President's Note

Dear Friends,

The hustle of the recent Parliamentary elections has died down and a new Government has taken charge amidst very high expectations. We understand that the First Union Budget of the new Government will be presented in Parliament on the 5th of July 2019. The whole country, especially trade and industry, is waiting with bated breath to see what the new Finance Minister Ms. Nirmala Seetharaman has in store to further promote the economic growth of the country.

As you all know, each year, the Chamber organizes a Post Budget Analysis Lecture aimed at explaining the announcements made in the Union Budget. This time too we will be conducting the Annual Post Budget Analysis on Monday the 8th of July 2019 at the Hotel Avenue Centre. The Lecture will be delivered by Mr. Homi P Ranina, one of India’s foremost Tax Consultants and a practicing Attorney from Mumbai. I cordially invite all of you to attend this event.

I am very happy to inform you that the Chamber is in the process of setting up a Research Wing and that it has already started working. To start with we have studied the draft Kerala Metropolitan Transport Authority (KMTA) Bill, 2018 and made submissions on the same to the Select Committee on the Kerala Metropolitan Transport Authority Bill.

We have been conducting CEO Forum Breakfast Meeting for the past 4 years. The Forum gives a platform for the CEOs to meet and discuss on various issues prevailing in the Industry and also to explore new ideas. We also have many eminent Speakers addressing the CEOs on a variety of subjects. The Guest Speaker at this month’s meeting was Mr. Vineet Satija, Director, Corporate Finance and Lead, Retail & Consumer – PwC who spoke on “Private Equity – How to get your Businesses Ready.” The session covered various financing options available for businesses today, benefits of raising capital from private equity, investment criteria for private equity and the process involved in raising private equity.

Accordingly, we have the next CEO Forum Breakfast Meeting on the 5th of July 2019. The meeting will be “An Interactive Breakfast Session with the new District Collector, Mr. Suhas S. I.A.S. “. I hope you will all find it convenient to attend this session and make the most out of it.

Last week, we organized a half-day “Refresher Session on GST Annual Returns and Audit Reports” which was a huge success. The Speaker for the session was Ms. Nisha Menon, Director, Tax – Pwc India. The session was organized with the intention of sharing key considerations regarding the GST annual returns filing. The programme hosted 150 delegates from various companies. A detailed report of this event can be found in the later part of this edition of the Chamber Voice.

On the 12th of July, we propose to do a one-day session on “Corporate Compliances, 2019.” This seminar is aimed at giving our member and non-member organisations a wider understanding about the current laws and compliances under Corporate Law. To address the audience we have Adv. Prashanth S Shivadass – Advocate & Founder of Shivadass & Shivadass (Law Chambers) and Adv. Hari Prasad M S – Advocate at Shivadass and Shivadass (Law Chambers). Details about this programme are given in the upcoming events section of this Newsletter. A mailer with all the speaker profiles will reach you in due course.

The Cochin Chamber has been consistently organizing programmes of importance to the business community in Kerala and I am proud being a part of its successful existance. The feedback that we have been getting after each programme has been very encouraging, and this motivates us to do more. As always, I am looking forward to your support in all our endeavours in the future.

Wishing you all the best!

V Venugopal

Fine Points

Recent Events

6th CEO FORUM Breakfast Meeting

"Private Equity - How to get your Businesses Ready!!" | 07.06.2019

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s – 6th Breakfast Meeting on Friday, 7th June, 2019 at the Taj Gateway Hotel, Ernakulam.

Mr. V Venugopal, President of the Chamber delivered the Welcome Address and introduced the Speaker for the meeting, Mr. Vineet Satija, Director, Corporate Finance and Lead, Retail & Consumer – PwC. The topic for the Session was “Private Equity – How to get your Businesses Ready.”

Mr. Vineet Satija explained in detail the different financing options available for businesses today, benefits of raising capital from private equity, investment criteria for private equity and the process involved in raising private equity.

Equity Funding and Debt Funding are the two ways of funding a business. Equity financing comes in a wide range of forms, including Venture Capital, an Initial Public Offering, business loans, and private placement. The risk for equity is higher and as a result, the return expectation is also higher.

Mr. Satija spoke on the different factors for choosing the capital namely – the company profile, repayment ability, nature of the industry, and the risk appetite of the company. Most of the options available in the market today to raise capital are Private Equity, Venture Capital, Public Markets, and Debt Funds.

Mr. Satija explained that the important factor that differentiates between all of the above is the risk-return expectation. The return expectation for private equity is 20% per annum, for a venture capital it is 2 times the investment, for public markets it is 12% per annum, for debt fund it is 10-15% per annum, he added.

He also mentioned that the number of deals in private equity has been constant but the value of transactions increased over the years. The two sectors which attracted the maximum investment in private equity were technology and financial services.

Mr. Satija concluded by mentioning the factors to be considered before investing in a Private Equity namely Market Dynamics, Scalability of the Business, Corporate Governance and Financial Performance.

Mr. C S Kartha, Past President of the Chamber presented a Memento to Mr. Satija.

Mr. S P Kamath, Executive Committee Member proposed the Vote of Thanks.

