President's Note

Dear Friends,

For over a month now four of the five states of southern India have been major covid hotspots. Kerala, the fifth State, which had apparently flattened the curve by May and was reporting only a gradual increase in cases. But that is no more true. This week, the outbreak in Kerala has intensified, and the State is supposedly considering a fresh lockdown after an 87% rise in active cases in a week. Among all countries with more than 10,000 fatalities, India has the worst weekly growth rate in cases, and at its current pace, could cross the 1.5 million mark by 29 July.

We are certain to face a period of stable deficit and increasing debt while the Government takes measures to deal with them. Unlike any other previous economic downturn, the uncertainty is very unusual. It is mainly about the virus transmission in India and other countries, optimistic medical intervention, effective social distancing and possible future lockdowns, the extent and duration of Government support and survival of physical and human capital through covid-19 regime etc.

The decision on a complete lockdown is pending as Kerala reported community transmission of COVID-19 in its coastal areas. There is a divide in the opinion over a total lockdown. Lockdowns can only help the Government prepare infrastructure required to deal with the situation, whereas the spread of the disease can be controlled only through the effective containment of the infected. Instead of bringing life to a halt through a fresh complete lockdown, preventive measures and other such restrictions should be strengthened and enforced.

Keeping in mind the current economic situation in the State owing to the Covid-19 pandemic, the Chamber has prepared a Memorandum aimed at protecting the economy of Kerala, its trade and industries. The Memorandum emphasizes measures that could revitalize the economy, facilitating a strong and speedy revival at the earliest.

The Union Govt. Vide Notification dated 07.07.2020 has published the Draft Rules on Code on Wages Act, 2019 inviting objections/suggestions from stakeholders. We invite inputs/suggestions from our member organisations to be included in a Representation to be submitted to the Union Government on the proposed policy changes, latest by Friday, 31st July 2020.

Coming to this month’s activities, we organized a Virtual CEO Forum Meeting on 3rd July 2020. Mr. Deepak Varghese, Head-Client Relations of IIFL Wealth & Asset Management, Kerala was the Speaker at this Session and he spoke on “Wealth Management – Approach and a Perspective. The session was well appreciated by all the participants.

On 6th July, we organised an Online Session on Business and Contracts: Pandemic Impact and Future. Mr. Prashanth S. Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers) Bangalore and Ms. Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers) Bangalore were the Speakers at the session. The session covered topics like the role of negotiations and evaluation of key terms, Sector-wise impact analysis of contracts, Digitization of contracts, Data privacy considerations, Business continuity, and contingency provisions, etc.

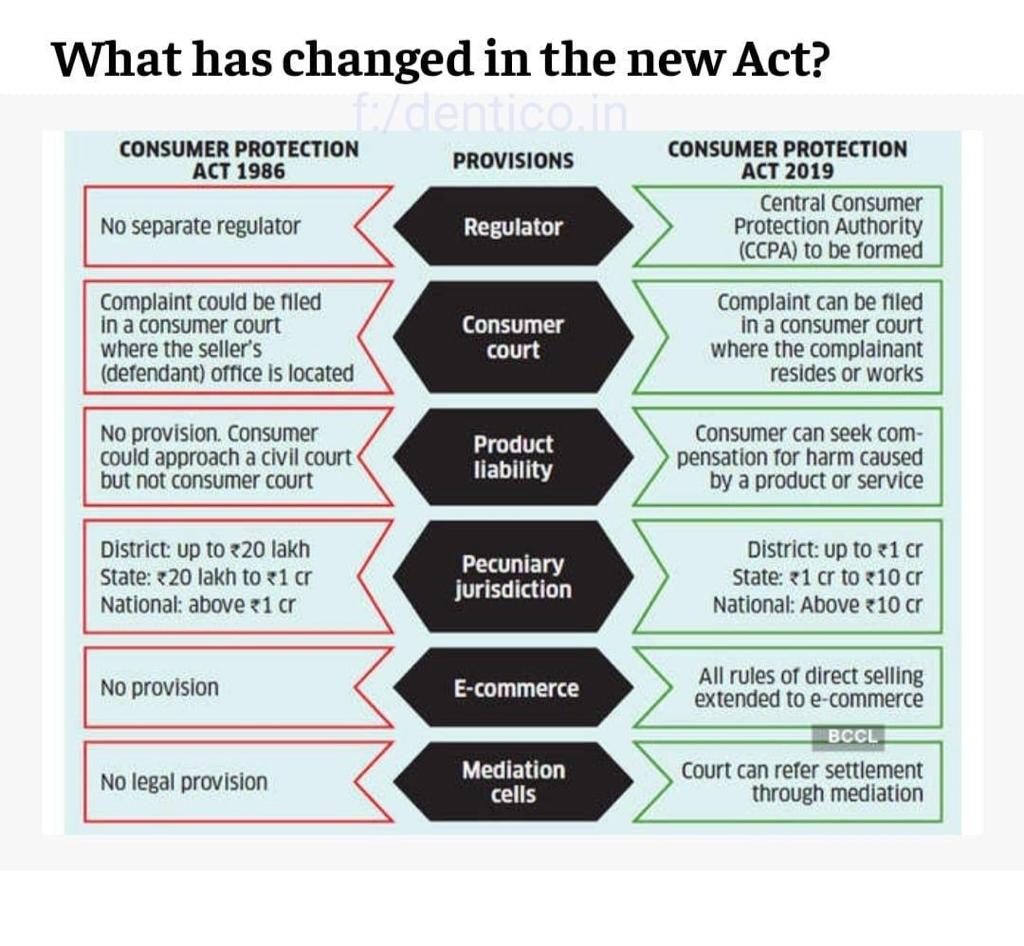

Consumer Protection has taken a big leap forward in the form of Consumer Protection Act, 2019. The new law which came into force on July 20, 2020, now draws attention to e-commerce activities, stricter and harsher penalties, additional dispute resolution mechanisms, and much more.

The Chamber will be conducting a virtual meeting on ‘Consumer Protection 2.0’ on August 5, 2020. Mr. Prashanth Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers) and Ms. Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers), will speak on the changes, nuances and the new measures that are to be taken by both buyers and sellers.

The next Virtual CEO Forum Meeting will be on “The Emerging Economic Opportunities in the post-Covid Scenario” to be addressed by Sri. APM Mohammed Hanish I.A.S, Principal Secretary ll, Department of Industries and Commerce, Government of Kerala on 8th of August 2020 on the Google Meet Platform. I trust you all will attend the session.

The virus crisis has started to change society. Currently, all abstract attention of most of us is engaged in predicting the possible trajectory of the ongoing pandemic. With the newly developed understanding that Covid-19 is here to stay for months and no vaccine is likely to be available for wider use before the middle of next year, the strategies to respond to the pandemic need to be upon effective implementation of public health and social measures and improved community engagement. Let us all contribute our mite in this endeavour.

Stay Safe Everyone!!!

V Venugopal

Quote

Fine Points

Chamber Vlogs!

The Chamber Vlog Series has been widely appreciated by our members and well-wishers since the first release in May 2020. The Chamber would like to thank you all for your support and hope to receive more in future.

We hope that you find our videos useful and informative. To view all the videos please go to the Cochin Chamber’s YouTube Channel. The most recent ones are added to the video players below. We will keep uploading new and relevant content for our members and the industry in general.

