually reopening since April 20, but a shortage of workers has made it difficult to resume operations fully.

The tally of cases has spiked in India this month, with widespread movement of people via special trains and flights and also due to the easing of various restrictions during the ongoing fourth phase of the nationwide lockdown. Many States have attributed the rising numbers to the influx of people from outside.

Although Kerala had managed to flatten the curve, it is suffering from the socio-economic consequences of the lockdown. Some measures have already been relaxed so that economic activities can resume, but the State remains vigilant, setting up protocols to prevent a spike in infections due to the return of thousands of migrant workers stranded abroad or in other States across the country.

The Reserve Bank of India said that the impact of COVID-19 is more severe than anticipated, and the GDP growth during the current financial year is likely to remain in the negative territory. It projected some pick-up in growth impulses from the second half of 2020-21 onwards.

Earlier this month, the Government announced about Rs 21 lakh crore stimulus package to help the nation tide over the economic crisis induced by the coronavirus and the lockdown to curb its spread. The mega economic package includes the Reserve Bank’s Rs. 8.01 lakh crore worth of liquidity measures.

The Finance Minister had announced this economic package in five tranches, which included a Rs. 3.70 lakh crore support for MSMEs, Rs. 75,000 crore for NBFCs and Rs. 90,000 crore for power distribution companies. Besides this, free food grains to migrant workers, tax relief to certain sections and Rs. 15,000 crore allocation to the healthcare sector to deal with the pandemic, were also announced as part of the economic package.

We can hope that despite the pain and destruction that COVID-19 has inflicted upon the whole world, these initiatives will usher in a new era of opportunities for every Indian.

On the 8th of May 2020, we had organised a ‘Virtual CEO Forum Meeting’. Mr. Aditya Narwekar, Partner, M&A Tax & Regulatory Practice, PwC India, and Mr. Kunal Wadhwa, Partner, Indirect Tax, PwC India were the Speakers for the meeting and they spoke on the topic “COVID: Impact on the Tax and Regulatory Environment in India.” The Forum discussed the various measures taken by RBI and SEBI, the major changes in Direct and Indirect taxes and the Foreign Trade Policy.

Let us hope that the worst of this pandemic is behind us and that we will be able to revive the economy at the earliest.

Stay Safe Everyone!!!

V Venugopal

Chamber Vlogs!

The Cochin Chamber has come up with a new initiative entitled ‘Chamber Vlogs.’ The intention of this series of short videos is to discuss topics of current relevance and to present them in an interesting and simple way.

We have so far released 6 videos since the first one on the 11th of May 2020. All the videos can be viewed from the video players seen below. We have many more videos lined up for release in the coming weeks. We will keep uploading new and relevant content for our members and the industry in general.

Kindly share these videos with your networks and subscribe to the Chamber’s YouTube Channel for more informative content.

Chamber Vlog - 01

Mr. Ashish Bhakta, Partner ANB Legal, Mumbai, explaining the Government’s rational behind the decision to make its prior approval mandatory for Foreign Direct Investments from countries that share a land border with India aimed at curbing”opportunistic takeovers” of domestic firms following the Covid-19 pandemic. Countries that share land borders with India are China, Bangladesh, Pakistan, Bhutan, Nepal, Myanmar, and Afghanistan.

Chamber Vlog - 02

Mr. Sarat Valsraj, General Manager of The Zuri Kumarakom, Kerala Resort & Spa discuss the Impact of the Lockdown and the future prospects of the Hotel and Tourism Industry post the Covid-19 pandemic.

Chamber Vlog - 03

Mr. Mark Sequeira, CEO – Maestro Human Resources, Bangalore and a Master Trainer speaking about the importance of staying positive amidst this pandemic and the need to reset and rebuild our Businesses and stay resilient until things get better.

Chamber Vlog - 04

Adv. Prashant Shivadass of Shivadass & Shivadass Law Chambers, Bangalore, who will encapsulate all of the Fiscal Reforms and the Legal Reforms that have taken place during the first two weeks of May 2020.

Chamber Vlog - 05

Mr. Arun James, Business Head at Outcome Infotech, Bangalore explains his views and ideas as to how Marketing per se, should evolve during these difficult times and beyond.

Chamber Vlog - 06

Adv. Ashish Bhakta, Partner ANB Legal, Mumbai, speaks about the “Effectiveness of the Conciliation Process in Resolving Disputes”.

Chamber's Repository for all the Notifications and Guidelines pertaining to the COVID-19 outbreak & resulting lockdown

Click here to gain access

Recent Event

CEO FORUM 2020

Virtual Meeting - COVID: Impact on the Tax and Regulatory Environment in India

The Cochin Chamber of Commerce and Industry conducted a Virtual CEO Forum Meeting on Friday, 8th of May, 2020.

Mr. Aditya Narwekar, Partner, M&A Tax & Regulatory Practice, PwC India, and Mr. Kunal Wadhwa, Partner, Indirect Tax, PwC India were the Speakers at the meeting. They addressed the “Impact on the Tax and Regulatory Environment in India” in the light of the Covid pandemic.

The President of the Chamber Mr. V Venugopal briefly welcomed the participants to the virtual ‘zoom’ meeting.

Initiating the session, Mr. Narwekar said that in light of the unprecedented times faced by the companies in India, the Ministry of Corporate Affairs (MCA) vide notification dated 19th March 2020 has relaxed certain provisions concerning the requirement of the physical presence of the Directors at Board Meetings allowing for all Board Meetings to be held till 30th June 2020 can now be held through video conferencing or other audiovisual means. For compliances, no additional fees will be charged for late filing during the moratorium period from April 1, 2020, to September 30, 2020.

Mr. Narwekar explained the various measures taken by the RBI and SEBI such as the extension of the period of realization of the value of exports to 15 months from the date of export and the relaxation of certain obligations and disclosure requirements such as filing of corporate governance reports and processing of documents on Foreign Portfolio Investors.

The threshold of default under Section 4 of the IBC has been increased from Rs 100,000 to Rs 10 million to prevent triggering of insolvency proceedings against MSMEs. If the current situation continues beyond 30 April 2020, Section 7, 9, and 10 of IBC will be suspended for 6 months to stop companies at large from being forced into insolvency proceedings in such force majeure causes of default, he said.

Mr. Wadhwa explained the major changes on the Direct and Indirect Tax regime. He said that the due date for filing the belated and revised tax returns for FY 2018-19 had been extended to 31st June 2020. An individual can claim a 100 percent deduction for a donation to PM CARES Fund. For claiming deduction in the return for FY 2019-20, donations to the PM CARES fund can be made till 30th June 2020, he said.