The interactive session concluded by 10 a.m with Breakfast.

Workshop on Goods & Services Tax

"Session on Annual Returns/Audit Report and Other Updates" | 14.06.2019

The Cochin Chamber of Commerce and Industry organized a session on “Annual Returns/Audit Report and other updates” on Saturday the 12th of June, 2019 at Hotel Park Central, Ernakulam. The session was handled by Ms. Nisha Menon, Director, Tax – PwC India.

Mr. V Venugopal, President of the Chamber delivered the Welcome Address. The session was organized with the intention of sharing key considerations regarding the GST annual returns filing and to provide latest updates on GST.

Ms. Menon gave the participants an insight into the basic concepts of GST Annual Returns, GSTR 9 and GSTR 9C. GSTR-9 or GST annual return is a type of GST return that must be filed by regular taxpayers and persons registered under GST composition scheme. She mentioned that every registered person whose aggregate turnover during a financial year exceeds two crore rupees should get their accounts audited and should furnish a copy of the audited annual accounts and a reconciliation statement, in form GSTR-9C.

Ms. Menon explained the GSTR 9C form which is meant for filing the reconciliation statement of taxpayers pertaining to a particular financial year. The form is a statement of reconciliation between the Annual Returns in GSTR-9 and the figures mentioned in the Audited Financial Statements of the taxpayer. She also gave a detailed explanation of the format of the GSTR 9C which includes the Reconciliation of Turnover, Reconciliation of Tax Paid, Reconciliation of ITC, Additional Liability etc.

The session also covered the accounts and other records to be maintained, what to expect out of a GST Annual Audit Programme and how to prepare for the audit procedures in detail. Ms. Menon also mentioned the latest updates on the GST front from a legislative as well as judicial perspective.

Following this, there was a question and answer session where the participants cleared their doubts regarding the GST Annual Returns.

Mr. C S Kartha, Past President of the Chamber presented a Memento to Ms. Menon and proposed the Vote of Thanks.

Decisions taken by the GST Council in the 35th meeting.....

The 35th GST Council Meeting was held under the Chairmanship of Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman. This was the first meeting of the Council after the swearing in of the new Government. The meeting was also attended by Union Minister of State for Finance & Corporate Affairs Shri Anurag Thakur besides Revenue Secretary Shri Ajay Bhushan Pandey and other senior officials of the Ministry of Finance.

The GST Council recommended the following decisions:

(A) Changes in law and procedure: In order to give ample opportunity to taxpayers as well as the system to adapt, the new return system to be introduced in a phased manner, as described below:

- Between July, 2019 to September, 2019, the new return system (FORM GST ANX-1&FORM GST ANX-2 only) to be available for trial for taxpayers. Taxpayers to continue to file FORM GSTR-1&FORM GSTR-3B as at present;

- From October, 2019 onwards, FORM GST ANX-1 to be made compulsory. Large taxpayers (having aggregate turnover of more than Rs. 5 crores in previous year) to file FORM GST ANX-1on monthly basis whereas small taxpayers to file first FORM GST ANX-1 for the quarter October, 2019 to December, 2019 in January, 2020;

- For October and November, 2019, large taxpayers to continue to file FORM GSTR-3B on monthly basis and will file first FORM GST RET-01 for December, 2019 in January, 2020. It may be noted that invoices etc. can be uploaded in FORM GST ANX-1 on a continuous basis both by large and small taxpayers from October, 2019 onwards. FORM GST ANX-2 may be viewed simultaneously during this period but no action shall be allowed on such FORM GST ANX-2;

- From October, 2019, small taxpayers to stop filing FORM GSTR-3B and to start filing FORM GST PMT-08. They will file their first FORM GST-RET-01 for the quarter October, 2019 to December, 2019 in January, 2020;

- From January, 2020 onwards, FORM GSTR-3B to be completely phased out

On account of difficulties being faced by taxpayers in furnishing the annual returns in FORM GSTR-9, FORM GSTR-9A and reconciliation statement in FORM GSTR-9C, the due date for furnishing these returns/reconciliation statements to be extended till 31.08.2019

To provide sufficient time to the trade and industry to furnish the declaration in FORM GST ITC-04, relating to job work, the due date for furnishing the said form for the period July, 2017 to June, 2019 to be extended till 31.08.2019

Certain amendments to be carried out in the GST laws to implement the decisions of the GST Council taken in earlier meeting

Rule 138E of the CGST rules, pertaining to blocking of e-way bills on non-filing of returns for two consecutive tax periods, to be brought into effect from 21.08.2019, instead of the earlier notified date of 21.06.2019

Last date for filing of intimation, in FORM GST CMP-02, for availing the option of payment of tax under notification No. 2/2019-Central Tax (Rate) dated 07.03.2019, to be extended from 30.04.2019 to 31.07.2019

(B) Rate changes on supply of good and services: The Council has recommended following GST rate related changes on supply of goods and services.

Electric Vehicles

On issues relating to GST concessions on electric vehicle, charger and hiring of electric vehicle, the Council recommended that the issue be examined in detail by the Fitment Committee and brought before the Council in the next meeting.