Kindly share these videos with your networks and subscribe to our YouTube Channel for more informative content.

Chamber Vlog - 11

The importance of maintaining Mental Health

Chamber Vlog - 12

Petrol & Diesel Prices - An Analysis

Chamber Vlog - 13

Managing the Workforce during the Pandemic

Chamber Vlog - 14

Lockdown is not a Solution to the spreading of Covid 19

Recent Events

CEO FORUM - 2020 | Virtual Meeting | 03.07.2020

Wealth Management - Approach and a Perspective

The Cochin Chamber of Commerce and Industry conducted a Virtual CEO Forum Meeting on Friday, 3rd of July, 2020.

Mr. Deepak Varghese, Head-Client Relations of IIFL Wealth & Asset Management, Kerala was the Speaker at the meeting and spoke on “Wealth Management – Approach and a Perspective.”

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

Mr. Varghese gave a brief introduction about wealth management and said that it is more than just investment advice, as it can encompass all parts of a person’s financial life. Rather than trying to integrate pieces of advice and various products from a series of professionals, high net worth individuals benefit from a holistic approach in which a single manager coordinates all the services needed to manage their money and plan for their own or their family’s current and future needs, he said.

Mr. Varghese said that while the use of a wealth manager is based on the theory that he or she can provide services in any aspect of the financial field, some choose to specialize in particular areas. This may be based on the expertise of the wealth manager in question, or the primary focus of the business within which the wealth manager operates.

He also explained the role of a wealth manager in detail and said that a wealth manager starts by developing a plan that will maintain and increase a client’s wealth based on that individual’s financial situation, goals, and comfort level with risk. After the original plan is developed, the manager meets regularly with clients to update goals, review and rebalance the financial portfolio, and investigate whether additional services are needed, with the ultimate goal being to remain in the client’s service throughout their lifetime.

Mr. Varghese briefly explained the setting up of an investment policy, portfolio creation, portfolio MIS and reporting, and portfolio analytics. He also threw some light on estate planning, credit solutions, and alternate investment opportunities.

Mr. Varghese spoke on the opportunities that have emerged in the structured credit space as the current environment is enabling managers to negotiate for better yields with strong collaterals and securities in place. He also mentioned that the inflation trajectory is expected to move downward with moderation in food prices, lower crude prices, and subdued demands.

Mr. Varghese also shared updates on the real estate front and mentioned that the Indian Commercial Sector has been on a growth trajectory with the corporate expansions led space attaining a peak in 2019. Covid-19 has severely hit the residential real estate business and the sector has come to a standstill with a complete halt to site visits, discussions, documentation, and closures.

Following Mr. Varghese’s talk there was a brief question and answer session wherein the Speaker clarified the issues raised by the participants.

The meeting ended with the Vice President of the Chamber, Mr. K Harikumar thanking everyone for having participated in the meeting.

Online Session | 06.07.2020

Business and Contracts: Pandemic Impact and Future

The Cochin Chamber of Commerce and Industry organised an Online Session on “Business and Contracts: Pandemic Impact and Future!” on Monday, 6th July 2020 on the Google Meet Platform.

Mr. Prashanth S. Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers) Bangalore and Ms. Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers) Bangalore were the Speakers at the meeting.

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

Commencing the session Mr. Prashanth said that one of the major concerns which emerged out of the standstill position on account of Covid 19 is whether businesses will ever go back to ‘normalcy’ and whether parties will continue to perform their obligations as agreed under the contracts entered earlier. This situation, he said, has led to several discussions around whether this pandemic will be treated as an ‘Act of God’ or ‘Force Majeure’ event, to excuse a party for non-performance of the contract or has frustrated the contract rendering it impossible or impractical to perform. He said that in modern business practice, Force Majeure clauses are generally embodied in the form of contractual provisions, agreed upon between parties, to excuse non-performance of the contract in cases of events beyond their control – such as an Act of God, natural calamities, war, labour unrest, epidemics, pandemics, etc. If the words epidemic or pandemic are used in the Force Majeure clause, then in all likelihood, the Force Majeure clause is triggered under the contract with the declaration of COVID—19 as a pandemic.

Mr. Shivadass said that with an increase in e-commerce and online transactions, the number of contracts being executed electronically has seen exponential growth and the ongoing COVID -19 crisis will further increase the execution of contracts electronically. The test and validity of an e-contract in India still encompass the pre-requisites of a contract as enumerated in the Indian Contract Act, 1872. It is pertinent to note that without an adequate legal framework, the implementation of e-contracts over traditional contracts may create an atmosphere of entropy. Further, the introduction of Section 65B to the Indian Evidence Act, 1872, and the enactment of the Information Technology Act, 2000 have enlarged the recognition of e-contracts under the law, he added.

Mr. Shivadass then explained certain things that an Organization must follow… like fair information practice principles, reasonable data processing, maintaining data transparency, maintaining storage limitations with exceptions, maintaining the data quality, etc. He said that an Organization must have an internal grievance cell for data within an Organization and the Grievance Officer must ascertain the gravity of a complaint.

Speaking thereafter, Ms. Joy explained the data protection law and data privacy and said that extraterritoriality norms have been made stricter for processing and storage of personal and sensitive data under the Data Protection Bill. She said that the last resort for entities dealing with economic distress from business disruptions due to Covid is termination and also spoke about the termination rights under contracts in detail.

Ms. Joy listed out the areas where businesses should pay extra attention such as vetting of new suppliers, contracts with aggregators to be strengthened in light of e-commerce, evaluating key commercial contracts, checking the terms of existing contracts for protection, including force majure clauses, examining the termination conditions and procedures in the contract in case if you are considering terminating the agreement or think the other party might, etc.

Following this, there was a brief question and answer session wherein the Speakers clarified the issues raised by the participants.

The meeting concluded with the Deputy Secretary of the Chamber, Mr. Manu Varghese thanking everyone for having participated in the meeting.

Article

SECTION 241 AND 242 APPLICATION & WAIVER UNDER SECTION 244 UNDER COMPANIES ACT, 2013

Priyanka Yavagal - Advocate - Shivadass & Shivadass (Law Chambers)

The Supreme Court in its recent judgement dated July 6, 2020, in the case of Aruna Oswal Vs. Pankaj Oswal & Ors., deliberated upon the much discussed ‘waiver’ proviso under Section 244 of the Companies Act, 2013 (‘Act’), for bringing an application under Sections 241 and 242 of the Act before the National Company Law Tribunal (‘NCLT’).

Background:

During the lifetime of Late Mr. Abhey Kumar Oswal, he held 5,35,3,960 shares in M/s. Oswal Agro Mills Ltd., a listed company. Before his demise, Mr Abhey Kumar Oswal documented a nomination in favour of his wife, Mrs, Aruna Oswal as per section 72 of the Act. In the said nomination was to supersede any other assignment or document made by Mr. Oswal prior to his death. This would entitle Mrs. Oswal to be the absolute registered holder of the shares held by her deceased husband.

Mr. Oswal’s son, Mr. Pankaj Oswal, preferred a partition suit claiming entitlement to 1/4th of the estate of Mr. Abhey Kumar Oswal i.e., 39.88% in M/s. Oswal Agro Mills. Ltd., and 11.11% in M/s. Oswal Greentech Ltd, its sister concern.

