President's Note

Friends,

Even before the scars of last year’s monsoon and the resulting deluge, the worst in over a century, could heal completely, the State was yet again at the receiving end of nature’s fury earlier this month. The State’s northern districts of Malappuram, Wayanad, Kozhikode, and Idukki in central Kerala were the worst hit in the torrential rains and its aftermath.

Recurring disasters such as these can break the back of any economy, and just as Kerala was getting its house in order, disaster struck again. State-wide, 47,622 people are being accommodated in 296 relief camps and 1,789 houses have been reported as fully damaged and 14,542, partially damaged.

Apart from claiming hundreds of lives, displacing lakhs of people and destroying infrastructure in Karnataka, Kerala, Maharashtra, Andhra Pradesh, and Goa, the flooding triggered by incessant rains inflicted heavy losses on the farming community. In Kerala, close to 29,000 hectares of cropped land has been washed away this year. The Kerala Agricultural Department has estimated the total economic loss to be around Rs. 3,700 crore, of which farm sector losses have been pegged at Rs. 1,100 crore.

Extensive damage to road surfaces and bridges has been reported from seven districts in the State due to the floods and landslips triggered by torrential rains. The Public Works Department has estimated losses to the tune of Rs. 2,611 crore in the recent floods and landslips with 1,600 km of roads, 88 bridges, and 80 government buildings having suffered damages.

The last time around, Keralites showed the world that we are united as a people in coming together to help those in need. I am confident that we will once again emerge from the devastating effects of this unforeseen calamity as resilient as before.

Kochi is a fast growing city and its roads carry huge volumes of traffic day in and day out. Vytilla is the biggest intersection in Kochi handling the maximum number of vehicles every day. The mounting traffic snarls at Vytilla and Kundanoor, which have been heavily barricaded for the flyover works has become a huge concern and nightmare for the public. The pathetic condition of many stretches of the NH bypass and its side roads in the vicinity of flyover’s worksites has been causing traffic hold-ups and accidents for several months now. We hope that the authorities to look into the matter urgently and ensure that the roads are repaired at the earliest thereby alleviating the trauma to those who use those roads.

The Goods and Services Tax has been one of the most radical tax reforms in India. To push for the digital economy and to curb tax evasion, in this year’s Union Budget, the Government made a major announcement, introducing an e-invoicing system from January 2020 onwards. As a result of this announcement, recently GST council has sought stakeholders’ comments on the new e-invoice format, which will be mandatory for all dealers in due course. This is a big step forward as it presents an opportunity for all stakeholders to make the economy digital, with no need for paper invoices in the future.

The Director General of Foreign Trade (DGFT) had issued a Trade Notice No. 21(2019-20) dated 28th June 2019 soliciting stakeholder comments for framing the Foreign Trade Policy for the next five years. While we appreciate the various initiatives taken by the Government in promoting the exim trade we feel that there are more initiatives that can be implemented to further the growth of this sector. In this connection the Chamber has made a representation to the DGFT outlining the issues that require urgent attention and a copy of the same is carried out in this issue of the newsletter for your reference. We are hopeful that our inputs will be taken into consideration.

Moving on, the Eighth Breakfast Meeting of the CEO Forum was held on the 2nd of August 2019. This time around, we had Mr. K Jayakumar I.A.S (Retd.), Director, Institute of Management in Government, Kerala as the Guest Speaker. The session was on ‘Commerce without Conscience–A Matter of National Concern’. Mr. Jayakumar delivered a very interesting and a thought provoking talk which was appreciated by all who attended the Session.

On the 8th of August, the Chamber in association with ‘anb’ Legal and Grant Thornton organized a Seminar on the ‘Proposed Constitution of the Hon’ble National Company Law Tribunal, Kochi’. The Seminar covered topics such as the powers and functions of the Hon’ble National Company Law Tribunal, the jurisdiction of and proceedings before the Tribunal.

Detailed reports along with pictures of these programmes are carried elsewhere in this issue of this Newsletter.

