President's Note

Dear Friends,

The outcome of the general elections of 2019 is historic in more ways than one. On behalf of the Cochin Chamber, I congratulate the new Government on their huge win. I hope that the coming days will be good for business, and India will fare even better than before.

For the Chamber it’s been a remarkable month!

As always we started off the month with our CEO Forum Breakfast Meeting. The Guest Speaker at the meeting was Mr. Madhu Damodaran, Business Head, CoAchieve Solutions Pvt. Ltd., Bangalore who spoke on the topic “Digitization of Labour Law Compliance – A Paradigm Shift.” In his talk, Mr. Damodaran spoke about the introduction of UAN in 2014, online generation of the temporary insurance card, online submission of the half-yearly returns and online registration of the ESIC. He explained in detail about the One-Stop-Shop for Labour Law Compliance, simplification of Registers and Forms, and simplification, amalgamation & rationalization of Central Labour Laws etc. Mr. Damodaran also highlighted the challenges in digitization of labour laws like evidence management, fast-changing laws, & checklists and the volume of data to be managed.

The next CEO Breakfast Meeting will be held on the 7th of June 2019. The session will be on the topic “Private Equity – How to get your Businesses Ready” and will be handled by Mr. Vineet Satija, Director, Corporate Finance, Lead, Retail and Consumer – PwC India.

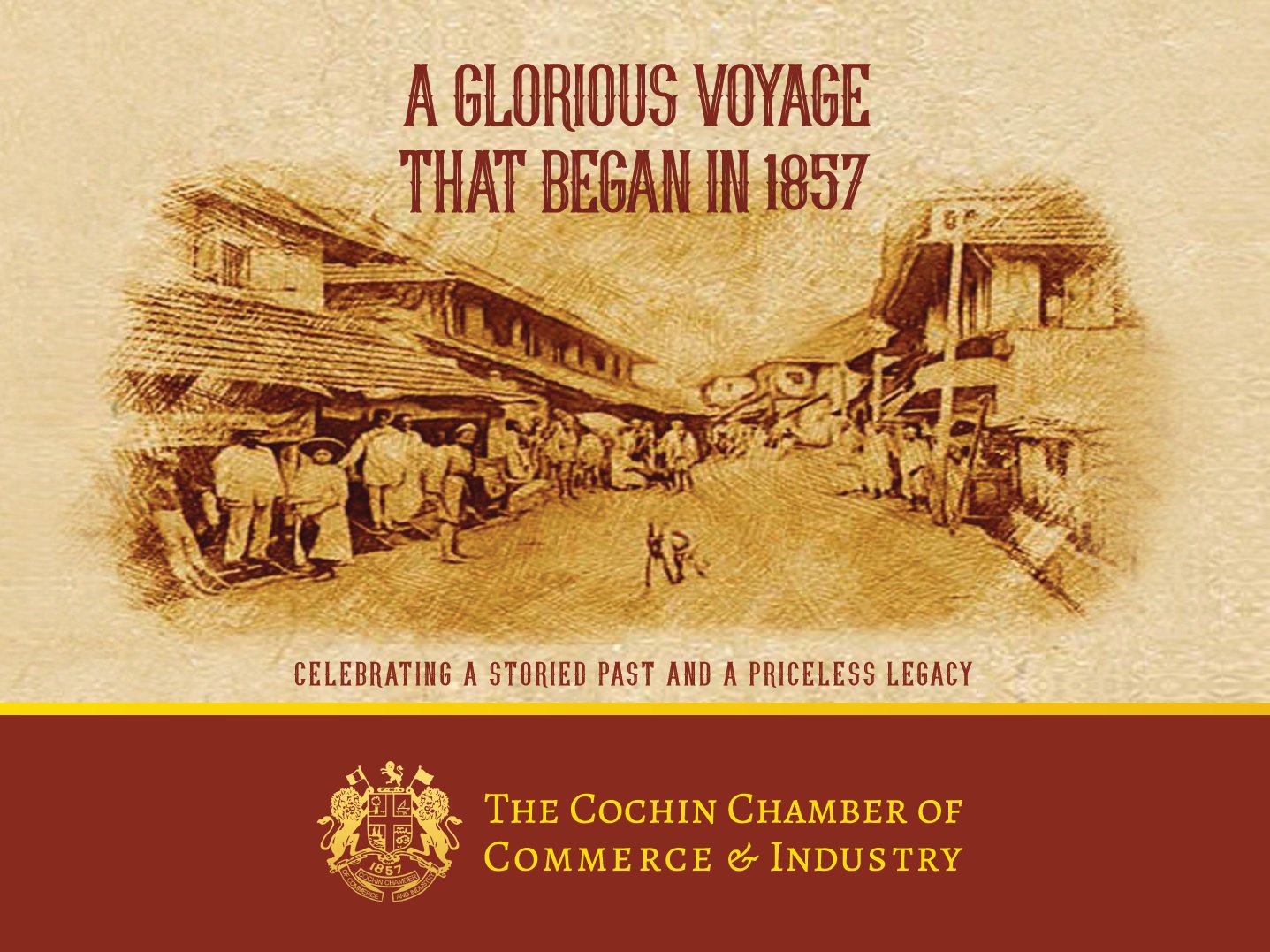

“A storied past and a priceless legacy”, is what defines the Cochin Chamber. To celebrate this, we conducted the 162nd Chamber Day on the 17th of May. The Chief Guest on this occasion was Mr. Ashutosh Khajuria, Executive Director & CFO, Federal Bank, Mumbai. Mr. Marcel R Parker, Chief Mentor, Quess Corp Limited, Mumbai was the Guest of Honour. On this occasion, we took the opportunity to honour the Past Presidents of the Chamber and also the former Secretary Mr. P Sethuram for their invaluable contributions to the Organisation.