During the pendency of the aforesaid suit, Mr. Pankaj Oswal (‘Respondent’), filed a Company Petition alleging oppression and mismanagement in the affairs of M/s. Oswal Agro Mills Ltd., and M/s. Oswal Greentech Ltd. In the said petition, the Respondent, in order to qualify for the minimum threshold stated that he holds 0.03% shareholding and has a ‘legitimate expectation’ to hold 9.97% shareholding M/s. Oswal Agro Mills Ltd., by virtue of being the son of Mr. Oswal. This was also a subject matter of the dispute in the partition suit.

While things stood thus, the NCLT, after a round robin proceeding before the National Company Law Appellate Tribunal (‘NCLAT’), via order dated November 13, 2018, dismissed the application holding the Respondent was the legal heir of Mr. Oswal and was entitled to 1/4th share of the estate. Three appeals were preferred before the NCLAT which were dismissed via order dated November 14, 2019. When an appeal was filed before the Supreme Court, an opportunity was granted to the parties to amicably settle the matter, however, since no settlement was arrived at, the matter was heard on merits.

CONTENTIONS BEFORE THE SUPREME COURT:

The following contentions were placed before the Supreme Court by the Appellant:

- The Respondent lacked requisite shareholding of 10% of total issued, paid-up and subscribed capital of the company to be eligible to file a petition under Section 241 and 242 of the Act as mandated under Section 244 of the Act;

- The Respondent also did not involve himself with the active day to day management of the Company;

- The matter relating to inheritance is a civil matter pending before the relevant forum and therefore could not have been adjudicated by the NCLT;

- The waiver requirement was also not pleaded anywhere by the Respondent;

- Filing successive petitions at different forums amounts to forum shopping and abuse of process of law.

On the other hand, the Respondent contended as under:

- It is permissible for a legal representative to maintain proceedings for oppression and mis-management in the affairs of the Company though his / her name is not entered as the registered owner of shares;

- The waiver requirement to hold 10% shares had been pleaded by the Respondent in the company petition filed by him;

- The partition suit’s pendency could not have come in the way of maintaining the application concerning oppression and mis-management, as only civil rights have to be determined in the suit. The Company petition to that extent is maintainable.

OBSERVATIONS OF THE SUPREME COURT:

The Supreme Court while considering the appeal, among others, ruled on the ‘waiver’ proviso under Section 244 of the Act. The Supreme Court observed that the Respondent does not hold the requisite minimum number of shares i.e., (10%), as specified under Section 244 of Act to pursue an application under Sections 241 and 242. Though the Respondent has bought holding of 0.03% in M/s. Oswal Agro Mills Ltd. after filing a civil suit, the remaining 9.97% is in sub-judice. In M/s. Oswal Greentech Ltd., the shareholding of deceased was 11.11%, out of which only 1/4th shares have been claimed by the Respondent. The question as to right title and interest needs to be adjudicated by the relevant forum before whom the matter is pending, alone.

The Supreme Court also observed that the Respondent was not involved in the day to day functioning of the Company since he had an independent business in Australia.

Therefore, the basis of arriving at the minimum threshold for filing an oppression and mis-management petition before the NCLT i.e., holding 0.03% shareholding and claiming 9.97% as inheritance, is not maintainable. Further, the NCLT does not have the power to adjudicate on the latter issue. The Respondent also does not represent the body of shareholders holding requisite percentage of shares in the Company, necessary to maintain the petition.

The Supreme Court also observed that the petition under Sections 241 and 242 of the Act, pending before the NCLT must be dismissed with liberty to file afresh in case the civil suit is decreed in favour of the Respondent and the shareholding of the Respondent is increased to the extent of 10% as required under Section 244 of the Act.

*The author is an Advocate with Shivadass & Shivadass (Law Chambers)

The contents and comments of this document do not necessarily reflect the views/position of Shivadass and Shivadass (Law Chambers) but remain solely of the author(s). For any further queries or follow up, please contact [email protected].

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

The Central Government further extends timelines specified under the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020

In the wake of the COVID–19 pandemic, the President of India promulgated the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020, (the Ordinance) on 31 March 2020, providing inter alia relaxations in certain timelines specified under the Income-tax Act, 1961 (the Act), and certain other laws. As per the aforesaid Ordinance, several statutory timelines falling due between the period 20 March 2020 to 29 June 2020 were extended to 30 June 2020.

Further, to these announcements, the Central Government has issued a notification , along with a Central Board of Direct Taxes (CBDT) Press Release, which seeks to further extend certain statutory timelines. Vide this notification 1 , compliances [as referred in section 3(1) of the Ordinance such as, completion of proceedings, passing of order, issuance of notices, filing of appeals etc.] falling between 20 March 2020 to 31 December 2020 have been extended to 31 March 2021, subject to certain carve-outs mentioned in the notification1, tabulated as follows:

*These measures were announced by the Finance Minister under the ‘Atmanirbhar Bharat Package’ on 13 May 2020.

This notification shall come into force from 30 June 2020.

CBDT grants relief to certain share transactions consummated below “fair value”

Background

The Indian Income-tax Act, 1961 (the Act) provides for levy of tax in certain cases where a transaction involving shares takes place at a price lower than its fair market value (FMV). For instance, if there is a transaction involving sale of shares, it could have the following consequences on the seller and the buyer:

- In the hands of the seller (applicable only for sale of unquoted shares): The FMV would be deemed as the sale consideration for computing the capital gains tax (section 50CA of the Act).

- In the hands of the buyer: The difference between the FMV and acquisition price would be taxable as “income from other sources” (section 56(2)(x) of the Act).The Finance (No.2) Act, 2019, empowered the Central Board of Direct Taxes (CBDT) under sections 50CA and 56(2)(x) of the Act to prescribe class of persons for which the above provisions would not apply.

In this regard, the CBDT has issued two notifications , amending Rule 11UAC and introduced Rule 11UAD in the Income-tax Rules, 1962, (the Rules) to prescribe certain cases that involve transfer/ acquisition of shares, where the above mentioned provisions would not apply.

Changes introduced

The changes introduced by the notifications4 are summarised as follows:

* Sections 56(2)(x) and 50CA of the Act would not apply to the transferor and shareholder receiving unquoted shares if all the following conditions are fulfilled:

- The Central Government has moved an application against a company before the National Company Law Tribunal (NCLT) under section 241 of the Companies Act, 2013;

- Based on the application, the NCLT has suspended the board of directors of the company and appointed new directors nominated by the Central Government under section 242 of the Companies Act, 2013;

- A reasonable opportunity of being heard is given to the jurisdictional Principal Commissioner/ Commissioner of Income-tax;

- Resolution plan is approved by the NCLT; and

- The transferor transfers/ shareholder receives unquoted shares of the company and its subsidiary and the subsidiary of such subsidiary pursuant to the resolution plan so approved.

For the purposes of the above, a company would be a subsidiary of another company, if such other company holds more than half in nominal value of the equity share capital of the company.