Mr. Wadhwa said that in the Vivad Se Vishwas Scheme, an individual was required to pay an additional percentage of the disputed taxes if the taxes were paid after 31st March but before 30th June 2020. As per the measures announced, even if the taxes are paid after 31st March but on or before 30th June 2020, no additional percentage of the disputed taxes is payable. The lower/NIL withholding certificates held for FY 2019-20 shall be valid till 30th June 2020 pending grant of approval by the tax department for a new certificate for FY 2020-21.

Mr. Wadhwa said that the due date for filing of annual returns under the GST legislation for Financial Year 2018-19 has been extended to June 30th, 2020. The due dates for filing of monthly returns under the CGST Act for February, March, and April 2020 have also been extended to the last week of June/ first week of July for taxpayers, basis their aggregate turnovers in the last FY. Taxpayers with a turnover of up to INR 5 crore are also eligible for a waiver of late fees, interest, and penalty on delayed payment of tax and filing of returns. Those with a turnover of above INR 5 crore would have to pay interest @ 9% per annum (against the prevalent 18%) on late payments, beyond the extended due dates.

The Government has also extended the validity and benefits under the Foreign Trade Policy up to March 31, 2021. Further, the expiry period of import or export authorizations, ending between February 01, 2020, to July 31, 2020, has also been extended for six months, he said. This would maintain the status quo and mitigate any potential pitfalls of the lockdown.

Following this there was a brief discussion wherein the Speakers clarified the issues raised by the participants.

The meeting ended with the President thanking everyone for having participated in the meeting.

Quote

Fine Points

Article

PAYMENT OF WAGES DURING COVID – 19: AN ANALYSIS

Priyanka Yavagal - Shivadass and Shivadass Law Chambers, Bangalore

“The outbreak of Covid19 is an unprecedented economic and human catastrophe”. When the global community accepted this quote, it meant that they were unprepared for this monumental shift in situations and to adopt a ‘new normal’. The domino effect placed by China, saw a collapse in global normalcy across the world and has thus called for uncertain unconventional measures to be implemented.

Following the declaration of Covid-19 as a “National Disaster” under the Epidemic Diseases Act, 1897, the Central Government and several State Governments in India, have imposed a regulated lockdown. With a view to ensure that the dense population are not left at the mercy of the virus, the Ministry of Labour and Employment issued an advisory on March 20, 2020, advising all employers (be it public or private), to extend their cooperation by not terminating the employees, especially casual and contractual workers, or reducing the wages of such employees. The advisory further stated that in case the place of employment is made non-operational due to the COVID-19 pandemic, then the employees of such unit will be deemed to be on duty. Thereafter, the Ministry of Home Affairs (‘MHA’) issued an order on March 29, 2020 in exercise of its power under section 10 (2) (l) of the Disaster Management Act 2005 (‘Act’), directing the States and Union Territories to take measures to ensure that all employers, be it in the Industry or under the Shops and Commercial Establishments, pay wages to their workers without any deductions for the period entire duration of the lockdown. A non-compliance of this order leads to criminal sanctions on the respective employer.

The order dated March 29, 2020 issued by the MHA was challenged by industries before the Hon’ble Supreme Court of India as being unconstitutional on several grounds including infringement of fundamental right to freedom of the industrial units and enterprises to carry on any occupation, trade or business under Article 19 of the Constitution of India, since it leads to a collapse of industrial units if salaries are forced to be paid without any revenue. Notwithstanding the above orders and directions, many employers initiated measures such as reduction of salaries, leave without pay, adjusting the applicable annual paid leaves against the days without work, terminating large number of employees and in some extreme cases declaring bankruptcy.

Faced with the above difficulties, a few trade unions and workers have also filed counter petitions seeking protection from wrongful termination and payment of wages. In one such petition filed by the Rashtriya Shramik Aghadi, a contract labourers’ union, the Aurangabad Bench of the Bombay High Court, on May 12, 2020, held that the principle of ‘no work-no wages’ cannot be applied during the present extraordinary situation prevailing in the country due to the COVID-19 pandemic and directed the principal employer to ensure that the contractor pays full wages, save and except food allowance and conveyance allowance, to the employees for the months of March, April and May, 2020.

On May 15, 2020, the Supreme Court terming the aforesaid MHA Order dated March 29, 2020 as an “omnibus order”, asked the government to re-examine the same and stayed its operation. The Government was also directed not to take any coercive steps against private companies who were unable to pay wages to workers. While things stood thus, the Government withdrew this order through a clarification dated May 17, 2020. It is therefore no longer compulsory for employers to pay the workers even when the organizations remain shut due to the lockdown 4.0. The MHA order dated May 17, 2020, reads as under:

“save as otherwise provided in the guidelines annexed to this order, all orders issued by the NEC (national executive committee) under Section 10(2)(I) of the Disaster Management Act, 2005, shall cease to have effect from 18 May 2020.”

Given the above, it becomes relevant to analyze the legality and the background of the advisories, orders and directions issued by the Central and State Government in binding employers with the liability to pay its employees during a daunting situation created due to the catastrophic outbreak of COVID-19.

The scope of the Act is to have a unified command over disaster management. It also empowers National Executive Committee appointed under the Act, to frame plans in order to meet disasters. A bare reading of the provisions of the Act indicate that the MHA does not have the power to issue directions to employers of any industry, shop and commercial establishment, private enterprise to pay wages during a disaster despite the employees not working. Similarly, the Epidemics Diseases Act, 1897 only enables the Government to prescribe measures to prevent the outbreak of such disease or the spread thereof and does not empower the Government with a power to direct a private employer to pay wages.

The major aspect of employment i.e., payment of wages, minimum wages, bonus, gratuity, contribution to provident funds, pension funds etc., are all governed under various labour legislations. These are being significantly revamped in the form of a Labour Code, which is pending discussions before both houses of the Parliament (some even before the standing committee). While these legislations are the primary source and genesis of power, another major influence for employment are contracts since it is essentially a relationship between the employer and the employee.

Arguments have been made that the order of the MHA dated March 29, 2020, pertains to issues falling within the domain of private employment governed by the employer-employee relationship. The exercise of power by the Central Government under the Act therefore is illegal. The MHA order dated May 29, 2020 can at best be an advisory and cannot have any mandatory effect.

On the other hand, several arguments have been made that the Act and powers conferred under it to the National Executive Committee, supersede any other power under any other legislation as this Act derives its powers from the Concurrent List (under Article 246 and List III) of the Constitution of India. Therefore, it is only the Central Government that will have the powers to pass such orders. These orders are omnibus orders and can supersede any other legislation for the time being in force.

