President's Note

Dear Friends,

Last monsoon, Kerala witnessed its worst nightmare in the form of floods that rendered millions homeless and disrupted trade and commerce across various sectors in the State. This year, the weather has swung to the other extreme; Kerala had a relatively dry spell after the monsoon began on 1st of June, with a 48% rain deficit till 17th of July. But the heavy rains since has reduced the deficit to 36% and it is gaining momentum. Let us hope that in the coming month or so we will have a reasonably good monsoon.

The trial run of the second phase of the Kochi Metro is on and according to reports it was a great success. With the delay in completing the construction of Vytilla flyover having made the journey through the busy Vytilla junction a nightmare, I hope the commissioning of the second phase of the Metro will happen at the earliest as it will help ease the problems being faced by commuters traveling through Vytilla.

The Union Government has introduced the Wages Bill intending to fix a single mandatory floor for minimum wages. We were extremely anxious about the recommendations made and are of the view that the penal provisions recommended are highly excessive. We have sent a representation to the Hon’ble Prime Minister of India and the Hon’ble Minister for Labour and Employment conveying our reservations on the recommendations on the Code on the Wages Bill made by the Standing Committee on Labour.

Since February this year, nearly 200 containers of cement are lying idle at the Cochin Port due to the imposition of 200 percent Customs Duty on all imports from Pakistan. The cargo has not been cleared due to technical issues and the huge variation in the revised duty would cause heavy financial burden to the trade. We have taken up the issue with the authorities concerned with a request to look into the matter urgently.

The month of July has been a busy month for the Chamber with several programmes. The Seventh meeting of the Fourth Edition of the CEO Forum Breakfast Meeting was held on 5th of July. This time, we had a very special Guest Speaker, the newly appointed District Collector of Ernakulam, Mr. Suhas I.A.S. The session was an interactive one between the CEOs at the Forum and the Collector where they shared their opinions on various matters about the city and the Collector outlining the tasks that need his immediate intervention.

Having said that, the next CEO Forum Meeting will be on the 2nd of August and the Guest Speaker will be Mr. K Jayakumar, I.A.S (Retired), Former Chief Secretary, Government of Kerala and Director, Institute of Management in Government, Kerala. The Session will be on the topic “Commerce without Conscience: A Matter of National Concern.” I hope you all will make it convenient to attend the session.

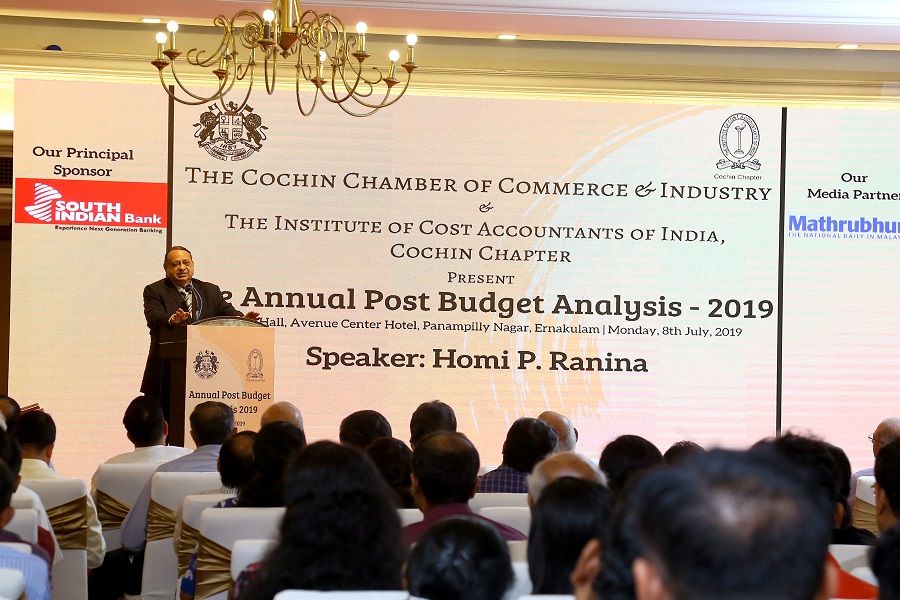

As is the practice, we conducted the Annual Post Budget Analysis on the 8th of July immediately after the Union Budget was presented in Parliament. Mr. Homi P Ranina, an eminent lawyer and Tax Consultant was the Speaker at the session. In his address, Mr. Ranina said that the emphasis of the Budget has been on growth and development with special mention on infrastructure, agriculture, and the education sector. The Chamber has, by and large, welcomed the proposals put forward by the Government and hopes that the implementation will ensure that the desired results are achieved. The gist of Mr. Ranina’s talk is given in this issue of Newsletter for your information.

In the second week of July, we conducted a Seminar on ‘Corporate Compliances, 2019 – A Tutorial for Companies’ with Adv. Prashanth S Shivadass and Adv. Hari Prasad M S, Shivadass and Shivadass (Law Chambers) from Bangalore. This was a very important and informative Session given the fact that Corporate Compliance has become very important as per the current Companies Act and any non-compliance attracts severe penalties.

Detailed reports along with the pictures of these programmes are carried elsewhere in this issue of the Newsletter.

The Chamber’s Research Wing has submitted a report on the Kerala Farmer’s Welfare Fund Bill to the Select Committee at a Public Consultation held recently to gauge the views of the stakeholders on the draft Bill. The Chamber’s suggestions were well received by the Select Committee headed by the Hon’ble Minister for Agriculture.

I am happy to inform our members that the Chamber Souvenir “A Glorious Voyage that began in 1857” which was released at the time of the 162nd Chamber Day is now available at the Chamber’s Office. The Souvenir outlines the Chamber’s 162-year journey and the information about the members and their areas of operation. Please get in touch with the Chamber’s Office if you wish to purchase the same.

On 30th of July, the Chamber in association with ‘anb Legal and Grant Thornton’ will be conducting a Seminar on the “Proposed Constitution of the Hon’ble National Company Law Tribunal. The Seminar will be handled by Mr. Pradeep Parikh, Ex-Vice President, ITAT & Senior Consultant with anb Legal and Ms. Shreni Shetty, Partner – Dispute Resolution, ANB Legal. The seminar will provide insights into the powers and functions of the Hon’ble National Company Law Tribunal. Details about this programme are given in the ‘Upcoming Events’ section of this Newsletter.

As stated by our Hon’ble Finance Minister, India hopes to become five trillion dollar economy by 2025 and start-ups are expected to play a huge role in this. In addition to creating wealth from their entrepreneurial ventures, entrepreneurs’ also create jobs and the conditions for a flourishing society. In this regard, on the 21st of August, World Entrepreneurs’ Day, the Chamber is planning to organize a programme to inspire and motivate the next generation of entrepreneurs in our society. The details of the same will be shared with you in due course.

I trust that you will make use of these opportunities to the fullest. Wishing you all the very best and assure you of the Chamber’s best services at all times.

Regards,

V Venugopal

Trivia

Advertisement

Recent Events

CEO FORUM 2019 - 7th Breakfast Meeting

An Interactive Breakfast Session with the new District Collector of Ernakulam | 05.07.2019

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s – 6th Breakfast Meeting on Friday, 7th June 2019 at Taj Gateway Hotel, Ernakulam.

Mr. V Venugopal, President of the Chamber delivered the Welcome Address and introduced the Speaker for the meeting.

The Guest Speaker at the meeting was the newly appointed District Collector of Ernakulam, Mr. Suhas I.A.S.

The Session was an interactive one between the CEOs at the Forum and the District Collector where they shared their concerns and suggestions regarding matters pertaining to the city. Mr. Suhas recollected his term as the District Collector of Alleppey during the time of floods last year and spoke about the relief activities carried out by him and the challenges he faced during the course of this. Mr. Suhas expressed his enthusiasm in taking forward the projects started by his predecessors, in the best possible manner and appreciated the great work done by them.

Mr. Suhas said that the main mandate the Government has given him is the need for infrastructure development in the city. He spoke about the ongoing Metro project and mentioned that land acquisition for the same has started and he hopes to finish it by July 20th.

Mr. Suhas spoke about the plans he has for the City and also mentioned the tasks that need his immediate intervention. He expressed his interest in exploiting the tourism potential of the city so as to attract more tourists. Mr. Suhas also spoke of his plans to have a proper waste management system in the city and also to introduce strict laws to control the dumping of waste on the streets.

The Collector appreciated the fact that he found it easy to get volunteers in Ernakulam as opposed to other parts of the State. He emphasized the fact that projects like cleaning of the canals in the city has huge potential that it will make the waterways within the city navigable.

The Collector assured the participants that he will take their concerns regarding the traffic problems in the city with the authorities concerned to see what can be done to ease the situation currently prevailing. He also mentioned about building an interactive platform where the people could interact with Collector and share their issues and suggestions.

Ms. Nisha Menon, Director – Tax, PwC India, gave the Quick Bytes on the upcoming changes in GST.

Mr. V Venugopal, President of the Chamber presented a Memento to the Collector.

Mr. S P Kamath, Executive Committee Member of the Chamber proposed the Vote of Thanks.

The programme was attended by over 35 CEOs and top-level Managers across different verticals of the Industry.