* Section 56(2)(x) of the Act would not apply to receipt of shares by an investor/ investor bank if all the following conditions are fulfilled:

- The shares are allotted under the Yes Bank Limited Reconstruction Scheme, 2020 (Scheme) notified by the Ministry of Finance; and

- The shares are allotted at a price specified in the Scheme.

As the above envisages a transaction of issue of shares, the provisions of section 50CA of the Act should not be relevant. The above changes are applicable retrospectively from 1 April 2019 (i.e., assessment year 2020-21 onwards).

PwC comments: As per the Memorandum to the Finance (No.2) Bill, 2019 the amendments empowering the CBDT were introduced to facilitate resolution of stressed companies. It was explained that considering the FMV (determined as per the Rules) could result in genuine hardship in case of transactions where certain authorities approve the consideration for transfer of shares and the person transferring such shares has no control over its determination.

In line with the above intent, the CBDT has issued the notifications4 giving relief from the levy of income-tax in case of resolution of stressed companies under specific scenarios described therein. The CBDT seems to have adopted a taxpayer-friendly stance towards the resolution of stressed companies where the resolution has been either initiated by the Central Government keeping the public interest in mind (cases involving oppression or mismanagement) or is a special case like that of Yes Bank Limited.

Delhi bench of the Tribunal allows deduction as bad debt, of income wrongly offered to tax in earlier year as capital gains but not recovered

The Delhi bench of the Income-tax Appellate Tribunal (Tribunal) upheld the write-off of non-recoverability of subsidiary share sale proceeds as bad debt, although the corresponding income was taxed under the head capital gains in the earlier year. Relying on judicial precedents, the Tribunal reiterated that if in an earlier assessment year, a taxpayer has offered and the tax officer (TO) has assessed the income under a particular head of income, although the same was liable to be assessed under a different head of income, there is no embargo on the taxpayer or TO to consider income from the same source under the correct head in a subsequent year.

PwC comments: The judgment reiterates the principle that the taxpayer offering any income under a particular head of income in one year cannot act as an estoppel against the taxpayer in a subsequent year to claim that income taxable under a different head of income. It further held that the TO of the subsequent year must determine whether the loss of the previous year may be set off against the profits of that year.

Supreme Court dismisses Revenue’s SLP against income from sale of land, held as an investment by a developer, being upheld as capital gains.

The Supreme Court of India dismissed the Revenue authorities’ Special Leave Petition (SLP) challenging the judgement of the Bombay High Court, wherein it was held that income arising on sale of land held as an investment by the taxpayer, being a developer, was chargeable to tax under section 45 of the Income-tax Act, 1961.

PwC comments: While the Supreme Court dismissed the Revenue’s SLP with a non-speaking order, the fact pattern of the case was the key determinant. Accordingly, one would have to emphasize the taxpayer’s intent, factual aspects and documentation to determine the tax implications in such cases. Note also that the statute has been subsequently amended to tax such conversion of business asset into capital asset.

Regulatory

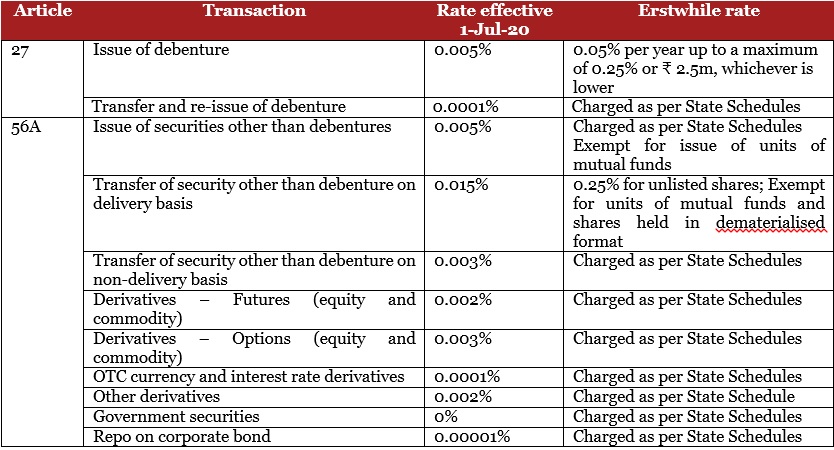

Stamp duty on securities transactions effective from 1 July 2020

The Finance Act, 2019, had introduced certain amendments in the Indian Stamp Act, 1899, to streamline the levy and collection of stamp duty on securities transactions. The Ministry of Finance notified the Indian Stamp (Collection of Stamp Duty through Stock Exchanges, Clearing Corporations and Depositories) Rules, 2019, on 10 December 2019, to regulate the centralised mechanism for the collection of stamp duty across the country. These amendments have come into force with effect from 1 July 2020.

Background

The relevant provisions of the Finance Act, 2019, amending the Indian Stamp Act, 1899 (the Act) and the Indian Stamp (Collection of Stamp-Duty through Stock Exchanges, Clearing Corporations and Depositories) Rules, 2019 (the Rules) were notified together on 10 December 2019 which were to come into force from 9 January 2020.

However, the Ministry of Finance, vide notifications dated 8 January 2020, extended the effective date to 1 April 2020, and vide notification dated 30 March 2020, further extended the effective date to 1 July 2020. This Regulatory Insight summarises the provisions of the Act as amended by the Finance Act, 2019 and the Rules, as applicable to securities transactions.

Amendments effective from 1 July 2020

Instruments of securities liable to stamp duty

* The definition of debentures has been inserted such that “debenture” includes –

- Debenture stock, bonds or any other instrument of a company evidencing a debt, whether constituting a charge on the assets of the company or not;

- Bonds, in the nature of debentures issued by any incorporated company or body corporate;

- Certificate of deposit, commercial usance bill, commercial paper and such other debt instrument of original or initial maturity up to one year, as the Reserve Bank of India (RBI) may specify from time-to-time;

- Securitised debt instruments; and

- Any other debt instruments specified by the Securities and Exchange Board of India (SEBI) from time-to-time.

* “Debenture” has been excluded from the definition of “bonds.” This exclusion ensures that stamp duty on “debentures” is chargeable only under any Article 27 (Union list) of the Constitution of India and not under the classification of “bonds.”

* The definition of securities has been widened to include –

- Securities, as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 (SCRA Act);

- A “derivative,” as defined in clause (a) of section 45U of the RBI Act, 1934;

- A certificate of deposit, commercial usance bill, commercial paper, repo on corporate bonds and such other debt instruments of original or initial maturity up to one year, as the RBI may specify from time-to-time; and

- Any other instrument declared by the Central Government, by notification in the Official Gazette, to be securities for the purposes of this Act.* The definition of the term “instrument” has been widened by including in its ambit, a document, electronic or otherwise, created for a transaction in a stock exchange or depository by which any right or liability is, or purports to be, created, transferred, limited, extended, extinguished or recorded.

Valuation mechanism

* Stamp duty is to be levied on the market value of a stock or security. The definition of market value provides as follows:

In relation to an instrument through which –

- Any security is traded in a stock exchange, means the price at which it is so traded;

- Any security that is transferred through a depository but not traded in stock exchange, means the price or the consideration mentioned in such instrument;

- Any security dealt otherwise than in the stock exchange or depository, means the price or consideration mentioned in such instrument.

