President's Letter

Dear Friends,

Onam has just passed and unlike in the past, the sights, smells and sounds of this festival were missing. From online stores and high-street boutiques to vegetable sellers, textiles, gold showrooms, white goods sales and auto manufacturers, no effort was spared to get consumers to loosen their purse strings during the festival season, to no avail. The Covid 19 spread has literally choked the economy and forced shoppers to stay away from markets leaving only memories of yesteryear Onam celebrations.

The business sector in the state is passing through a really trying period. The closure of businesses on account of the nation-wide lockdown and setting up containment zones have resulted in job losses, businesses collapsing and total chaos since 95 per cent of the businesses in Kerala fall under the MSME category. The tourism industry is among the worst hit. Their total loss from March to September 2020 is estimated at Rs 20,000 crore. The demand slowdown is expected to continue till September 2021.

Kerala’s usual economic pillars— from enterprises to remittances to tourism— have been crumbling and in distress amid the pandemic. Many traditional shopping complexes have become vacant and unviable on account of the prolonged lockdowns. As lakhs of diaspora workers are repatriated, the State has projected a 15% fall in the ₹1 trillion remittance pipeline in 2020. Tens of thousands of hotels and other tourism hubs, otherwise buzzing with foreign tourists enjoying the State’s spectacular monsoon rains, remain in a vicious cycle of job loss and debts, as air travel and other modes of transportation remain unavailable. Not to mention the fear of contracting the corona virus.

However, for a clutch of IT companies and start ups in Kerala, there is palpable excitement in the air, owing to a boost in business. Like elsewhere, there is an increased demand for technology solutions on every front owing to the pandemic.

Coming to this month’s activities, the Chamber organised an Online Session on ‘Consumer Protection 2.0’ on Wednesday, 5th August 2020 on the Google Meet Platform. Prashanth S. Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers) Bangalore and Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers) Bangalore were the Speakers at the meeting. The session detailed the changes, nuances and the new measures that are to be taken by both buyers and sellers, comparisons between the 1986 Act and the 2019 Act, the interplay with other enactments, liabilities and responsibilities and the do’s and don’ts for industry and consumers. It was a very informative session and was reasonably well attended.

On the 8th of August we conducted a Virtual CEO Forum Meeting. We had Sri. A.P.M. Mohammed Hanish I.A.S., Principal Secretary II, Department of Industries and Commerce, Government of Kerala who spoke on “The Emerging Economic Opportunities in the post Covid Scenario.” The session was well appreciated by all the attendees.

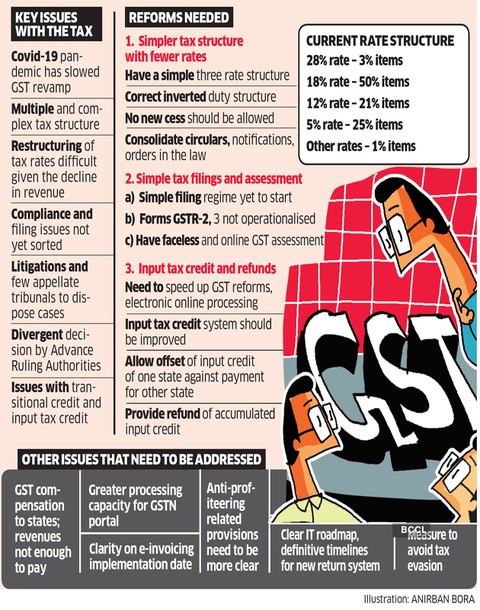

The Goods and Services Tax (GST) regime has completed 3 years. Hailed as the single-biggest tax reform, the GST was rolled out subsuming 17 existing indirect taxes including the excise duty and sales tax. Although the initial period was very stressful for the trade and the Government, over a period of time it has stabilised to a large extent, however many issues still remain unresolved. The Chamber organised an Online Session on ‘3 Years of GST’ on Friday, 21st August 2020 on the Zoom Platform. Justice P.B. Sureshkumar, High Court of Kerala delivered the Inaugural Address at the Session. The Session was handled by Tax Expert, G. Shivadass, Senior Advocate, High Court of Karnataka. We also had Ms. Devika Rajagopal, Assistant Manager – Taxation & Finance, Harrisons Malayalam Limited, who spoke on behalf of the Industry about the pain points that businesses and trade face. The session was attended by 60 participants from various organisations.

The next Virtual Meeting of the Cochin Chamber’s CEO FORUM will be held on Friday, 4th September 2020 on the Zoom Platform. Shri Ravindra Kumar I.R.S., Principal Chief Commissioner of Income Tax, Kerala Region will address the Forum on “Faceless Assessment Scheme and Tax Payers’ Charter”. I trust that you will make use of this opportunity to the fullest.

We don’t know how long the COVID-19 pandemic will last, but one thing is clear – this is our chance to reset, to create a fairer, stronger, safer and cleaner country. In doing so, we can build resilience to future pandemics and to other risks, like climate change, natural disasters and the like.

Wishing you all a safe and happy festive season

Stay Safe Everyone!!!

V Venugopal

Quote

Fine Points

Recent Events

Virtual Meeting on Consumer Protection 2.0 | 05.08.2020

The Cochin Chamber of Commerce and Industry organised an Online Session on ‘Consumer Protection 2.0’ on Wednesday, 5th August 2020, on the Google Meet Platform.

Prashanth S. Shivadass, Advocate and Founder, Shivadass & Shivadass (Law Chambers) Bangalore and Jomol Joy, Advocate and Of-Counsel, Shivadass & Shivadass (Law Chambers) Bangalore were the Speakers at the meeting.

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

The session covered, in detail, the changes, nuances and the new measures that are to be taken by both buyers and sellers, Comparisons between the 1986 Act and the 2019 Act, Interplay with other enactments, Liabilities and Responsibilities and the Do’s and don’ts for industry and consumers.

Mr. Shivadass said that this new Act will empower consumers and help them in protecting their rights through its various notified rules and provisions like the Consumer Protection Councils, the Consumer Disputes Redressal Commissions, Mediation, Product Liability and punishment for manufacture or sale of products containing adulterant / spurious goods.

He said that under the new law the CCPA (Central Consumer Protection Authority) will be empowered to conduct investigations into violations of consumer rights and institute complaints / prosecution, order recall of unsafe goods and services, order discontinuance of unfair trade practices and misleading advertisements, impose penalties on manufacturers/endorsers/publishers of misleading advertisements. Mr. Shivadass further said that the rules for prevention of unfair trade practice by e-commerce platforms will also be covered under this Act.

Ms. Joy said under this Act every e-commerce entity is required to provide information relating to return, refund, exchange, warranty and guarantee, delivery and shipment, modes of payment, grievance redressal mechanism, payment methods, security of payment methods, charge-back options, etc. including country of origin which are necessary for enabling the consumer to make an informed decision at the pre-purchase stage on its platform. She said that e-commerce platforms have to acknowledge the receipt of any consumer complaint within forty-eight hours and redress the complaint within one month from the date of receipt under this Act.

Mr. Shivadass further said that the new Act provides for simplifying the consumer dispute adjudication process in the consumer commissions, which include, among others, empowerment of the State and District Commissions to review their own orders, enabling a consumer to file complaints electronically and file complaints in consumer Commissions that have jurisdiction over the place of his residence, videoconferencing for hearing and deemed admissibility of complaints if the question of admissibility is not decided within the specified period of 21 days.

Mr. Shivadass further said that the new Act also introduces the concept of product liability and brings within its scope, the product manufacturer, product service provider and product seller, for any claim for compensation. The Act provides for punishment by a competent Court for manufacture or sale of adulterant/spurious goods. He also added that the new Act provides for mediation as an Alternate Dispute Resolution mechanism, making the process of dispute adjudication simpler and quicker. This will help with the speedier resolution of disputes and reduce pressure on consumer courts, which already have numerous cases pending before them.