On this occasion, we released the Chamber Souvenir “A Glorious Voyage that began in 1857” which showcases the Chamber’s storied past and its priceless legacy. I would like to thank everyone who contributed to the success of the Souvenir.

I thank everyone who joined us in this celebration and making it a huge success.

Detailed reports on this event along with pictures are carried in this Newsletter.

I am sure you all will know that the last date of filing of GST Annual Returns is the 30th of June 2019. The Chamber has decided to organize a half-day session on the 12th of June, “Refresher on Annual Returns/ Audit Report and Other Updates” for the benefit of trade and industry. The session will be handled by Ms. Nisha Menon, Director – Tax, PwC India. The details of the same will be sent to you shortly.

The Chamber has always wanted to have a “Research Wing.” This dreams has finally taken shape and we are happy to announce that the Research Wing of the Chamber will be up and running shortly. We hope to come out with exclusive research papers on various socio-economic topics, shortly.

The Cochin Chamber has always taken initiatives for the betterment of the trade and industry and we continue to do the same. As always, I know that I can count on your support and cooperation in all our activities.

I wish you all, the very best and assure you of the Chamber’s best services at all times.

Regards

V Venugopal

Fine Points

The Cochin Chamber Souvenir depicting its 162 year Legacy

The Souvenir can be had from the Cochin Chamber office from mid-June 2019.

Recent Events

CEO FORUM Breakfast Meetings 2019 - "Digitisation of Labour Law Compliance - A Paradigm Shift"

03.05.2019 | Taj Gateway Hotel, Ernakulam

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s – 5th Breakfast Meeting on Friday, 3rd May 2019 at Taj Gateway Hotel, Ernakulam. The Guest Speaker at the meeting was Mr. Madhu Damodaran, Business Head, CoAchieve Solutions Pvt. Ltd., Bangalore.

Calling the meeting to order, Mr. V Venugopal, President of the Chamber delivered the Welcome Address and introduced the Speaker of the day.

Mr. Damodaran’s talk was on the “Digitization of Labour Law Compliance – A Paradigm Shift.”

In his talk, Mr. Damodaran spoke about the introduction of UAN in 2014, online generation of the temporary insurance card, online submission of the half-yearly returns and online registration of the ESIC.

Mr. Damodaran said that Professional Tax remittances are online in almost all the States and CLRA registration and licensing is online in Gujarat, Maharashtra, Jharkhand, Chattisgarh, and Karnataka. There is also a Central Licensing Platform to get all the registrations under Central CLRA rules, he added.

He explained in detail the One-Stop-Shop for Labour Law Compliance, Simplification of registers and forms, Simplification, amalgamation and rationalization of Central Labour Laws etc.

Mr. Damodaran also highlighted the challenges in digitization of labour laws like evidence management, fast-changing laws and checklists and the volume of data to be managed. With changes being made in the registration and filing procedures, the need for systematic management is of prime importance, he said.

He also explained the pitfalls in the Current Compliance Delivery and the parameters companies are looking forward to improve, namely Security and Process Control, Process Improvement, Document Management, Data Analytics, and Modelling, etc.

Mr. C S Kartha, Past President of the Chamber presented a Memento to Mr. Damodaran.

Mr. S P Kamath, Executive Committee Member of the Chamber proposed the Vote of Thanks.

The interactive session concluded by 10 a.m with breakfast.

162nd Chamber Day Celebrations

17.05.2019 | Hotel Monsoon Empress, Ernakulam

The Cochin Chamber of Commerce and Industry celebrated its 162nd Chamber Day on Friday the 17th of May, 2019 at Hotel Monsoon Empress, Ernakulam.

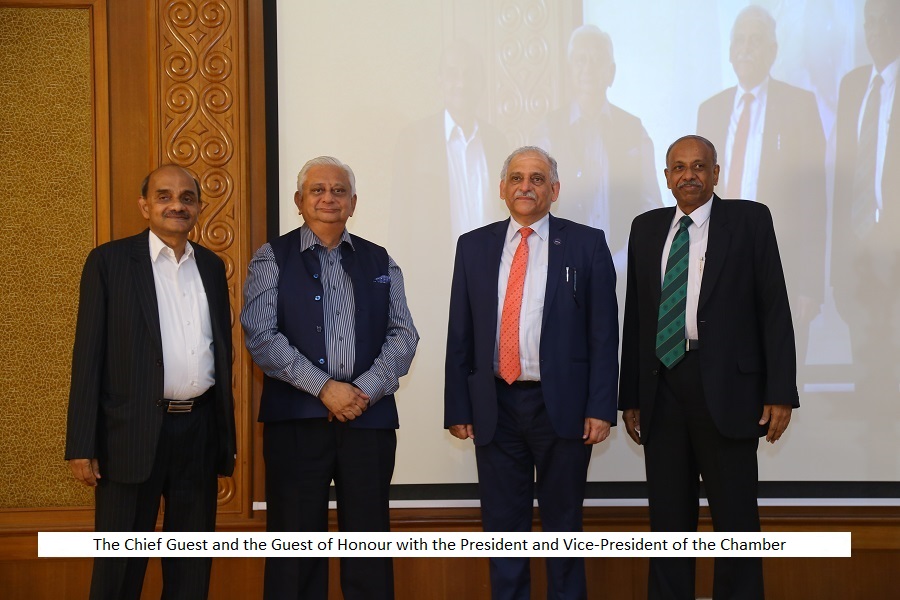

The Chief Guest on this occasion was Mr. Ashutosh Khajuria, Executive Director & CFO, Federal Bank, Mumbai. Mr. Marcel R Parker, Chief Mentor, Quess Corp Limited, Mumbai was the Guest of Honour.

Mr. V Venugopal, President of the Chamber delivered the Welcome Address.