* In the absence of a specific provision for market value in case of transfers without consideration, it seems that such transactions would not be subject to stamp duty in the absence of any other instrument of transfer. The Government of India has issued frequently asked questions (FAQs) for the implementation of amendments in the Act and the Rules made thereunder. Questions 15 and 24 of the FAQs clarify that no stamp duty is payable in relation to transactions without consideration, i.e., gift, bonus shares, transmission of securities, etc.

* In the following cases, the market value for computation of stamp duty is as under:

- In case of Options in any securities: premium paid by the buyer;

- In case of Repo on corporate bonds: interest paid by the borrower; and

- In case of Swap: only the first leg of cash flow, i.e., in a swap agreement, the notional/ gross value of the contract for the buyer.

Levy of stamp duty

- The newly inserted sections 9A and 9B of the Act consolidate the stamp duty provisions relating to the issue, sale or transfer of securities.

- The instrument on which stamp duty is chargeable under section 9A of the Act shall be the principal instrument for the levy of stamp duty, and no stamp duty shall be charged on any other instruments relating to the said transaction.

- The new section 8A provides levy of stamp duty in relation to the transfer of dematerialised securities and units of mutual funds between beneficial owners. The transfer of securities from a person to a depository (dematerialisation) or from a depository to a person (rematerialisation) shall continue to be exempt.

- A quick glance of the changes to the stamp duty rates are provided in the below table:

- There has been significant reduction in stamp duty on certain transactions. For example, stamp duty on the transfer of unlisted shares is now reduced from 0.25% to 0.015%. In addition, stamp duty on allotment of shares is now 0.05%, which was 0.1% in certain States.

Stamp duty payment

- In the absence of an agreement to the contrary, the person responsible for the payment of stamp duty in case of different transactions is described in the below table.

Stamp duty collection mechanism

- The provisions prescribe the centralised collection and payment mechanism of stamp duty by stock exchanges, clearing corporations and depositories (collecting agents).

- The collecting agents for certain transactions provided in the below table.

* For the sale of any securities through the stock exchange, including the sale of any listed units of any registered pooled arrangements or scheme or tripartite repo –

- Stamp duty shall be collected on the settlement day;

- For transactions reported to a stock exchange, stamp duty shall be collected on the entire sale consideration when the transfer is reported, even if the consideration is paid in part or in instalments to be paid in future. However, if reporting is by the depository, and such depository has collected stamp duty and informed about it, the stock exchange should not collect stamp duty on such transactions;

- The sale consideration reported to a stock exchange shall be considered as the actual sale value;

- In case of interoperability of clearing corporations, the trades of a client across the stock exchanges shall be considered for determining whether they would result in a delivery or not.* For transfer of securities for consideration made by a depository otherwise than through a stock exchange –

- Stamp duty has to be collected before the execution of all off-market transfers involving the transfer of securities in the depository system. This includes over-the-counter trades occurring in dematerialised or electronic form;

- In case of transfer of securities pursuant to the invocation of a pledge, duty shall be collected from the pledgee on the market value of securities.* On the issue of securities leading to creation or change in records of the depository –

- Stamp duty shall be collected from the issuer before executing any transaction in the depository system;

- Stamp duty shall not be collected on the creation or destruction of securities on account of corporate actions such as stock split, consolidation, mergers and acquisitions, or such similar actions, if it does not involve change in beneficial ownership. Provided there is fresh issue to an investor as part of a corporate action, such issuance shall be subject to stamp duty.

- The collecting agent shall round off the stamp duty to the nearest rupee and transfer it to the account of the concerned State Government, with the RBI, or any specified scheduled commercial bank.

- Within three weeks of its collection, stamp duty collected is to be transferred to the State Government where the buyer resides. If the buyer is located outside India, the stamp duty is to be transferred to the State where the trading member/ broker of the buyer is located. If there is no such trading member, it needs to be deposited to the State Government having the registered office of the participant.

- Collecting agents may deduct 0.2% of the stamp duty collected as facilitation charges before transferring it to the concerned State Government.

- The collecting agent will submit a monthly stamp duty return along with the list of defaulters in the prescribed manner, within seven days of the succeeding month. An annual return is also required to be filed on or before 30 June of the immediately following financial year.

Potential impact

- Multiple incidences of taxation are prevented, as States shall not collect stamp duty on any secondary record of transaction associated with a transaction on which the depository/ stock exchange has been authorised to collect the stamp duty.

- The burden of stamp duty costs in certain transactions, such as transfer of securities on non-delivery basis and derivatives, has reduced, as stamp duty is now levied only on one side (either on the buyer or the seller but not on both) instead of being levied on both seller and buyer.

- The incidence of stamp duty has been reduced in many segments, such as the issue of shares, debentures, transfer of shares not in dematerialised format, transfer of debentures (including re-issue), etc. This shall aid capital formation and promote the corporate bond market.

- Investors should be cognisant of stamp duty implications on transactions involving units of mutual funds and alternative investment funds.

- The standardisation of levy and collection mechanism shall avoid tax arbitrage for the issue or re-issue or sale or transfer of securities happening outside stock exchanges and depositories.

- This system will help develop equity markets and equity culture across the length and breadth of the country,

- ushering in balanced regional development.

- This rationalised and harmonised system through the centralised collection mechanism is expected to minimise the cost of collection and enhance revenue productivity.

PwC comments: The amendments made effective from 1 July 2020 will lead to a standardised stamp duty regime for securities transactions. This is a welcome step towards a robust and well-defined framework for securities transactions in India.

Central Government notifies criteria for classification and procedure for filing of memorandum by MSMEs

The Central Government, after obtaining the recommendations of the Advisory Committee, has notified certain criteria for classifying enterprises as micro, small and medium enterprises (MSMEs) and specifying the form and procedure for filing the memorandum (hereafter in this notification to be known as Udyam Registration), with effect from the 1 July 2020.

The Government had notified the criteria for classification of MSMEs vide notification dated 1 June 2020.

The Government has now superseded the said notification and have now released a composite notification on June 26, 2020, carrying the specification and the form and procedure for filing the memorandum to register as a MSME (also known as “Udyam Registration”).

The criteria for classification as MSME are discussed below.

A. Classification of enterprise

- Micro enterprise: Investment in plant and machinery or equipment does not exceed ₹ 10m and turnover does not exceed ₹50m;

- mall enterprise: Investment in plant and machinery or equipment does not exceed ₹ 100m and turnover does not exceed ₹ 500m; and

- Medium enterprise: Investment in plant and machinery or equipment does not exceed ₹ 500m and turnover does not exceed ₹ 2500m.

B. Composite criteria of investment and turnover

- A MSME shall meet the revised criteria of both the investment and turnover limits specified.

- Any breach of the limits in either investment or turnover criteria will classify the entity in the next category.

- No enterprise will be placed in the lower category unless it goes below the ceiling limit specified for its present category in both the criteria of investment and turnover.

All units with goods and services tax number against the same permanent account number (PAN) will be collectively treated as one enterprise and the investment and turnover limit will be calculated considering the aggregate value of all such enterprises

C. Calculation of investment in plant and machinery or equipment

- Previous years Income-tax Return (ITR) filed under Income-tax Act, 1961 (the Act), will be considered for calculation of investment in plant and machinery or equipment.

- In case of a new enterprise, self-declaration by the promoter will be considered, which will be valid until 31 March of the financial year in which it files it first ITR.