Annual Post Budget Analysis

08.07.2019

Gist of the speech delivered by Mr. H. P. Ranina

The maiden budget of Ms. Nirmala Sitaraman lays down the road map for a strong and vibrant economy. This is despite the gloomy global economic scenario and the lower projected growth rate of 6.8% for the Indian economy during 2018-19. The success of the second term of the Modi Government will be tested by the outcomes rather than the outlays proposed in this year’s budget documents.

The Finance Minister has presented her budget proposals with a degree of caution and trepidation. Her exercise at creating a fine balance between the need for fiscal consolidation and promoting growth has ensured that no populist measures are announced. She needs to be complimented for having brought down the fiscal deficit to 3.3% of GDP for fiscal year 2019-20.

Fiscal consolidation is the only path available for restoring credibility in the Indian economy.

The Government has shown its sincerity and commitment to tackle the problems facing the jobless youth. The emphasis is to encourage young job seekers to become job creators. Promoting employment opportunities in the textile, retail, food processing and construction sectors has been a critical need which has been partially addressed by the Government. Not enough has been done to make labour laws flexible and in line with modern day trends prevailing in developing countries which have a growing young population as in India.

To promote ease of doing business, the Government has successfully launched an e-Biz portal which will integrate 14 regulatory permissions. This will make it possible to start a new business without obtaining prior approvals, so long as such start-ups are in conformity with guidelines and criteria. Exemption of start-ups from the angel tax is a step in the right direction. The objective is to encourage young entrepreneurs to create value out of ideas and initiatives.

Affordable housing has been given the right impetus which will also give a boost to employment creation, given the high degree of forward and backward linkages with other segments of the economy. The higher tax break in respect of interest paid upto Rs. 3.5 lakhs on loans taken for purchase of houses valued at Rs 45 lakhs or less will help young people to settle down and at the same time give a boost to the construction industry.

To drive the momentum on private consumption, the budget proposals focus on ways to increase rural income which, in turn, will promote rural demand. To ensure higher income in the hands of agriculturists, involvement of the corporate sector has been suggested which would enable use of advance technology in key areas, like micro-irrigation, crop care, advanced seeds and selection of the right crop having regard to the soil conditions. Agri reforms are sought to be introduced by encouraging adoption of the Model Agricultural Land Leasing Act, 2016 to facilitate consolidation of land.

Between July and September this year, the Government is proposing to invest Rs.15,000 crore in the Jal Shakti Abhiyan scheme which will cover 200,000 works to be taken up for water conservation in nearly 1,100 water stressed blocks. The employment guarantee scheme which mandates that 60% of its expenditure is to be incurred on national resource management, has set a target for construction of farm ponds, rainwater harvesting, re-use of water and intensive afforestation. The Government is determined to provide piped drinking water to every household by 2024.

As a key measure of labour reform, the Government has introduced the Code on Wages Bill which will make minimum wages applicable in both formal and informal sectors and make it mandatory for payment of wages directly into the bank account of employees. Under this legislation, the Central/State Governments will determine the factors for fixing the minimum wages for different categories of employees based on their skill, the arduous nature of the work, geographical location and other critical and special aspects.

Personal income tax rates have been left unchanged and those who have taxable income upto Rs. 5 lakhs will not have to pay tax at all. Increase in the rate of surcharge on those having more than Rs. 2 crores of taxable income will affect just a few tax payers, less than 50,000 out of a population of 1.3 billion. Citizens are greatly relieved that wealth tax and inheritance tax are not proposed to be introduced as was feared.

Tax on companies having turnover of upto Rs. 400 crores has been reduced to 25% which will now be applicable to 99.7% of the corporate sector. The capital gains tax structure has not been tinkered with. Gifts made by residents to non-residents will be taxable in India in the hands of the latter unless such non-residents are relatives as defined in the Income tax Act. If payment made to a contractor or professional exceeds Rs. 50 lakhs in a financial year, tax will be deductible at source by an individual who pays such amount.

Foreign institutional investors and other market players have invested more than USD 11 billion in Indian equities in the past few months primarily on ground of political stability and the present Government’s commitment for pushing economic reforms. This is also due to the fact that other economies like China are facing uncertainty with the trade war with the U.S. Government looming large. Foreign investors are also banking on the fact that interest rates will keep coming down in India and the domestic demand will show a healthy trend in the coming year.

The Budget proposals are replete with big ideas in social security, education and foreign direct investment. Policy credibility is a precious commodity in these turbulent global times. If consumption demand picks up as a result of additional public expenditure and a normal monsoon this season, India would be on the growth path with a 7.2% increase in GDP in fiscal year 2019-20 as against 6.8% in 2018-19. This will lay the foundation for a strong and vibrant economy which is expected to grow to US$ 5 trillion by 2023, making it the third largest economy in the world.

Seminar on “Corporate Compliances, 2019 – A Tutorial for Companies"

12.07.2019

The Cochin Chamber of Commerce and Industry conducted a seminar on “Corporate Compliances, 2019 – A Tutorial for Companies” on 12th July 2019 at Hotel Park Central, Kaloor, Cochin. The Seminar was led by Mr. Prashanth G Shivadass, Advocate & Founder of Shivadass & Shivadass (Law Chambers) and Mr. Hari Prasad M S, Advocate at Shivadass & Shivadass (Law Chambers).

The purpose of the Seminar was to give the participants an insight into the major amendments in the Companies Act, 2013, SEBI Compliances, Start-Up Compliances, and the Competition Law.

Mr. V. Venugopal, President of Cochin Chamber of Commerce and Industry delivered the Welcome Address.

Mr. Venugopal C Govind, Past President of the Chamber gave an introduction to the Companies Act and the importance of compliance in Organizations.

The Session commenced with an overview of the Start-up Policy and the criteria to be considered for start-up recognition. The Company should have a turnover not exceeding Rs. 100 crores and it should be registered as a Private Limited Company and it should work towards the development and improvement of a product. The Session also covered Foreign Direct Investment and its permitted and prohibited sectors and Start-up incentives in Finance Bill, 2019.

The next half of session dealt with topics like Companies (Amendment) Ordinance, 2018, Companies (Amendment) Bill, 2019, Companies (Amendment) Ordinance, 2019 and Companies (Amendment), Second Ordinance, 2019. Mr. Hari Prasad explained the changes effected in the Memorandum and Articles, registration of significant beneficial owners in a Company, disqualification for the appointment of Directors, number of Directorships, and adjudication of penalties before and after the amendments.

He also explained in detail the changes in the penal provisions stating that 16 out of 81 compoundable offenses are liable to penalty instead of being punishable with imprisonment.

The Speaker explained the new E-Forms under the Companies Act, 2013 namely FORM NFRA-1, FORM BEN-1, FORM DPT-3, FORM INC 22 A and so on. The Session also covered topics like ‘annual returns on foreign liabilities and assets, annual performance report, external commercial borrowings, single master form, and FORM FC-GPR under the RBI and FEMA Compliances’ in detail.

Mr. Hari Prasad later discussed the statement of Investor Complaints, Corporate Governance, Shareholding pattern and Reconciliation of Share Capital Audit under SEBI Compliances. He also explained the definitions of terms in the Insolvency and Bankruptcy under the IB Code, Corporate Insolvency Resolution process, initiation of the Corporate Insolvency Resolution process, National Company Law Tribunal, etc.

The final session covered topics under the Competition Law related Compliances like the key considerations of Competition Law, risk of non-compliance, provisions of the Competition Act and anti-competitive agreements in detail. Markets sharing and limiting production & supply, bid rigging, leniency, dominance and abuse, and compliance strategy were also discussed during the Session.

The Seminar concluded by a Q&A session where the participants clarified their doubts on various aspects of the compliance format. The Chamber presented Mementos to the Speakers and the Vote of Thanks was delivered by Ms. Archana, Executive – Business Development, CCCI.

The Seminar was attended by 32 participants representing different Organisations.

Key Highlights of Economic Survey 2018-19

The Union Minister for Finance and Corporate Affairs, Smt. Nirmala Sitharaman tabled the Economic Survey 2018-19 in Parliament on July 4th, 2019.

The Key Highlights of Economic Survey 2018-19 are as follows:

- Shifting gears: Private Investment as the Key Driver of Growth, Jobs, Exports and Demand

- Policy for Real People, Not Robots: Leveraging the Behavioral Economics of “Nudge”

- Nourishing Dwarfs to become Giants: Reorienting policies for MSME Growth

- Data “Of the People, By the People, For the People”

- Ending Matsyanyaya: How to Ramp up Capacity in the Lower Judiciary

- How does Policy Uncertainty affect Investment?

- India’s Demography at 2040: Planning Public Good Provision for the 21st Century

- From Swach Bharat to Sundar Bharat via Swasth Bharat: An Analysis of the Swachh Bharat Mission

- Enabling Inclusive Growth through Affordable, Reliable and Sustainable Energy

- Effective Use of Technology for Welfare Schemes – Case of MGNREGS

- Redesigning a Minimum Wage System in India for Inclusive Growth

- State of the Economy in 2018-19: A Macro View

- Fiscal Developments

- Money Management and Financial Intermediation

- Prices and Inflation

- Sustainable Development and Climate Change

- External Sector

- Agriculture and Food Management

- Industry and Infrastructure

- Services Sector

- Social Infrastructure, Employment and Human Development

Please click the below link to download the detailed key highlights of Economic Survey 2018-19.