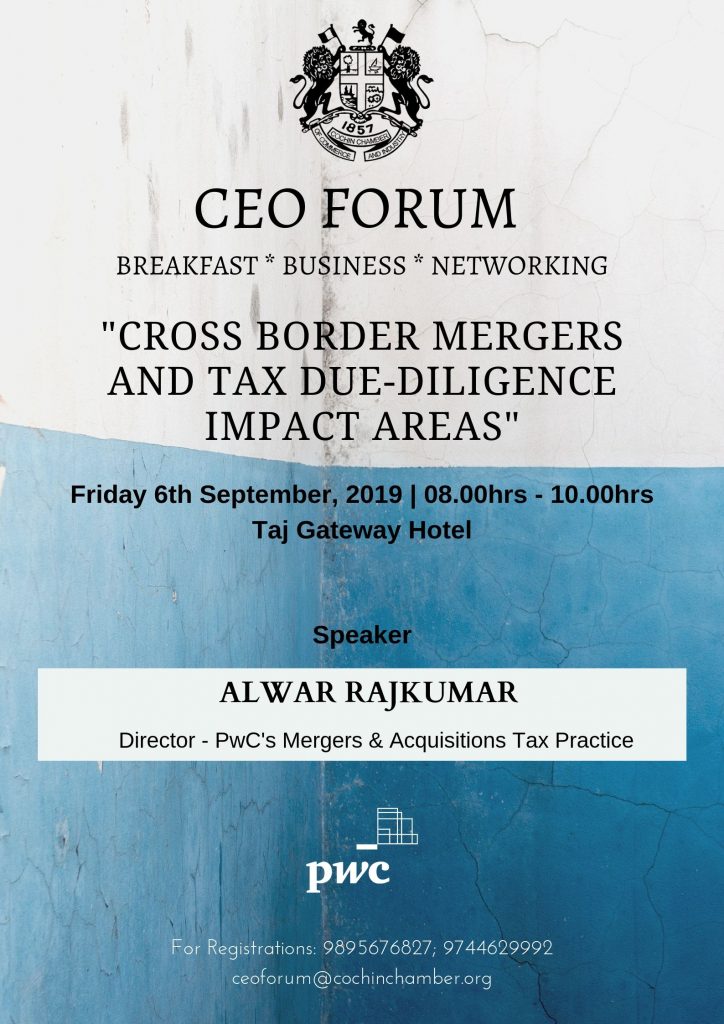

The next CEO Forum Breakfast Meeting will be on 6th of September. The Speaker at the Session will be Mr. Alwar Rajkumar, Director, PwC’s Mergers & Acquisitions Tax Practice. The topic under discussion will be ‘Cross-Border Mergers and Tax Due-Diligence Impact Areas.’ I hope you all will make it convenient to attend the Session as it will provide a conceptual understanding of the regulations relating to cross-border mergers and the key impact areas while undertaking a tax due-diligence.

In today’s world, it is essential to challenge the status quo to stay ahead of the competition. This starts with everyone, leading by example, trying new approaches, and welcoming fresh ideas. To understand the concept of ‘Status Quo’ and to meet challenges fearlessly, the Chamber is organizing an Interactive Workshop on ‘Challenge the Status Quo’ on 20th September 2019 at Hotel Park Central, Kaloor. The Workshop will be handled by Cmde. S. Sreeram and Cdr. Ninad Phatarphekar, Founders of Transformavens Training & Consulting LLP, Mumbai. I trust that you will have received the details of this event.

Onam, the biggest festival of Kerala is around the corner, and Malayalis all over the world are set to celebrate the auspicious day. Let this season bring joy and prosperity to you and your family, and I wish you all a Happy Onam.

Counting on your continued support of the Chamber and its activities.

Regards

V Venugopal

President

Famous Quote

We are Hiring!!

Recent Events

Seminar on the Proposed Constitution of Hon'ble National Company Law Tribunal, Kochi

Tuesday, 30th July 2019 | Chamber Hall, Willingdon Island

The Chamber, in association with ANB Legal, Mumbai and Grant Thornton, Cochin organized a Seminar on the Proposed Constitution of the Hon’ble National Company Law Tribunal, Kochi on Tuesday, 30th July 2019 in the Conference Hall of the Cochin Chamber,.