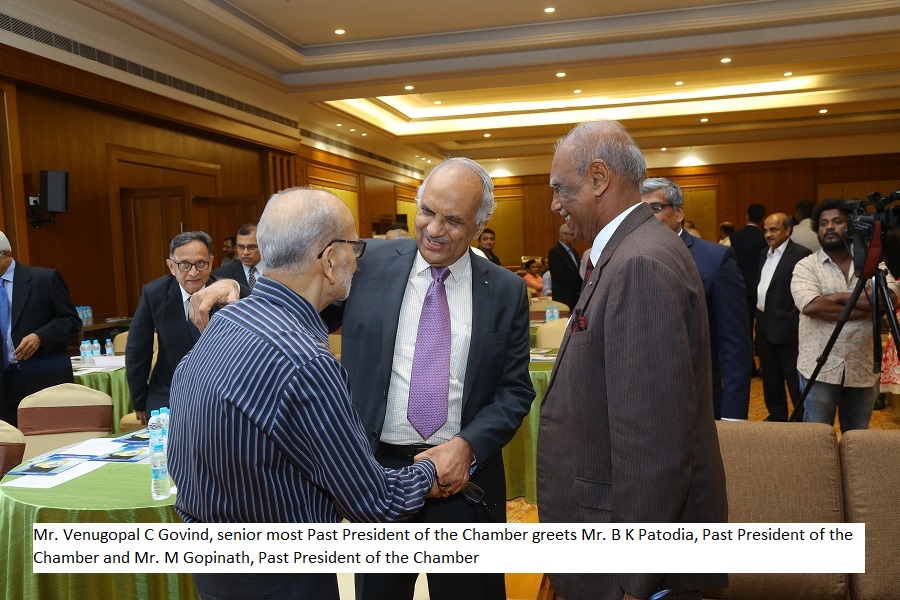

The Welcome Address was followed by the inauguration of the 162nd Chamber Day function with the lighting of the lamp by the Chief Guests. Mr. V Venugopal, President of the Chamber, Mr. Venugopal C Govind, Senior most Past President of the Chamber and Mr. C S Kartha, Programme Committee Chairman were present on the dais during the lighting of the lamp.

Followed by the lighting of the lamp, Mr. Venugopal C Govind, spoke about the history of the Chamber in retrospect. He spoke about the tremendous efforts that the Chamber took in the past establishing the first Municipal Council of Fort Kochi, introducing telegraph facilities, building the Shornur – Ernakulam railway line, inception of protected water supply and a drainage system, setting up of the Cochin Harbour etc.

Mr. Ashutosh Khajuria, Chief Guest for the evening, spoke on the Indian economy in comparison with the other economies of the world. Mr. Khajuria explained the “Impossible Trinity” which is faced mainly by the exporters and importers for whom the external value of domestic currency is very important. He mentioned how the Government and the Central Bank could help emerging economies in managing the exchange risks. He also pointed out the positives in the Indian Economy namely high forex reserve, 3.4% fiscal deficit, high growth rate etc.

Mr. Marcel R Parker addressed the guests on how important it is to nurture the next generation and the way to go forward for every organization from what they have achieved so far. Mr. Parker mentioned the gig economy and its low penetration rate in Kerala owing to lesser employment opportunities for the youth. He added that the younger workforce prefers open working environments than a restricted one and also expected higher returns. The practice of investing in higher wages irrespective of the results needs to be changed, he added. Mr. Parker said that India has been unable to create the requisite jobs in the country thereby resulting in the migration of young people to other countries. He also suggested that the Chamber should take initiative in creating more opportunities for the youth and in enhancing their skills.

Mr. K Harikumar, Vice President of the Chamber, proposed the Vote of Thanks.

The evening concluded with a networking dinner.

Honouring the Past Presidents of the Chamber & the former Secretary

Mementos being presented to the Chamber’s Past Presidents

The Past Presidents of the Chamber were honoured at the event with a Ponnada and a Memento.

The former Secretary of the Chamber, Mr. P Sethuram was also honoured on this occasion.

1) Venugopal C Govind 2) B K Patodia 3) M Gopinath 4) M Jairam 5) A S Narayanamoorthy 6) V R Nair 7) N R Pai 8) A K Nair 9) N Sreekumar 10) Jose Dominic 11) Anand Menon 12) P Narayan 13) C P Mammen 14) C S Kartha 15) Shaji Varghese

16) Memento being presented to the former Secretary of the Chamber Mr. P Sethuram

Release of the Souvenir commemorating the 162 Year Legacy of the Chamber

Article

Proven and Tested Tool for Retention – Engaging Our Employees

LAKSHMI J. AJIT

Director HR, Eliptico IT Solutions Pvt. Ltd. (iSpace, Inc., Enterprise)

“Change is the law of life and those who look only to the past or present are certain to miss the future.” —John F. Kennedy

What makes one Organisation more successful than the other? Is it the products, services, tools, money power or any other factor?

Certainly, all these contribute to the growth of the organisation. But there is one long term strength whose contribution results in the most competitive advantage of one organisation against the other- We call it the Workforce.

In this fight of competitive advantage with workforce the differentiator will be engaged employees.

Employee engagement first appeared as a concept in management theory in the 1990s, becoming widespread by the Gallup Organization’s yearly global surveys. Employee engagement can seem like a state that is indescribable yet is desired. It is an emotional attachment the employee feels towards the place, work, position, culture and so on which impacts the well being and productivity of the organisation.

Companies and leaders worldwide recognize the advantages of engaging employees. However, they are hesitant to devote the time and money resources it takes to ensure the desired results – increased employee engagement.

What the companies need to realise is that when employees are fully engaged their operating costs keeps improving over the 12 months whereas employees who are not engaged end up taking more sick leaves eventually resulting in higher operating costs.