Fine Points

MANDATORY COMPLIANCES UNDER COMPANIES ACT, 2013

With the rise in number of young entrepreneurs we have noticed a significant rise in new company registrations in India. Such entrepreneurs have great expertise and insight in their field. However, they need assistance and guidance is making sure that all the required mandatory compliances under Companies Act, 2013 are done in required time frame.

Types of Compliances under Companies Act, 2013

Compliances under Companies Act, 2013 can be categorized in following types:

- After incorporation compliances under Companies Act, 2013

- Annual compliances under Companies Act, 2013

- Event based compliances under Companies Act, 2013

After Incorporation Compliances under Companies Act, 2013

There are certain Compliances under Companies Act, 2013 that are required to be done once company registration is successfully completed. After registration, every company gains a separate legal entity and it becomes liable to comply with all the legal requirements mandated under the Act. Following is a list of all such required compliances under Companies Act, 2013:

- Verification of Registered Office

After successful incorporation, every company is required to complete verification of its registered office with the registrar of companies. They have an option to communicate the same via SPICe Form at the time of incorporation. However, if that is not done, then it must be communicated through INC-22 within 30 days of incorporation.

- Display company information

Every registered company is required to display the following information outside its registered office and above its business letters, billheads and on all other official documents and publications:

- Company’s name

- Corporate Identification Number

- Registered office address

- Official phone number

- Website, email Id & Fax No.

- First Board Meeting

Every newly incorporated company is required to conduct its first board meeting within 30 days from the date of its incorporation.

- Appointment of auditor

Every company is required to appoint an Auditor within 30 days of incorporation in a board meeting who will either be confirmed or changed in the subsequent AGM.

- Share Certificate Issuance

Every Company is required to issue share certificates to the shareholder named in the incorporation document. All the incorporation details along with share certificate numbers must be mentioned in the records maintained by the Company.

- Disclosure of interest by Directors

Every Director is required to disclose the details of interest in other Registered Companies through Form MBP-1 in the First Board Meeting held within 30 days after incorporation.

- Maintenance of Minutes

Every Company is required to maintain Minutes of every meeting held. These Minutes must be prepared within 15 days of such meeting and are to be finalized within 30 days.

8 . Maintenance of Statutory Registers

As per Section 85 & 88 of companies Act, 2013 every Registered Company is required to prepare and maintain certain statutory registers at its Registered Office. These statutory registers include Register of Members, Register of Shareholders, Register of Charges, Register of Employee Stock Option, etc.

In case any Registered Company fails to maintain such statutory registers then such Company and Directors will be prosecuted and fined under the Act.

Annual Compliances under Companies Act, 2013

Following is a list of all such yearly compliances under Companies Act, 2013:

- Board Meetings

In addition to the first Board Meeting every Registered Company is required to conduct as per incorporation compliances a minimum 4 board meeting every year. The maximum gap allowed between two consecutive Board Meetings is 120 days.

- Annual General Meeting

Apart from 4 board meetings every company is required to conduct its Annual General Meeting of its members every year. The first AGM is required to be conducted within 9 months from the end of financial year and in the subsequent years it is required to be conducted within 6 months from the end of financial year. The maximum gap allowed between two subsequent Annual General Meetings is 15 months.

- Receipt of Form MBP-1

Every director is required to submit a disclosure of his/her interest in every other registered entity in Form MBP-1. This disclosure is required to be done every year in the first Board Meeting by every existing director on a mandatory basis. Along with yearly disclosure every director must also disclose any change in his/her interest in the subsequent board meeting after such change happened.

- Receipt of Form DIR-2

DIR-2 is used for submission of disclosure of non-disqualification by the directors of the company. The company must ensure receipt of this disclosure form every financial year.

- Preparation of Director’s Report

As per Section 134 of the Companies Act, 2013 Board of Director of every registered company is required to prepare Director’s report. This Director’s report will be submitted with the Form AOC-4 at the time of annual filing. Director’s report will include information including financials, state of affairs, any kind of changes in company’s composition, declared dividends, loans etc.

- Preparation and circulation of Financial Statements

Every Company is required to ensure maintenance of its financials and circulate the same along with Director’s Report and Auditor’s Report along with the Notice of their Annual General Meeting.

- Appointment of Auditor

Every registered Company is required to appoint an Auditor. Auditor can be appointed for a period of 5 years and information of their appointment is required to be submitted with the ROC in Form ADT-1. Earlier this appointment was required to be ratified every year in the AGM during the course of those 5 years. However, this requirement has been done away with.

- Filing of E-Form MGT-7

Section 92 of Companies Act, 2013 specifies that the Annual Return of every Company is required to be submitted in e-Form MGT-7. It must be filed within 6 days from the date of its Annual General Meeting. For every Company with paid up capital more than 10 crore rupees along with listed companies the annual return is required to be certified by practicing Company Secretary.

- Filing of E-Form AOC-4

Along with annual return you are also required to file the Company’s financials with the ROC within 30 days from the date of its Annual General Meeting in e-Form AOC-4. The following documents are submitted as attachments with this form:

- Copy of Balance Sheet

- Copy of Profit and Loss A/c

- Notice of AGM

- Director’s Report

- Auditors’ Report

Event based Compliances under Companies Act, 2013

Apart from regular compliances there are several event based compliances under Companies Act, 2013 that are required to be adhered to. Such compliances under Companies Act, 2013 are non-negotiable and are to be adhered to without any lapse. If there is any delay in filing such forms after due date then it attracts penalties and punishments.

Following are examples of few such event based compliances

- Change in Directorship

Whenever there is any change in Board of Directors including appointment and cessation or change in designation it must be communicated to the registrar through filing of DIR-12 within 30 days of such change.

- Change in Registered Office Address

Any Company can change its registered office due to various reasons. However, it is obligated to intimate such change to the Registrar of Companies. Following are different scenarios for change in registered office:

- If such change is within the local limits of the city then only INC-22 is required to be filed for intimation.

- If such change is outside the boundaries of city but within the state then special resolution is passed. E-Form MGT-14 along with INC-22 is required to be filed.

- On the other hand, if registered office is shifted to another state or outside the jurisdiction of one ROC to another there are some additional compliance. Furthermore, along with MGT-14 and INC-22 company is required to file for Central Government approval in INC-23 and its confirmation is filed in INC-28.

- Increase in Authorized Capital

In case there is a plan to increase the authorized capital of any Company the first step is to pass a special resolution for changing the MOA in the EGM. File MGT-14 for registering such special resolution. The final step is to file SH-4 with the ROC.

- Change in Company Name

If the members decide to change the name of a Registered Company then following steps are required to be followed:

- Check for name availability and reserve it through RUN service.

- Pass special resolution and file MGT-14.

- File INC-24 for Central Government approval.

- Registration/Amendment/ Settlement of Charge

These are the compliances under Companies Act, 2013 in case the company creates any charge i.e a security given for securing any amount of loan. In case of creation of a fresh charge or any modification of existing charge e-Form CHG-1 is required to be submitted.

On the other hand, in case of settlement of charge e-Form CHG-4 is to be filed.

Quote

Advertisment

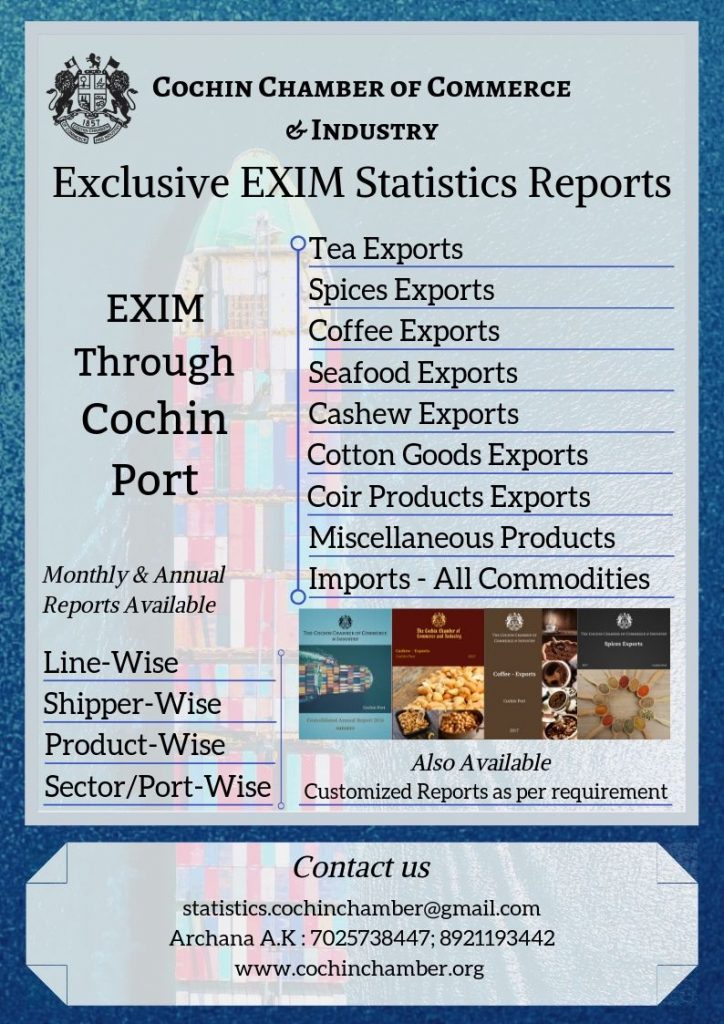

Digital Certificate of Origin

Exclusive EXIM Statistics

Advertisement

India Ranked 52nd in Global Innovation Index-2019

Union Minister of Commerce & Industry and Railways, Mr. Piyush Goyal, launched the Global Innovation Index (GII) 2019 in New Delhi. India jumped five places to improve its position from 57th last year to 52nd in 2019.