Mr. V. Venugopal, President, Cochin Chamber of Commerce & Industry delivered the Inaugural Address

Mr. Dhanraj Bhagat, Partner, Grant Thornton India LLP, then gave a brief overview of the Insolvency and Bankruptcy Code journey so far.

Mr. Pradeep Parikh, Ex-Vice President, ITAT and Senior Consultant with ANB Legal then spoke on the Inception, Formation and Functioning of the Tribunal.

Mr. Sridhar R, Partner – Tax, Grant Thornton India LLP & CA Subham Kumar spoke on Mergers and Acquisitions under the Companies Act and regulations mandated under the FEMA Law with a special emphasis on Cross Border Mergers

Ms. Shreni Shetty, Partner – Dispute Resolution, ANB Legal then spoke on the Jurisdiction of & proceedings before the Tribunal.

Ms. Payal Parikh, Managing Partner, ANB Legal, proposed the Vote of Thanks.

8th CEO FORUM Breakfast Meeting 2019 | Commerce without Conscience - A Matter of National Concern

Friday, 2nd August 2019 | Taj Gateway Hotel, Ernakulam

The Cochin Chamber of Commerce and Industry conducted the CEO Forum’s 8th Breakfast Meeting on Friday, 2nd of August 2019 at the Taj Gateway Hotel, Ernakulam.

Mr. V Venugopal, President of the Chamber, delivered the Welcome Address and introduced the Speaker for the meeting.

Mr. K Jayakumar, I.A.S (Retd.), Director, Institute of Management in Government, Kerala was the Guest Speaker at the meeting, and he spoke on ‘Commerce without Conscience – A Matter of National Concern.’

Mr. Jayakumar addressed the CEOs of the Forum on how to overcome the presumption that commerce and conscience are strange bedfellows. He said that everyone wants their work to live even after their time, and this quest for immortality makes people to do great things in life. Art and literature are by-products of this quest, he added.

Mr. Jayakumar said that the moment one thinks that greatness is beyond them, they hamper their chances of becoming a better version of themselves. He said that one can strive for an achievement like success, but greatness cannot be engineered. He said that all successful people are not great, whereas all great people are successful, in their own definition of success.

Mr. Jayakumar added that the main problem arises when one confuses success with greatness, thereby undervaluing the latter, as it can only be achieved by manifesting the greatness within. Deep down, everyone is great, but yet one opts to be ordinary because of the fear of the unknown. He said thisfear prevents one from discovering their inherent greatness as it makes them complacent and limits them from doing their best.

Mr. Jayakumar said that everyone likes to go down the same old path, as one dreads to be different. He spoke about the subconscious fear that makes people prefer their accustomed attitudes and behaviour. Thoughts confine everyone and false assumptions limit them from exploring new avenues.

The session covered the importance of integrity as a catalyst in eliminating fear and realizing one’s self-worth. Mr. Jayakumar spoke on mending the gaps between one’s thoughts and words, between thoughts and actions, between head and heart, between compassion and courage, etc. as it is an important step in cultivating integrity. He said that if one feels less fearful from day to day, he/she is in the process of discovering his/her greatness.

He concluded the session by saying that Mahatma Gandhi brought everyone to the baseline, reminding us that nothing is without its proper balance: wealth should be earned through work, pleasure must be enjoyed responsibly, science must regard the feelings and fate of individuals and politics must be conducted with principle. Mr. Jayakumar urged everyone to not give in to the fear of failure and false assumptions which are a roadblock in recognizing the opportunities ahead.

Ms. Nisha Menon, Director – Tax, PwC India gave ‘Quick Bytes’ on the Legacy Dispute Resolution Scheme, 2019.

Mr. K Harikumar, Vice President of the Chamber, proposed the Vote of Thanks.

The interactive session concluded by 10 a.m with Breakfast.