Let’s introspect little more and see what Business means and what needs helps business to attain more (both in terms of capacity utilisation as we well as general wellbeing)

“Business is more about emotions than most businesspeople care to admit.” ~ Daniel Kahneman, Ph.D., Nobel Prize Laureate and Behavioural Economist.

This is where the Maslow’s hierarchy of needs become relevant. As per this need hierarchy human beings needs in general can be characterised into two:

- Extrinsic factors

- Intrinsic factors.

Examples of Extrinsic factors are tangible results like pay rise, bonuses etc while intrinsic factors are physiological rewards employees get by meaningful work.

In short now there is a new feel to this theory which we now call it as HIERARCHY OF EMPLOYEE NEEDS.

It is clearly depicted in the diagram below:

Employee engagement is defined in many ways including, “we know it when we see it.”

Employees are engaged as mentioned in the hierarchy above when many different levels of employees are feeling fully involved and enthusiastic about their jobs and the various levels of Extrinsic and Intrinsic factors are met. More and more studies have predicted that more the care taken towards Intrinsic motivators like relationship, recognition and personal growth the more the engaged/ productive employees the organisation will develop.

Obviously, the next question is how we do it without too much investment.

Over the years, The Right Group has amassed a customisable databank of tested measures of employee engagement and the organisational elements that drive organisations to develop fully engaged employees.

These can be called as “Satisfaction Factors” which can act as lever in creating a culture of satisfied and productive work force.

The diagram depicts in simple manner various factors which both affect the sentiment and culture of an organisation which aids in creating fully engaged employee population.

In short investing one’s time in engagement activities promotes the general wellbeing and satisfaction which ultimately affects your bottom line.

Employers always feel that employees leave the organisation only for pay, of course it does happen but just a very minor percentage of employees do that. Remaining percentage in fact the most crucial performers quit when they feel their work is not contributing to the organisational growth and personal happiness.

Finally: –

“What you believe about employees comes out in how you treat them. And how you treat them ultimately determines how effectively you engage them “ …… Scott Carbonara

LAKSHMI J. AJIT

Director HR, Eliptico IT Solutions Pvt. Ltd. (iSpace, Inc., Enterprise)

Profile of Lakshmi J. Ajit

Lakshmi Ajit is a HR Professional with over 18 years of experience. She has held various corporate positions in different organisations like IBM, OpenText and ZenQ before Eliptico. Presently, she is settled in Hyderabad for the past 14 years.

She is a Strategic Thinker with a passion for creating and implementing new initiatives and ideas in the field of HR. During her tenure, she has performed diverse assignments covering a broad area of HR functions such as – employee relations, staffing, performance management, compensation management, affirmative action, organization development, and training. She also has the reputation of being a highly innovative and result oriented professional with good interpersonal skills and a flair for building team cohesiveness.

Lakshmi has conducted sessions at various Schools, Universities and for experienced professionals. She loves imbibing and imparting knowledge.

Lakshmi completed her schooling in Kochi and graduated in Business Administration from the Kerala University. She went on to do her Post-Graduation in Management from Rajagiri College of Social Sciences and was the Gold Medallist from the University for the year 2001. She is also a Certified Neurolinguistic Professional (NLP).