In my view however, employers of industries or shops and commercial establishments cannot be fastened with any financial liability as a measure to mitigate disaster. The obligation cast on the private employers to ensure payment of wages during the period of lockdown appears to suffer from the vice of wrongful exercise of power and overreach of authority. This imposition cast on private employers could undoubtedly be termed as capricious and unwarranted as it appears to have no rational nexus for the purposes of achieving the objectives of the Act and Epidemics Diseases Act.

Article 19 (1)(g) of the Constitution of India enables both an employer and an employee to carry on any occupation, trade, or business, which fundamental right stands effectively suspended during the lockdown. However, it appears that the order by the MHA dated March 29, 2020, only seeks to take measures to mitigate the economic hardship of the employees/workers to the detriment of the employer.

Further, from a humanitarian perspective, casting a financial obligation on private employers to ensure timely payment of wages without any monetary aid from the Government at a time when operations are nil and no revenue is / can be generated for the foreseeable future, is prejudiced. This, given that several State Governments including Telangana and Maharashtra itself have taken an executive decision to deduct salaries including that of the Chief Minister, Cabinet Ministers, local bodies, PSUs etc.

The measures adopted by the Government to mitigate economic hardship, has overlooked the rights of an employer and have failed to consider that COVID-19 is adversely impacting both employer and employee. As the nationwide lockdown has been extended by the Government, it is likely that all businesses across all industries would be severely impacted. In such a situation it would neither be prudent nor fair to further direct an employer to continue payment of wages to its workers without any corresponding business being transacted by them. Therefore, a balanced approach towards the same was incumbent on the Government.

Now that the MHA has, by virtue of order dated May 17, 2020, withdrawn all its earlier orders on this subject. However, it is still unclear if payments between March 29, 2020 and May 17, 2020, are still to be made to the employees. The Supreme Court will decide this ambiguity on May 29, 2020. A word of caution though to all employers – since notice has been issued by the Supreme Court and the matter is still pending adjudication, employers must be careful in acting freely as the force of the March 29, 2020 has not been made illegal. It is better that the employers continue to comply with the MHA March 29, 2020 order until the matter is finally adjudicated upon by the Supreme Court.

While the intentions of the Government appear to be noble, the measures adopted to ensure payment of wages are clearly not adequate to tackle the problem. The need of the hour is a dedicated framework in the form of monetary subsidies similar to the ones declared by Governments across the globe. In the absence of assistance and measures, industries or shops and commercial establishments will be put through hardships that would most likely push them to bankruptcy, the impact of which will be on the workers that are far greater than the pandemic itself.

*The author is an Advocate with Shivadass & Shivadass (Law Chambers) The contents and comments of this document do not necessarily reflect the views/position of Shivadass and Shivadass (Law Chambers) but remain solely of the author(s). For any further queries or follow up, please contact [email protected].

Tax and Regulatory Updates from PricewaterhouseCoopers

Regulatory

COVID-19 update: Economic, regulatory and Tax measures announced by Finance Minister to help boost the Indian economy

The Finance Minister (FM) over a span of five-days has announced a special economic and comprehensive package that when added to the earlier stimulus announcement and the liquidity infusion through previous monetary measures announced by the Reserve Bank of India adds up to over INR 20 trillion – equivalent to about 10% of India’s gross domestic product. The measures have been directed at providing relief to the poor and needy and providing a helping hand to businesses towards getting the Indian economy up and running again post the COVID-19 pandemic fallout. The Prime Minister (PM) in his address to the nation on 12 May 2020 had said that the pandemic should be looked at as a crisis and the challenge is an opportunity to build a “Self-Reliant India”. The FM has announced the intent to undertake several short-term and long-term reform measures along with the monetary and fiscal stimulus package. The announcements on these today include measures and reforms to enhance Ease of Doing Business for corporates, Insolvency and Bankruptcy Code (IBC), public sector enterprise policy for a new, self-reliant India, technology-driven education, healthcare, Companies Act, support to State Governments. The relief measures announced aim to help businesses, including micro, small and medium enterprises (MSMEs) recover from the economic impact of the COVID-19 pandemic and “getting back to work.” Further, the hardship of individuals was also recognised, and consequent suitable relief measures were announced. Effort to strengthen Non-Banking Finance Institutions (NBFCs), Housing Finance Companies (HFCs), Micro Finance Sector and Power Sector were also announced. In addition, tax relief to businesses, relief from contractual commitments to contractors in public procurement and compliance relief to the real estate sector were also covered.

This Insight is based on the information released by the Press Information Bureau. It is recommended that implementation decisions be taken after reviewing the necessary notifications and/ or required legislative amendments giving effect to these announcements.

The measures announced by the FM are listed in detail below.

Direct Tax

- Reduction in rates of TDS and TCS: To provide more liquidity in the hands of taxpayers, reduction in the rates of tax

- Deducted at source (TDS) for non-salaried payments made to residents (that include payments to contractors for carrying out work, professional fees, interest, rent, dividend, commission, brokerage, etc.), and rates of tax collection at source (TCS) by 25% of the existing rates has been announced. This benefit shall be effective for the remaining part of the financial year (FY) 2020-21, i.e., from 14 May 2020 to 31 March 2021.

- Extension in due dates for filing income-tax returns: To ease the burden of compliance, due date for filing all income-tax returns for FY 2019-20 (corporate or non-corporate) shall be extended from 31 July 2020 and 31 October 2020 to 30 November 2020. In addition, the due date for filing tax audit reports has also been extended to 31 October 2020 (from 30 September 2020).

- Extension of timelines for time-barring assessments: All assessments time-barring on 30 September 2020 will now be extended to 31 December 2020. In addition, all assessments time-barring on 31 March 2021 shall now stand extended to 30 September 2021.

- Extension of the Vivad se Vishwas (VsV) Amnesty scheme: The period of applying for the VsV scheme has been extended until 31 December 2020 (from the current due date of 30 June 2020) without paying any additional amount.

- Processing of income-tax refunds: Immediate processing of all pending refunds of non-corporate taxpayers (charitable trusts and non-corporate businesses and professions, including proprietorship, partnership, limited liability partnership, and co-operatives) to facilitate liquidity in the hands of taxpayers..

Indirect tax

- Special ‘Refund and Drawback Disposal Drive’ implemented up to 30 April 2020, for all pending refund and drawback claims (vide Instruction No. 3/2020-Customs dated 9 April 2020).