Chamber's representation on the need for the revision of the Foreign Trade Policy (2015-2019)

1 INCLUSION OF MORE TRADE ORGANISATIONS ON THE BOARD OF TRADE

The Directorate General of Foreign Trade vide. Notification No. 11/2015-20 dated 17th July, 2019 merged the Council for Trade Development and Promotion (CTDP) with the Board of Trade (BOT) while retaining the name Board of Trade (BOT). The objective of BOT is to have regular discussion and consultation with trade and industry and advise the Government on policy measures related to Foreign Trade Policy in order to achieve the objective of boosting India’s trade and to bring about greater coherence in the consultation process. The presence of National Level Trade Organisations like ASSOCHAM, CII, FICCI, FIEO etc. as ex officio members will definitely boost the morale of the industry players. We request you to consider inclusion of reputed trade organisations from individual States to improve the quality of the discourse. This will also be in consonance with the BOT’s mandate to provide a platform for State Governments and UTs to articulate their perspectives on trade policies. The Cochin Chamber’s rich experience in foreign trade can definitely support the Board in successfully fulfilling their mandate.

2 REPLICATION OF COCHIN CHAMBER’S E-CERTIFICATE OF ORIGIN MODEL

The Cochin Chamber of Commerce and Industry is an enlisted agency under Appendix 2E authorised to issue Certificates of Origin (Non Preferential). We have developed a system for issuing an Aadhaar based e-Certificate of Origin. This service, the first of its kind in India, was developed with the help of Myeasydocs, a Chennai-based firm which was incubated by IIT Madras. This practice of issuing an e-Certificate of origin can be incorporated in the policy to promote ease of trading. The tool saves time, costs and increases transparency. (Details available at http://bit.ly/CochinChamber)

3 ESTABLISHING DGFT FUNDED TRADE STUDIES RESEARCH CENTRES

The Ministry of Human Resource Development under the scheme of Intellectual Property Education, Research and Public Outreach (IPERPO) has set up IPR Chairs in various Universities and Institutes to promote IPR Education, Research and Training. The scheme was supposed to promote scholarships and fellowships for conducting research in economic, social, legal and technological aspects of World Trade Organisation. Currently twenty IPR Chairs have been set up so far in premier institutes such as Indian Institutes of Management, Indian Institutes of Technology, National Law Universities etc. However, centres focusing on WTO studies are limited to a few institutions like Indian Institute of Foreign Trade (IIFT), Central University of Kerala etc. This represents the lack of institutional arrangements for the promotion of trade research. The DGFT should consider setting up research institutes across the country to promote and engage researchers and academicians working on trade policies. These can also serve as a platform for undertaking empirical research that can be used as evidence for policy making processes. These institutions could also complement the works of IIFT, Centre for Research in International Trade etc.

4 INITIATING DISCUSSION ON ESTABLISHMENT OF FREE PORTS IN INDIA

Dr. HardeepPuri IFS, (current Civil Aviation Minister) in his Carnegie India research paper (available at http://bit.ly/HSPuriFTP) on India’s Trade Policy Dilemma emphasised the conceptual clarity required for trade promotion and trade policy. He pointed at poor logistics infrastructure and weak trade facilitation resulting in India’s rapidly losing competitiveness in the global trade market. We support his suggestion of the unveiling of an innovation incentivization policy for the promotion of innovation. We should also consider adoption of Free Ports as a policy measure for facilitating trade. We need to adopt the lessons offered by reputed free ports such as Hong Kong, Singapore and Dubai. Free Ports are legally areas that, although within the geographic boundary of a country, are considered outside the country for customs purposes. This means that goods and services can enter and re-exit the Port without incurring usual import procedures or tariffs, thereby, effectively promoting and incentivising domestic manufacturing.

5 DIGITALLY INFORMED AND DRIVEN FOREIGN TRADE POLICY

Rashmi Banga’s RIS Research paper (available at http://bit.ly/DigitalReadyFTP ) highlights India’s inadequate digital preparedness for international trade, particularly in comparison to some of the leading players in developing as well as developed countries, which are also its key competitors in international trade. Steps ought to be taken to promote digital elements in different stages of trade, consequently enhancing digital connectivity of traders; developing digital and ICT infrastructure for trade through industrial and institutional partnerships; promoting digital innovation start-ups that facilitate ease of trading etc. Single window digital systems could be put in place to avoid cumbersome application processes required for various stages of trade. GPS enabled Customs clearances can reduce the time taken for the manual verification of seal numbers. The practice of manual submission of E-Way Bills by exporters can be discontinued. Digital integration of compliance requirements at DGFT, Customs and Banks can go a long way in facilitating ease of trade. The Government can also explore the possibilities of Bilateral or Multilateral agreements with major trading nations and partners to facilitate adoption of ‘digitally signed and verifiable’ trading documents.