Talking about the penalties of misleading advertisements, Ms. Joy said that the CCPA may impose a penalty of up to INR 1,000,000 (Indian Rupees One Million) on a manufacturer or an endorser, for a false or misleading advertisement. The CCPA may also sentence them to imprisonment for up to 2 (two) years for the same. In case of a subsequent offence, the fine may extend to INR 5,000,000 (Indian Rupees Five Million) and imprisonment of up to 5 (five) years.

In his concluding remarks, Mr. Shivadass said that in earlier Consumer Protection Act, 1986 a single point access to justice was given, which is also time consuming. The new Act has been introduced after many amendments to provide protection to buyers not only from traditional sellers but also from the new e-commerce retailers/platforms.

Following this, there was a brief discussion wherein the Speaker clarified the issues raised by the participants.

The meeting ended with the Deputy Secretary of the Chamber, Mr. Manu Varghese thanking everyone for having participated in the meeting.

CEO FORUM 2020 - Emerging Economic Opportunities in the Post COVID Scenario | 08.08.2020

The Cochin Chamber of Commerce and Industry conducted a Virtual CEO Forum Meeting on Saturday, 8th of August, 2020.

Sri. A.P.M. Mohammed Hanish I.A.S., Principal Secretary II, Department of Industries and Commerce, Government of Kerala was the Speaker at the meeting. The topic of his address was “The Emerging Economic Opportunities in the post Covid Scenario.”

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

Commencing his address, Mr. Hanish said that though Covid has turned out to be the biggest crisis of our time, Kerala can use the adverse situation to its advantage through some out-of-the-box strategies to attract investments and create jobs locally.

In India, the strangulation of business activities has caused industries to bear the brunt of rising operational costs in the face of reductions in orders. Against this backdrop, the Government and the business ecosystem stakeholders are working in a dynamic synergy to mitigate the socio-economic fallout and set the nation down the path to recuperation, he said.

Mr. Hanish said that every challenge brings an opportunity along with it and overcoming challenges is closely connected with utilising the opportunities that emerge alongside. The fact that amid all these challenges, the entire Government machinery and society as a whole – including voluntary organisations – have been in perfect sync makes the State stand out as a safe and secure destination for investments. In this backdrop, he said that the Government of Kerala has decided to grant all major industrial licenses and permits within one week of application, with the condition that entrepreneurs will complete due procedures within a year. Multi-modal Logistics Centres are sought to be established in Thiruvananthapuram, Ernakulam, Kozhikode and Kannur connecting the airport, port, railways and roads in these cities. Once this plan materialises, the State could emerge as a major player in international trade and commerce. Logistics parks are to be set up in different parts of the State to take advantage of the opportunities in export and import, he added.

Mr. Hanish further said that if there is one sector whose significance has been thrown into sharp relief by the incumbent crisis, it is the healthcare and biotech. While medical professionals and supporting staff are engaged on the front-lines battling the virus, researchers and scientists are occupied in an equally critical pursuit of developing a vaccine that will effectively put an end to the viral outbreak.

In the wake of the booming demand, tech players across sectors are rising to the occasion. Edtech is a key example, he said. Today, millions of educators and students are connecting online to continue with their learning activities. New-age players are closely following this development and continuously improvising to ensure seamless online engagement. This trend will not die down in the foreseeable future, he said.

Every business will now be technology-enabled. Rather, boundaries between business and technology will be blurred. People will travel less, consumer spending will come down. Mr. Hanish said that this is a huge advantage for Kerala if we can take advantage of the situation as most companies look to rationalise the costs. Working remotely and virtual working will be the norm, and that will be where the future of jobs lie. We will see remote working in healthcare, remote education, remote banking and finance, etc. he said.

Mr. Hanish said that agri-innovations, entrepreneurship, and technology need to be promoted to improve production and productivity post COVID-19. Moreover, precision farming methods will pave the way for optimising cost of production and productivity. The Micro, Small and Medium Enterprises (MSME) sector, which has been badly affected by the COVID-19 crisis, is making an effort to promote agribusiness and agri-industrial sector.

Pharmaceuticals, biotech, medical supplies and equipment and related infrastructure for health sector capacity building, supply and value chain is a vital multi-sectoral cluster to create with all stakeholders — private and public. Consumer durables, construction materials, electronics, engineering goods, IT, speciality textiles and garments, AI and robotics are other promising areas, he said.

During this ‘Corona Shock’, Kerala has realised that it is imperative to think outside the box. Having an abundance of human resources, which will be further enriched with the influx of returned migrants, the State is relying on its strengths and going all out to woo investments so that jobs and incomes in whatever manner possible, are ensured to its people.

Concluding the meeting, Mr. Hanish said that if Kerala or even India sees a recovery of all those infected by the COVID-19, it can’t be said that we have successfully overcome the danger it poses; because till date, no specialised treatment protocol has been devised for COVID-19 and a vaccine is yet to be invented as well. Hence, the presence of SARS-CoV-2 anywhere in the world is a threat to the entire world as such. Therefore, what is required now is to be prepared with the ‘worst case scenario’ in mind. Based on the information we have till date, those countries or regions that have prepared for the most adverse situations are the ones that have been able to resist COVID-19 better than the rest. Even if the health emergency is mitigated, experts say that the economic fallout of this pandemic, across sectors, will linger for a few more years.

Following this, there was a brief discussion wherein the Speaker clarified the issues raised by the participants.

The meeting ended with the Vice President of the Chamber, Mr. K Harikumar thanking everyone for having participated in the meeting.

Virtual Meeting on 3 Years of GST | 21.08.2020

The Cochin Chamber of Commerce and Industry organised an Online Session on ‘3 Years of GST’ on Friday, 21st August 2020 on the Zoom Platform.

Hon’ble Justice P.B. Suresh Kumar of the High Court of Kerala delivered the Inaugural Address at the Session. The Session was handled by Tax Expert, G. Shivadass, Senior Advocate, High Court of Karnataka. Ms. Devika Rajagopal, Assistant Manager – Taxation & Finance, Harrisons Malayalam Limited, spoke on behalf of the Industry outlining the pain points that businesses and trade face today.

The President of the Chamber Mr. V Venugopal welcomed the participants to the virtual meeting.

Inaugurating the Webinar, Justice Suresh Kumar appreciated the Chamber for consistently organizing such relevant sessions for trade and industry. He said that the introduction of GST has been a

game-changer for the Indian economy as it has replaced the multi-layered, complex indirect tax structure with a simple, transparent and technology–driven tax regime. The GST collections have been hit this year as the raging Covid19 pandemic and resultant lockdown have derailed the Indian and global economy. As the economic activity gets back on track across the country, the GST collections are expected to look up in the forthcoming quarters.

Mr. Shivadass started the Session by saying that the Goods and Services Tax (GST) has completed almost three years of operation. Hailed as the single-biggest tax reform, the GST was rolled out with a bang in a special session of Parliament three years ago and subsumed 17 existing indirect taxes including the excise duty and sales tax. GST was introduced as the biggest tax reform and is showcased as a ‘One Nation One Tax’. He said that the initial period was very stressful for the trade and the Government, but over a period of time it has stabilized to a large extent though many issues still remain unresolved.

Mr. Shivadass said that the GST law has enabled plenty of optimistic possibilities, some of which are already beginning to bear fruit like 3.5 million new dealers registered in the first 6 months, 12.3 million (June 20) registered dealers with more than 50% being fresh registrations. The introduction of e-way bills and removal of state check posts have reduced transportation time by 20-25%. Indirect tax to GDP ratio has increased from 4.38% in 2014-15 to 4.9% in 2018-19 and Indirect tax to total tax ratio increased from 43.85% in 2014-15 to 45.10% in 2018-19.

On the benefits of GST, Mr. Shivadass said that before the GST, businesses had to spend a lot of time complying with different rules and regulations of various tax departments. Fortunately, the cascading effect of taxes on goods and services has been eliminated with the implementation of GST, making it easier for businesses to expand their operations and increase revenue. The transparency in procedures and laws has also resultedin an increase the Government’s monthly average revenue collection under the indirect tax. Traders and the various industry segments are also enjoying a seamless flow of tax credit, stabilizing their cash flow.