- Relaxation in GST compliances, including with nil/ reduced rate of interest and waiver of late fees for belated filings (vide Notifications issued on 3 April 2020)

- 24 hours custom clearance facilitated till 30 June 2020 (vide Instruction No. 02/2020-Customs dated 20 February 2020).

Real Estate

- COVID-19 to be treated as an event of “Force Majeure” under Real Estate (Regulation and Development) Act, 2016 (RERA).

- Automatic extension of registration and completion date by six months for all registered projects expiring on or after 25 March 2020. Further, flexibility to extend the period by additional three months, if required.

- Automatic issuance of fresh “Project Registration Certificates” with revised timelines.

- Extension of timelines for various statutory compliances under RERA concurrently.

- An additional time of one year has been given for the commencement for commercial operations date for loans provided by NBFCs to the commercial real estate sector.

- Building and Construction Workers Welfare Fund allowed to be used to provide relief to workers.

NBFCs/ HFCs/ MFIs

Special Liquidity Scheme

- Government will launch an INR 300bn Special Liquidity Scheme (Scheme).

- Under the Scheme, investment will be made in primary and secondary market transactions in investment-grade debt papers of NBFCs/ HFCs/ Micro Finance Institutions (MFIs).

- Securities will be fully guaranteed by the Government of India.

- The Scheme is targeted at providing liquidity support and creating confidence in the market.

Partial Credit Guarantee Scheme (PCGS Scheme) 2.0

- Existing PCGS Scheme will be extended to cover borrowings such as primary issuance of bonds/ commercial papers (liability side of balance sheets) of NBFCs/ HFCs/ MFIs.

- First 20% of loss will be borne by the guarantor, i.e. Government of India.

- AA paper and below, including unrated paper, will be eligible for investment (particularly relevant for many MFIs).

- The PCGS Scheme will result in liquidity of INR 450bn.

Contractors

Extension upto six months (without costs to contractors) to be provided by all Central Agencies (such as Railways, Ministry of Road Transport and Highways, etc.) for construction/ works and goods and service contracts, completion of work, intermediate milestones, etc. and extension of concession periods.

Government agencies to partially release bank guarantees to the extent that contracts are partially completed to ease cash flow.

EPF support for business and workers

Under the Pradhan Mantri Garib Kalyan Package, payment of 12% of employees’/ employers’ contribution was supported by the Government from April-May 2020, which has been further extended to June-August 2020.

EPF contribution

The statutory provident fund contribution limit for employers and employees will be reduced from 12% to 10% for all

establishments covered by the Employees’ Provident Fund Organisation for the next three months. This is to provide liquidity of INR 67.5bn to employers and employees over the three months.

Financial support to MSMEs

Collateral free loan to MSMEs

- INR 3000bn loans for businesses including MSME;

- Borrowers with up to INR 0.25bn outstanding and INR 1bn turnover eligible;

- Loan tenure – four years, 12 months moratorium on principal repayment.

Subordinate debt for stressed MSMEs

- INR 200bn loan to be provided as subordinate debt.

- Promoters will be given loan by banks to infuse the loan amount through equity capital.

Equity infusion through fund of funds

- INR 500bn funds for expansion and encouragement to MSMEs to get listed on the stock exchange.

- MSMEs with growth potential and viability will be eligible.

Revision in the definition of MSMEs

Economic measures

The government has maintained a fine balance between fiscal prudence and the need for stimulus. The expected tax revenue losses are going to be significant, to the tune of INR 3 trillion contraction over the previous year. Budgeted proceeds of INR 2 trillion from divestments are unlikely to be realised in this fiscal, given the market conditions. States will need support to meet their deficits, with their GST revenues taking a plunge. However, it has to be seen how this protection is navigated by the GST Council. The key measures announced and their consequent implication on the fiscal for financial year (FY) 2020-2021 are as follows:

- The biggest item of INR 3 trillion collateral free loans for micro, small and medium enterprises (MSMEs) will not entail any cost to the exchequer this FY. The banks will do the lending and the only cost will be the non-performing assets on account of these loans that are being guaranteed by the government. These costs will begin occurring only in the next FY and that too only due to any loan going bad. Micro, small and medium enterprises getting this collateral free loan would not like to be willful defaulters on these as it will cause their credit records to be spoilt and good performance on servicing these loans may lead to lesser collateral requirements for such borrowers in future. The change in definition of MSMEs and also doing away with the distinction between service and manufacturing MSMEs will allow headroom to these units to further grow without the fear of losing out of the benefits available to MSMEs.

- Similarly, on the items of subordinated debt and equity infusion in MSMEs of INR 20,000 crore and INR 50,000 crore respectively, the actual fiscal outlay is of INR 14,000 crore only.

- The employee provident fund (EPF) support for additional three months will help prevent job losses and entail an outlay of INR 2,500 crore this year. The reduction in statutory PF limits does not entail any additional fiscal outlay.

- The INR 30,000 crore special liquidity scheme for non-banking financial companies/ housing finance companies/ micro-finance institutions also does not entail any additional fiscal burden during this FY and the implication can come in the year of maturity of these securities in case there is a default and invocation of the guarantee.

- Similar is the case with the Partial Credit Guarantee scheme. The INR 90,000 crore of liquidity injection in the discoms will also not entail any additional stress on the fiscal as this money will come back to the Central Government through the gencos as they will receive this from the discoms. If the receivables of the discoms go bad, it will put pressure on the State budgets as the liquidity infusion to the discoms is expected to be guaranteed by the States.

- The INR 50,000 crore liquidity injection through relief on tax deducted at source and tax collected at source is also an accounting issue and it will only impact to the extent of float with the government as these get settled in the next FY with cash basis accounting being followed by the government.

- The special credit scheme for the street vendors announced will ease the availability of credit for them. The impact of this is not only immediate but long term; it will help bring down the very high cost of credit for the vendors. It will also help create credit history for them and allow them to access formal financing, without depending on money lenders. Fintech companies could help reach these street vendors; however, it will also need to be complemented with a financial literacy programme for them to make this a transformative measure for the long run.

- The working capital needs of the farmers have also been addressed through the emergency working capital fund through NABARD, which will provide necessary cash to farmers to meet post-harvest expenses. The agenda for

- financial inclusion and formal credit availability has been furthered through the announcements related to Kisan Credit Cards (KCC). Additional concessional credit through the KCC and extension of the facility to animal husbandry and fishermen is laudable. These measures do not entail additional fiscal outlay.