6 SETTING UP USDA FOREIGN AGRICULTURAL SERVICE LIKE AGENCY

The USA is very proactive in publishing and releasing regular reports on other markets. The United States Department of Agriculture’s Foreign Agricultural Service is responsible for releasing reports on markets in different countries for different products. This data serves as a resource for researchers in aiding the Government through evidence based policy interventions. A similar governmental or quasi-governmental institution exclusively dedicated to track the market of products, trade barriers, compliance hurdles etc. can play a huge role in improving the policy landscape in India.

7 SETTING UP AN OMBUDSMAN FOR FOREIGN TRADE RELATED ISSUES

Ease of availing legal recourse for problems faced while trading, plays a crucial role in encouraging trade. Most traders do not file complaints for fear of vindictive retaliation that they may encounter while pursuing the case. The delay in the resolution of disputes through the existing framework owing to factors like jurisdiction, lack of coordination between departments, confusion in the interpretation of policy provisions etc. hurt the trading community. Hence, there is an urgent need to create a non- bureaucratic dispute resolution mechanism,preferably an Ombudsman. Mediation can also be considered as an option for resolving trade disputes.

8 GI COMMODITIES MARKETING AS A FOREIGN TRADE POLICY PRIORITY

Since the first Geographical Indication (GI) in India was registered in 2004, 301 GI’s have been granted Registration as on July 20, 2019 by the GI Registry, India. The Commerce Ministry has initiated a programme to promote branding and commercialisation of GI products for exports. GI products in developed countries generate sizeable export revenues. Unfortunately, State Governments in India are involved in political battles without really focusing on the aggressive marketing required to tap into the export potential of these products. The new Foreign Trade Policy should expressly mention the need for State and National level marketing interventions required to boost the dormant GI market in India. It should complement the Agricultural Export 2018 policy’s approach which highlighted the need for branding India at global markets.

9 INCLUSION OF RUBBER IN AGRICULTURE EXPORT CLUSTERS AND EXTENSION OF RUBBER PRODUCTIVITY PROGRAMMES

The Union Ministry of Commerce had constituted a list of 50 district product clusters for export promotion, and it is disappointing that of these, only banana, turmeric, pepper and cardamom have been recommended from Kerala. Kerala has a substantial share in the production of four plantation crops – rubber, tea, coffee and cardamom. Kerala’s share in the national production of rubber is 78 percent and definitely deserves a rubber district cluster, preferably in Kottayam which produces almost three fourths of the rubber produced in the country. The National Rubber Policy 2019 also accepted the demand of the rubber growers for its categorisation as an agricultural product.

The Foreign Trade Policy Statement 2017, acknowledged the need for productivity enhancement for all plantation products, particularly tea and coffee. The Government is planning to expand production area expansions schemes in Chhattisgarh, Jharkhand, Odisha, Maharashtra. We would like the Government to devise schemes for enhancing productivity support to farmers and planters.

10 RESUMPTION OF SHRIMP EXPORTS TO THE US

The Department of State in the US issued a notification in May 2017 banning wild caught shrimp from countries that do not comply with fishing practices to protect sea turtles. The notification imposed a ban on shrimps caught by vessels not fitted with Turtle Excluder Devices (TED). The US team comprising of Department of State environmental officer Joseph A Fette and US National Marine Fisheries Service (NMFS) equipment specialist Kendall Falana had visited Kerala in March to study the activities at Ernakulam and Thrissur harbours and the types of fishing nets used by trawlers. The delay in decision on ban is hurting the business of shrimp exporters.The United States is the largest market for Indian frozen shrimp, followed by Vietnam, Japan, Belgium and the Netherlands. There is an urgent need for an intervention to safeguard the interests of those involved in these businesses.