Talking about the shortcomings of GST, Mr. Shivadass said that after the introduction of GST, there has been a steady rise in the offense of creating fake invoices to fraudulently claim an input tax credit (ITC). Such invoices are created by racketeers who do not carry out any business and issue invoices without the actual supply of goods and services. Due to the ongoing COVID-19 pandemic, any significant step for GST reform has come to a halt. Although multiple tax structures make it complex, restructuring of tax rates is difficult due to the decline in revenue. There have also been issues with transitional credit and input tax credit, he said.

Mr. Shivadass added that the most crucial requirement today is the need to introduce fewer tax rates and consolidation of various circulars, notifications, orders in the law for a simple GST compliance. Presently, there are five tax rates. The Government is already taking severe measures to put an end to tax evasion and bring efficiency into GST compliance. Businesses can utilize GST software solutions to help them overcome compliance challenges and make time to focus on their growth.

Going forward, it is important to lay down a clear, taxpayer-centric strategy to ensure predictability and consistency in the application of the GST laws and procedure, he said. Efforts should be undertaken to widen the tax-base, rationalize rates, and simplify the law. Initiatives such as E-invoicing should be broadened to cover pre-filled return/refund claims as well as risk-based E-Audit. The IT platform should be made more robust for a richer user experience. Input Tax Credit, the very soul of GST, should be freed of needless restrictions, Mr. Shivadass said.

The second half of the session dealt with the issues trade and industry face with respect to various changes in the GST reform in light of the current circumstances.

Ms. Devika Rajagopal said that the pandemic has arrested business activities across the board and recovery of full payments from the customers on outstanding invoices, is proving to be an uphill task. In order to manage the working capital, businesses are bound to offer some discounts to its customers for realizing timely payments. Further, in several cases, debts will turn out to be bad, and businesses would not be able to realize any payment. What emerges from the ruling is that if there are no pre-fixed criteria and basis for arriving at the quantum of discounts which is mentioned in the agreement on the date of supply, then no tax adjustment would be permitted in any case. Businesses are issuing credit notes for discounts during the COVID period without application of mind and careful reading of the legislation, which may prove to be a costly affair once the accounts are audited by the Department.

Companies may get Input Tax Credit (ITC) for free distribution of personal protective equipment (PPE) kits, sanitizers, masks, and other such goods which provide relief from coronavirus. Companies can attain relaxation through corporate social responsibility (CSR) norms; however, CSR rules have already allowed companies’ spend on Covid-related goods to be treated as CSR expenditure.

She also spoke on the ever changing GST legislation and added that it is hard to keep updated with the GST legislations as there is a new notification or circular every day. She also added that with the introduction of new GST return, one has to go through the pain of understanding the return once more, that too when people have just gotten used to the existing return.

Following this, there was a brief discussion wherein the Speaker clarified the issues raised by Ms. Rajagopal.

The meeting ended President of the Chamber thanking everyone for having participated in the meeting.

Corporate Governance: Succession Planning & Continuity During COVID-19

Devika A. Gadgi, ANB Legal Mumbai

“Corporate governance is the system by which companies are directed and controlled.”

-The Cadbury Committee (U.K.)

The current COVID-19 crisis is unprecedented and marked by uncertainty. The present situation has adversely impacted the world economy and the continuity of most of the business organisations is under the radar and the sustainability of the business organisations is under grave uncertainty. The Board of Directors of a Company (“Board”) needs to ensure that the crisis is tackled in a proper and organised manner. In such a scenario, corporate governance practices play a key role. It is imperative that the Board adopts the best corporate governance practices to ensure the sustainability and continuity of the business and effective crisis management. For instance, Companies need to ensure that there is an accurate and transparent review of the financial forecasts as well as the earning disclosure owing to the current scenario and financial environment.

Scope

The present article analyses the concept of succession planning and continuity in terms of corporate governance in the backdrop of the COVID- 19 scenario. Section I deals with the importance of corporate governance in the present scenario. Section II deals with the importance of emergency succession plan in case a Key Managerial Person (KMP) contracts COVID- 19. Section III deals with the measures to be taken to ensure smooth functioning of the Board and whether a Company can substitute virtual meetings in place of physical meetings.

Analysis

Section I: Corporate Governance: A Key Player During Covid-19?

Corporate Governance in India

Corporate Governance has always been an issue of paramount importance in the Indian economy. The Indian corporate governance framework focuses mainly on protection of the shareholders, accountability of the Board and management of the company, timely reporting and disclosure requirements, Corporate Social Responsibility, etc. The Securities and Exchange Board of India (“SEBI”) and the Ministry of Corporate Affairs (“MCA”) are the regulators in this regard. The COVID-19 outbreak has created multiple hurdles and challenges for Indian companies. There are several corporate governance issues to be dealt with in order to effectively tackle and respond to the challenges posed by COVID-19.

Why is Corporate Governance important during COVID-19?

In the backdrop of the current pandemic, there is a dire need of risk identification and assessment resulting in effective management of the same. The Board needs to be in constant close contact with the management to ensure the security and well-being of the workforce and the stakeholders. A proper strategy needs to be devised paired with constant monitoring for management of the risks and minimising and mitigating any adverse consequences. The Board needs to take into consideration the financial health of the company and stress on factors such as the indebtedness of the company, financing policy, liquidity risk (short term and long term), etc. amongst others.

During the present scenario, the need for complete disclosure is of utmost importance. The Board needs to be in compliance of the various mandatory disclosure requirements such as under the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (as amended from time to time) (“LODR”). It is imperative for the companies to provide full and fair disclosure to ensure that the investors’ and the shareholders’ interests are not being compromised. The mechanism with regard to succession, appointment, etc. needs to be updated. The Corporate Governance policies need to be updated and modified in light of the current scenario for the efficient functioning of the Company.

Section II: The Need for An Emergency Succession Plan During Covid-19

Provisions relating to succession planning under law

Succession Planning is an important element of Corporate Governance in a Company. It is an on-going process and there needs to be a planned mechanism in place to ensure the continuity of leadership in key positions as well as in securing the future of the Company. The Board is entrusted with the responsibility of overseeing the succession planning. The recent Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2018 (“Amended LODR”) brought about amendments in the Board and their strategies with a view to strengthen the aspect of succession planning. The definition of the term “senior management” was ammended vide the Amended LODR so as to include one level below Chief Executive Officer/Managing Director/Whole time Director/Manager (including Chief Executive Officer/Manager, in case they are not part of the Board) and specifically includes the Company Secretary and the Chief Financial Officer. Thus, it states that the Board of the listed entity shall satisfy itself that plans are in place for orderly succession for appointment to the Board and Senior Management. This amendment has ensured that the succession planning needs to be undertaken by the Board for a wide array of employees and is not limited in its application.

Further, under Section 178 of the Companies Act, 2013 (“Act”), the Company is required to constitute a ‘Nomination and Remuneration Committee’ which amongst other things is entrusted with the responsibility of development of a succession plan for the Board and Senior Management. Countries such as United Kingdom, Japan, Italy, etc. have similar corporate governance policies regarding succession.

In case of a private company, the LODR and provisions under Section 178 is not applicable. However, it is advisable for a private company to have a succession policy in place. In case of an unforeseen situation, if the private company does not have an emergency succession plan, the operation of the company might come to a standstill. A private company cannot ignore succession planning just on the ground of lack of regulatory compliance. The consequences of lack of a succession policy resulting in vacancy in the office of key personnel will have an adverse impact on the company’s ability to achieve its targets and ensure sustainability and survival. The Tata Group has been a prime example of the need of a proper succession plan on the backdrop of sudden departure of Mr Mistry as the Chairman.