- The definition of plant and machinery or equipment will be considered as prescribed under the Income-tax Rules, 1962 and it will include all tangible assets (other than land and building, furniture and fittings).

D. Calculation of turnover

- Exports of goods or services or both is excluded while calculating the turnover.

- Details of turnover and exports turnover for an enterprise shall be linked to the Act or the Central Goods and Services Act, 2017 (CGST Act) and the GSTIN.

- Turnover details of entities that do not have PAN will be considered on self-declaration basis until 31 March 2021, and thereafter, such enterprise shall mandatorily obtain PAN and GSTIN.

E. Registration of new enterprise

- Registration can be obtained basis the self-declaration with no requirement to upload documents, papers, certificates or proof.

- On registration, the enterprise will be issued an e-certificate (Udyam Registration Certificate).

- Only one registration will be allowed to the enterprise and any additional activities undertaken by the entity will be allowed to be incorporated in the existing registration.

- Aadhar number is mandatory for the registration of an enterprise.

F. Registration of existing enterprises

- All existing enterprises registered under EM–Part-II or UAM shall register again on the Udyam Registration portal on or after 1 July 2020.

- The existing registration is valid until 31 March 2021.

- All enterprises registered until 30 June 2020, shall be re-classified in accordance with the revised notification dated 26 June 2020.

- An enterprise registered with any other organisation under the Ministry of Micro, Small and Medium Enterprises, shall register itself under Udyam Registration.

G. Updating of information and transition period in classification

- In case of an upward change in the terms of investment in plant and machinery or equipment or turnover, or both, and consequent re-classification, an enterprise will maintain its prevailing status until the expiry of one year from the close of the year of registration.

- In case of reverse-graduation of an enterprise, whether as a result of re-classification or because of actual changes in investment in plant and machinery or equipment or turnover, or both, and whether the enterprise is registered under the Act or not, the enterprise will continue in its present category until the closure of the financial year. It will be given the benefit of the changed status only with effect from 1 April of the financial year following the year in which such change took place.

PwC comments: All existing registered MSMEs and new enterprises seeking to register as micro, small or medium enterprises will have to comply with the revised classification norms and registration process.

Amendments to the Insolvency and Bankruptcy Code

The Insolvency and Bankruptcy Code, 2016 (IBC), has been amended on 5 June 2020 pursuant to the promulgation of the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2020 (Ordinance). The Ordinance has made the following changes to the IBC.

Suspension of IBC

A new section 10A is inserted in the IBC, which provides that –

- No application for initiation of corporate insolvency resolution process (CIRP) of a corporate debtor (CD) shall be filed, for any default arising on or after 25 March 2020. This suspension is applicable for a period of six months or such further period, not exceeding one year from such date, as may be notified in this behalf.

- No application shall ever be filed for initiation of CIRP of a CD for the said default occurring during the said period.

- These provisions shall not apply to any default committed before 25 March 2020.

Relaxation from wrongful trading

A new sub-section (3) under section 66 of the IBC has been introduced to provide that the resolution professional shall not file an application under section 66(2) of the IBC in respect of such defaults against which the initiation of CIRP is suspended under the section 10A.

Indirect Tax

Phased roll out of faceless e-assessment in customs

“Turant Customs” is one of the key initiatives of the Central Board of Indirect Taxes and Customs (CBIC) towards faster clearance, transparent decision making and ease of doing business. To support this initiative, the CBIC has taken numerous steps for the self-registration of goods by importers, automated clearances of bills of entry (BoE), digitisation of customs documents, paperless clearance, etc., thereby easing customs clearances.

As the next step under the initiative, the CBIC has now rolled out the concept of faceless e-assessment in customs. Since mid-2019, the pilot programme of faceless e-assessment, covering specific goods falling under chapters 39, 50 to 71, 72 to 83, 84, 85, 86 to 92 of the Customs Tariff Act, 1975 (the Act), has been undertaken in Chennai, Delhi, Bengaluru, Gujarat and Visakhapatnam.

Basis the evaluation of the pilot programme, in February 2020, the CBIC released a concept paper on faceless e-assessment for comments/ responses from trade/ stakeholders. The CBIC considered the comments/ inputs in revisiting the modalities and processes of faceless e-assessment for pan-India roll out by December 2020.

However, as faceless e-assessment is a complete departure from the present assessment practices, trade and other stakeholders need time to adapt to the new system without impacting operations. Hence, a phased implementation of faceless e-assessment will be undertaken, starting with the ports that were part of the earlier pilot programme.

Guidelines, including amendments in regulations for the phased roll out of faceless e-assessment, are outlined in Notification Nos. 50/ 2020-Customs (NT) and 51/2020-Cus (NT) read with Circular No. 28/2020-Cus and Instruction No. 9/2020-Cus dated 5 June 2020.

The key features of the phased rollout of the faceless e-assessment are discussed below.

Framework of faceless e-assessment

- Phased roll out to commence from 8 June 2020 at Bengaluru and Chennai ports for imports covering Chapters 84 and 85 of the Act. The Customs Automated System (CAS) will assign the non-facilitated BoE filed for imports of goods under Chapters 84 and 85 of the Act, at any of the customs stations at Bengaluru and Chennai to the officers of the concerned Faceless Assessment group (FAG) on a first-cum-first basis for assessment. For this, suitable amendment is affected in the regulations enabling an assessing officer, who is physically located in a particular jurisdiction, to assess a BoE pertaining to imports made at a different customs station, whenever such a BoE is assigned by the CAS.

- The FAG, one each for Chapters 84 and 85 of the Act, will comprise of Appraisers/ Superintendents and Assistant Commissioners/ Deputy Commissioners of Bengaluru and Chennai Customs Zone. They will undertake verification of assessment of any BoE assigned by the CAS. Initially, the officers from the existing Appraising Groups for Chapter 84 and 85 of the Act in each customs station will form part of the FAG, depending upon the volume of BoE to be processed.

- The present appraising groups located in each port will function as Port Assessment Groups (PAGs) and verify the assessment and other related functions, as is the normal practice. The PAGs will handle all other functions pertaining to the BoE that are not marked to the FAG by the CAS and the BoE that are referred by the FAG in specific cases.

- The jurisdictional Commissioners of Customs (Appeals) at Bengaluru and Chennai will be empowered to take up appeals filed in respect of faceless e-assessments pertaining to imports made in their jurisdictions, although the assessing officer may be located at the other customs station.

- The Principal Commissioner/ Commissioner of Customs in Bangalore and Chennai Customs to act as Nodal Commissioners for administratively monitoring the assessment practice in the CAS by the officers of the FAGs. This would enable the establishment of National Assessment Commissionerates (NACs) in future with the mandate to examine the assessment practices of imported articles across customs stations and suggest measures to ensure uniformity and enhanced quality of assessments.

- Dedicated Turant Suvidha Kendras will be established in every customs station staffed by custom officers to support trade in relation to customs clearances in terms of accepting bond or bank guarantee, carrying out specific verifications that may be referred by FAGs, defacing of documents/ permits licences or debit of documents/ permits/ licences, as required, etc.