11 MEIS BENEFIT FOR TRADERS

The 2015-20 policy reduced the Merchandise Exports from India Scheme (MEIS) benefit from 5 per cent to 3 per cent in respect of bulk teas which adversely impacted the tea industry. In response to a Rajya Sabha question dated 29th April 2015, the then Commerce Minister Smt. Nirmala Sitaraman acknowledged the representation from Tea traders suggesting restoration of the reward rate for bulk tea exports from 3% to 5% of FOB value as available under the previous Foreign Trade Policy (FTP). The Ministry promised to review these representations and consider them while updating the Foreign Trade Policy.

Fine points

Article

India could lose the equivalent of 34 million jobs in 2030 due to global warming, says ILO

Farmers are set to be worst hit by rising temperatures

The agricultural and construction sectors would be hit, says report India is projected to lose 5.8 per cent of working hours in 2030, a productivity loss equivalent to 34 million full-time jobs, due to global warming, particularly impacting agriculture and construction sectors, a report by the UN labour agency said.

The International Labour Organisation (ILO) released its report ‘Working on a Warmer Planet: The Impact of Heat Stress on Labour Productivity and Decent Work’, which said that by 2030, the equivalent of more than two per cent of total working hours worldwide is projected to be lost every year, either because it is too hot to work or because workers have to work at a slower pace.

“Projections based on a global temperature rise of 1.5 degrees C by the end of the 21st century, and also on labour force trends, suggest that, in 2030, 2.2 per cent of total working hours worldwide will be lost to high temperatures — a productivity loss equivalent to 80 million full-time job,” the report said.

It said that the accumulated global financial loss due to heat stress is expected to reach USD 2,400 billion by 2030. “If nothing is done now to mitigate climate change, these costs will be much higher as global temperatures increase even further towards the end of the century,” the report said.

India most affected

Countries in Southern Asia are the most affected by heat stress in the Asia and the Pacific region and by 2030, the impact of heat stress on labour productivity is expected to be even more pronounced. In particular, up to 5.3 per cent of total working hours (the equivalent of 43 million full-time jobs) are projected to be lost, with two-thirds of Southern Asian countries facing losses of at least two per cent.

In a dire warning, the report said that the country most affected by heat stress is India, which lost 4.3 per cent of working hours in 1995 and is projected to lose 5.8 per cent of working hours in 2030. Because of its large population, India is in absolute terms expected to lose the equivalent of 34 million full-time jobs in 2030 in productivity as a result of heat stress.

“Although most of the impact in India will be felt in the agricultural sector, more and more working hours are expected to be lost in the construction sector, where heat stress affects both male and female workers,” it said.

Inequality to increase

National-level GDP losses are projected to be substantial in 2030, with reductions in GDP of more than five per cent expected to occur in Thailand, Cambodia, India and Pakistan due to heat stress.

Heat stress is defined as generally occurring at above 35 degrees Celsius, in places where there is high humidity. Heat stress affects, above all, outdoor workers such as those engaged in agriculture and on construction sites. Excess heat at work is an occupational health risk and in extreme cases can lead to heatstroke, which can be fatal, the UN agency said.

The report also noted that Ahmedabad incorporated a cool roofs initiative into its 2017 Heat Action Plan, notably by providing access to affordable cool roofs for the city’s slum residents and urban poor, i.e., those who are most vulnerable to the health effects of extreme heat. The initiative aims to turn the roofs of at least 500 slum dwellings into cool roofs, improve the reflectivity of roofs on government buildings and schools, and raise public awareness.

“The impact of heat stress on labour productivity is a serious consequence of climate change,” said Catherine Saget, Chief of Unit in the ILO’s Research department and one of the main authors of the report. “We can expect to see more inequality between low and high-income countries and worsening working conditions for the most vulnerable.”

Farmers, senior citizens worst hit

With some 940 million people active in agriculture around the world, farmers are set to be worst hit by rising temperatures, according to the ILO data, which indicates that the sector will be responsible for 60 per cent of global working hours lost from heat stress, by 2030.

Construction will also be “severely impacted”, with an estimated 19 per cent of global working hours lost at the end of the next decade, ILO says. Other at-risk sectors include refuse collection, emergency services, transport, tourism and sports, with southern Asian and western African States suffering the biggest productivity losses, equivalent to approximately five per cent of working hours by 2030.