Succession Planning in the backdrop of COVID-19

In the current scenario, it is of utmost importance that the Company (both private and public) has an efficient Succession Policy. The Board is responsible for the succession of the CEO and the other KMP’s. If in case of an unfortunate event wherein the CEO or any of the KMP is contracted with COVID-19, the Board needs to have a well-planned succession policy so as to tackle any unforeseen situation. The succession risks pertaining to the entire senior management needs to be considered. The Board can incorporate a separate team to oversee the change in leadership, if any. The roles and responsibilities for the management team needs to be demarcated in a proper and well-defined manner. The company needs to have a robust emergency succession plan in case of any unforeseen situation.

As discussed in the above paragraphs, there are legal provisions under the Act as well as several regulations dealing with succession planning. The importance of succession planning in case of private companies has also been discussed above. However, the implementation of the same is a major hurdle even in today’s time.

Section III: Continuity During Pandemic: A Key Challenge

Measures for continuity of the Board

During the current pandemic, it is imperative that the Board remains intact and functioning if such a situation arises wherein the continuity is threatened. The Board needs to be proactive while dealing with such a scenario.

Adoption of succession plan and emergency by laws

The Board can ensure that an effective succession plan as discussed above is in place. Further, a set of emergency rules can be adopted by the company during such an unforeseen situation.

Regular meeting via virtual mode

The Board needs to ensure that meetings are conducted on a weekly basis or more frequently as required, via video conference or telephonic medium.

Undertaking critical functions

Even though the companies are being managed remotely, the Company needs to undertake the critical functions such as IT system, cyber security, regulatory compliance, functioning protocols etc. in a proper manner. The key support mechanisms such as IT services need to be operative since the entire workforce including the Board are working remotely and need access to the files and data to function.

Formation of a Monitoring Committee and Expert Advisory Committee

A Committee can be set up for the purpose of monitoring the entire situation. The Committee can evaluate the situation and adopt necessary measures to prevent and tackle the impact of the pandemic.

Virtual Meeting: A Substitute For Physical Meetings

There is a set legal framework in India which governs the regulations pertaining to board meetings as well as shareholders meetings, namely as:

1) The Act and Rules thereunder

2) The SEBI Regulations

3) The Standard Listing Agreement

4) Secretarial Standards issued by the Institute of Company Secretaries of India (ICSI)

There are many policy decisions which require the approval of the Board or the shareholders, for which it is essential to conduct the meetings. In the present scenario due to the pandemic, it is not possible for the Board or the Management or the shareholders to be physically present for any of the meetings. However, in the judgments of “Wagner v. International Health Promotions” and “Byng v. London Life Association”, the English Courts have held that virtual meeting via telecommunication or other modes are considered to be valid.

The Ministry of Corporate Affairs vide circular dated April 08, 2020 and a clarification issued on April 13, 2020 has permitted companies to convene their Extraordinary General Meetings (“EGM”) through video conferencing or other audio-visual means. Such relaxation is available until June 30, 2020. The decisions can be taken through e-voting or simplified voting (as the case maybe). E-voting is mandatory in prescribed companies only. As per the circular, the companies which are required to provide e-voting or have opted for it shall conduct the voting via video conferencing (“VC”) or other audio visual means (“OAVM”).However, in other cases, the shareholders can approve or reject the resolutions by sending emails at the registered e-mail ID provided by the companies. The detailed procedure has been mentioned in the circular pertaining to convening of the EGMs. Further, the MCA vide circular dated March 19, 2020 amended the rule 4 of the Companies (Meetings of Board and its Powers) Rules, 2014 thereby permitting the Companies to conduct Board Meetings via video conferencing or other visual means until June 30, 2020. Thus, it is permissible for the Companies to hold Board Meetings and the General Meetings via video conferencing or other modes.

The Board must ensure that the ability of the shareholders or the Board members to put forth resolutions and give opinions at the virtual meetings or vote on such matters or raise concerns should not be hampered in any manner. Virtual meetings can be a way of life in the near future rather than just an exception.

Conclusion

Corporate Governance plays a key role in ensuring the sustainability of the companies. It will play a vital role in the near future and will emerge as an essential mechanism to tackle the crisis. This will help in effective planning, reassessing the goals, long term sustainability, risk mitigation, etc. The Board plays a major role during the current crisis since it is entrusted with the responsibility of implementation of the Corporate Governance rules. The Board needs to adopt various techniques to ensure that the financial well-being and continuity of the Company is not threatened. For attaining this purpose, it is imperative that the Board functions in a proper manner and the functioning of the Board is not disrupted. There are certain regulations in place with regard to same. However, even in case of companies such as a private company, wherein there are no regulatory compliances in place, the Company should adopt the Corporate Governance polices such as succession planning for the effective and efficient functioning and continuity of the Company. A Company can ensure the continuity, crisis management and sustainability only if it focuses on adoption of the best corporate governance practices.

References

Books

- Geeta Rani & R.K. Mishra, Corporate Governance: Theory and Practice 74-78,(1 ed. Excel Books, 2008)

- M.Y. Khan, Indian Financial System (10 ed. McGraw Hill Education, 2018)

- A.C.Fernando, Corporate Governance: Principles, Policies and Practices 17 (1 ed. Dorling Kindersley (India) 2006)

- G K Kapoor, Sanjay Dhamija, Company Law: A Comprehensive Text Book on Companies Act 2013 (20 ed, Taxmann, 2017)

Report

- Report of Expert Committee on Company Law, Management & Board Governance Ministry of Corporate Affairs

Articles

- William Kucera, Jodi Simala, and Andrew Noreuil, Mayer Brown LLP, COVID-19 and Corporate Governance: Key Issues for Public Company Directors, HARVARD LAW SCHOOL FORUM ON CORPORATE GOVERNANCE (https://corpgov.law.harvard.edu/)

- Jennifer Buchanan Et Al., A Digital workplace and culture: How digital technologies are changing the workforce and how enterprises can adapt and evolve, Delloitte(https://www2.deloitte.com/content/dam/Deloitte/us/Documents/human-capital/us-cons-digital-workplace-and-culture.pdf)

Statutes

- Companies Act, 2013

- Companies (Management and Administration Rules), 2014

- Companies (Meetings of Board and its Powers) Rules, 2014

- Securities and Exchange Board Of India (Listing Obligations And Disclosure Requirements) (Amendment) Regulations, 2015

Cases

- Wagner v. International Health Promotions

- Byng v. London Life Association

Endnotes

[1] D. Geeta Rani & R.K. Mishra, Corporate Governance: Theory and Practice 74-78,(1 ed. Excel Books, 2008)

[2] Report of Expert Committee on Company Law, Management & Board Governance Ministry of Corporate Affairs (May 27, 2020, 10.30 A.M.), http://www.mca.gov.in/MinistryV2/management+and+board+governance.html

[3] M.Y. Khan, Indian Financial System (10 ed. McGraw Hill Education, 2018)

[4]A.C.Fernando, Corporate Governance: Principles, Policies and Practices 17 (1 ed. Dorling Kindersley (India) 2006)

[5] Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2018 regulation 17 (4)

[6] G K Kapoor & Sanjay Dhamija, Company Law: A Comprehensive Text Book on Companies Act 2013 (20 ed, Taxmann, 2017)

[7] William Kucera, Jodi Simala, and Andrew Noreuil, Mayer Brown LLP, COVID-19 and Corporate Governance: Key Issues for Public Company Directors, Harvard Law School Forum on Corporate Governance (May 22, 11.00 A.M.), https://corpgov.law.harvard.edu/

[8] Jennifer Buchanan et al. A, Digital workplace and culture: How digital technologies are changing the workforce and how enterprises can adapt and evolve, Deloitte (May 22, 2020, 11.30 A.M.), https://www2.deloitte.com/content/dam/Deloitte/us/Documents/human-capital/us-cons-digital-workplace-and-culture.pdf

[9] G K Kapoor & Sanjay Dhamija, Company Law: A Comprehensive Text Book on Companies Act 2013 (20 ed, Taxmann, 2017)

[10] (1994) 5 ACSR 419

[11] (1990) 1 Ch 170

[12] The term “e-voting” refers to remote e-voting or voting by electronic means.