The Cochin Chamber's Research Wing

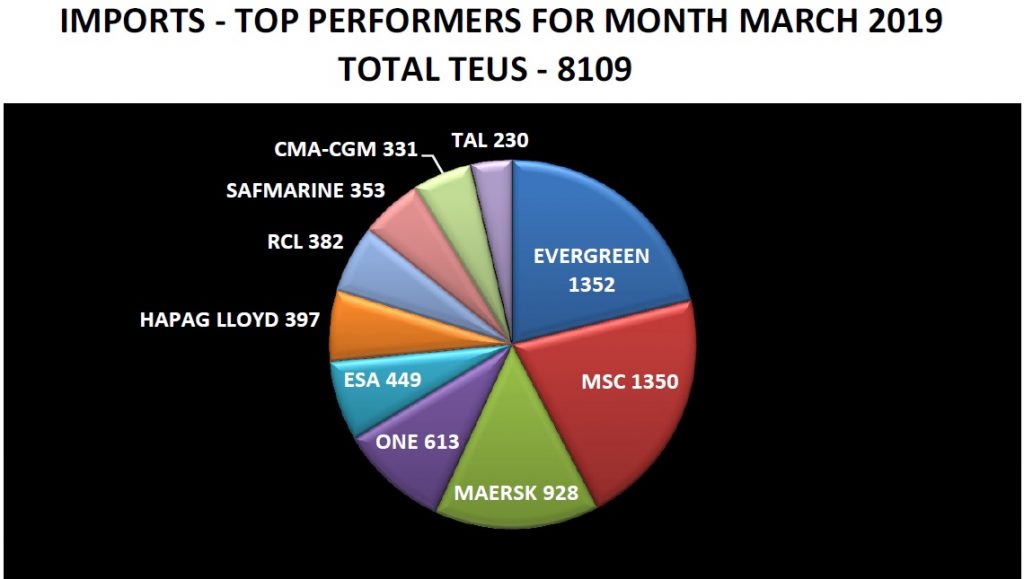

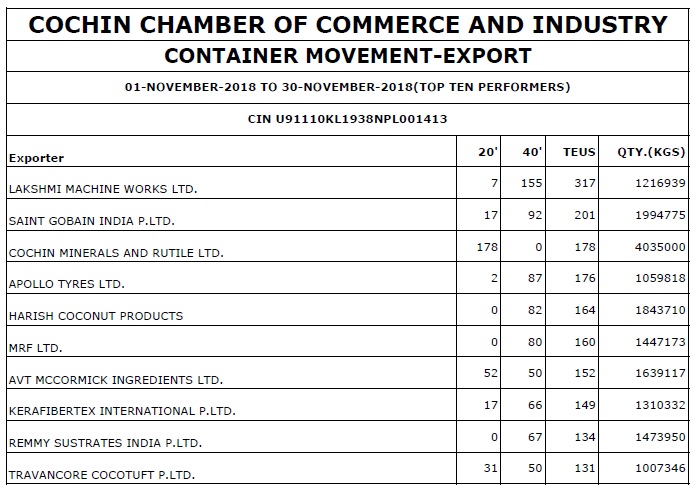

Exclusive EXIM Statistics

{kind=link}

{kind=link}

- Covers for pictorial representation only

- Coffee

- Tea

- Spices

- Cashews

- Cotton Goods

- Seafood and

- Coir and coir products

Details on all other commodities that do not fall under the above mentioned heads are carried as the ‘Miscellaneous Report’. Customized reports will also be available according to customers requirement.

Our newest Member

Ozak Technologies Pvt. Ltd.,

Kottayam

Business Activity

Manufacturer of Electronic Components & Products

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

SC dismisses Revenue’s SLP relating to disallowance of expenses under section 14A in the absence of any exempt income

Recently, the Supreme Court (SC) has dismissed the Revenue’s Special Leave Petition (SLP) against the decision of the Delhi High Court (HC) holding that no question of law arose from the order of the Income-tax Appellate Tribunal (Tribunal), thereby deleting the disallowance under section 14A of the Income-tax Act, 1961 (Act), absent any exempt income during the year.

The Delhi HC, relying on its previous decision, had dismissed the appeal filed by the Revenue against the Tribunal’s ruling holding that, in the absence of any exempt income, disallowance under section 14A of the Act was not warranted.

Aggrieved by the HC’s decision, Revenue filed the SLP before the SC, which was dismissed by the SC.

PwC comments: This is another instancewhere the SC has dismissed the SLP filed by the Revenue for disallowing expense under section 14A of the Act in the absence of exempt income and can be considered as a useful reference by taxpayers in similar case.

Rental income from letting out of shops in the mall taxable as business income

Recently, the Kerala High Court (HC) upheld the order of the Cochin bench of the Income-tax Appellate Tribunal (Tribunal) that income derived from letting out of shop rooms in a shopping mall constructed by the taxpayer has to be treated as business income, and assessed to tax under the head “profits and gains of business”. The Tribunal observed that the primary intention of the taxpayer was commercial exploitation of property, from which it had derived substantial part of its income by way of complex set of activities. Further, since, such activities constituted its main business objective, the income so derived should be taxed as business income.

PwC comments: The decision affirms the dictum laid down by various courts that where the main intention of the taxpayer is for letting out of immovable property, rental income should be considered as income from house property. However, where the main intention is to exploit the immovable property by way of complex commercial activities, rental income should be considered as business income. This decision of the HC is likely to provide more clarity on the vexed issue of characterization of rental income to other taxpayers facing similar issues.

Income-tax return forms for FY 2018-19 notified

The Central Board of Direct Taxes (CBDT) has amended the income-tax rules and introduced new Income-tax return forms (ITR forms) applicable for the financial year (FY) 2018-19 (assessment year 2019-20). Similar to last year, a simplified one page ITR Form-1 (Sahaj) [ITR1] has been notified for Resident and Ordinarily Resident (ROR) taxpayers whose total income does not exceed ₹ 50 Lakhs.

The key changes introduced are summarized as follows:

- For better transparency, individual taxpayers are now required to also select the relevant rule of residency (based on the individual’s physical presence in India) against the residential status selected by them (resident/ not ordinarily resident/ non-resident).

- Non-resident (NR) individuals are also required to report their overseas residency information along with taxpayer identification number. Overseas Citizen of India (OCI)/ Person of Indian Origin (PIO) taxpayers selecting residential status as “non-resident” in India are required to report their actual number of days in the relevant FY and in the last four FYs immediately preceding the relevant FY.

- ROR individuals claiming expense deduction under the head “income from other sources” (except for family pension) or holding unlisted shares in India or a director in a company, will no longer be able to use ITR1.

- The option of paper filing of ITR1 and ITR4 is now available only for ROR super senior citizens (age 80 years or more).

- ITR4 available for filing tax return under the presumptive taxation scheme is now restricted only to ROR individuals having total income not exceeding ₹ 50 Lakhs.

- The new ITR forms require disclosure in relation to unlisted shares with details of opening balance, acquired/ transferred during the year and the closing balance.

- More details are necessary to be filled for Double Taxation Avoidance Agreement (tax treaty) benefits claimed by the taxpayers under the “exempt income schedule,” including confirmation of tax residency certificate.

- Foreign assets and income schedule (Schedule FA) requires expanded disclosures, i.e., details of foreign depository accounts, foreign custodian account, holding of foreign equity and debt, foreign cash value insurance/ annuity held, either as an owner or beneficiary.

- Agricultural income exceeding ₹ 5 Lakhs is now required to be reported separately, along with additional details, such as the district name with pin code, measurement of agricultural land, whether owned/ leased, whether irrigated or rain fed under the “exempt income schedule.”

PwC comments: Several changes have been made in the forms seeking additional details, which will help in automatically validating or cross-checking the income and other details that the tax authorities may have from other sources.

This will not only improve the processing of tax returns in an automated environment but also help in keeping a check on income-escaping cases.

Seeking details about overseas tax residency etc. from NRs will help to validate treaty relief availed by such taxpayers in India. OCI/ PIO individual claiming NR status in their India tax returns should carefully track the number of days they stay in India and provide accurate details in the return form. Such details can now easily be cross-validated with the records already available with the immigration authorities which has also adopted the automation route in their working and have details of individual’s visits in India.