Solar Power Generating Systems and Wind Turbines

In terms of order of the Hon’ble High Court of Delhi, GST Council directed that the issue related to valuation of goods and services in a solar power generating system and wind turbine be placed before next Fitment Committee. The recommendations of the Fitment Committee would be placed before the next GST Council meeting.

Lottery

Group of Ministers (GoM) on Lottery submitted report to the Council. After deliberations on the various issues on rate of lottery, the Council recommended that certain issues relating to taxation (rates and destination principle) would require legal opinion of Learned Attorney General.

(C) Setting up of GSTAT, extension of tenure of National Anti-Profiteering Authority and introduction of e-invoicing taken: The Council took a decision regarding location of the State and the Area Benches for the Goods and Services Tax Appellate Tribunal (GSTAT) for various States and Union Territories with legislature. It has been decided to have a common State Bench for the States of Sikkim, Nagaland, Manipur and Arunachal Pradesh.

The tenure of National Anti-Profiteering Authority has been extended by 2 years.

The Council also decided to introduce electronic invoicing system in a phase-wise manner for B2B transactions. E-invoicing is a rapidly expanding technology which would help taxpayers in backward integration and automation of tax relevant processes. It would also help tax authorities in combating the menace of tax evasion. The Phase 1 is proposed to be voluntary and it shall be rolled out from January 2020

Article

NDA 2.0 – NO CAKE WALK

India has undoubtedly been the fastest growing major economy in the world and is expected to be one of the top three economic global powers over the next decade, backed by its strong fundamentals.

However, what is important to observe is that, the growth rates may not be as consistent as is perceived to be. The data shown below, clearly shows a slowdown in GDP (Q4). The International Monetary Fund (IMF) has cut India’s GDP growth forecast for 2019-20, following a similar action by the Asian Development Bank (ADB) and the Reserve Bank of India (RBI).

Though the IMF expects a road to recovery, through continued investment, reducing public debt and increase in consumption, the road to that goal will be a huge challenge.

The Lok Sabha elections, are certainly a moral boost for the NDA, the Narendra Modi Government and the economy, however, a 5-point reform based agenda is imperative to bolster growth.

1. REDUCING THE BANKING & NBFC (NON BANKING FINANCE COMPANY) STRESS

The NPAs (Non-Performing Assets) of State run Banks and other financial institutions, that most certainly are likely to be written off, prevents new investment from taking place. The new Bankruptcy Law, and the Reserve Bank of India’s attempt to make it operational and effective, has found limited success.

This, if not resolved, will allow the situation to linger and even worsen, rather than improve. Mergers of smaller banks with larger ones, is not the only solution to this problem.

The liquidity pressure the NBFCs are facing, after the IL&FS default in September 2018, has certainly affected consumer finance. Adding to this, delayed credit payments by DHFL, have fuelled the much debated hypothesis called the ‘liquidity cholesterol.’

The flow to NBFCs, which finance a significant portion of car loans, home loans, gold loans and other discretionary spends, has slowed. As is known, when liquidity is tight people do not make discretionary purchases.

With the RBI cutting Repo Rate by 25 basis points, the ball is set to roll. Still, better liquidity, fuels optimism. The New Finance Budget, needs serious provisioning to address this issue.

2. BOOSTING CONSUMPTION

A slack in overall consumption is the result of an income growth slump in urban and rural areas, falling money supply in the economy and rising uncertainty over how customers will respond to regulatory action. The NBFC stress has added its share to reducing consumption.

While on the FMCG (Fast Moving Consumer Goods) business, the number of brands in the family get reduced. On the automobile front, the passenger car volumes have dropped in nine out of the past 10 months. Growth was down to 2% in the last fiscal year. Two-wheeler volume growth fell to the lowest since the currency note swap exercise in November 2016.

3. RATIONALISE DIRECT TAXES, GST & PROMOTE A ROBUST DISINVESTMENT DRIVE

The Governments effort to bring more tax payers into its fold has had reasonable success. From 3.6 Crore IT returns in 2014-15, the number has risen to 7.1 Crores in 2018-19. However, to have a reasonable broadening of the tax payer base, IT slabs need to be rationalized in keeping with current Per Capita Income and Inflation. This could drastically, fuel Governments expenditure plans on reform till 2023.

An important reform, the GST, needs to be simplified further and implemented fully. Many goods and services, that are in 28% slab needs to be rationalized. Continuing to broaden the income tax base, and working out an effective and non-capricious way of collecting corporate taxes, especially from multinational corporations, is mandatory.

Troubled State-run enterprises and Corporations, are a drain on the exchequer and a wastage of the tax payers’ money. The troubled airline, Air India, is a classic example. Ideally the Government should disinvest its stake/sell off ensuring limited job cuts. This should be defined target and executed in a time bound manner.

4. MAKE IN INDIA & RE-ENERGISING EXPORTS

Among the many reforms of NDA 1, the Make in India initiative did not take off as expected. While it is a visionary reform, introduced to promote exports, enable skill empowerment, create jobs and as a result reduce the CAD (Current Account Deficit), it has not been able to achieve the goals envisaged.