[13] Companies Act, 2013 s.108;

[14] Companies (Management and Administration Rules), 2014 rule 20

NATIONAL EDUCATION POLICY, 2020

Priyanka Yavagal - Advocate - Shivadass & Shivadass (Law Chambers)

Michelle Obama said, “Empower yourselves with a good education, then get out there and use that education to build a country worthy of your boundless promise”. The New Education Policy, 2020 incorporates this idea by revamping the education system, focusing on broadening the reach of education to all parts of the society, making teachers the focus point by ensuring recruitment of the very best, prioritizing practical knowledge instead of rote learning and reconnecting with our rich cultural heritage, instilling a sense of pride in the future generations. The Indian education system has been remodelled and redefined after nearly three decades. But has the Government been too ambitious and impractical with this Policy? Or has it missed out on some changes that were anticipated?

The National Education Policy 2020 was approved on July 29, 2020. The erstwhile policy came in 1986 and was modified in 1992 and has been aided by Mid-day meal scheme and Right of Children to Free and Compulsory Education Act 2009 but this is the first time that the old policy is being replaced completely. The key changes in the new policy are as follows:

CHANGE IN SCHOOL MODELS:

1) The Policy now implements a 5+3+3+4 (i.e. 5 years of Foundational schooling, 3 years of Preparatory Schooling, 3 years of Middle School and 3 years of Secondary education for ages 3-18), as against the earlier 10+2 structure. The students will now be tested in Grades 3,5 and 8, respectively. NCERT will be given the responsibility of framing Early Childhood Care and Education (ECCE), which will be the curriculum for Foundational education.

[A] Foundational Education:

i. The 5 years of foundational education will be further divided into Pre-school/Anganwadi (for ages 3-5yrs) and Grade 1-2 (for ages 6-8). This is to promote at maximum foundational education to ensure a strong base in children. The curriculum will be focusing on enriching reading and basic arithmetic abilities, practical teaching and innovate ways to make children acquainted with learning instead of rote learning.

ii. The Policy further proposes a two-fold model to implement: (i) to make Anganwadis more accessible by paying special attention to secluded districts and regions and construction of new Anganwadis or by developing co-located Anganwadis with existing primary schools. (ii) to start training programs for teachers in these pre-schools and Anganwadis. Teachers with qualifications of 10+2 and above shall be given a 6-month certificate programme in ECCE; and those with lower educational qualifications shall be given a one-year diploma programme covering early literacy, numeracy, and other relevant aspects of ECCE through digital/distance mode using DTH channels as well as smartphones, allowing teachers to acquire ECCE qualifications with minimal disruption to their current work.

iii. The policy also plans on opening Ashramshalas in Tribal Areas for children.

iv. School libraries with State of Art facilities will be constructed in Villages to promote literacy in both adults for promoting the culture of learning.

v. Breakfast including groundnuts with Jaggery and local fruits, in addition to midday meals have been proposed.

vi. A national repository of high-quality resources on foundational literacy and numeracy will be made available on the Digital Infrastructure for Knowledge Sharing (DIKSHA).

[B] Preparatory Education (Grade 3-5):

i. There will be an examination in Grade 3 which will test basic literacy, numeracy, and other foundational skills of the children. The results of this examination will be stored in the National Education Policy 2020 system and will be used to further improve irregularities and observe patterns in child learning.

ii. A 3-language system will be adopted, wherein maximum focus shall be given to mother-tongue (regional language) till Grade 5. Wherever possible, the medium of instruction, at least till Grade 5 will be the mother-tongue and the same shall be encouraged till Grade 8. Students may switch/change their choices with 3 languages between Grades 6-8. This will be followed by both public and private schools. High-quality textbooks, including subjects like science, will be made available in home languages/mother tongue.

[C] Middle School (Grade 6-8):

i. Every student in the country will be encouraged to participate in a project/activity relating to ‘The Languages of India’, such as, the ‘Ek Bharat Shrestha Bharat’ initiative.

ii. Sanskrit will be offered at all school levels and higher education as an important, enriching option for students, including as an option in the three-language formula. In addition to Indian languages and English, foreign languages, such as Korean, Japanese, Thai, French, German, Spanish, Portuguese, and Russian, will also be offered at the secondary level.

iii. Ethical values and “what is right/wrong conduct” with practical examples along with themes including cheating, violence, plagiarism, littering, tolerance, equality, empathy will be taught to students.

[D] Secondary Education (Grade 9-12):

i. Since majority of the students drop out post Grade 8, the policy suggests measures such as upgrading and re-establishing Government schools by adding to the present infrastructure and new buildings and increasing safety measures for girls by providing conveyance to and from schools.

ii. Board exams for Grades 10 and 12 will continue but there will not be a rigid division in streams and students will be open to taking a plethora of options as per their interests for Board exams.

iii. To eliminate all high stakes, pressure and subsequent coaching culture, students will be allowed to appear twice for Boards during any given school year and the best-of-two attempts shall be considered.

iv. The policy is also open to new ideas that it may over time receive/develop to make viable models of Board Exams that reduce pressure and the coaching culture.

COLLEGE ENTRANCES:

The policy proposes National Testing Agency (NTA) testing services for the purpose of common entrance exams as against the prevailing norms of individual exams for every University. Liberty will be given to individual universities and colleges to use NTA assessments for their admissions.

GENERAL KEY CHANGES/PROPOSALS FOR FUTURE:

i. NCERT books will be available in all regional languages.

ii. Progress reports to be redesigned to portray a holistic approach and highlight unique abilities of each child.

iii. It is proposed to set up a National Assessment Centre, PARAKH (Performance Assessment, Review, and Analysis of Knowledge for Holistic Development), as a standard-setting body under MHRD that fulfils the basic objectives of setting norms, standards, and guidelines for student assessment and evaluation for all recognized school boards of India, guiding the State Achievement Survey (SAS) and undertaking the National Achievement Survey (NAS)

iv. The Policy promoted community and alumni volunteer peer-tutoring and volunteer activities by educated citizens to increase literacy rate and treat it as a national mission. This shall be at the prerogative of the State Government. Databases of literate volunteers, retired scientists/Government/Semi-Government employees, alumni, and educators will be created for this purpose.

v. More NCC wings to be opened, especially in tribal dominated areas.

vi. State will enable technology-based solutions for the orientation of parents/caregivers along with wide-scale dissemination of learning materials to enable parents/caregivers to actively support children with special learning needs/disabilities as under Rights of Persons with Disabilities Act, 2016 under Divyang scheme.

vii. Encouragement shall be given to the idea of “School Clusters” and “Bal Bhavans” where children of all ages can visit once a week (e.g., on weekends) or more often, as a special daytime boarding school, to partake in art-related, career-related, and play-related activities.

viii. The un-utilized capacity of school infrastructure will be used to promote social, intellectual, and volunteer activities for the community and to promote social cohesion during non-teaching / schooling hours and may be used as a “Samajik Chetna Kendra”.

ix. For a periodic ‘health check-up’ of the overall system, a sample-based National Achievement Survey (NAS) of student learning levels will be carried out by the proposed new National Assessment Centre, PARAKH.

x. Financial assistance to students shall be made available through various measures. Efforts will be made to incentivize the merit of students belonging to SC, ST, OBC, and other SEDGs. The National Scholarship Portal will be expanded to support, foster, and track the progress of students receiving scholarships. Private HEIs will be encouraged to offer larger numbers of scholarships to their students.

xi. Vocational training courses will be instituted and encouraged to remove the stigma around them and utilize the talent of children as per their area of interest.