- The measures of providing employment and income to the migrant labourers who are headed home will support them in the immediate term as many have lost their savings in these two months. However, the flip side of this is the delay in the return of labour, who are not expected to return to cities before November, considering the onset of the monsoons in June, sowing season, harvesting season, followed by the festive season. Industry will need to significantly incentivise labourers to return, with higher wages and better living and working conditions. Technology and automation are likely to see more adoption given these scenarios. An additional outlay of INR 45,000 crore has been announced for MGNREGA that is laudable and it will be an additional outgo from the budget.

- The announcement of the ‘one nation, one ration card’ is a great move for the migrants who lose out on the benefits because they hardly stay for a long duration in one location or their hometowns and villages. They will now be able to draw their entitlements at any location. This is a measure that will provide relief to the migrants over the long term. However, the onus of implementation is with the State Governments and it will be the speed and efficiency of the State Governments that will determine the level of distribution. One option for the States is to collaborate with the civil society organisations and informal networks that have been helping the migrant workers.

- The interest subvention of 2% for next 12 months on the Mudra Shishu loans of up to INR 50,000 is a good measure for helping self-help groups and very small entrepreneurs. The fiscal outgo will depend on the level of uptake of these loans.

Education

Recognising the importance of online and digital mode of education, certain strategic announcements were made by the FM today as part of the comprehensive economic package for the education sector. The announcements are as follows:

PM eVidya program to be launched immediately:

- DIKSHA would continue to be a one nation, one digital platform for school education.

- Efforts to increase access – SWAYAM PRABHA DTH channels to continue in locations not having internet facility; another 12 channels to be added; tie-up with private DTH players; use of radio and podcasts.

- One dedicated TV channel per class.

- Special e-content for visually and hearing impaired.Universities ranked in Top 100 will be permitted to automatically provide online courses by 30 May 2020.Manodarpan initiative to be launched for providing stress-related support to students, teachers and families.New National Curriculum and Pedagogical framework for school, early childhood and teachers will be launched; efforts to revise the National Curriculum Framework with NCERT has started; idea is to align the curriculum needs with global standards and evolving skill requirements.

Public Sector Enterprise Policy for a New, Self-reliant India

The FM emphasised on the need for more coherent policy where all sectors are open to the private sector while the public sector enterprises (PSEs) will play an important role in defined areas. Accordingly, the government will announce a new policy whereby –

- List of strategic sectors requiring presence of PSEs in public interest will be notified.

- In strategic sectors, at least one enterprise will remain in the public sector, private sector will also be allowed.

- In view of minimising the administrative costs, number of enterprises in strategic sectors will ordinarily be only one to four; others will be privatised/ merged/ brought under holding companies.

- In other sectors, PSEs will be privatised (timing to be based on feasibility etc.).

Companies Act

Some of the key proposals include –

- Direct listing of securities by Indian public companies in permissible foreign jurisdictions.

- Private companies which list non-convertible debentures on stock exchanges not to be regarded as listed companies.

- Decriminalisation of Companies Act violations involving minor technical and procedural defaults (shortcomings in Corporate Social Responsibility reporting, inadequacies in board report, filing defaults, delay in holding Annual General Meeting). The amendment will de-clog the criminal courts and National Company Law Tribunal.

- Majority of the compoundable offences sections to be shifted to internal adjudication mechanism (IAM) and powers of Regional Director for compounding enhanced to –

- Seven compoundable offences altogether dropped and five to be dealt with under alternative framework.

- Lower penalties for all defaults for small companies, one-person companies, producer companies and start-ups.

Insolvency and Bankruptcy Code

- Empowering Central Government to exclude COVID-19 related debt from the definition of “default” under IBC.

- Suspension of fresh initiation of insolvency proceedings upto one year.

- For MSMEs, a special insolvency resolution framework would be introduced under section 240A of IBC.

Healthcare

- Public expenditure on public health will be increased.

- Investment will be made to ramp up of health and wellness centre in rural and urban areas.

- Building hospital blocks for infectious diseases in all districts.

- Implementation of National Digital Health blueprint.

- Strengthening of lab network and surveillance through integrated public health labs in all districts and block level, and public health unit to manage pandemics.

- National Institutional platform for One Health by ICMR.

Companies Fresh Start Scheme, 2020 and LLP Settlement Scheme, 2020

For existing companies and limited liability partnerships (LLPs) to make good any filing related defaults, irrespective of the duration of default, and make a fresh start as a compliant entity, the Ministry of Corporate Affairs’ (MCA) has issued two circulars on 30 March 2020, one being the Companies Fresh Start Scheme, 2020 (CFSS) and the second being LLP Settlement Scheme, 2020 (LLPSS)

A. Key provisions under Companies Fresh Start Scheme, 2020

- CFSS to remain in force from 1 April 2020 until 30 September 2020.

- It applies to a company that has defaulted in filing any document, statement, return, etc., on the MCA portal.

- When filing any belated document, only the normal fee would be required to be paid and no additional fee would be levied on such filing.

- Immunity shall be provided from launch of any prosecution or proceeding for imposing penalty on delay in filing the document.

- If the company or any of its officers in default has filed an appeal against any prosecution launched or proceedings for imposing penalty, then such appeal should first be withdrawn.

- Once the delayed forms are filed and are taken on record, and after the closure of CFSS, the company shall apply for an immunity certificate under CFSS.

- CFSS shall not apply to companies against which action for final notice for striking off has already been initiated, where any application for striking off has been filed, companies which have amalgamated, where applications have already been filed for obtaining dormancy status, vanishing companies or where the action of increase in authorised capital or filing of charge related documents is involved.

- The defaulting inactive companies can file the due documents under CFSS and then apply to either obtain dormancy status or for striking off the company’s name.

B. Key provisions under the LLP Settlement Scheme, 2020

- LLPSS to remain in force from 1 April 2020 until 30 September 2020.

- This applies to an LLP that has defaulted in filing any document, statement, return, etc., on the MCA portal.

- Defaulting LLPs are permitted to file belated documents, which were due for filing until 31 August 2020.

- Defaulting LLPs that have filed their belated documents until 30 September 2020 and made good the default shall not be subjected to prosecution by the Registrar of Companies.

- LLPSS shall not apply to LLPs that have applied for striking off their names.

PwC Comments: Both these schemes present a one-time opportunity to all defaulting companies and LLPs to complete their filings and obtain immunity from all related prosecutions.

Government releases notification for incentive schemes for electronic products/ components – PLI and SPECS

The Ministry of Electronics and Information Technology (MeitY) has notified the following two

schemes on 1 April 2020:

PLI scheme – Notification no. CG-DL-E-01042020-218990 dated 1 April 2020 and SPECS scheme – Notification no. CG-DLE-01042020-218992 dated 1 April 2020

- Production Linked Incentive Scheme (PLI), which provides incentives to companies registered in India, subject to eligibility thresholds, target segments, etc., in order to boost large-scale electronic manufacturing.

- Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS), which aims to address the disabilities faced by manufacturers of components and semiconductors by offering capital subsidy of 25%.

A. PLI Scheme

The PLI scheme will provide an incentive of 4% to 6% on incremental sales to any company registered in India and manufacturing goods covered under target segments. The total budgetary outlay of the proposed scheme is approximately INR 40,951 crore. The below table summarises the main aspects of the guidelines:

B. SPECS Scheme

PwC comments: The PLI scheme aims to boost domestic manufacturing while also attracting large investments in mobile phone manufacturing and specified electronic components, including ATMP units. Since the application window is four months from 1 April 2020, it will be beneficial for applicants to apply under the PLI scheme at the earliest. Further, detailed guidelines would shed light on eligible heads of investment to determine eligibility under the PLI scheme.

The SPECS scheme is expected to create an indigenous manufacturing eco-system for electronic components and semiconductors in the country. The appraisal and disbursement guidelines will be elaborated in this scheme guidelines to be issued by MeitY separately. Applicants may start evaluating the benefits available that would ultimately reduce the cost of investment of proposed set up.

Direct Tax

The Supreme Court upholds constitutional validity of clause (f) of section 43B of the Income-tax Act, 1961, relating to disallowance for sums payable in lieu of leave

Recently, the Supreme Court upheld the constitutional validity of section 43B(f) of the Income-tax Act, 1961 (the Act) overruling the judgement of the Calcutta High Court.

Constitutional validity of clause (f) of section 43B of the Act

- Based on the two-fold and prudent approach laid down in the case of Rakesh Kohli & Anr and various other decisions, the legislature has the power to enact clause (f) in section 43B of the Act. The enactment of clause (f) does not violate any right provided in Part III of the Constitution of India.

- Section 43B of the Act does not restrict the taxpayer to adopt a particular method of accounting nor deprives it of any lawful deduction. It merely operates as an additional condition for availing the deduction qua the specified head.

- Clause (f) was inserted to curb the mischief of claiming the deduction of liability of leave encashment, i.e., advance deduction from tax liability, and refusal to pay when the event occurs, which is in line with the purpose of introducing other clauses under section 43B of the Act.

Non-disclosure of objects and reasons

- The non-disclosure of objects and reasons has no impact upon the constitutional validity of a provision unless the provision is ambiguous. While examining the validity of a provision, the primary concern is to interpret the literal text of the provision for its true meaning and purpose.

- The Calcutta High Court’s approach on striking down the constitutional validity was flawed on the following three counts –- it made no attempt to discover any constitutional infirmity in the provision;

– it did not dissect the text of the provision to demonstrate the need to go beyond the text; and

– it went into the background of the enactment, which was not required unless the provision is ambiguous.

Inconsistency of clause (f) and absence of nexus with section 43B of the Act

- Based on a reading of the Memorandum of Finance Bill, 1983 (which introduced section 43B), and the amendments to the provisions of section 43B of the Act over the years, the legislature never restricted the provision only to deduction of statutory liabilities. It had taken within its fold diverse nature of deductions, ranging from tax, duty to bonus, commission, interest on loans and general provisions for welfare of employees, and there was no uniformity in the nature of deductions that were included within the ambit of this section.

- The introduction of clause (f) of section 43B of the Act fits within the broad objective of enacting the section to protect the larger public interest, primarily of revenue, and including the welfare of employees.

Defeating the dictum in the case of Bharat Earth Movers

- While the legislature cannot overrule or invalidate a judgment of this Court, it can amend or enact a valid law on a topic within its legislative field.

- Clause (f) of section 43B of the Act neither reverses the nature of the leave encashment liability (i.e. present liability) nor has it taken away the deduction. It merely defers the benefit of deduction to be availed by the taxpayer, by linking it to the actual payment of the concerned employee. The clause was introduced with prospective effect and with the intent to regulate the deduction of leave encashment liability to curb mischief.

PwC comments: The Supreme Court’s decision affirms the legitimacy and purpose of enacting clause (f) of section 43B of the Act and upholds its constitutional validity. This decision should put to rest the ongoing litigation on this issue.

Indirect Tax

Delhi High Court reads down circular dated December 2017 to the extent that it restricts rectification of Form GSTR-3B with respect to period in which error occurred

Recently, through a writ petition, the petitioner has challenged Rule 61(5) of the Central GST Rules, 2017 (CGST Rules) (Form GSTR-3B) and a circular (relevant circular) as ultra vires the provisions of the Central GST Act, 2017 (CGST Act), to the extent they do not provide for the modification of the information to be filled in the return of the tax period to which such information relates. This circular prevented the petitioner from correcting the monthly GST returns in Form GSTR-3B for the period July to September 2017 (relevant period), to claim additional credits, rectify errors, and consequently, seeking refund of excess taxes paid. The High Court held that the rectification of the return for that very month to which it relates is imperative, and accordingly, read down para 4 of the relevant circular, to the extent that it restricts the rectification of Form GSTR-3B with respect to the period in which the error had occurred

PwC comments: This is a welcome decision and provides relief to taxpayers who could not rectify the returns already filed due to inadvertent errors and had omitted to claim ITC or paid excess tax. The High Court has examined the entire gamut of issues faced by the taxpayers in the initial months of the GST regime and the non-implementation of the system-based matching of credits, which has also resulted omissions in claiming ITC in the respective months. The High Court has not commented on whether Form GSTR-3B is a return in addition to or in place of Form GSTR-3, although this is referred in the submissions made by petitioners. While the High Court has read down the relevant circular2 restricting the rectification of returns in the relevant period, it remains to be seen how this decision would be practically implemented. A deeper analysis is necessary on the applicability of the decision to specific facts and situations, the period for which the decision would apply and the situations in which the rectification would be permitted.

Delhi High Court holds that time limit for filing FORM GST TRAN-1 for transitioning the credit is directory and cannot take away vested right of credit accrued as on 1 July 2017; permits taxpayers to claim transition credit until 30 June 2020

Facts

The petitioners have filed writ petitions before the Delhi High Court seeking to avail input tax credit (ITC) of the accumulated Central value added tax (CENVAT) credit as on 30 June 2017 (transitional credit), by filing FORM GST TRAN-1 beyond the time period provided under the Central GST Rules, 2017 (CGST Rules).