Procedural and functional guidelines

Responsibilities of Nodal Commissioners

Nodal Commissioners, inter alia, will be responsible for following in relation to assessments undertaken by the FAG:

- Monitoring the assessment practice for uniformity of classification, valuation, exemption benefit and compliance with import policy conditions.

- Evaluating audit objections and taking corrective actions vis-à-vis assessments, and provide inputs to the concerned ports of import, if required.

- Analysing the Risk Management System facilitated BoEs pertaining to Chapters falling under their purview and advising the Directorate General of Analytics and Risk Management regarding possible interventions or review of risk parameters.

- Liaising with Principal Commissioner/ Commissioner of Customs at ports of import on interpretational issues pertaining to classification, valuation, scope of exemption notifications and trade policy conditions, etc.

- Interacting with trade and industry for inputs and resolve their assessment-related issues.

- Examining the orders/ appellate orders in relation to

- assessment practices pertaining to commodities assigned to each FAG and providing inputs to the Commissionerates for reviewing such orders to ensure uniformity of assessment orders, so that they can be upheld at legal forums.

Procedure for verification of assessment of BoE by FAG

The flow of BoE in faceless e-assessment is provided as annexures to the instruction. The key aspects of the flow are as follows:

Normal course

- The importer, as per the current practice, will upload the BoE and relevant documents in the ICEGATE and e-Sanchit. As at present, the selection of a BoE for verification of self-assessment will be on the basis of risk evaluation through appropriate selection criteria.

- For clearances requiring furnishing of bond or bank guarantee (e.g. provisional assessment or concessional duty benefit claim), the importer will be encouraged to opt for continuity bond.

- The CAS will assign the BoE to the concerned FAG for verification of assessment purposes. On verification, the FAGs may decide to –

- Return the BoE to the importer for payment of duty after verification on the basis of the declaration made and documents available in e-Sanchit; or

- Seek additional information or documents for proceeding with the verification; and/ or

- Get examination and/ or testing of goods carried out,

- to determine duty liability and/ or for ensuring compliance of restriction and prohibition.

- In case FAG requires additional information or documents for the verification of assessment, a query will be raised electronically for seeking additional information or documents, preferably in a consolidated manner, through the ICEGATE portal. The importer will need to respond to the query electronically and/ or provide additional documents through e-Sanchit. After scrutinising this, the FAG may –

- Return the BoE for payment of duty after verification; or

- Disagree with the self-assessment and re-assess the BoE. In that case, if the importer does not agree with the re-assessment, the FAG will issue a speaking order as prescribed in the law.

- The FAG, either at the time of accepting the self-assessment or re-assessing the BoE, can order for second check examination of the goods, including giving directions to the shed officers at the port of import to verify original documents, deface documents, take custody of the document, NOC from Participating Government Agencies, verification of country of origin certificate, etc.

- Alternatively, FAGs for the purpose of verification or at the request of importer can –

- Order for first check examination or testing of goods with specific directions or testing parameters to the shed officers at the port of import.

- Pending examination, permit provisional clearance and refer the BoE to PAG for assessment and clearance including any action to be taken basis the outcome of test/ examination.

- Any time after the BoE is returned from the FAG to the port of import, if the imported goods are found to be subject to some restriction or prohibition or misdeclared, the PAG can undertake re-assessment and initiate suitable action, as may be required.

Exceptional circumstances

- In specified exceptional circumstances such as goods liable to confiscation, related party imports requiring examination by Special Valuation Branch, inability to complete verification in the absence of document/ information, etc., the FAG with the specific approval of specified officers, transfer the BoE using the CAS to PAG at the port of import for assessment, without completion of verification of assessment. The FAG can also transfer a BoE to the PAG in any other exceptional circumstances, after due approval from the concerned commissioner.

- However, the Principal Commissioner/ Commissioner of Customs at the port of import may, in specific circumstances and for reasons recorded in writing, direct the PAG to pull the pending BoE from faceless e-assessment to the PAG.

Miscellaneous matters

- FAGs, as is the present practice, are required to pass a speaking order (within 15-days of the date of re-assessment after giving an opportunity for hearing) in case the importer does not agree with the re-assessment. The hearing is to be conducted through video conferencing or other reliable technological means in terms of guidelines prescribed by CBIC.

- An appeal against the assessment order or speaking order lies with the Commissioner (Appeals) having jurisdiction over the port of import.

- The review of any speaking order on re-assessment passed by FAG will lie with the reviewing authority having administrative control over that FAG.

- Issuing of demands for recovery of customs duty short paid or not paid, etc., adjudication thereof and handling of audit objections to be done by the officers of the port of import. In specific cases, clarifications and inputs can be given by the FAG to port of import in such matter for which the Nodal Commissionerates will be the coordinating authority.

- In cases of approved provisional assessment, the FAG may assess the BoE provisionally subject to registration of bonds, etc., at the Turant Suvidha Kendra. If the FAG concludes that the prior testing of goods is going to take considerable time and the BoE needs to be assessed provisionally, they may refer it to the PAG at the port of import. In such cases, the BoE will be assessed by the PAG at the port of import, after the receipt of the examination/ test report.

- The Directorate General of Systems has enabled a facility, whereby, requests for amendments can be made online via the ICEGATE Portal for which process and guidelines, including for payment of fee, are laid down.

- All communications between the FAG and the importer are to be exclusively on ICEGATE. All internal communications between the FAG and the officers at the port of import or the Turant Suvidha Kendra to be exchanged exclusively via the electronic mode.

PwC comments: The phased roll out of faceless e-assessment is a welcome initiative for the ease of doing business, as it obviates the physical interface between the importer and customs authorities, thereby, significantly reducing the cargo clearance time and transaction cost. It should also encourage importers and companies to handle import and export clearances themselves. Hopefully, the proposed system will reduce disputes and ensure uniformity in assessment. However, the effectiveness and success of faceless e-assessment can only be established with the passage of time and experience of stakeholders. To make this initiative a success, periodic interaction and feedback on experience of using the system by trade, as indicated by the CBIC, will help in making it an effective and trade friendly system.

GST Council further waives/ reduces late fees and interest on delay in filing of Form GSTR-3B

The fortieth meeting of the Goods and Service Tax (GST) Council was held on 12 June 2020 through a video conference. The major recommendations concluded at the GST Council meeting are summarised below.

A. Reduction/waiver of late fee and interest for GSTR-3B

B. Other Recommendations

- Time limit for filing application for restoration of registrations cancelled till 12 June 2020 has been extended upto 30 September 2020; and

- Certain clauses of the Finance Act, 2020 amending the Central Goods and Service Tax Act, 2017 and the Integrated Goods and Service Tax Act, 2017 2 would be brought into force from 30 June 2020.

PwC comments: The recommendations are welcome and would provide relief, mainly to small taxpayers, who are faced with issues of reduction in revenues and shortage of working capital due to the COVID-19 pandemic. This news flash is based on the information released by the Press Information Bureau. It is recommended that implementation decisions be taken after reviewing the necessary notifications and/ or required legislative amendments giving effect to these announcements.