CHANGES FOR TEACHERS:

i. B.Ed. programmes may also allow a specialization in the education of gifted children.

ii. Teachers will be sensitized to the needs of the children and the new system. They will also be encouraged to spot and promote individual talents by giving additional study material/task to children showing inclination and talent in any field ranging from academics to sports, arts and leadership. The aim is to create individuals ready to take positions in real life with excellence and leading the country best as per their talent and inclination.

iii. To ensure onboarding of quality teachers especially from rural areas a large number of merit-based scholarships shall be instituted across the country towards the 4-year integrated B.Ed. programmes and preference shall be given to students well-versed in the local language. This will promote local job opportunities and will give more local role-models to their students.

iv. The TETs (Teacher Eligibility Tests) will be initiated and also be extended to cover teachers across all stages (Foundational, Preparatory, Middle and Secondary) of school education.

v. Sharing of teachers across schools will be considered in accordance with the grouping-of-schools adopted by State/UT Governments.

vi. Teachers will be given continuous opportunities for self-improvement and to learn the latest innovations and advances in their professions. Each teacher will be expected to participate in at least 50 hours of CPD (Continuous Professional Development) every year, for their own professional development, driven by their own interests per year.

vii. School Principals will also have a similar 50 hour leadership/management workshop and various online development opportunities per year.

viii. A guidance system in the form of National Professional Standards for Teachers (NPST) will be developed by 2022, by the National Council for Teacher Education, the new Professional Standard Setting Body (PSSB) under the General Education Council (GEC), in consultation with NCERT.

ix. By 2030, the minimum degree qualification for teaching will be a 4-year integrated B.Ed. degree that prescribe a wide range of content and pedagogy, including strong practical training at local schools. A 2-year B.Ed. programmes will also be offered, by the same multidisciplinary institutions offering the 4-year integrated B.Ed and will be intended only for those who have already obtained Bachelor ’s degree in other specialized subjects.

PROMOTING RESEARCH:

i. The Policy envisions the establishment of a National Research Foundation (NRF) to enable a culture of research among universities. In particular, the NRF will provide a reliable base on merit and equitable peer-review based research funding, through suitable incentives and recognition for outstanding research. This will be undertaken at State Universities and other public institutions where research capability is currently limited.

ii. The NRF will competitively fund research in all disciplines. Successful research will be recognized, and where relevant, implemented through close linkages with governmental agencies as well as with industry and private/philanthropic organizations.

iii. The NRF will be governed, independently of the Government, by a rotating Board of Governors consisting of the very best researchers and innovators across different fields.

GENERAL PROMOTION OF EDUCATION AMONGST ADULT DROP-OUTS

i. The Policy seeks to expand the scope of Open and Distance Learning (ODL) Programmes offered by the National Institute of Open Schooling (NIOS).

ii. NIOS and State Open Schools will offer the following programmes in addition to the present programmes: A, B and C levels that are equivalent to Grades 3, 5, and 8 of the formal school system; secondary education programmes that are equivalent to Grades 10 and 12; vocational education courses/programmes; and adult literacy and life-enrichment programmes in regional languages.

The New Education Policy seeks to change years of bias ingrained in the Indian society and liberates children and future generations from the concrete, narrow constructs imposed by the former policy. It is all-encompassing and if implemented effectively, will change the course of the future of this nation. However, the present funds currently allocated to education sector is only 4% of the GDP which needs to increase to at least 6% to even start beginning working on these radical and infrastructural changes. The policy enumerates the ideas and vision of a digitally transformed India and the ways in which it can be attained. But are these changes enough? Has the policy thought through the rapidly changing technology related issues? The Covid 19 Pandemic has made a number of elements of the education system redundant – physical schooling seems a thing of the past. Is this policy also enough to address practical issues such as anxiety, suicidal rates, stress etc? or is it enough to compete with large Universities abroad?

A majority of these questions remain in limbo and a wait and watch game is in play, like every other policy/legislation in India, the key lies in its effective implementation and continued modification with times, standards and growth of India as a Nation.

Chamber Vlogs!

To view all the videos in the Chamber Vlog series and other informative contents from the Chamber, please go to the Cochin Chamber’s YouTube Channel.

The most recent ones are added to the video players below. We will keep uploading new and relevant content for our members and the industry in general.

Kindly share these videos with your networks and subscribe to our YouTube Channel for more informative content.

Chamber Vlog 15

Understanding 'Income Tax' in India

Chamber Vlog 16

Leadership Dilemma during COVID times

Chamber Vlog 17

Corporate Governance: Succession Planning and Continuity during COVID-19

Chamber Vlog 18

The Practice of Generating Energy

Tax and Regulatory Updates from PricewaterhouseCoopers

Regulatory

Amendment in General Finance Rules, 2017 imposing restrictions including prior registration requirement for bidders from countries sharing land border to participate in public procurements

The Department of Expenditure (DoE) has inserted Rule 144 (xi) under the General Finance Rules, 2017 (GFR), empowering the DoE to impose restrictions, including registration and/ or screening requirements on procurement from bidders from a country or countries, or a class of countries, on the grounds of defence of India, or national security.

As per the powers exercised under 144 (xi) of the GFR, the DoE has ordered that any bidder from a country that shares a land border with India must register with the Competent Authority for bidding under a Public Procurement Order. This restriction does not apply to orders placed or contracts concluded or letter/ notice of award/ acceptance (LoA) issued before the date of issue of Order. For tenders that are yet to be opened, or with incomplete evaluation of technical bid or the first exclusionary qualificatory stage, no contracts shall be placed on bidders from such countries. If the bid has crossed the first exclusionary stage, the contract shall be considered de novo.

The restrictions under Rule 144 (xi) of the GFR are summarised below.

Registration requirement for bidders of countries sharing land borders with India

Rule (xi) to Rule 144 of the GFR has been inserted, which empowers the DoE to impose restrictions or screening requirements on bidders from country on ground of defence and national security.

In the exercise of powers laid under Rule 144 (xi) of the GFR, the DoE has placed a requirement that a bidder from a country that shares land borders requires prior registration with the Competent Authority outlined in point 4. This requirement would be placed as a pre-requisite in the tender condition and a certificate shall be taken from bidders in the tender documents regarding their compliance with this Order. The requirement shall also be applicable to sub-contractors appointed by the bidder under works contracts.

Applicability on following procurement agencies

This Order would be applicable to the following:

- Central Government Ministries and Departments;

- All autonomous bodies;

- Public sector banks and

- public sector financial institutions;

- Central Public Sector Enterprises; subject to orders of the Department of Public Enterprises;

- Public Private Partnership projects receiving financial support from the Government or public sector enterprises/ undertakings;

- Union Territories, National Capital Territory of Delhi and all agencies/ undertakings thereof;

- Government E-Marketplace (GeM) registering vendors/ bidders.

The Government of India, while invoking the provisions of Article 257(1) of the Constitution of India, has directed the Chief Secretaries of the State Governments to implement the Order in procurement by the State Governments, State undertakings, etc.

Who does this apply – Bidder from country sharing land border

“Bidder” shall mean the following:

a) An entity incorporated, established or registered in such a country; or

b) A subsidiary of an entity incorporated, established or registered in such a country; or

c) An entity substantially controlled through entities incorporated, established or registered in such a country; or

d) An entity whose beneficial owner is situated in such a country; or

e) An Indian (or other) agent of such an entity; or

f) A natural person who is a citizen of such a country; or

g) A consortium or joint venture where any member of the consortium or joint venture or agency, branch or office controlled by any of the above.

The term “beneficial owner” means –

A) In reference of following entities, a natural person(s), who, whether acting alone or together, or through one or more juridical person(s), has

B) Where no natural person is identified, the beneficial owner is the relevant natural person who holds the position of a senior managing official.

Competent authority for registration

The Department for Promotion of Industry and Internal Trade (DPIIT) shall constitute a registration committee comprising of officers not below the rank of joint secretary from following Ministries/ Departments:

A) DPIIT, who shall be the Chairman;

B) Ministry of Home Affairs;

C) Ministry of External Affairs;

D) Departments whose sectors are covered by applications under consideration.

The DPIIT shall lay down the method of application, format, etc., for registration process. The Competent Authority shall first seek political and security clearances from the Ministry of External Affairs and Ministry of Home Affairs, as per guidelines issued from time to time.

The States have also been assigned similar functions to the DPIIT to constitute registration committees; however, the security and political clearance process will remain the same. However, State registration shall be valid for procurement of such States only.