The focus of the Make in India programme is on 25 sectors, ranging from high consumption sectors like automobiles, aviation, chemicals and pharmaceuticals and scaling up to space, thermal power, roads and highways and electronics systems. The Finance Minister should push this flag ship reform to greater heights through more investment and allocations in the upcoming Finance Budget.

The recent trade sanctions with the US, may not be a considered a great dampener to India’s exports to the US, however, the impact of the removal of India from the Generalized System of Preference (GSP) by the Trump administration needs be viewed seriously.

5. ENERGISE THE AGRICULTURE SECTOR

The real strength of the Indian economy, gets tested time and again, when rural India, where the majority still reside, remains relatively poor and is falling further behind. While reasonable support has enabled better farm produce since 2014, restrictions on marketing and trade often constrain the ability of farmers to get the most value for their crops. Intermediaries continue to exert disproportionate power in markets for inputs and products. This needs to be tackled.

With RBIs latest repo rate cut, and with another expected shortly, the liquidity crunch may be far from over. In the fifth Governing Council meeting of the NITI Aayog, the Prime Minister has said that the food processing sector should grow at a faster pace to benefit the farmers. Effective steps to tackle the drought situation facing the country with the spirit of ‘per drop more crop’, if enacted well, should increase productivity.

The results of flagship schemes like PM-KISAN, hopes to reach intended beneficiaries well within time. In his recent address the Prime Minister has said that the aim of his new government was to provide piped water to every rural home by 2024 for which special attention had to be given to water conservation and management.

All having been said, tokenism and vote bank politics should not define the growth of Rural India. We hope that the Finance Minister will have reasonable allocations for the betterment of Rural India, in her maiden Budget.

Article courtesy Mr. Manoj Mullath, Founder & Head – Wealth & Key Relationships Capricorne Mindframe, Chennai.

Manoj Mullath

A distinguished Wealth and Portfolio Management Professional with 17 Years of distinguished service in areas covering FMCG, Banking and Investment Banking and Wealth Management.

With a Bachelors in Economics and Management Degree (in affiliation with the IIFT, New Delhi) with specialisation in International Finance and Marketing, Manoj has had an illustrious career both in the corporate world and through his Wealth and Portfolio Management venture, Capricorne Mindframe, founded in 2009. A speaker on selective forums on topics concerning the Economy, Wealth Management, Soft Skills and the role of education for empowerment as well as specific reforms like Demonetisation.

Chamber in News

The President Mr. V Venugopal and Mr. C S Kartha, Past President attended a Public Hearing organised by the District Administration at the requet of the Mayor Ms. Soumini Jain, to address the grievances of the general public in connection with the setting up of a new waste treatment plant at Brahmapuram.

The Hearing was held to ensure the new project is implemented after addressing their apprehensions of the general public and the locals on the plant.

Civic Administrators had asked the implementing agency to ensure that the proposed waste-to-energy plant did not convert into an open waste dumping yard in the future. They also cited the existing Brahmapuram plant as an example. The Plant construction should be carried out in a scientific manner and water bodies near the proposed plant’s site, including Chitrapuzha and Kadambrayar, should be protected.

A majority of the people who attended the meeting also asked about the possibility of sound pollution from the proposed plant. Other concerns raised include, separation of chlorinated materials, experience of the company and clauses mentioned in the contract with local bodies for the construction of the plant. They also demanded the progress of the project be monitored at regular intervals. “Waste collection and transportation of waste to the plant should be carried out in a scientific manner and the project should be completed in a time-bound manner.

The officials from the implementing agency had said that the technology adopted by thickly populated foreign countries will be used for the construction and maintenance of the plant. The plant will emit smoke equivalent to three diesel cars’ emission, while running on the road. There are special facilities to make the plant odour-free. The water from the plant will not be diverted to nearby water bodies. It will be collected separately.

The President of the Chamber also spoke at the Hearing and advocated for a new plant at Brahmapuram. He emphasised the fact that the concerns of the local people needed to be taken into consideration and their fears allayed before embarking on the project.

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

CBDT specifies procedure, formats and standards for the issuance of Form 16, makes it mandatory to download Part B of Form 16 from TRACES Portal

In a recent notification the Principal Director General of the Income-tax (Systems) has specified the procedure, formats and standards for the generation and downloading of certificate of tax withheld (Form 16). This is applicable from financial year (FY) 2018-19, and all employers need to download Part B of Form 16 from the TRACES Portal. In addition, they need to authenticate the correctness of the contents mentioned therein before issuing it to its employees, and verify the same using either a manual or digital signature. The other guidelines in the notification are as follows –

- All employers shall be able to issue Part B of Form 16 (as downloaded from the TRACES Portal) provided that the tax deducted at source (TDS) statement for quarter four (Form 24Q) is furnished with duly filled-in Annexure II (i.e. details of salary paid/ credited and net tax payable) as substituted vide notification no. 36/ 2019.

- TRACES generated Form 16 shall have a unique TDS certificate number.

- Details of exemptions under section 10 of the Income-tax Act, 1961 (Act) and deductions under chapter VI-A of the Act, which are not specifically provided in Annexure II of Form 24Q are to be filled in by the employer manually, before the issuance of Form 16.