RORs will now be required to provide more details of their overseas assets, such as foreign depository accounts, foreign custodian account etc. India has already started getting details automatically from several countries with which it has information exchange treaties. Such overseas financial details will be cross-validated and a tighter control will be put on foreign income-escaping cases. Foreign nationals, who come to India temporarily, for a period of three to five years and become ROR of India, will face challenges in making such numerous disclosures, as they are already concerned for the privacy of their financial information.

Considering the Indian Government’s focus on tightening the compliance, taxpayers are required to take a note of these changes diligently and ensure they provide accurate details to avoid any questioning from the tax authorities at a later stage. is another instance where the SC has dismissed the SLP filed by the Revenue for disallowing expense under section 14A of the Act in the absence of exempt income and can be considered as a useful reference by taxpayers in a similar case.

Form 16 and Form 24Q amended to capture additional details

The Central Board of Direct Taxes has issued a new format for Form 16 (Salary TDS Certificate). Concurrent amendments have been made in the format of Form 24Q (TDS return). Following are the key amendments in the aforesaid Forms effective 12 May 2019:

Amendments in Form 16

Following individual line items have been added to capture additional details:

- Salary reported by the employee as received from other employer(s).

- Bifurcation of allowances exempt under section 10 of the Income-tax Act, 1961 (Act):

- Travel concession;

- Death-cum-retirement gratuity;

- Commuted pension;

- Cash equivalent of leave salary encashment;

- House rent allowance; and

- Any other exemption under section 10 of the Act.

- Income (or admissible loss) as reported by employee from housing property and income from other sources which have been reported to employer for excess tax deduction.

- Section-wise breakup of deductions claimed under Chapter VI-A of the Act which were earlier required to be reported as a consolidated number.

Amendments in Form 24Q

Following individual columns have been added to capture the additional details:

- Bifurcation of salary between gross salary, value of perquisites, and profits in lieu of salary.

- Bifurcation of allowances exempt, and deductions claimed (as introduced in Form 16).

- PAN of lender (mandatory) where the housing loan on which interest is paid is taken from a person other than a financial institution or the employer (previously optional).

PwC comments: In view of elevated use of technology and automated processes, the above amendments will expedite individual income-tax return processing by comparing the line items as appearing in the individual tax return forms with the TDS returns to allow rightful deductions and exemptions claim.

International Tax

CBDT proposes to amend rules for profit attribution to PEs – calls for public consultation

The issue of profit attribution to a Permanent Establishment (PE) has been the subject matter of extensive litigation. The Indian Revenue authorities and the Indian judiciary have, in the past, adopted/ upheld different approaches to profit attribution based on the facts of each case by applying Rule 10 of the Income-tax Rules, 1962 (the Rules).

With a view to bring greater clarity, objectivity, and predictability in the matter of attribution of profit to a PE, the Central Board of Direct Taxes (CBDT) formed a Committee (the Committee) to examine the existing scheme of profit attribution under Article 7 of the Double Taxation Avoidance Agreements, and to recommend changes in Rule 10 of the Rules.

The Committee has suggested a three-factor apportionment approach, by assigning equal weightage to sales, manpower (i.e., employees and wages) and assets. This represents a mix of both demand and supply related factors, thereby allocating profits derived from India, partly to the jurisdiction where sales take place (driven by consumers and market), and partly where factors of production are located or where supply related activities are conducted.

Further, the Committee has suggested that the aforesaid apportionment shall be applied to “profit derived from Indian operations” which will be the higher of the following amounts:

- The amount arrived at by multiplying the revenue derived from India by the global operational profit margin, or

- Two percent of the revenue derived from India.

Thus, even in a situation where the foreign enterprise has global losses or global profit margin of less than 2%, a minimum of 2% of the turnover derived from India, shall be deemed as “profits derived from Indian operations”.

If arm’s length profits derived from Indian operations have already been taxed in India in the hands of an Indian subsidiary of the foreign enterprise, then to that extent, such profits should be deducted from the profits apportioned to the PE (which has come into existence primarily due to the presence of the subsidiary). No profits, however, shall need to be apportioned to such PE, where the foreign enterprise does not receive payments exceeding INR 1 million from sales or services from any person resident in India.

Notably, the Committee has also explained its rationale for not entirely adopting the OECD guidance that gives primacy to the ‘Functions, Assets & Risk’ (FAR) analysis while attributing profits. The Committee is of the view that the OECD guidance focuses only on the supply side factors for attribution of profits and ignores factors related to markets and demand, which could have significant adverse consequences for developing economies like India that are primarily importers of capital and technology.

PwC Comments: The conclusions and recommendations set forth in the report have been put up for public consultation by the CBDT. This consultative and inclusive approach being adopted by the CBDT of inviting comments from stakeholders with respect to new policy measures and statutory amendments, is certainly welcome.

Regulatory

Manufacturing activity under an LLP

The provisions of the Limited Liability Act, 2008 (LLP Act) enabled an additional form of business organization in the form of a Limited Liability Partnership (LLP). As it provided a convenient mix of limited liability, a corporate entity and operational flexibility on the lines of a conventional partnership firm, it soon became a widely accepted structure for various domestic and international organizations when setting themselves up in India.

However, in the recent past, it has been observed that the Registrar of Companies (RoC), under the Ministry of Corporate Affairs (MCA), has been rejecting applications for the incorporation of new LLPs or the conversion of existing companies into LLPs for carrying out or intending to engage in manufacturing and allied activities. Such applications are being rejected on the basis of the definition of the term “Business” under the LLP Act.

Definition of “Business” under the LLP Act

Section 2(1)(e) of the LLP Act defines the term as, “Business” includes every trade profession, services and occupation. Although the definition is inclusive in nature and is not expected to be read in order to limit the coverage only to the activities in the services sector, there appears to be a view at the RoC/ MCA level that LLPs cannot be engaged in manufacturing and/ or allied activities.