Speaking on this occasion Commerce and Industry Minister first congratulated all those involved in the process and said that India has made a significant progress to 52nd rank in the GII-2019 and now the culture of innovation is coming to the centre-stage. He said that India will continue its efforts to reach upwards of top 50 ranks in the GII. He further said that India will not rest on past laurels until it achieves its target of positioning itself among the top 25 countries of the Global Innovation Index. To achieve this ranking, he urged all stakeholders to work in mission mode.

The Minister urged the R&D institutions, universities and private sector to transform the country into a hub of innovation. The Commerce and Industry Ministry requested the World Intellectual Property Organization (WIPO) to factor in India’s rural innovation as part of the innovation index in future.

The Commerce and Industry Minister in his address said that the improvement in the rankings should inspire Indians to help marginalized and under privileged section of society and R&D must provide sustainable solutions to the problems that India is facing at present like rising pollution levels in cities, water crises faced in different parts of the country, depleting natural resources, issues of climate change and solving problems of food wastage. All these problems that the country is facing should be solve through innovative ideas. The Commerce and Industry Minister further added that India must be a responsive country and work in mission mode by engaging with academia, private sector and government agencies to improve the quality of citizens’ lives even in the remotest parts of the country.

Referring to GII theme of this year which is Creating Healthy Lives – The Future of Medical Innovation, he said that Government of India is focusing on not just curative but preventive healthcare where wellness becomes a part of society.

The GII rankings are published every year by Cornell University, INSEAD and the UN World Intellectual Property Organization (WIPO) and GII Knowledge Partners. This is the 12th edition of the GII rankings of 129 economies based on 80 indicators ranging from intellectual property filing rates to mobile-application creation, education spending and scientific and technical publications.

Switzerland remains number one is the GII index followed by Sweden, the United States of America, the Netherlands, the United Kingdom, Finland, Denmark, Singapore, Germany and Israel.

(Source : PIB, GoI)

New Members of the Chamber

Regular Members

1. SEP & Associates

43/2695A, Kari Parambil Lane, SRM Road,

Cochin-682 018

Phone Numbers : 0484 4873636, 4874242

E-mail : [email protected]

Web site : www.sepassociates.in

2. Logiware Supply Chain Solutions

XX/626, Thadiyittaparambu,

South Vazhakulam, Aluva,

Cochin-683 106.

Phone Numbers : 0484 2633432

Mob: 8086800103

E-mail : [email protected]

Web site : www.logiware.scs.com

3. SFO Technologies Pvt. Ltd.

Plot No.2, Cochin Special Economic Zone,

Kakkanad,

Cochin-682 037.

Phone Numbers : 0484 6614300

E-mail : [email protected]

Web site : www.nestgroup.net

Affiliate Members

1. Desire Kochi

Door No.65/4655-A, Manappatti Parambu, Kaloor,

Ernakulam-682 017.

Phone Numbers : 0484 2980730 Mob: 9895897612

E-mail : [email protected], [email protected]

1. Stream Perfect Global Services

Jyothirmaya, First Floor, Wing-2, Infopark Phase-II,

Brahmapuram P.O., Cochin-682 303.

Phone Numbers : 0484 2972793 Mob: 9446319895

E-mail : [email protected]

Web site : www.spgs.in

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

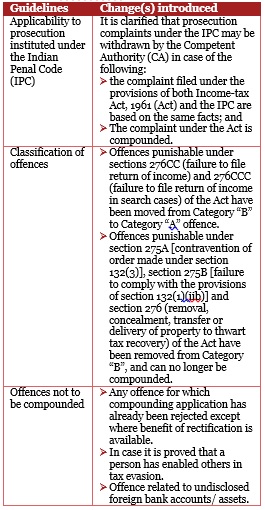

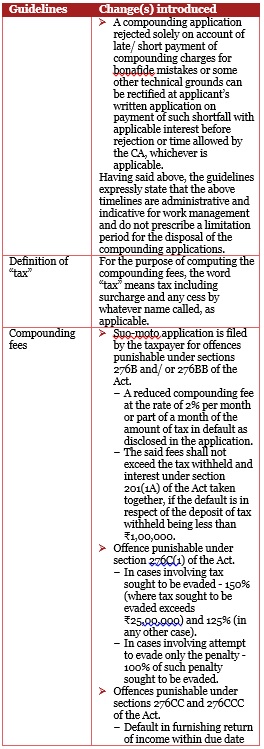

CBDT issues revised guidelines for Compounding of Offences under Direct Tax Laws, 2019

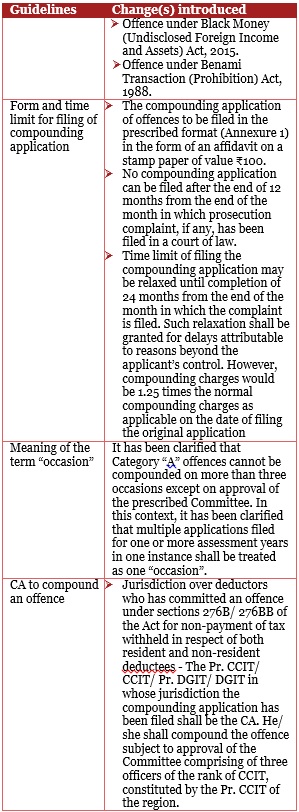

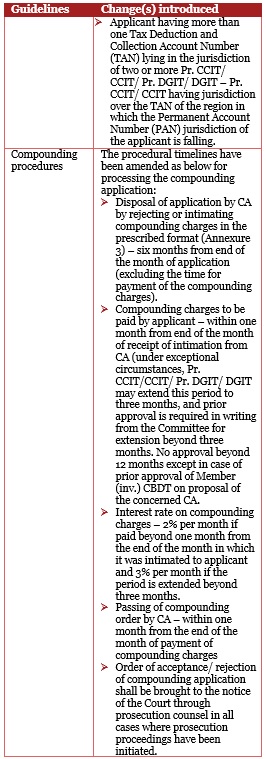

The Central Board of Direct Taxes (CBDT) has issued guidelines for compounding of offences under the Direct Tax Laws, 2019 in supersession of its previous guidelines dated 23-Dec-14. The new guidelines shall come into effect from 17-Jun-19 and shall apply to all applications for compounding received on or after the aforesaid date. The key changes in the revised guidelines have been summarised below.

PwC comments: The CBDT, by revising the compounding guidelines, has brought in a more stringent framework for compounding offences punishable under the Direct Tax Laws. The emphasis in the revised guidelines is on preventing serious offences under the Black Money Act and Benami Transaction (Prohibition) Act from being compounded. Certain other offences such as contravention of search and seizure orders, denial of access to electronic records to the authorities, property related offences to thwart tax recovery, etc., are no longer compoundable. The CBDT has also tried to ensure that the taxpayers do not undergo hardship in genuine cases. For instance, compounding can be allowed up to three occasions (earlier, only one opportunity was available) in case of non-filing of return of income. Also, the Finance Minister has the powers to relax the restrictions for compounding of an offence in deserving cases, based on the recommendation of the CBDT.

District Court upholds prosecution for delay in deposit of taxes deducted – reasonable cause not substantiated by evidence

Recently, the Mumbai District Court sentenced the taxpayer for three months rigorous imprisonment and monetary fine for delay in deposit of taxes that was deducted. The court observed that the reasonable cause cited by the taxpayer was not substantiated by evidence on record. Further, the court held that the taxes deducted on behalf of the Government must be deposited to the credit of the Central Government and not be used for other purposes.

PwC Comments: The judgement is a clear indication of the strict approach of the tax department and the courts, regarding the stringent compliance with the provisions of Chapter XVII-B of the Act. Therefore, it becomes imperative for taxpayers to closely monitor their withholding tax compliance to avoid any adverse consequences. Further, in case of default, the taxpayer must suitably weigh the remedies available under the Act

International Tax

Union Cabinet of India approves the ratification of MLI

The Union Cabinet of India recently approved the ratification of the Multilateral Convention (MLI) to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS). It has also requested the Ministry of External Affairs to obtain the instrument of ratification from the Hon’ble President of India.

Overview MLI is a unique instrument developed by OECD to prevent tax base erosion and profit shifting (BEPS). It will enable the signatories to implement BEPS principles swiftly, as it covers a large number of double tax treaties. The MLI already covers 88 jurisdictions which include jurisdictions from all the continents. India signed the MLI in Paris on June 07, 2017.

Application The MLI does not apply to all the tax treaties of signatories, but only to those where both the parties to a tax treaty have notified that it is covered. Such treaties are known as Covered Tax Agreements (CTAs). Further, for MLI to apply, countries have to ratify it in accordance with their domestic laws (where such ratification, acceptance or approval is required), and deposit their instrument of ratification with the OECD’s Depositary (Depositary).