The main grievance of the petitioners was that on account of technical difficulties faced by them (e.g. dependence at group level for tax compliances and involvement of multiple entities, carry forward of credits being inadvertently missed, etc. As a result, they were unable to avail the transitional credits within the time period prescribed under Rule 117 of the CGST Rules. Therefore, the petitioners contended that they must be permitted to avail transitional credit in accordance with various judicial precedents.

The petitioners challenged Rule 117 of the CGST Rules as being arbitrary, unconstitutional and violative of Article 14 of the Constitution of India, to the extent it imposes a time limit to carry forward the CENVAT Credit to the GST regime.

High Court’s decision

The Delhi High Court permitted the petitioners to file Form GST TRAN-1, as the cause for not filing the Form within time was sufficiently explained and justified that the Petitioners’ case was squarely covered by earlier decisions pronounced by the Courts.

Time period prescribed for filing Form GSTR TRAN-1 is not sacrosanct

The Delhi High Court held that the time period under Rule 117 of the CGST Rules is not sacrosanct or mandatory, after observing the following:

- 90 days period mentioned in the CGST Rules has no rationale;

- The Government has granted extensions from time-to-time, which substantiates that the time period prescribed under the CGST Rules is not considered as sacrosanct or mandatory by the legislature;

- No mechanism was provided for the refund of credit that existed on the appointed date and the only mechanism was for the utilisation of such credit by migrating it to the GST regime; and

- In the absence of any consequence in section 140 of the Central GST Act, 2017 (CGST Act) for delayed filing of Form GST TRAN-1, Rule 117 of the CGST Rules has to be read and understood as directory and not mandatory.

The High Court referred to the Supreme Court’s decision in the case of ALD Automotive (which was also relied on by the Department), wherein it was observed that “whether particular provision is mandatory or directory has to be determined on the basis of object of particular provision and design of the statute” and “such interpretation should not be put which may promote the public mischief and cause public inconvenience and defeat the main object of the statute.” As the purport of the transitory provisions is to allow smooth migration from the erstwhile regime to the new GST regime, the High Court held that the interpretation must be in consonance with the said purpose.

Thus, Rule 117 of the CGST Rules was read down as being directory in nature and was held as unconstitutional, arbitrary and violative of Article 14 of the Constitution of India to the extent it imposes a time limit to carry forward the CENVAT credit.

“Technical difficulties” cannot be restricted to technical glitches in GSTN portal”

The High Court held that the classification introduced by sub Rule (1A) of the CGST Rules, restricting the benefit only to taxpayers whose cases are covered by “technical difficulties on common portal” is arbitrary, vague and unreasonable, after observing the following:

- The Government cannot adopt different yardsticks while evaluating the conduct of taxpayers, and its own conduct, acts and omissions. The “technical difficulties” cannot be restricted only to a difficulty faced by or on the part of the Government and would include technical difficulties faced also by the taxpayers.

- Extremely narrow interpretation of the concept of “technical difficulties” to cover only the “technical glitches” faced in the GSTN portal is contrary to the statutory mechanism built in the transitory provisions of the CGST Act.

CENVAT credit balances as per “erstwhile returns” is taxpayers’ property

The High Court held that the CENVAT credit, which stood accrued and vested, is the property of the taxpayer, and is a

constitutional right under Article 300A of the Constitution of India, which cannot be taken away merely through delegated legislation by framing rules, without there being any overarching provision in the CGST Act.

The Court observed that the case of ALD Automotive (in context of the Tamil Nadu VAT law) is not applicable since ITC was not taken and the statute did not give any indication with respect to the extension of time for claiming ITC. However, in the instant case, the ITC had been claimed in the erstwhile regime and was reflected in the CENVAT credit ledger. Thus, the High Court held that this credit, being the property of the petitioner that stood accrued, needs to be carried forward under section 140(1) of the CGST Act.

Limitation Act, 1963 to apply to time limit for filing Form GST TRAN-1

The High Court observed that the CGST Act does not restrict the transition of CENVAT credit in the GST regime by a particular date, and that there is no rationale for curtailing the said period, except under the law of limitation.

In the absence of any specific provision under the GST law, Court it was held that the transitional credit could be availed within a period of three years from the appointed date in accordance with the residuary provisions of the Limitation Act, 1963, i.e., on or before 30 June 2020.

Form GST TRAN-1 can be filed before 30 June 2020 by similarly placed taxpayers

To conclude, the High Court held that in cases where petitioners have filed or attempted to file Form GST TRAN-1 on or before 30 June 2020, they are entitled to avail the ITC accruing to them. The respondents have been directed to open the online portal to enable filing of Form GST TRAN-1 electronically or accept the same manually. Further, other taxpayers in similar situations should also be entitled to this benefit.

PwC comments: This judgement analyses the background of the amendments, considered the object of smooth transitioning of credits and recognised the divergent views adopted for interpreting the term “technical difficulty.” The High Court has reiterated that the right to avail the transition credit (as reflected in the CENVAT Register on the appointed date) cannot be fettered by a limitation in a Rule. Interestingly, the High Court has applied residuary provisions of the Limitation Act, 1963, to allow transition of credits and has made this specifically applicable to other taxpayers who are similarly situated, thereby, seeking to reduce litigation. However, it remains to be seen if the department would further appeal this decision, the practical implementation of this decision and the situations in which the decision would be applied.