The decision of the Committee shall be for all types of tenders or for a specified type of goods or services and it may be for a specified or unspecified duration of time, as deemed fit. The registration granted by the Competent Authority of the Government of India shall be valid not only for procurement by the Central Government and its agencies/ public enterprises, etc., but also for procurement by State Governments and their agencies/ public enterprises.

The Competent Authority is empowered to cancel the registration already granted if it determines that there is sufficient cause. The Competent Authority shall not be required to give reasons for rejection/ cancellation of registration of a bidder.

Existing tenders

- Orders that are placed or contracts concluded or letter/ notice of award/ acceptance (LoA) issued would continue;

- Tenders that are yet to be opened, or with incomplete evaluation of technical bid or the first exclusionary qualificatory stage will need to be re-issued;

- The tendering process that has crossed the first exclusionary qualificatory stage shall be considered de novo and will be re-issued.

Exceptions to the Order

The Order shall not apply to the following:

- Procurement by Indian missions and by offices of Government agencies/ undertakings located outside India;

- Projects receiving international funding, except with the approval of the Department of Economic Affairs;

- Bona fide small procurements, made without knowing the country of the bidder;

- Bona fide procurements made through the GeM without knowing the country of the bidder till the date fixed by GeM;

- Medical supplies directly related to the containment of the COVID-19 pandemic until 31 December 2020.

PwC comments: Going forward, all Government procurement contracts would require bidders from countries with which India shares land border a prior registration to become eligible to supply goods and services under public procurement orders Detailed application process and procedure would be issued by DPIIT in due course of time.

Direct Taxes

Supreme Court holds that a separate agreement for non-compete fee, on facts, not sham; not taxable as part of capital gains on shares

The Supreme Court of India allows the taxpayer’s appeal and reverses the High Court’s order of re-characterising the non-compete fees taxable, as consideration for sale of shares. Further it was emphasised that the Revenue has no business to second-guess the commercial or business expediency of what parties at arms-length decide for each other.

PwC comments: The Supreme Court has reaffirmed the established principle that commercial expediency must be adjudged from the perspective of a prudent businessman and not from that of the Revenue.

Tribunal holds slump sale of business to be succession for depreciation in the hands of purchaser; allows depreciation on goodwill recorded as a result of the purchase

The Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) held that section 170 of the Income-tax Act, 1961 (the Act), is applicable to the acquisition of business pursuant to slump sale, and therefore, the fifth proviso to section 32 of the Act was also applicable. The Tribunal reaffirmed that the difference between consideration for slump sale and the value of assets acquired from the transferor and added to the block of assets will be “goodwill” and will be eligible for depreciation.

PwC comments: The Tribunal affirmed that section 170 of the Act would be applicable to a slump sale, being succession in business. It also upheld that the fifth proviso to section 32 of the Act will be applicable to assets acquired pursuant to a slump sale, irrespective of whether section 170 of the Act applies or not.

Scheme of amalgamation, once approved by High Court, is of binding nature

Recently, the Kolkata bench of the Income-tax Appellate Tribunal (Tribunal) held that the High Court’s order approving the scheme of amalgamation (Scheme) is binding in nature and the Commissioner of Income-tax (Appeals) [CIT(A)] cannot take a view contrary to that and such view is against law. Further, the Tribunal also held that using the proposed provisions of the general anti-avoidance rule (GAAR) for drawing support, when they are not brought into effect, is also bad in law. The Tribunal upheld CIT(A)’s contention that the period of holding of a capital asset needs to be determined based on the date from which the taxpayer “held” the capital asset, and not from the date of acquiring the ownership of land.

PwC comments: The Tribunal has reaffirmed the position that an order of the High Court approving a Scheme is binding in nature. The Tribunal has also confirmed that the Revenue cannot draw strength from future proposed provisions of the GAAR, which are not effective for the concerned financial year.

Indirect Tax

CBIC issues FAQs on manufacturing and other operations in customs bonded warehouse

To promote the “Make in India” initiative and as part of the ease of doing business measures, the Central Board of Indirect Taxes and Customs (CBIC), had notified the Manufacture and Other Operations in Warehouse (No. 2) Regulations, 2019 (Scheme). This Scheme enabled businesses to import raw materials and capital goods without payment of duty for manufacturing and other operations in a bonded manufacturing facility for exports, while allowing import duty deferral for the domestic market.

The key features of the Scheme are as follows:

- Locational flexibility with no geographical limitation.

- One-time approval.

- Deferment of customs duty on imports and duty saving to the extent that final products are exported out of India.

- No export obligation with no limitation on export or domestic clearances.

- Minimal compliances, documentation and approval requirement.

The CBIC explained the modalities of the Scheme through Circular No. 34/2019-Customs dated 1 October 2019.

Basis inputs received in trade consultation, the CBIC has released a set of Frequently Asked Questions (FAQs) relating to undertaking manufacturing and other operations in a bonded warehouse. The FAQs have been summarised below.

Eligibility

- Any person who is a citizen of India or entity incorporated in India is eligible. The eligible person or entity has been granted a licence for the establishment of a private bonded warehouse in terms of Private Warehouse Licensing Regulations, 2016, or alternatively, is seeking permission to establish one, along with the approval to undertake manufacturing in bond in terms of section 65 of the Customs Act, 1962 (Customs Act).

- Manufacturing and other operations in a bonded warehouse under the Scheme is allowed only to a private bonded warehouse licensed under section 58 of the Customs Act and not a private bonded warehouse licensed under section 57 of the Customs Act.

- Eligibility to seek approval under the Scheme is not linked to the quantum of clearances for exports and the domestic market.

- Any existing domestic tariff area manufacturing unit (i.e. not an Export Oriented Unit/ Special Economic Zone) can seek approval under the Scheme. The existing capital goods and inputs must be accounted in the accounting form prescribed in the Scheme.

- In terms of infrastructure, the regulations Scheme does not mandate that a fully enclosed structure is a prerequisite for the grant of licence. The applicant needs to ensure that the proposed site or building is suitable for the purpose of secured storage of goods and discharge of compliances, such as proper boundary walls, gate(s) with access control and personnel to safeguard the premises, etc. Moreover, the requirement may vary in the operations, nature of goods, etc. Hence, the approving customs authorities will consider the relevant facts in considering the application.

Physical control and validity of approvals

- The customs authorities have no physical control of the unit. However, the unit will be subject to risk-based audits without any defined periodicity.

- The license and permission granted is valid unless it is cancelled or surrendered. Therefore, there is no requirement of license renewal.

Duty/ tax implications on various transactions

An approved unit under the bonded warehouse can import capital goods without payment of duty. The import duties stand deferred until they are cleared for home consumption or are exported, in which case, there is no duty liability. The capital goods can be cleared for home consumption on the payment of applicable duty without interest or exported after use, without the payment of duty.

Duty deferment is without any time limitation

- Inputs/ raw materials can be imported and deposited in the bonded warehouse without the payment of Basic Customs Duty and Integrated Goods and Services Tax (IGST). No interest is applicable at the time of payment of duties on the clearance of finished goods manufactured using inputs/ raw materials. Only the duties on inputs/ raw materials are to be paid when the resultant goods are cleared for home consumption apart from GST/ IGST on the finished goods.

- No incremental duty on the finished goods cleared into Domestic Tariff Area is payable on account of imported capital goods (on which duty has been deferred).

- The eligibility to avail export benefits under the Foreign Trade Policy or seek exemption under the Customs (Import of Goods at Concessional Rate of Duty) Rules, 2017 would depend upon the respective Schemes. A unit operating under the Scheme can avail any other benefit, if the Scheme allows.

Procedure/ compliances

- Depreciation is not available if the imported capital goods (on which duty has been deferred) are cleared for home consumption. If the capital goods are exported, the valuation will be in terms of section 14 of the Customs Act read with the Customs Valuation (Determination of Value of Export Goods) Rules, 2007.