Entry into force In general, the MLI comes into force from the first day of the month, following expiration of three months from the date the instrument of ratification has been deposited with the Depositary.

Entry into effect In order to complete the process, India would also have to deposit its MLI position with the depositary or indicate that its draft MLI position for CTAs with various countries may be treated as final. Once the MLI is ratified by India, it’s effect will be known only after MLI positions of respective treaty partners are known.

PwC Comments: Potentially, a thorough understanding of the impact of MLI on the conduct of business is essential not only prospectively for the investments and operations ahead, but also to reassess the availability of treaty benefits for existing structures and arrangements.

Annual return on Foreign Liabilities and Assets (FLA return) – Change in system of reporting

The Reserve Bank of India (RBI) has operationalized a web-based system online reporting portal – Foreign Liabilities and Assets Information Reporting (FLAIR) system for submission of foreign liabilities and assets (FLA) return by 15 July of every year, to enhance the security-level in data submission and improve data quality. This replaces the present email-based reporting system for submission of FLA return.

The main features of the FLAIR system are as follows:

- FLA return is required to be submitted by the following entities, which have received foreign direct investment and/ or made overseas investment:

- A Company within the meaning of section 1(4) of the Companies Act, 2013.

- A limited liability partnership registered under the Limited Liability Partnership Act, 2008

- Others, including SEBI-registered Alternative Investment Funds (AIFs), Partnership Firms, Investment Vehicles, Public Private Partnerships, etc.

The circular now specifically mentions AIFs and Investment Vehicles as reporting entities required to file FLA return.

- Reporting entities must create a login-name and password and register themselves on the following web portal: https://flair.rbi.org.in

- The existing mechanism of email-based submission of FLA forms will be discontinued.

- These directions will come into force with immediate effect and would be applicable for reporting information for the financial year 2018-19, i.e. FLA due on 15 July 2019 also needs to be filed on the new portal.

- The FAQs issued by RBI in this regard provide that RBI approval would be required in case an entity wants to –

- File FLA return beyond the due date or file FLA return for any previous years

- Delete or modify the previous version of FLA return

The RBI approval may be obtained by sending an email to:- [email protected].

- Indian entities not complying with above will be treated as non-compliant with the Foreign Exchange Management Act, 1999 and regulations made thereunder.

The RBI has issued a user manual containing step-by-step instructions for registration and data entry, and FAQs, both of which can be downloaded from the FLAIR portal (https://flair.rbi.org.in)

Regulatory

RBI announces prudential framework for resolution of stressed assets

The Reserve Bank of India (RBI) recently released a prudential framework for the resolution of stressed assets by banks. The fundamental principles of the framework are listed below

Prudential framework

- Applicability

This framework would apply to the following lenders –

- Scheduled commercial banks;

- All India term FIs;

- Small finance banks; and

- NBFC-ND-SI and NBFC-D

- Special mentioned accounts categorization

Lenders are required to classify the accounts immediately on default of principal of interest wholly or partly overdue or in case of revolving credit facilities, the outstanding balance remains in excess of sanctioned amounts. The accounts can be classified as special mention accounts (SMA)-0, SMA-1 and SMA-2

- Reporting

Lenders are required to report the credit information/ classification as SMA to the Central Repository of Information on Large Credits (CRILC) for borrowers having aggregate exposure of ₹50 million and above on a weekly and monthly basis

- Resolution plan

- The lenders must put in place a board approved resolution policy for resolution of stressed assets

Once the borrower is in default of any scheduled commercial bank, all India term FIs or small finance banks, the lenders shall undertake a prima facie review of the borrower within 30 days of the default and may decide on resolution strategy, approach, etc. With the introduction of the concept of review period, the lenders get an additional period of 30 days over and above the timeline as mentioned in the framework

- In case lenders decide to implement the resolution plan, they will enter into an ICA during the review period, which would provide that the decision agreed upon by the following shall be binding on all lenders:

- Lenders representing 75% of the value of total outstanding credit facilities; and

- 60% of lenders in number

This is a new requirement where the decision-making is not only linked to the quantum of loan held by lenders but also the number of lenders

- The resolution plan should provide that dissenting lenders will not get less than the liquidation value due to them.

- The framework also states that the ICA may provide for duties of lenders and protect the rights of dissenting lenders and treatment of lenders with priority in cash flows/ differential security interest

- Timelines

- The resolution plan should be implemented within 180 days from the end of the review period:

- ₹20 billion or more: In case of accounts with exposure to scheduled commercial banks, all India term FIs or small finance banks with more than ₹20 billion, the review period shall commence from

- 7 June 2019 in case the account is already under default; or

- Date of default after 7 June 2019

- ₹20 billion or more: In case of accounts with exposure to scheduled commercial banks, all India term FIs or small finance banks with more than ₹20 billion, the review period shall commence from

- ₹15 billion and above but less than ₹20 billion: In case of accounts with exposure more than ₹15 billion but less than ₹20 billion, the reference period to calculate the review period is 1 January 2020. Thus, the review shall commence from:

- 1 January 2020 – in case the account is in default on that date; or

- Date of default after 1 January 2020

This means that accounts between ₹15 to 20 billion, which are already in default have already been given an extended period from 7 June 2019 until 31 December 2019 to get their default rectified. If default still stands on 1 January 2020 the period of 30 + 180 days shall commence

- Less than ₹15 billion: The RBI has not yet announced the reference date for such accounts and thus in case of defaults in such accounts, they can continue to rectify the same until the date a reference date is announced for them

- The resolution plan may involve any action, plan, reorganization including, but not limited to, regularization of the account by payment of all over dues by the borrower entity, sale of exposures to other entities, investors, change in ownership and restructuring

- Resolution plans (RP) involving restructuring change in ownership shall require independent credit evaluation by credit rating agencies appointed by the lenders. Only such plans that receive a credit opinion of RP4 or better for the residual debt, shall be considered for implementation. This would be relevant for PE/ strategic players who are trying to acquire companies in the pre-IBC mechanism and acquire ownership of the company. Their resolution plans need to obtain a credit opinion of RP4 for the residual debt. The change in ownership will also be deemed to be implemented when all documentation is completed, new capital structure is reflected in the books and no default subsists with any lenders

- Resolution plan that involves lenders exiting the exposure by assigning them to third party or a RP involving recovery action shall be deemed to be implemented only if the exposure to the borrower is fully extinguished. This would be relevant for varied structures being adopted through asset reconstruction companies etc. The plan would be implemented only if the exposure to the borrower is fully extinguished

Additional provisioning

In case the implementation of resolution is delayed beyond 180 days, lenders must undertake an additional provisioning of 20% of total outstanding. If implementation is delayed beyond 365 days from the end of the review period, an additional provision of 15% is to be made of the total outstanding (i.e. total additional provisioning of 35%). These additional provisions can be reversed if:

- The resolution plan involves payment of overdue by the borrower. Then only if there is no additional default for a period of six months from the date of clearing of overdue

- If the plan involves restructuring change in ownership outside IBC then upon its implementation

- If plan is pursued under IBC, then 50% when the application is filed under IBC and the balance when the application is admitted

The lenders would have stringent criteria to evaluate and approve plans outside the IBC. In case the lenders believe that there is no viable plan being offered, they may be inclined to push the company into IBC to avoid additional provisioning norms. This effectively takes this framework back to similar lines as promulgated earlier in the 12-Feb-18 circular that unless a viable resolution plan is offered to lenders under the pre-IBC regime, then the companies would have to be pushed into IBC. The only difference is that under the 12-Feb-18 circular, the lenders were statutorily required to pursue IBC at the end of the 180 day period. However, in this case, it is left to the commercial and economic judgment of the lenders. Lenders must undertake a balancing act between their commercial judgment of waiting beyond 180 day period versus additional provisioning requirements and supervisory review by the RBI

Insolvency proceedings

Notwithstanding anything contained in this framework, wherever necessary, the RBI will issue directions to banks for initiation of insolvency proceedings against borrowers for specific defaults. This framework shall not be available for borrower entities for which specific instructions have already been issued or are issued by the RBI to the banks for initiation of insolvency proceedings under IBC. “Lenders shall pursue” such cases as per the specific instructions issued to them. With this, the RBI may continue to refer specific cases like ‘top 12 cases’ to IBC from time-to-time

MSMEs

The above-mentioned provisions, except the SMA classifications and reporting requirements, shall not apply to MSMEs and they shall continue to be governed by the Framework for Revival and Rehabilitation of Micro, Small and Medium Enterprises (MSMEs) prescribed by the RBI vide RBI/ 2015-16/338 dated 17 March 2016

Withdrawal of existing resolution structures

The extant instructions on resolution of stressed assets such as:

- Framework for Revitalizing Distressed Assets;

- Corporate Debt Restructuring Scheme;

- Flexible Structuring of Existing Long-Term Project Loans;

- Strategic Debt Restructuring Scheme (SDR);

- Change in Ownership outside SDR; and

- Scheme for Sustainable Structuring of Stressed Assets (S4A)

stand withdrawn with immediate effect. Accordingly, the Joint Lenders’ Forum, as mandatory institutional mechanism for resolution of stressed accounts also stands discontinued. This brings utmost clarity to lenders and companies that, no other traditional framework can be pursued by lenders in dealing with stressed assets except this framework

Prudential norms applicable to resolution plans

The key norms are as follows –

- Asset classification: In case of restructuring, the accounts classified as “standard” shall be immediately downgraded as non-performing assets (NPAs), i.e., “sub-standard” to begin with

- Additional Finance: Any additional finance approved under the resolution plan (including plan approved under IBC) may be treated as “standard asset” during the monitoring period under the approved plan, provided the account demonstrates satisfactory performance during the monitoring period. If the restructured asset fails to perform satisfactorily during the monitoring period or does not qualify for upgradation at the end of the monitoring period, the additional finance shall be placed in the same asset classification category as the restructured debt. This is a critical factor for banks that are providing additional funding under the resolution plan proposed in IBC.