- If the deductor opts to authenticate Part B manually, TRACES downloaded Part B will contain fields at the bottom for the exemptions/ deductions as mentioned above, which the deductor shall duly fill in, where applicable.

- In case of digital authentication, the Form will contain no such fields and deductors may prepare the details of other exemptions/ deductions as annexure and issue it to the employees, where applicable, before furnishing the Form 16 to its employees.

PwC Comments: All employers should take note of the above procedures, as the TDS statements for the fourth quarter of FY 2018-19 are due by 31 May 2019, and all employers need to issue Form 16 to their employees within the due date, i.e., 15 June 2019. Employers should also ensure correct and accurate disclosure at the time of filing TDS statement to avoid any questioning by the tax authorities in relation to the difference in the amounts reported in Part A and Part B of Form 16 issued to employees.

Manual return of income can be filed if the online utility is not amended to reflect the correct tax position

In a recent decision, the Delhi High Court (HC) held that a mere software glitch cannot prevent the taxpayer from claiming a benefit in the tax return, and directed the Revenue to either allow the taxpayer to manually file return or alter the online utility to enable the taxpayer to file the return

PwC Comments: This is a welcome ruling by the HC, allowing the taxpayers to file the Return of Income manually before the Tax Officer, if the online return form utility does not allow a genuine claim/ benefit.

Bombay HC rules that the revenue authorities cannot hold back refunds merely on account of a lapse in their computer system

The proceedings under section 201(1) of the Income-tax Act, 1961 was concluded against the taxpayer and a tax demand was raised which was also upheld by the Commissioner of Income-tax (Appeals). The taxpayer had deposited approximately 77% of the amount against the said demand and preferred an appeal on merits before the Income-tax Appellate Tribunal (Tribunal). The Tribunal ruled in favour of the taxpayer and deleted the said demand. Accordingly, the taxpayer requested for refund of the sum deposited by it. Separately, there was an outstanding demand owing to human error due to duplicate recording of a payment under old as well as new Tax Deduction Account Number (“TAN”). The revenue authorities agreed that this was an error and the corresponding demand should be deleted. However, despite such a communication, the demand was not deleted from the revenue authorities’ computer system and the refund due to the taxpayer (discussed above) was withheld by the revenue authorities.

The High Court (HC) disposed the petition in favour of taxpayer and held the following:

- The HC ruled that revenue authorities cannot withhold the refund owed to the taxpayer, irrespective of whether it is accepted by the system, as factual aspects cannot be overridden.

- The HC directed the revenue to release the refund owed to the taxpayer along with applicable interest within a prescribed timeline. Further, the revenue authorities were instructed to take steps to rectify the error in their computer system as expeditiously as possible.

PwC comments: This is a welcome decision in favour of the taxpayers as practically, there are a lot of cases where the tax demand is deleted by the revenue authorities but the refund cannot be processed in a timely manner owing to technical glitches in computer systems. This decision can be a useful reference for taxpayers being denied of rightful refund due to lapse in IT processes

Section 56(2)(vii) applicable to ‘property’ in the nature of capital asset and not which is traded in the normal course of business or trade

Recently, the Jaipur bench of the Income-tax Appellate Tribunal (Tribunal) held that the intention of clause (vii) of section 56(2) of the Income-tax Act, 1961 (Act) is not to tax the transactions entered in the normal course of business or trade, where the profits are taxable under the specific income head..

PwC Comments: This decision provides guidance on the interpretation of the term ‘property’ as appearing in section 56(2)(vii)(b) of the Act and now for section 56(2)(x)(b) of the Act. It also re-emphasizes that the intent is not to tax transactions entered into normal course of business. However, going forward this is likely to evolve further where transactions of similar nature could potentially be challenged

Tribunal holds that amount received by a retiring partner above his capital account is chargeable as capital gains

Recently, the Bangalore bench of Income-tax Appellate Tribunal (Tribunal) held that the retiring partner is liable to capital gains tax being the excess payment received over and above the sum to the credit of her capital account at the time of retirement. However, the Tribunal modified the computation by treating the goodwill, which was recorded post 31 March 2007, as a part of the partner’s capital account.

PwC Comments: While the taxability in the hands of the partners upon retirement is an issue prone to litigation, this decision adds up to the conflicting judgements on this issue

International Tax

Consideration received for granting of distribution rights for a TV channel is not royalty

Recently, the Bombay High Court (HC) dismissed Revenue’s appeal against the Income-tax Appellate Tribunal’s (Tribunal) ruling to hold that the payment received for granting distribution rights of a TV channel is not taxable as ‘royalty’ under section 9(1)(vi) the Income-tax Act, 1961 (Act) as well as the India–Singapore Double Taxation Avoidance Agreement (tax treaty).

PwC Comments: The HC reconfirmed the distinction between ‘copyright’ and ‘BBR’, both of which are defined under the Copyright Act in the context of foreign telecasting companies. Further, the decision of HC affirms the position that where a non-resident company has granted a non-exclusive distribution right of a channel which enables the individual customers to view the programs telecasted on channels, without any right to use/ exploit any copyright, the ‘distribution fee’ received by such non-resident entity should not be treated as ‘royalty’.