Trivia

Trivia

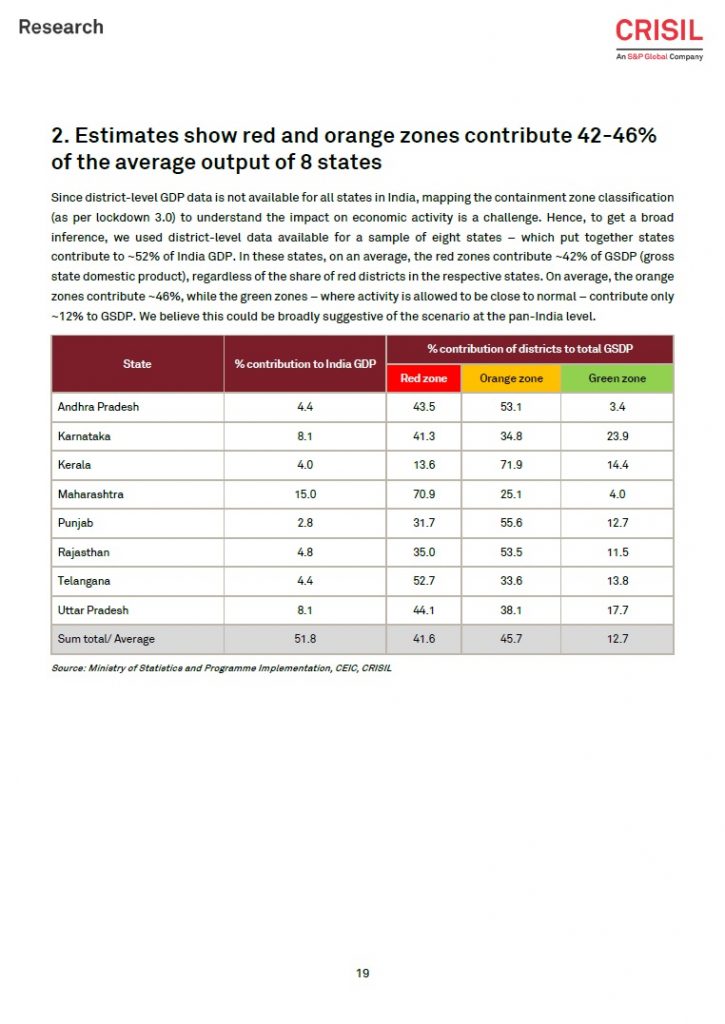

CRISIL's Research Report on India's GDP Growth

From the Research Wing......

- The Chamber is preparing a representation to the Expert Committee constituted by Government of Kerala that will study the impact of Covid-l9 and the consequent lockdown measures on the public finances of the State and the various sectors of its economy.

POLICY DEVELOPMENTS CORNER

1) On 12th May, Prime Minister Narendra Modi, announced the Aatmanirbhar Bharat Special Economic Package of Rs 20 lakh crores. Presentations made by the Finance Minister are listed below ( Credits -PRS India)

- Presentation made by Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman on 13th May. https://static.pib.gov.in/WriteReadData/userfiles/Aatmanirbhar%20Presentation%20Part-1%20Business%20including%20MSMEs%2013-5-2020.pdf.

- Presentation of details of Tranche 2 by Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman on 14th May. https://static.pib.gov.in/WriteReadData/userfiles/Aatma%20Nirbhar%20Bharat%20presentation%20Part-2%2014-5-2020.pdf.

- Presentation of details of 3rd Tranche by Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman on 15th May. https://static.pib.gov.in/WriteReadData/userfiles/Aatma%20Nirbhar%20Bharat%20Presentation%20Part-3%20Agriculture%2015-5-2020%20revised.pdf.

- Presentation of details of 4th Tranche announced by Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman on 16th May. https://static.pib.gov.in/WriteReadData/userfiles/AatmaNirbhar%20Bharat%20Full%20Presentation%20Part%204%2016-5-2020.pdf.

- Presentation of details of 5th Tranche announced by Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman on 17th May. https://static.pib.gov.in/WriteReadData/userfiles/Aatma%20Nirbhar%20Bharat%20%20Presentation%20Part%205%2017-5-2020.pdf.

2) Central Board of Indirect Taxes and Customs (CBIC) has invited comments on the draft circular on Electronic sealing-Deposit of and removal of goods from a customs bonded warehouse. Deadline: 12th June. Contact id: [email protected] or [email protected]

3) Competition Commission of India has invited comments on Amendments to the Combination Regulations . Deadline: 15th June (Notice date-16th May). Contact id: [email protected]

4) The Insolvency and Bankruptcy Board of India has invited comments on the Regulations notified under the Insolvency and Bankruptcy Code, 2016. Deadline: 31st December. Submission Link: https://lnkd.in/gtQd3Ek

Forthcoming Events

CEO FORUM 2020

Virtual Meeting - "Beyond the Pandemic, How to move ahead" | 05.06.2020

The next CEO FORUM Virtual Meeting is scheduled for Friday, 5th June, 2020 between 8.30 a.m and 9:30 a.m.

We have Dr. Sujit Vasudevan, Renowned Consultant Physician with over 35 years of experience in private Medical Practice addressing us on “How to move ahead, beyond the Pandemic.”

Please note that, in order to join the meeting, you will need to have the Zoom Meeting app installed on your device.

We kindly request you to join the meeting at 8:30 a.m. sharp using the link below.

https://us04web.zoom.us/j/3310023664?pwd=ejhzSld5cGllRXpsbUowZkNVMFVOUT09#success

Meeting ID: 331 002 3664

Password: 8Fpa9Z

Online Facilitative Workshop on Managing Virtual Teams Effectively

Virtual Meeting - 10.06.2020 | 03.00 p.m - 05.00 p.m | Zoom app

The Chamber is organising an Online Facilitative Workshop on Managing Virtual Teams Effectively, on Wednesday, 10th June, 2020 from 3-5 pm on the Zoom Platform.

The ongoing COVID-19 pandemic has affected every businesses. Enterprises are now looking for ways to revive themselves, stay relevant and evolve strategies to recast their future given the different post-COVID world order. A peek into the future indicates the following as possible trends:

(a) Shopping, work, learning & play/ entertainment will all shift predominantly online

(b) Supply chains will be local rather than global

(c) Digitalisation will be the new normal. Those not connected will be left out.

(d) Investors will have a bias towards investing closer to home to avoid uncertainty

(e) Healthcare availability may become more democratic, and infrastructure will get impetus

The programme will be conducted by Transformavens Training & Consulting LLP, Mumbai and would use a mix of imparting inputs, as well as collecting and disseminating group wisdom through facilitation, to equip mid-level leaders to effectively handle teams using the virtual domain. The duration would approximately be about 120 minutes.

For registrations,

cochinchamber.org

9895676827/9744629992/6238383922

E-Certificate of Origin

Advertisement

Exclusive EXIM Statistics

Statistical Reports on Exports and Imports through the Cochin Port.

The Cochin Chamber of Commerce and Industry publishes statistical reports on Exports and Imports through the Cochin Port on a monthly basis followed by a Consolidated Annual Report at the end of each calendar year. The reports on exports are classified as commodity wise and pertain to the following commodities:

- Coffee

- Tea

- Spices

- Cashews

- Cotton Goods

- Seafood and

- Coir and coir products

Details on all other commodities that do not fall under the above-mentioned heads are carried as the ‘Miscellaneous Report’. Customized reports will also be available according to customers requirement.

We have several members in the export/import fraternity subscribing to these reports on a monthly basis and from the feedback received they are immensely benefited by the same.

We are confident that our reports will be of help to your Company in staying one step ahead of your competitors in business. A sample of the report is attached herewith for your reference. Also attached is the ‘Subscription Form’ to enable you to subscribe to the report should you want to do so.

Should you have any queries please feel free to contact Ms. Archana (7025738447).

For more details, visit Export-Import Statistics

Sample Reports