- Interim Finance: Similarly, any interim finance extended by the lenders to companies undergoing IBC may be treated as “standard asset” during the CIRP. Subsequently, upon approval of the RP the treatment of such interim finance shall be as per the norms applicable to additional finance, provided above. This clause may hamper situations where resolution professionals are trying to raise interim finance. The lenders would now weigh the possibility of failure of CIRP and consequent classification of interim finance provided by them.

- Conversion of Principal into Debt Equity: Asset classification, provisioning and valuation norms would also apply to converted debt/ debentures/ bonds/ ZCBs/ LCBs issued as part of restructuring/ resolution plan. The framework also provides valuation norms for equity/ preference shares issued consequent to the resolution plan.

- Change in Ownership: In case of change in ownership of the borrower entity, the credit facilities of the concerned borrowing entities may be continued/ upgraded as “standard” after the change in ownership is implemented, either under the IBC or under this framework. If the change in ownership is implemented under this framework, then the classification as ‘standard’ shall be subject to the following conditions:

- Acquirer shouldn’t be disqualified under section 29A of IBC

- ‘New promoter’ should not be a person/ entity/ subsidiary/ associate etc. (domestic as well as overseas), from the existing promoter/ promoter group (as defined in SEBI ICDR).

- The new promoter shall have acquired at least 26% of paid up equity capital as well as voting rights of the borrower entity and shall be the single largest shareholder of the borrower entity.

- The new promoter shall be in “control” of the borrower entity (‘control’ as defined in Companies Act and SEBI).

- The conditions for implementation of RP as provided in this framework are complied with.

- Sale and Leaseback transactions: A sale and leaseback transaction of the assets of a borrower or other transactions of similar nature will be treated as an event of restructuring for the purpose of asset classification and provisioning in the books of lenders with regard to the residual debt of the seller as well as the debt of the buyer, if the seller is in financial difficulty and more than 50% of the revenues of the buyer from the specific asset are dependent upon the cash flows from the seller and 25% or more of the loans availed by the buyer for the purchase of the specific asset are funded by the lenders who already have a credit exposure to the seller

- Refinancing of Exposure to Borrowers: If borrowings/ export advances for the purpose of repayment/ refinancing of loans denominated in same/ another currency are obtained from lenders who are part of the Indian banking system or with the support from the Indian banking system in the form of Guarantees/ SBLC / Letters of Comfort, etc., such events shall be treated as “restructuring” if the borrower concerned is under financial difficulty.

- Regulatory Exemptions: RBI Acquisition of non-SLR securities by conversion of debt is exempted from the restrictions and the prudential limit on investment in unlisted non-SLR securities prescribed by the RBI

- Acquisition of shares due to conversion of debt to equity during a restructuring process will be exempted from regulatory ceilings/restrictions on capital market exposures, investment in para-banking activities and intra-group exposure. However, these will require reporting to the RBI and disclosure by banks in Annual Financial Statements and it will be subject to compliance with the provisions of section 19(2) of the Banking Regulation Act, 1949

- Regulatory Exemptions – SEBI

- Exemptions available under SEBI ICDR for restructuring as per regulations issued by the RBI shall continue to apply.

- A new pricing methodology is prescribed in the framework which shall apply with respect to sub-regulation 158(6)(a) of the SEBI ICDR. The reference date in such cases shall be the date on which the bank approves the restructuring scheme. In the case of conversion of convertible securities into equity, the “reference date” shall be the date on which the bank approves the conversion of the convertible securities into equities

Indirect Tax

CBIC augments powers of NAA, prescribes manner of valuation of Kerala cess and mentions QR code in tax invoices

The CGST Rules, 2017 have been amended with immediate effect (unless specified otherwise). The key areas of impact are as follows:

- Anti-profiteering related investigations

- The Standing Committee can now apply for an extension of one month from the National Anti-Profiteering Authority (NAA), post completion of the two month time period allowed for examining any complaint received.

- Time limit to complete investigations by the Director General of Anti-profiteering (DGAP) from the date of receipt of reference from the Standing Committee has been increased to six months, which was earlier limited to within three months. Similarly, the NAA can now issue its order within a period of six months (instead of three months) from the date of receipt of report from the DGAP.

- If the NAA has reasons to believe that there has been contravention of the provisions of anti-profiteering law in respect of goods or services not covered in the report issued by the DGAP, the NAA can direct the DGAP to renew its enquiry qua such other goods or services. Such investigation by DGAP is deemed as a new investigation.

- The NAA now has the power to summon any person in relation to an enquiry, which was earlier limited to the DGAP or its officers.

- NAA may order a registered person who has been adjudicated to have profiteered to deposit interest at the rate of 18% along with the amount determined.

- Computation of Kerala cess: Kerala cess will be calculated on the (same) value of supply determined as per section 15 of the CGST Act, 2017.

- Invoicing: Tax invoice/ bill of supply must include the Quick Response (QR) code with effect from a date notified later.

- Domestic procurements by duty free shops: Retail outlets established in the departure area of an international airport, selling indigenous goods to an outgoing international tourist, will be eligible to claim refund of tax paid by it on purchase of such goods; subject to specified conditions.

- Tax payment: The facility of transfer of tax, interest, penalty, fees from one account head to another in the electronic cash ledger can be done by filing FORM GST PMT – 09.

- E-way bills: Provisions relating to the validity of e-way bills extended to goods transported through multimodal transport, in which at least one leg involves transportation by ship.

PwC Comments: While the NAA’s term was extended by two years in the thirty fifth GST Council meeting, the DGAP and NAA now have additional time of three months each to complete investigations for new and pending cases. The new power of directing the DGAP to conduct investigations in relation to goods or services not covered in their report may now possibly extend enquiries to situations outside the original complaint. Therefore, the scope of anti-profiteering proceedings has now widened, possibly in response to a large number of enquiries currently underway and challenges faced by the NAA. This could also heighten the level of scrutiny faced by the industry. The ambiguity over the computation of Kerala cess has been clarified to avoid a tax-on-tax situation. The empowering provision of requiring QR codes in invoices is in tandem with the introduction of e-invoicing. The provision for tax-free domestic procurements by duty free shops has been a long-term demand of industry.

GST Council extends the date of filing annual return and audit report, introduces transition plan to new GST returns and extends the tenure of National Anti-profiteering Authority

The GST Council, in its thirty fifth meeting, described the phase-wise implementation of the new return system introduced. The Council extended the due date of furnishing annual return and reconciliation statement, and extended the tenure of the National Anti-profiteering Authority (NAA) by two years. Further, the Council also decided to roll out electronic invoicing (e-invoicing) in a phase-wise manner from January 2020. GST rate-related changes on electric vehicles, solar power generating systems and wind turbines are to be examined by the Fitment Committee and to be taken up for discussion in the next Council meeting.

The major decisions by the Council at the meeting are summarized as below:

- The new return system [FORM GST ANX-1 & ANX-2] will be implemented on a trial basis from July 2019 to September 2019. Simultaneously, taxpayers will continue to file FORM GSTR-1 and GSTR-3B until October 2019.

- From October 2019, FORM GSTR-1 (details for outward supplies) will be compulsorily replaced by FORM GST ANX-1 and taxpayers can upload invoices in FORM GST ANX-1 on a continuous basis.

- For October and November 2019, large taxpayers (i.e. those having an aggregate turnover of more than ₹50 million in the previous year) will continue to file FORM GSTR-3B. However, small taxpayers will stop filing FORM GSTR-3B and start filing FORM GSTR PMT-08 from October 2019.

- Both large and small taxpayers will file their first FORM GST-RET-01 in January 2020 for the month of December 2019 and the quarter of October to December 2019, respectively.

- From January 2020, FORM GSTR-3B is to be completely phased out and taxpayers will file FORM GST PMT-08.

- The due date for filing the annual return in FORM GSTR-9/9A and the audit report/ reconciliation statement in FORM GSTR-9C for financial year (FY) 2017-2018 has been extended until 31 August 2019.

- The time limit for taxpayers to file an application in FORM GST CMP-02 to opt for the composition scheme has been extended until 1 July 2019.

- The introduction of an e-invoicing system in a phase-wise manner for B2B transactions is to be rolled out from January 2020.

- The tenure of NAA has been extended by two years.

PwC Comments: The decisions taken by the GST Council are in line with industry expectations, which seek to improve GST-related processes. The decision to extend the timelines for filing annual return and audit reports for FY 2017-18 is a welcome move, as the industry was not prepared for the current deadline. The road map for the transition to the new simplified return system will require sufficient time as the taxpayers prepare for and adopt the new system. It will be interesting to see the roll out of the e-invoicing model, which will initially be implemented for B2B transactions only. If this experiment is successful, one could see it getting extended to the B2C segment as well.