Indirect Tax

HC allows input tax credit on input materials/ services used for developing a shopping mall against GST payable on rent received from tenants

In a ruling that underscores a progressive approach to input tax credit (ITC), the Orissa High Court (HC) has recently issued a ruling on how the bar on availing ITC on construction activities should be interpreted.

Facts

- The petitioner was engaged in the construction of shopping malls for the purpose of letting out units to tenants/ lessees. To carry out the construction activity, the petitioner purchased a range of goods (cement, steel, lifts, escalators, equipment, etc.) and services (consultancy, design and engineering, etc.)

- GST was paid on the goods and services thus procured on which credit was availed. Upon near commencement of rental activities, the petitioner approached the revenue authorities to seek clarity on availing ITC for the same and utilising it to pay GST on the rentals received from the tenants.

- The authorities denied ITC to the petitioner in view of section 17(5)(d) of the Central Goods and Services Tax Act, 2017 (CGST, Act) which restricts ITC of goods or services received for construction of an immovable property (other than plant or machinery) on one’s own account, and directed the petitioner to ensure that ITC is not availed so as to avoid the imposition of penalties.

High Court’s decision

The HC, in a response to writ filed against this approach adopted by the tax authorities, ruled in favour of the petitioner and observed that:

- The narrow interpretation of the GST Act put forward by the authorities frustrates its objective, which is to provide a seamless credit mechanism between expenses and revenues; it should, instead, be interpreted in a manner that obviates double taxation, as the taxpayer has paid substantial amounts of GST on procurements.

- Importantly, such an approach will create a distinction between real estate developers who incur such expenses in selling the immovable property prior to completion (where ITC is admitted as allowed) and scenarios where the constructed property was rented out (where ITC is denied). Such a distinction, in the opinion of the court, would debar businesses undertaking a continuous operation (i.e. renting) from availing credit, creating an unequal distinction and diluting the right to do business.

- An analysis of section 17(5)(d) of the CGST Act indicates that it should apply to a situation where the property is retained for one’s own use/ purpose, but not when property is let out.

PwC Comments: It should be noted that section 17(5)(d) of the CGST Act has not been struck down, but its interpretation (as proposed by the tax authorities) has been restricted. Given the positions adopted by the real estate and warehousing sector since the introduction of GST, tax payers should monitor further developments and examine the impact on their business models.

Maharashtra ARA holds that technical know-how provided by a foreign entity to an Indian entity are intangible goods and the situs of sale is where the property is registered for the purposes of VAT

Facts

The applicant is a UK-based entity engaged in bulk drugs research and production. The applicant did not have a registered office in India and was operating from the UK. It had entered into an agreement with an Indian entity wherein it provided consultancy/ advice regarding the manufacturing and development of products to improve manufacturing processes and techniques, procurement of raw material for formulations of products that are not available in India, ensure quality control, results of clinical trials, etc., against payment of consideration termed as “royalty.”

The questions before the Advance Ruling Authority (ARA) constituted under the Maharashtra Value Added Tax Act, 2002 (MVAT Act) were as follows:

- Whether the above transaction is covered by the scope of taxing entry 39 “technical know-how or services” of Schedule C of the MVAT Act?

- Whether the transaction effected can be considered as a “sale in the course of export” under the MVAT Act?

- Whether it is necessary to give prospective effect to the ruling?ARA’s ruling

- Applying the legal meaning and the test of common parlance, expertise, thoughts/ ideas in the nature of technical support and knowledge on specific technology or way of undertaking an activity more efficiently and effectively is covered under the scope of “technical know-how.”

- Such know-how falls under the category of intangible goods. The ARA relied on the decision of the Supreme Court in Tata Consultancy Services, where it was held that properties that are capable of being abstracted, consumed and used and/ or transmitted, transferred, delivered, stored or possessed are “goods” for the purposes of sale tax.

- The situs of intangible property is where the property is registered, or, if not registered, where the rights to the property can be enforced. In this case, the right of technical know-how is enforced in Maharashtra and is not a sale in the course of export.

- The discretionary power to declare the prospective effect of tax liability was not exercised by the ARA in order to protect legitimate tax liability.

PwC Comments: This rare ruling by the ARA constituted under the MVAT Act potentially unsettles historical positions in the pre-GST era. Primarily, the view espoused is against the position adopted by the industry that situs of sale for right to use or lease goods is the location where the agreement is executed, relying on rulings in 20th Century Finance and Ambalal Sarabhai. Recently, the Kerala HC in Lal Products held that situs of sale of trademarks (also treated as intangible goods) is the principal place of business of the transferor, while the Bombay HC, in Mahyco Monsanto Biotech (India) Private Limited, held that situs of ownership of an intangible asset would be the closest approximation of the situs of intangible asset. Moreover, the arrangement here has the characteristics of a service contract for consultancy/ advice, which could constitute a “work for hire.” Considering the difference in positions taken by various courts on intangible goods, this ruling may prompt the tax office to question positions taken by overseas parties until 30 June 2017.