Possible intent behind rejection by RoC

Various corporate governance and accountability measures have been prescribed for companies pursuant to the provisions of the Companies Act, 2013 (CA 2013). Entities engaged in manufacturing activity have the potential to become sizeable. If manufacturing and allied activities were allowed under LLPs, it would become an escape route to avoid the robust governance and accountability mechanisms, which otherwise, is applicable to companies registered under the CA 2013.

PwC comments: In view of this discussion on the definition of the term “Business” and in the absence of any specific circular or amendment to the LLP Act by the MCA, questions may arise on the validity of such action by the RoC. However, as the RoC is not permitting registration or conversion into LLP for manufacturing or allied activities, it is important to structure and plan business organizations accordingly.

Indirect Tax

SC upholds decision that salary reimbursed by Indian entity to foreign company for deputation of employees will not be taxed as manpower supply

Facts of the case

The assessee had entered into an agreement with its overseas parent company in Japan for payment of salary and other perquisites for employees deputed from such parent company. The employees deputed by the parent company operated under the control, direction and supervision of the assessee. Further, the assessee withheld tax on the salary paid to such employees as per the requirements of the Income-tax Act, 1961. The salary payment to such employees was disbursed by the overseas parent company. Subsequently, the salary cost was reimbursed to the parent company by the assessee.

The Revenue sought to tax such reimbursement of salary as manpower supply services and demanded service tax under the reverse charge mechanism.

The Tribunal ruled in favour of the assessee, after which the Revenue had filed an appeal with the Supreme Court (SC).

Supreme Court’s decision

The SC dismissed the appeal filed by the Revenue and upheld the Tribunal’s ruling. While determining the nature of service, it made the following key observations:

- The deputed person works under the control, direction and supervision of the assessee, and the compliance to withhold tax was also undertaken as an employer by the assessee.

- The assessee did not pay any direct or indirect compensation to its parent company for the deployment of employees, apart from the reimbursement of salary at cost.

- The terms of the agreement makes it clear that the relationship between the assessee and the deputed employee is that of employer-employee.

- Method of salary disbursement [through a group company] will not result in provision of service.

PwC comments: This is an important decision in favour of the industry, potentially concluding several on-going litigations pending at various Tribunals. The SC decision has laid down the essential principle that needs to be considered while determining an employer-employee relationship. While the decision pertains to the service tax regime, the industry should assess whether the tax authorities will accept the said position in the GST regime.

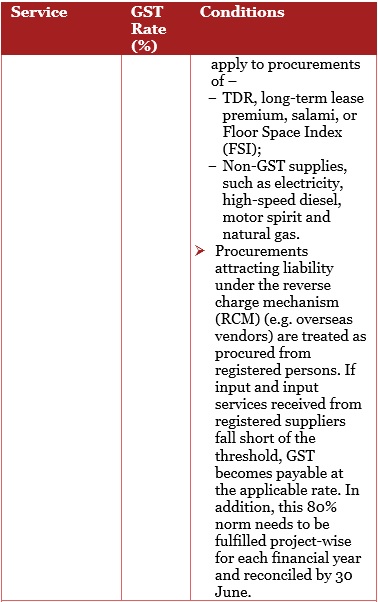

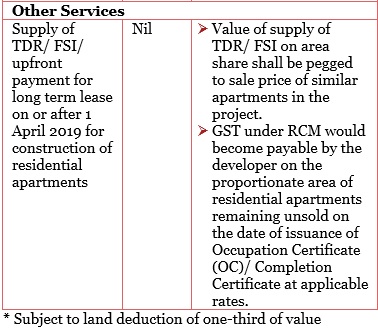

Goods and Service Tax update – Real Estate

The Government issued notifications containing the fine print on recent amendments that reduced the Goods and Service Tax (GST) rate on residential housing projects. For new residential real estate projects, the key amendments that became effective from 1 April 2019, and the conditions prescribed thereto, are discussed below:

Changes in ITC rules and calculation of transitional credits

The rules governing ITC on procurements by the developer also have been altered. The key takeaways are as follows:

- Projects commencing before 1 April 2019, would not be treated as on-going projects in cases where no apartments have been booked before 1-Apr-2019. In such cases, ITC as on 31-Mar-19 cannot be transitioned.

- On-going and new projects (with commercial and residential apartments) that do not transition ITC as on Mar-2019 can avail ITC (post 1 April 2019) only to the extent of the sales prior to OC.

- ITC eligibility as on 31 March 2019 in case of new projects/ on-going projects opting to pay tax in the new tax regime will need to be calculated as prescribed.

- For a project transitioning credits, as on 31 March 2019, the ITC computation of final eligible common credits (from 1 July 2017 until 31 March 2019) is calculated in the project in the prescribed manner.

- Projects (without a commercial portion) that transitioned credits as on 31 March 2019 would not require computing ITC on project completion.

- The above calculations are to be made for ITC reversal project-wise.

- ITC in respect of common inputs, input services and capital goods shall be assigned to each project and attract ITC reversals on project-level basis. ITC attributable to capital goods with useful life remaining at project completion shall be availed in a project in which capital goods are further used.

PwC Comments: The option provided to existing projects to remain in the erstwhile rate regime and the transition of credit is a welcome move. However, the computation mechanics to determine eligible and non-eligible credits (since new projects will be under the lower tax regime without ITC) are complex and will require a high degree of analysis, especially as computation is at the project-level. The decision to stay or exit the earlier regime and on-going compliances appears to require technology-based support and an audit trail for future assessments. The industry will find it challenging to comply with the said condition, including revalidating “project pricing.”