Forthcoming Events

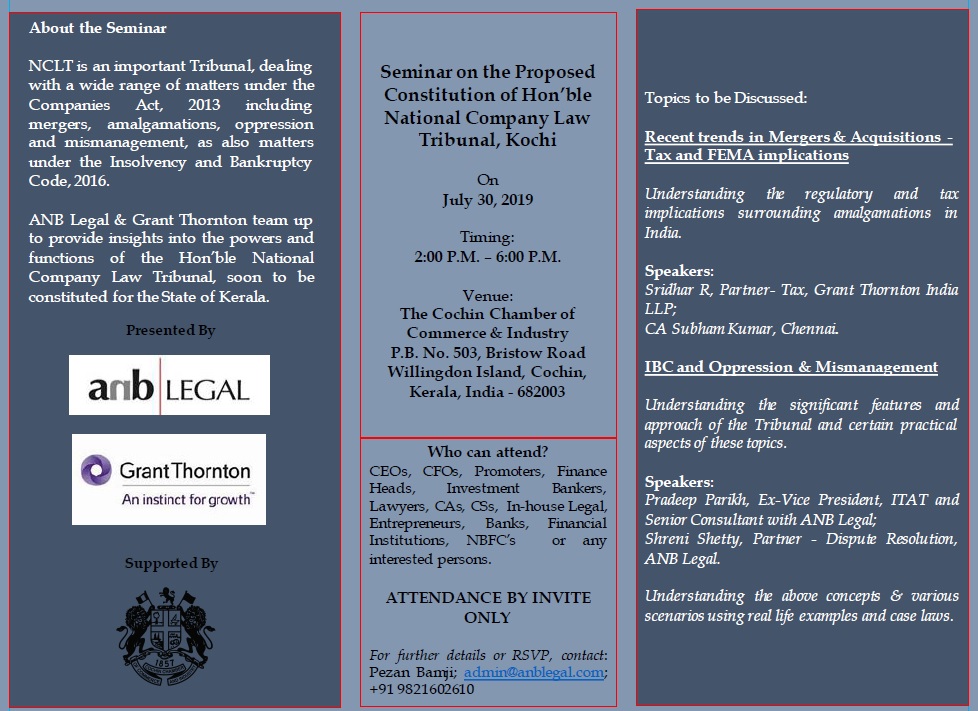

Seminar on the Proposed Constitution of Hon'ble National Company Law Tribunal, Kochi

Cochin Chamber Hall, Willingdon Island, Ernakulam | 1400hrs - 1800hrs | 30.07.2019

The Chamber, in association with ‘anb Legal, Mumbai and Grant Thornton, Cochin’, will be organizing a Seminar on the Proposed Constitution of the Hon’ble National Company Law Tribunal, Kochi on Tuesday, 30th July, 2019.

The Session will be held between 2.00 p.m. and 6.00 p.m. on that day in the Conference Hall of the Cochin Chamber, Willingdon Island, Cochin -3.

We trust that you will attend this programme and/or depute someone from your Office to attend.

While there is no participation fee for the programme, online registration is mandatory.

Click here to register.

CEO FORUM 2019 - 8th Breakfast Meeting

Hotel Taj Gateway, Ernakulam | 0800hrs - 1000hrs | 02.08.2019

The 8th Breakfast Meeting under the aegis of the Chamber’s CEO FORUM 2019 will be held on Friday, the 2nd of August 2019 between 8.00 am and 10.00 am at the Anchor Hall, Taj Gateway Hotel, Marine Drive, Ernakulam.

The Speaker at this Session will be Mr. K. Jayakumar I.A.S. (Retd.), Director, Institute of Management in Government, Kerala who will speak on “Commerce without Conscience: A Matter of National Concern”

Click Here to register for this programme

From........... the Research Wing

REPORT ON SELECT COMMITTEE'S PUBLIC CONSULTATION ON

THE KERALA FARMERS’ WELFARE FUND BILL, 2018

JULY 19, 2019, THODUPUZHA

The Kerala Legislative Assembly’s Select Committee hosted a ‘public consultation’ meeting at Thodupuzha Town Hall on the 19th July 2019, to deliberate the changes required in the Kerala Farmers’ Welfare Fund Bill, 2018.

Inaugurating the Session, the Hon’ble Agriculture Minister V S Sunilkumar (Chairman of the Select Committee on Kerala Farmers’ Welfare Fund Bill,2018) said that the purpose of the hearing is to seek and incorporate inputs of the relevant stakeholders before the Bill is finalized.

The meeting was attended by farmers, organisations working for the welfare of farmers and agricultural labourers, social workers etc. who deposed before the Committee and suggested changes to the present policy framework.

The event was dominated by complaints even after multiple reminders from Minister’s side on restricting the discussion to the contents of the Bill.

At this juncture, the Committee found the Chamber’s submission relevant and appreciated the clause wise submissions submitted by the Chamber. The Select Committee was requested to consider the clause wise comments for institutionalising a comprehensive legislation for farmers welfare in the ten minute slot given for individual speakers. The opportunity given was also utilised to highlight the need for expediting the much awaited ‘Plantation Policy’ and the need for extending welfare facilities like schools, hospitals etc. to the plantation workers.

Overview of responses

- Increase the income, land limit requirement in the definition of the word “farmer”.

- Better clarity required in the definitions of the words “agriculture” , “family”, “non-official director”, “allied-sectors” , “expert” etc.

- Constitution of the Board should be explained properly detailing the process of selection of the 9 farmer members, inclusion of other non-official members working in the agriculture sector etc.

- Special package and/or policy for the plantation sector.

- Defining the pension amount.

- Extending low premium insurance for plantation crops.

- Create regular awareness initiatives to promote the implementation of crop insurance schemes instituted by the Government.

- Initiate health insurance for farmers and their dependents.

- Make Government Offices farmer friendly.

- Facilitate reforms that promote youth in taking up farming as a means of livelihood

- Incorporate modules on farming in school syllabuses

- Efficient functioning of Krishi Bhavans and Procurement Centers

- Need for better coordination between various Government Agencies and Voluntary Organizations working for the welfare of farmers

1. The Chamber submitted comments on the Kerala Farmers’ Welfare Fund Bill, 2018. Through this submission, the Chamber re-emphasised on its commitment towards the overall development of Kochi and Kerala. The submission critiques the version of the bill by suggesting necessary amendments and additions that will strengthen the foundation of this social welfare legislation. The Chamber has advocated for a non-bureaucratic centric composition of Farmers Welfare Fund Board, adoption of participatory processes, adoption of gender neutral language, inclusion of provisions for promotion and dissemination of research content etc. The Chamber also requested the Government to expedite the process of finalising a Comprehensive Policy for Plantation Sector.

The detailed submission is available in the Chamber

2. The Research Wing submitted comments on the Union Budget 2019-20 as a post budget memorandum. The submission highlighted issues like the need for abolition of cess, impact of corporate tax and individual surcharge, upgradation of India’s domestic EV capacity etc.

POLICY DEVELOPMENTS CORNER

- The Department for Promotion of Industry and Internal Trade (DPIIT) will soon float a Draft National Retail Policy to seek the views of stakeholders. This will be a comprehensive policy aimed at promoting the growth of 65 million small traders in the country.

- Ministry of Housing and Urban Affairs has uploaded the draft Model Tenancy Act, 2019, for public comments. Draft available at http://mohua.gov.in/cms/draftmodificationact.php

- Ministry of Health and Family Welfare released the National Digital Health Blueprint for comments on 15th July 2019. Draft available at https://mohfw.gov.in/sites/default/files/National_Digital_Health_Blueprint_Report_comments_invited.pdf

Exclusive EXIM Statistics - Sample Reports

Chamber in the News

UNION BUDGET 2019-2020 | Highlights

SEVERAL TAX PROPOSALS AIM TO PROMOTE INVESTMENTS IN START-UPS AND SUNRISE INDUSTRIES IN THE COUNTRY

LOWER 25% CORPORATE TAX RATE IS TO BE APPLICABLE TO THOSE WITH ANNUAL TURNOVER UPTO RS.400 CRORE INSTEAD OF THE CURRENT LIMIT OF RS.250 CRORE

INCREASE IN SURCHARGE BY 3% FOR THOSE WITH TAXABLE INCOME BETWEEN 2-5 CRORE RUPEES AND BY 5% TO THOSE WITH INCOME OF OVER RUPEES 5 CRORE

DIGITAL ECONOMY TO BE PROMOTED. A TDS OF 2% ON CASH WITHDRAWAL EXCEEDING RS.1 CRORE IN A YEAR FROM A BANK ACCOUNT IS PROPOSED

BOTH DIRECT AND INDIRECT TAX INCENTIVES FOR PROMOTION OF ELECTRIC VEHICLES IN A BIG WAY ANNOUNCED

SEVERAL CUSTOMS DUTY PROPOSALS ANNOUNCED FOR PROMOTING MAKE IN INDIA, REDUCING IMPORT DEPENDENCE, PROTECTION TO MSME SECTOR AND PROMOTING CLEAN ENERGY

SPECIAL ADDITIONAL EXCISE DUTY AND ROAD & INFRASTRUCTURE CESS OF ONE RUPEE EACH ON PETROL AND DIESEL PROPOSED

CUSTOMS DUTY ON GOLD AND OTHER PRECIOUS METALS INCREASED FROM 10% TO 12.5%

PROMOTING INVESTMENTS

Several of the tax proposals announced by the Union Minister of Finance and Corporate Affairs Smt. Nirmala Sitharaman, while presenting the Union Budget 2019-20 in Parliament, are aimed at promoting investments in Sunrise Advanced Technology industries and in Start-ups. To boost economic growth and Make in India, a Scheme is to be launched to invite global companies through a transparent competitive bidding to set up mega-manufacturing plants in Sunrise and Advanced Technology Areas such as Semi-conductor Fabrication (FAB), Solar Photo Voltaic cells, Lithium storage batteries, Solar electric charging infrastructure, Computer Servers, Laptops, etc. Such global companies are to be given investment linked Income Tax exemptions under Section 35 AD of the Income Tax Act, and other Indirect Tax benefits.