References:

Notification No. 09/ 2019 dated 06 May, 2019

W.P. (C) 3598/2019 & CM Appl. No. 16512/ 2019

Writ Petition No. 1103 of 2019 (Bombay HC)

ITA No. 392/JP/2019

ITA No. 1700/Bang/2016 [TS -257-ITAT-2019(Bang)]

ITA 103 and 207 of 2017

Writ Petition No. 20463 of 2018 (Orissa HC)

Order No. ARA Mumbai – 09 of 2016-17/2019-20

Upcoming Events

7th CEO FORUM Breakfast Meeting

An Interactive Breakfast Session with the new District Collector of Ernakulam

The 7th CEO FORUM Breakfast meeting will be held on the 5th of July, 2019.

An Interactive Breakfast Session with the new District Collector of Ernakulam, Mr. Suhas S. I.A.S.

Date: Friday, 5th July 2019

Time: 8 am to 10 am

Anchor Hall, Hotel Taj Gateway, Marine Drive, Ernakulam

Click Here to register

Contact us at:

[email protected]/ 6238383922

Annual Post Budget Analysis 2019-20

Monday | 08.07.2019

The Cochin Chamber of Commerce & Industry will be organising the Annual Post Budget Lecture – 2019-20 on Monday the 8th of July, 2019 at Hotel Avenue Centre, Panampilly Nagar, Ernakulam.

The Speaker for this session will be Mr. Homi P Ranina, one of India’s foremost Tax Consultants and a practicing Attorney from Mumbai.

You are invited to attend this event at which the nuances and implications of the First Union Budget of the New Government will be analysed and explained.

Free entry by prior registration only.

Click Here to register

Contact us for further details

9895676827, 9744629992, 7025738447

Corporate Compliances, 2019

A Tutorial for Companies | Friday | 12.07.2019

The Cochin Chamber of Commerce & Industry is organising a one-day Seminar on “Corporate Compliances, 2019 – A tutorial for Companies.”

Speakers:

Prashanth S Shivadass – Advocate & Founder of Shivadass & Shivadass (Law Chambers)

Hari Prasad M S – Advocate at Shivadass and Shivadass (Law Chambers)

Click Here to register

Contact us for more details

Thomas Sebastian: 6238347779

Manu Varghese: 9895676827

From........... the Research Wing

SUBMISSION TO THE SELECT COMMITTEE ON THE KERALA METROPOLITAN TRANSPORT AUTHORITY (KMTA)

The Chamber submitted its comments on the ‘Draft Kerala Metropolitan Transport Regulatory Authority Bill, 2018’ recently. Through this, the Chamber re-emphasised its commitment towards the overall development of Kochi and Kerala. The submission critiques the version of the Bill by suggesting necessary amendments and additions that will strengthen the foundation of the Transport Regulatory Authority. We have advocated for a non-bureaucratic centric composition of the Transport Authority, adoption of participatory processes, adoption of gender neutral language, inclusion of provisions for promotion and dissemination of research content etc.

Detailed submissions available on request.

KERALA FLOOD CESS

The Chamber submitted a representation to the Finance Minister on 29th May 2019 in connection with the Government’s Notification No. 80/2019 proposing to levy a Kerala Flood Cess from 1st June 2019 . Based on the apprehensions raised from various corners, the State Government issued Notification G.O.(P) No. 81/2019/TAXES and deferred the collection of the Flood Cess to 1st July 2019.

The Chamber is preparing a detailed note explaining the possible impact of the cess with alternative ways to generate revenue for the proposed reconstruction process.

POLICY DEVELOPMENTS CORNER

- The Directorate General of Foreign Trade released the Draft ITC (HS) Export Policy, 2019 on 23rd May 2019 for public comments. Draft available at https://dgft.gov.in/sites/default/files/Draft_Comprehensive_ITC_(HS)_Export_Policy_2019.pdf

Comments, if any, may be sent to [email protected] at the earliest.

- Disaster management activities including relief rehabilitation and reconstruction activities are part of Schedule 7, Section 135 of the Companies Act that outlines CSR guidelines and the areas where expenditure could be made. This amendment was notified on 30th May 2019 vide GSR 390 E. The Notification is available at

http://www.mca.gov.in/Ministry/pdf/Notification_06062019.pdf

- The Dr. K. Kasturirangan Committee for Draft National Education Policy submitted its report on May 31, 2019. The draft Policy suggests overarching reforms at all levels of education from preschool to higher education. The Public can submit their comments before 30th June 2019 at https://innovate.mygov.in/new-education-policy-2019/

- The Task Force constituted by the Ministry of Finance to review the Income-Tax Act, 1961 will submit its report before 31st July 2019.