Reference

- Special Leave Petition (Civil) Diary No. 2755 of 2019

- Cheminvest Ltd. v. CIT [2015] 378 ITR 33 (Delhi HC)

- While dismissing the SLP, the SC has relied on its earlier ruling in the case of CIT v. Essar Teleholdings Ltd. [2018] 401 ITR 445 (SC), a detailed ruling on the retrospectivity of Rule 8D

- CIT v. Chettinad Logistics (P.) Ltd. SLP (Civil) Diary No. 15631 of 2018 where the SC has dismissed the SLP after a discussion on merits.

- TA No. 166 of 2016

- Notification No- GSR. 279(E), dated 1 April 2019

- CIT v. Chettinad Logistics (P.) Ltd. SLP (Civil) Diary No. 15631 of 2018 where the SC has dismissed the SLP after a discussion on merits.

- Vide Notification no. 36/ 2019

- 2018-TIOL-1976-CESTAT-DEL

- 2019-TIOL-151-SC-ST

- Notification Nos. 03/2019, 04/2019, 05/2019, 06/2019, 07/2019, 08/2019- Central Tax (Rate) and 16/2019- Central Tax dated 29 March, 2019

Résumé Portal

The Cochin Chamber of Commerce & Industry is pleased to announce that it now has a ‘Résumé Portal’ for freshers and others who are seeking jobs.

The Resume Portal of the Chamber is an initiative to help students find jobs in today’s highly competitive market. While we do not guarantee jobs for those who upload their résumés on the portal we will ensure that your résumé reaches the widest possible audience for their consideration.

The résumé/application you submit will undergo a strict scrutiny process following which, if accepted, it will be hosted on our portal. The acceptance or rejection of your résumé will solely be the Chamber’s prerogative based on various selection criteria.

Click here to submit your resume

Upcoming Events

CEO FORUM Breakfast Meetings 2019 - "Private Equity - How to get your Business ready!!!"

07.06.2019 | Taj Gateway Hotel, Ernakulam

The 6th Breakfast Meeting under the aegis of the CEO Forum 2019

Speaker: Mr. Vineet Satija, Director, Corporate Finance and Lead, Retail & Consumer – PwC India.

Topic: Private Equity – How to get your Businesses Ready!!!

Venue: Anchor Hall, Hotel Taj Gateway, Marine Drive, Ernakulam

Date: Friday, 7th June 2019

Time: 8 am to 10 am

GST - Refresher on Annual Returns/Audit Report and Other Updates

12.06.2019 | Park Central Hotel, Kaloor, Ernakulam

The Cochin Chamber of Commerce & Industry will be conducting a GST – ‘Refresher Session’ on the Annual Returns/Audit Report and other updates on Wednesday the 12th of June, 2019 from 02.00 p.m. to 05.00 p.m. at the Hotel Park Central, Kaloor.

The Session will be handled by Ms. Nisha Menon, Director – Tax | PwC, India.

The past few months leading to the Union Elections have seen quite a few changes in the GST space. With the Government notifying the updated Form GSTR-9 for GST Annual Returns and Form GSTR-9C for GST audits (which needs to be certified by a Chartered Accountant) to be filed by 30 June 2019 for FY 2017–18, Companies would have started to prepare for these compliances and would be in the advanced stages of finalization. The Government also intends to roll out the new simplified GST Return formats on a trial basis from July 2019.

During our session, we will share key considerations regarding the finalizing your first GST Annual Return/Audit Report, help re-assess your preparedness for the GST Audit process and provide updates on GST from a judicial as well as legislative perspective.

Delegate fees are as below

Members: Rs.750/- (incl. GST)

Non-Members: Rs.1,000/- (incl. GST)

Click Here to register

Representation on ........

Levy and Collection of Kerala Flood Cess | 29.05.2019

The Cochin Chamber has taken up the matter on the “Levy and Collection of Kerala Flood Cess” with the Government of Kerala for the immediate intervention of the Finance & Taxes Department, Government of Kerala.

The Letter sent to the Honourable Minister of Finance is shown below.

Mr. Thomas Isaac

Honourable Minister for Finance

Government of Kerala

Trivandrum

Sir,

LEVY AND COLLECTION OF KERALA FLOOD CESS

The Government of Kerala has issued Notification No. 80/2019 proposing to levy the Kerala Flood Cess. The reports and certain views expressed have created some confusion regarding the levy and collection of the cess within the business community.

The Cochin Chamber is of the understanding that the levy and collection of Kerala Flood Cess is similar to the GST Compensation to States Act, 2017 and that Clause 2 of the Finance Bill is drafted similar to Section 8 of the GST Compensation to States Act 2017. Accordingly, the KFC @1% would be on value of supply before CGST and SGST and thus the effective the rate of GST (CGST+SGST+Cess) would result in 1% additional tax. We are also of the understanding that reference to the value of supply in the levy of cess is only to clarify that the cess is not on the SGST.

However, there is some confusion in the minds of the trade and industry that the reference of levy to the value of supply would be to mean that CGST and SGST will have to be worked out on the value including Cess. We request you to be good enough to issue a clarification to clear the doubts in this regard.

Further, the KFC is intended only on B2C transactions and in the case of goods covered under MRP, this can result in the last point dealer absorbing the same as his cost unless a clarification is issued. A similar issue had arisen on the introduction of GST where the tax rates had gone up and Government had clarified that the additional tax can be collected by displaying the old and new MRP due to the charge of cess and the increase should be only on account of the cess.

The Chamber would be extremely pleased if clarification is issued urgently since the retailers have to modify their software to suit the new billing structure from 1.6.2019 which is just two days away.

Requesting your immediate and positive intervention in the matter.

Yours faithfully

V Venugopal

President

Exclusive EXIM Statistics Sample Reports