- A warehouse keeper needs to be appointed for a premise to be licensed as a private bonded warehouse to maintain accounts correctly and sign documents on behalf of the licensee.

- The Generally Accepted Accounting Principles will be followed for inventory control. The First in First Out method can be followed.

- A licensee can surrender the licence granted to him by making a request in writing to the Principal Commissioner of Customs or Commissioner of Customs. On receipt of such request, the licence will be cancelled subject to payment of all dues and clearance of remaining goods in such warehouse.

PwC comments: Manufacturing and Other Operations in Warehouse Regulations, 2019 extends operational flexibility to businesses in terms of duty deferment, interface with domestic market, etc. Businesses are exploring this as an alternative or an option for undertaking manufacturing in India. The FAQs will hopefully address the concerns of businesses and enable them to adopt the Scheme.

Larger Bench of Tribunal holds that foreclosure charges collected by banks and NBFCs on premature termination of loans is not leviable to service tax; analyses what constitutes “consideration” for service and damages for breach of contract

Owing to divergent views of the Division Benches of Ahmedabad and Kolkata Customs Excise and Service Tax Appellate Tribunals (Tribunal) respectively, a Larger Bench of the Chennai Tribunal was constituted to decide the issue of applicability of service tax on foreclosure charges collected by banks and non-banking financial companies (NBFCs) on premature termination of loans.

The Tribunal held that foreclosure charges collected by banks and NBFCs on premature termination of loans are not leviable to service tax under “banking and other financial services” (BOFS), as defined under the Finance Act. Reference was made to the provisions of the Finance Act, the Indian Contract Act, 1872, relevant Indian and foreign decisions and a few dictionaries and commentaries, to analyse the meaning of “consideration,” “breach of contract” and “liquidated damages.”

The Tribunal observed that foreclosure charges are recovered as compensation for disruption of a service and not towards lending services. The phrase “in relation to lending” cannot be stretched to cover those activities that terminate the main contractual activity. Thus, the Tribunal held that service tax under the BOFS, as defined under the Finance Act, is not attracted on foreclosure charges collected by banks and NBFCs on premature termination of loans and directed the appeals to be listed before the regular bench for hearing.

PwC comments: This is an important much-awaited ruling relating to the pre-negative list regime. While the ruling is in the context of taxability of charges for foreclosure, the analysis and principles laid out would be a relevant guide to determine the nature of amounts received as compensation for premature termination of services by the service recipient. There has been much debate and controversy on the taxability of such payments, including payment towards damages for breach of contract, liquidated damages, notice pay recovery, etc., in the pre-GST and the GST regime. The detailed analysis of the meaning of the terms “consideration,” “breach of contract” and “liquidated damages,” particularly in the context of charges/ recoveries made on the basis of “conditions of a contract,” as juxtaposed with “consideration for a contract” is noteworthy. The Tribunal has also referred to the ECJ rulings and Australian GST law and applied similar principles in the context of the Indian legislation, which emphasizes the relevance of foreign laws and rulings to other interpretive areas of controversies in the GST laws. This ruling is rendered in the context of the provisions in the pre-negative list regime, and thus, there is no discussion on the declared service. It would be relevant to examine the applicability of this ruling post the negative list and in the GST regime, considering that the EU VAT directives and the ECJ ruling referred by the Tribunal provide that the “supply of services” includes inter alia “an obligation to refrain from an act or to tolerate an act or situation.”

Madras High Court holds Rule 117 of the CGST Rules to be intra vires section 140 of the CGST Act to conclude that time limit specified under Rule 117 of the CGST Rules is mandatory and not directory

Recently in a Writ Petition challenging the validity of Rule 117 of the Central Goods and Service tax Rules, 2017 (CGST Rules), the Madras High Court held Rule 117 to be intra vires section 140 of Central Goods and Service Tax Act, 2017 (CGST Act) and the time limit specified under Rule 117 of the CGST Rules to be mandatory and not directory. It was also held that input tax credit (ITC) is a concession and not a vested right.

The High Court held as under:

Observations on other High Court decisions

- With respect to decisions in Brand Equity Treaties and Micromax Informatics v. Union of India, wherein it was held that CENVAT credit had accrued and vested in the taxpayer, and is consequently, the property of the taxpayer, the High Court has observed that the decisions were dated before the amendment to section 140 of the CGST Act, whereby, the words “within such time” were inserted. In Brand Equity Treaties Limited10, the High Court specifically noted that the Supreme Court has granted a stay on the operation of the judgment.

- Reference has been made to the decision in the case of Nelco Limited, which was dated pre-amendment to section 140 of the CGST Act, wherein it was held that Rule 117 of the CGST Rules is intra vires section 140 of the CGST Act and imposes a reasonable time limit for availing ITC. It was also held that ITC is a concession that is required to be availed within the prescribed time limit, failing which it would lapse. A similar view was taken in Willowood Chemicals Limited.

- In SKH Sheet Metals Components, which is dated post amendment of section 140 of the CGST Act, it has been held that the amendment answers the question regarding the power to frame rules fixing the time limit for filing the declaration, but does not fix a time limit for transitioning credit. The High Court has observed that it cannot subscribe to this view, as the power to prescribe a time limit is expressly incorporated in section 140 of the CGST Act, which deals with transitional ITC, and Rule 117 of the CGST Rules that fixes such a time limit.

Rule 117 of the CGST Rules is intra vires section 140 of the CGST Act

- The power to frame Rules with retrospective effect has been conferred by section 164 of the CGST Act subject to the limitation that it should not pre-date the date on which the entry under the CGST Act came into force. Accordingly, Rule 117 of the CGST Rules was framed, whereby, a time limit was fixed for submitting Form GST TRAN-1 on the common portal.

- Thereafter, the words “within such time” were introduced in section 140 of the CGST Act, with retrospective effect from 1 July 2017, thereby, conferring express power to prescribe time limits under section 140 of the CGST Act, without relying entirely on the generic rule-making power under section 164 of the CGST Act. Thus, the High Court concluded that Rule 117 of the CGST Rules is intra vires section 140 of the CGST Act.

ITC is a concession and not a vested right

- The Supreme Court, in Jayam and Company, has held that ITC has to be construed as a concession and not a vested right.

- ITC being a concession cannot be availed without complying with the conditions prescribed in relation thereto.

Time limit is mandatory and not directory

- The High Court referred to section 16(4) of the CGST Act and section 19(3)(d) of the TNVAT Act to state that GST provisions and the erstwhile VAT laws, are indicative of the legislative intent to impose time limits for availing ITC. Therefore, disregarding the time limit and permitting a party to avail transitional ITC, in perpetuity, would render the provision unworkable.

- Regarding the observation in SKH Sheet Metals Components14 that ITC is the heart and soul of GST legislations, the High Court observed that it is not a logical corollary that the time limits for availing transitional ITC are inimical to the object and purpose of the statute.

- It was also observed that if the time limit is construed as mandatory, the substantive rights of the taxpayer would be impacted, and if construed as directory, the Government’s revenue interest would be adversely impacted, including the predictability thereof. Thus, on weighing all relevant factors, it has been held that the time limit is mandatory and not directory.

- It was also held that Form GST TRAN-1 is required to be filed electronically on the common portal and the requirement is not satisfied by handing over the Form in person to the Revenue authorities.

PwC comments: Recently, there have been various contrary judgements on the issues relating to transitional credit, constitutional validity of amendment to section 140 of the CGST Act and whether the time limit prescribed under Rule 117 of the CGST Rules is mandatory or directory, etc. Owing to technical difficulties in filing Form GST Tran-1, while the entitlement/ eligibility of the taxpayer to avail such credit has been upheld in some decisions, such entitlement has been disallowed by some High Courts. It appears that availing such disputed credits is becoming increasingly difficult, especially after the retrospective amendment allowing the Government to specify time limits.

Importantly, in the present case, while the petitioner has challenged the constitutional validity of the retrospective amendment to give validity to the time limit provided under Rule 117 of the CGST Rules, the petitioner has not argued this in detail and it has not been examined by the High Court.