Central Government further extends due dates for compliance, procedures and applications as a relief

measure in view of COVID-19 pandemic

The Ministry of Law and Justice issued the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 (Ordinance) to introduce relief measures like extension of time limit for filing appeals, passing of order, issuance of notice etc considering the COVID-19 pandemic. Giving effect to the relief measures introduced by the Ordinance, the Central Government issued several notifications and the Central Board of Indirect Taxes and Customs issued a circular in April 2020. Recently, the Central Government has issued Notifications on 27 June 2020 to further extend the deadlines for various compliances, procedures and applications under the Central Goods and Service Tax Act, 2017 (CGST Act). The below table summarises the extended deadlines.

Chamber Voice - Flip Book

Click Here to view

Fine Points

Advertisement

Forthcoming Events

Consumer Protection has taken a big leap forward in the form of Consumer Protection Act, 2019. The new law which came into force on July 20, 2020, now draws its attention to e-commerce activities, stricter and harsher penalties, additional dispute resolution mechanisms, and much more.

The Cochin Chamber of Commerce & Industry is conducting a virtual meeting on ‘Consumer Protection 2.0’ on August 5, 2020. Mr. Prashanth Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers) and Ms. Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers), will speak on the changes, nuances and the new measures that are to be taken by both buyers and sellers. The other topics that will be covered in this meeting are: 1. Comparisons between the 1986 Act and the 2019 Act; 2. Interplay with other enactments; 3. Liabilities and Responsibilities; 4. Do’s and Don’t for industry and consumers

Speakers:

Mr. Prashanth Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers)

Ms. Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers)

Click Here to register

The next CEO FORUM Virtual Meeting is scheduled for Saturday, 8th August, 2020 between 8.00 a.m and 09:30 a.m.

We have Sri. A.P.M. Mohammed Hanish I.A.S., Principal Secretary II, Department of Industries and Commerce, Government of Kerala who will speak on “The Emerging Economic Opportunities in the post Covid Scenario.”

This is a free session for the Members of the Chamber who have already subscribed for the CEO FORUM on an Annual basis. The meeting link will be sent to the registered participants separately.

Click Here to register

Chamber's Repository for all the Notifications and Guidelines pertaining to the COVID-19 outbreak & resulting lockdown

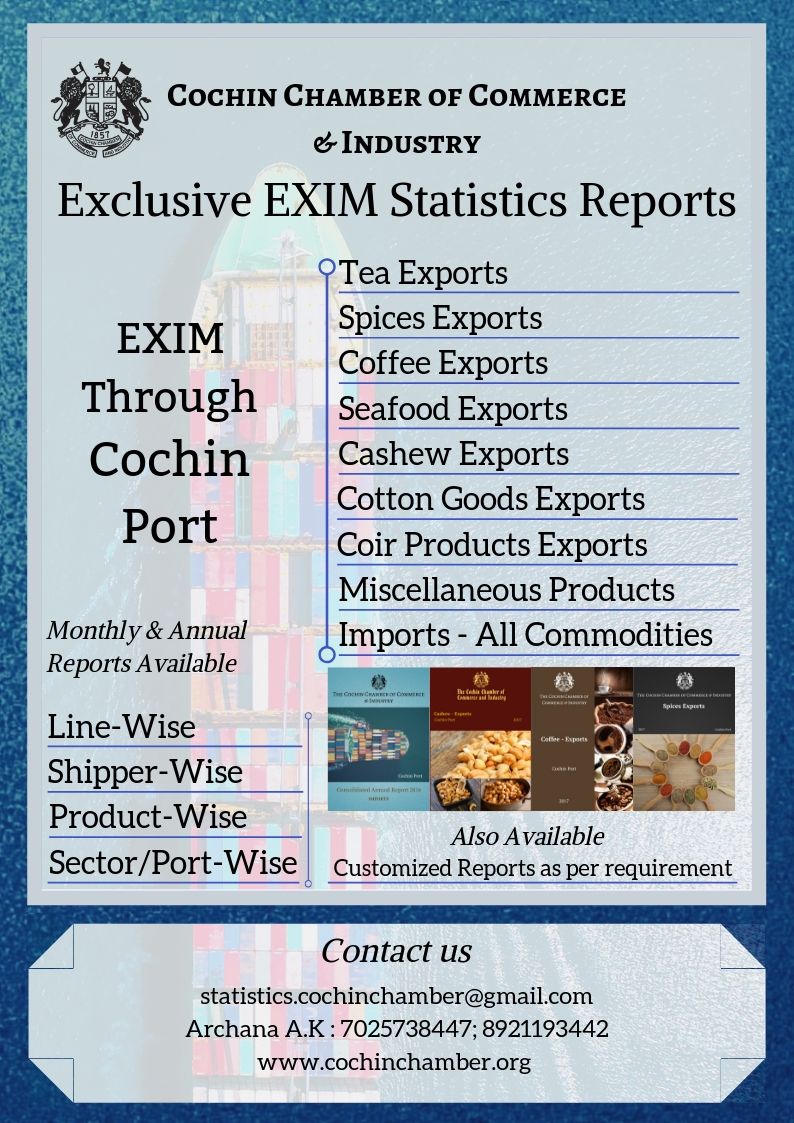

Exclusive EXIM Statistics

Statistical Reports on Exports and Imports through the Cochin Port.

The Cochin Chamber of Commerce and Industry publishes statistical reports on Exports and Imports through the Cochin Port on a monthly basis followed by a Consolidated Annual Report at the end of each calendar year. The reports on exports are classified as commodity wise and pertain to the following commodities:

- Coffee

- Tea

- Spices

- Cashews

- Cotton Goods

- Seafood and

- Coir and coir products

Details on all other commodities that do not fall under the above-mentioned heads are carried as the ‘Miscellaneous Report’. Customized reports will also be available according to customers requirement.

We have several members in the export/import fraternity subscribing to these reports on a monthly basis and from the feedback received they are immensely benefited by the same.

We are confident that our reports will be of help to your Company in staying one step ahead of your competitors in business. A sample of the report is attached herewith for your reference. Also attached is the ‘Subscription Form’ to enable you to subscribe to the report should you want to do so.

Should you have any queries please feel free to contact Ms. Archana (7025738447).

For more details, visit Export-Import Statistics

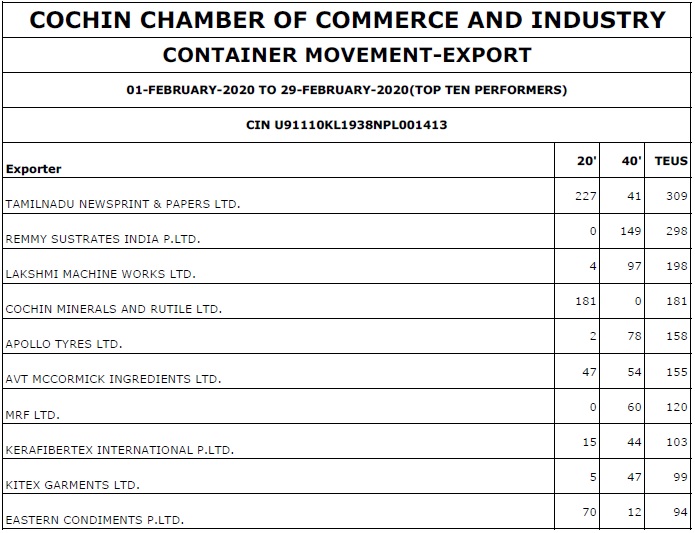

Sample Reports