The Finance Minister, Smt. Nirmala Sitharaman presenting her maiden budget, said “to resolve the so-called angel tax‟ issue, the start-ups and their investors who file requisite declarations and provide information in their returns will not be subjected to any kind of scrutiny in respect of valuations of share premiums. The issue of establishing identity of the investor and source of his funds will be resolved by putting in place a mechanism of e-verification. With this, the funds raised by start-ups will not require any kind of scrutiny from the Income Tax Department. Special administrative arrangements shall be made by CBDT for pending assessments of start-ups and redressal of their grievances. No inquiry or verification in such cases can be carried out by the Assessing Officer without obtaining approval of his supervisory officer. ” Start-ups will not be required to justify fair market value of their shares issued to Category-II Alternative Investment Funds also. Valuation of shares issued to these funds shall be beyond the scope of income tax scrutiny. She said it is also proposed to relax some of the conditions for carry forward and set off of losses in the case of start-ups. It is also proposed to extend the period of exemption of capital gains arising from sale of residential house for investment in start-ups up to 31.3.2021.

AFFORDABLE HOUSING

Affordable housing gets further encouragement in the form of additional tax deduction of Rs.1.5 lakh beyond Rs. 2 lakh of interest paid on loans borrowed upto 31st March, 2020 for purchase of an affordable house valued up to Rs. 45 lakh. The Finance Minister said “thus a person purchasing an affordable house will now get an enhanced interest deduction up to Rs. 3.5 lakh. This will translate into a benefit of around Rs 7 lakh to the middle class home-buyers over their loan period of 15 years.”

MODERNISATION OF TAX ADMINISTRATION

Expressing thanks to the taxpayer, including self-employed, small traders, salary earners and senior citizens, Smt. Sitharaman said that “the direct tax revenue has significantly increased over the past couple of years. It has increased by over 78% from Rs. 6.38 lakh crore in Financial Year 2013-14 to around Rs. 11.37 lakh crore in Financial Year 2018-19. It is now growing at double digit rate every year.”

Saying that those in the highest income brackets need to contribute more to the nation‟s development and for revenue mobilization, the Finance Minister announced enhancement of surcharge of 3 % on individuals having taxable income from Rs. 2 crore to Rs. 5 crore and 7 % for those with taxable income of Rs. 5 crore and above.

At the same time, several measures are announced to leverage technology to make tax administration and tax payment easier. Those without Pan Card are now allowed to file income tax returns by quoting their Aadhar number.

Pre-filled tax returns would be made available to taxpayers with details of salary income, capital gains from securities, bank interests, and dividends and tax deductions etc,. Information regarding these incomes will be collected from the concerned sources such as Banks, Stock exchanges, mutual funds, EPFO, State Registration Departments etc.

A Scheme of Faceless Assessment in electronic mode involving no human interface is being launched this year in a phased manner. To start with, such e-assessments shall be carried-out in cases requiring verification of certain specified transactions or discrepancies. Cases selected for scrutiny shall be allocated to assessment units in a random manner and notices shall be issued electronically by a Central Cell, without disclosing the name, designation or location of the Assessing Officer. The Central Cell shall be the single point of contact between the taxpayer and the Department.

CORPORATE TAX

On Corporate Tax, the Minister said, “we continue with phased reduction in rates. Currently, the lower rate of 25 % is only applicable to companies having annual turnover up to Rs 250 Crore. This is proposed to be widened to include all companies having annual turnover up to Rs 400 crore. This would cover 99.3% of the companies. With this only, 0.7 % of companies will remain outside this rate”.

DIGITAL PAYMENTS

To further encourage digital payments practices in the country or discourage cash payments, the Finance Minister announced several measures which include discouraging the practice of making business payments in cash, proposal to levy TDS of 2% on cash withdrawal exceeding Rs.1 crore in a year from a bank account. Business establishments with annual turnover more than Rs. 50 crore shall offer low cost digital modes of payment to their customers and no charges or Merchant Discount Rate is to be imposed on customers as well as merchants. RBI and Banks will absorb these costs from the savings that will accrue to them on account of handling less cash as people move to these digital modes of payment. Necessary amendments are being made in the Income Tax Act and the Payments and Settlement Systems Act, 2007 to give effect to these provisions.

ELECTRIC VEHICLES

For promotion of electric vehicles in a big way in the country, both direct and indirect tax incentives are announced. The Finance Minister said –“considering India‟s large consumer base, we aim to envision India as a global hub of manufacturing of Electric Vehicles”. Inclusion of Solar storage batteries and charging infrastructure in the above Scheme will boost our efforts, she said. The Finance Minister announced that the “Government has already moved GST Council to lower the GST rate on electric vehicles from 12% to 5%. Also to make electric vehicle affordable to consumers, our Government will provide additional income tax deduction of Rs 1.5 lakh on the interest paid on loans taken to purchase electric vehicles. This amounts to a benefit of around Rs 2.5 lakh over the loan period to the taxpayers who take loans to purchase electric vehicle”. The Minister while proposing increase in customs duties on automobile and automobile parts, had provided for exemption of customs duties on certain parts of electric vehicles.

CUSTOM DUTY PROPOSALS

In general, other Customs Duty proposals are aimed at promoting Make in India, reducing import dependence, protection to MSME sector, promoting clean energy, curbing non-essential imports and correcting inversions.

To provide level playing field to domestic industry, custom duties are enhanced on 36 items including :

- Cashew kernels

- Fatty acids. Acid oils from refining used in manufacture of oleochemicals and soaps

- Poly Vinyl Chloride

- Floor cover of plastics, Wall or ceiling coverings of plastics

- Articles of plastic

- Butyl Rubber

- Chlorobutyl rubber or bromobutyl rubber

- Paper for newsprint and magazines

- Printed books (including covers for printed books) and printed manuals

- Water blocking tapes for manufacture of optical fiber cables

- Ceramic roofing tiles and ceramic flags and pavings, hearth or wall tiles etc.

- Stainless steel products

- Wire of other alloy steel (other than INVAR)

- Base metal fittings, mountings and similar articles suitable for furniture, doors, staircases, windows, blinds, hinge for auto mobiles

- Indoor and outdoor unit of split –system air conditioner

- Stone crushing (cone type) plants for the construction of roads

- Charger/ power adapter of CCTV camera/ IP camera and DVR / NVR

- Loudspeaker

- Digital Video Recorder (DVR) and Network Video Recorder (NVR)

- CCTV camera and IP camera

- Optical Fibres, optical fibre bundles and cables

- Friction material and articles thereof (for example, sheets, rolls, strips, segments, discs, washers, pads), not mounted, for brakes, for clutches or the like, with a basis of asbestos, of other mineral substances or of cellulose, whether or not combined with textile or other materials.

- Glass mirrors, whether or not framed, including rear-view mirrors

- Locks of a kind used in motor vehicles

- Catalytic Converter

- Oil or petrol filters for internal combustion engines

- Intake air filters for internal combustion engines

- Lighting or visual signaling equipment of a kind used in bicycles or motor vehicles

- Horns for vehicle

- Other visual or sound signalling equipment for bicycle and motor vehicle

- Parts of visual or sound signaling equipment, windscreen wipers, defrosters and demisters of a kind used in cycles or motor vehicles

- Windscreen wipers, defrosters and demisters, Sealed beam lamp units, Other lamps for automobiles.

- Completely Built Unit (CBU)of vehiclesfalling under heading 8702, 8704

- Chassis fitted with engines, for the motor vehicles of headings 8701 to 8705

- Bodies (including cabs), for the motor vehicles of headings 8701 to 8705

- Naphtha

- Methyloxirane (Propylene Oxide)

- Ethylene dichloride (EDC)

- Raw materials used in manufacture of Preform of Silica: -a) Silicon Tetra Chloride

b) Germanium Tetra Chloride

c) Refrigerated Helium Liquid

d)Silica Rods

e) Silica Tubes* Wool fibre, Wool Tops

Inputs for the manufacture of CRGO steel: –

a) MgO coated cold rolled steel coils

b) Hot rolled coils

c) Cold-rolled MgO coated and annealed steel

d) Hot rolled annealed and pickled coils

e) Cold rolled full hard

- Amorphous alloy ribbon

- Cobalt mattes and other intermediate products of cobalt metallurgy