Contact id [email protected]

More details available at

https://www.incometaxindia.gov.in/Pages/task-force-on-direct-taxes.aspx

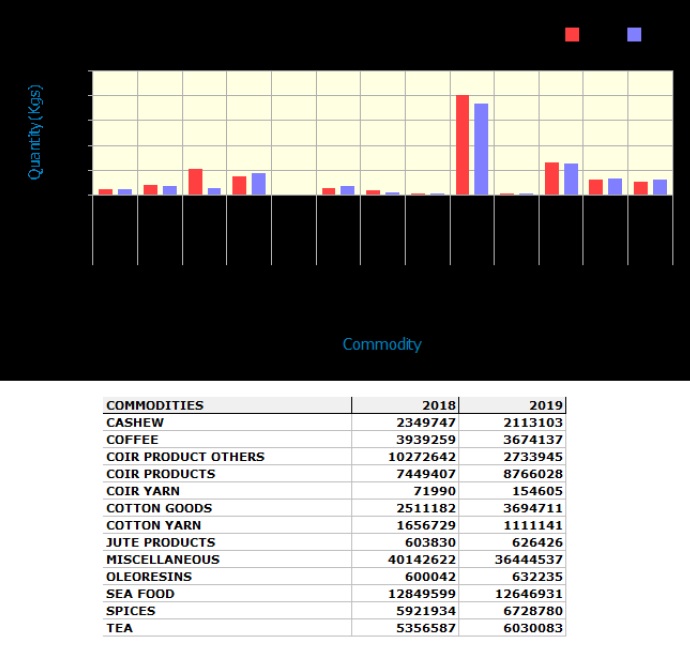

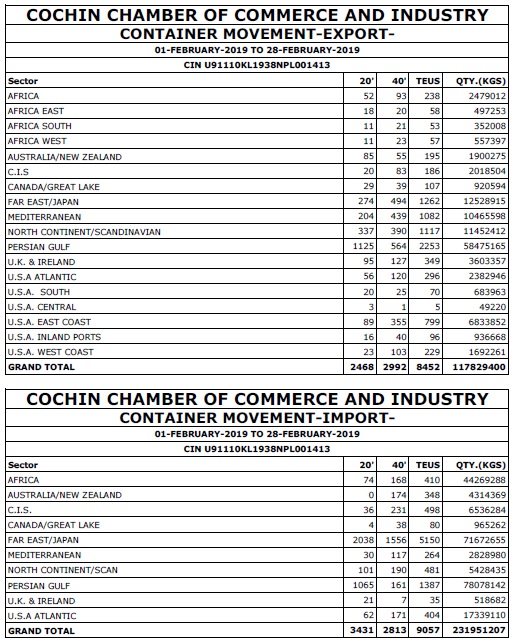

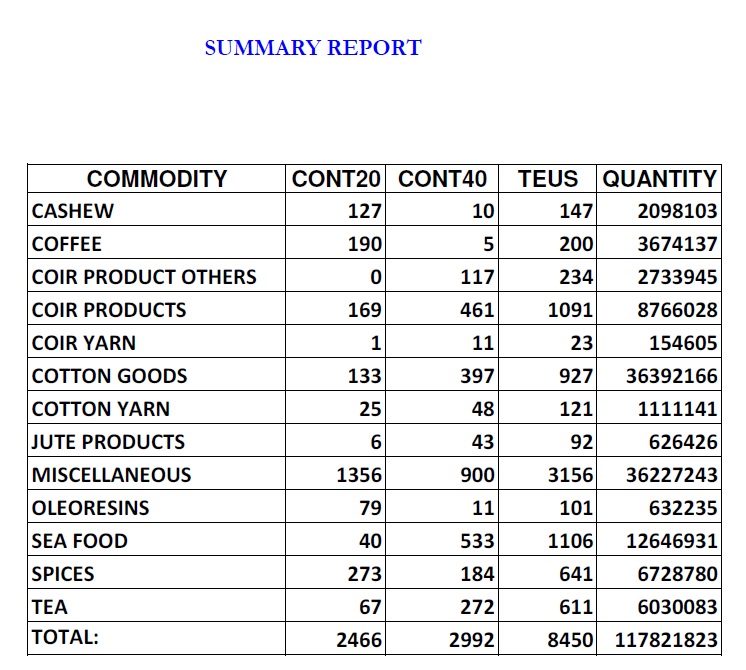

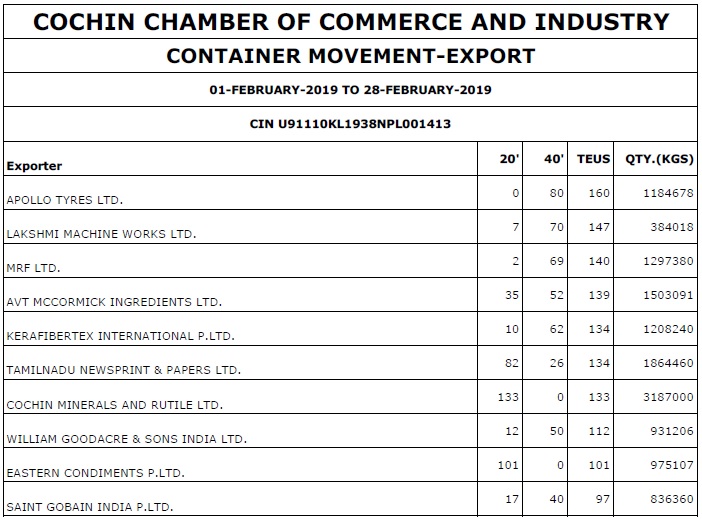

Digital Certificate of Origin

Exclusive EXIM Statistics

Advertise with us