The report noted that a labour market challenge pertains to the high rates of informality in the region, particularly in Southern Asia and South-East Asia.

As many as 90 per cent of all workers in India, Bangladesh, Cambodia and Nepal work informally. Although the prevalence of informality can to a great extent be explained by the high share of employment in agriculture, informality is also pervasive in other sectors, including construction, wholesale and retail trade, and the accommodation and food service industries.

“Temperatures exceeding 39C can kill. But even where there are no fatalities, such temperatures can leave many people unable to work or able to work only at a reduced rate. Some groups of workers are more vulnerable than others because they suffer the effects of heat stress at lower temperatures,” the report said. Older workers, in particular, have lower physiological resistance to high levels of heat and represent an increasing share of workers, a natural consequence of population ageing.

From........... the Research Wing

The Chamber has submitted inputs to the Directorate General of Foreign Trade, New Delhi on the Foreign Trade Policy. Through this submission, the Chamber has re-emphasised its commitment towards supporting trade related policy initiatives institutionalised by the Government. Among the various submissions the Chamber has suggested the need for the inclusion of trade organisations in the various Committees, the promotion of digitisation of trade processes and documentation, setting up research centres at premier institutes etc. The Chamber has also requested the Government to urgently intervene in the US ban imposed on shrimp exports from India.

POLICY DEVELOPMENTS CORNER

- The Finance Minister Ms. Nirmala Sitharaman has, on 23rd August 2019, announced a number of measures to boost the economy. The Government announced its decision to withdraw the surcharge on FPI and Angel Tax on Start-ups. Among the other important announcements, Ms. Sitharaman said that CSR violations wouldn’t be treated as a criminal offence and promised to release pending GST refunds within 30 days.

Click here to view details

- GSTN has uploaded the draft E Invoice standard for public comments. Click here to view the draft

- Comments invited on Model Framework for Guidelines on e-Commerce for Consumer Protection : Submit by 16th September. Draft can be viewed in this link

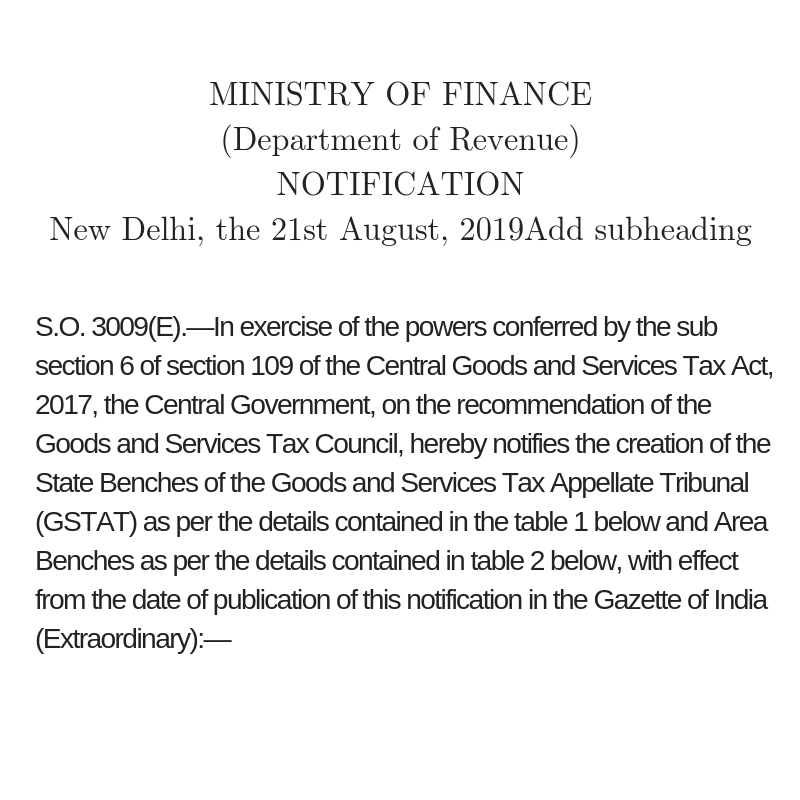

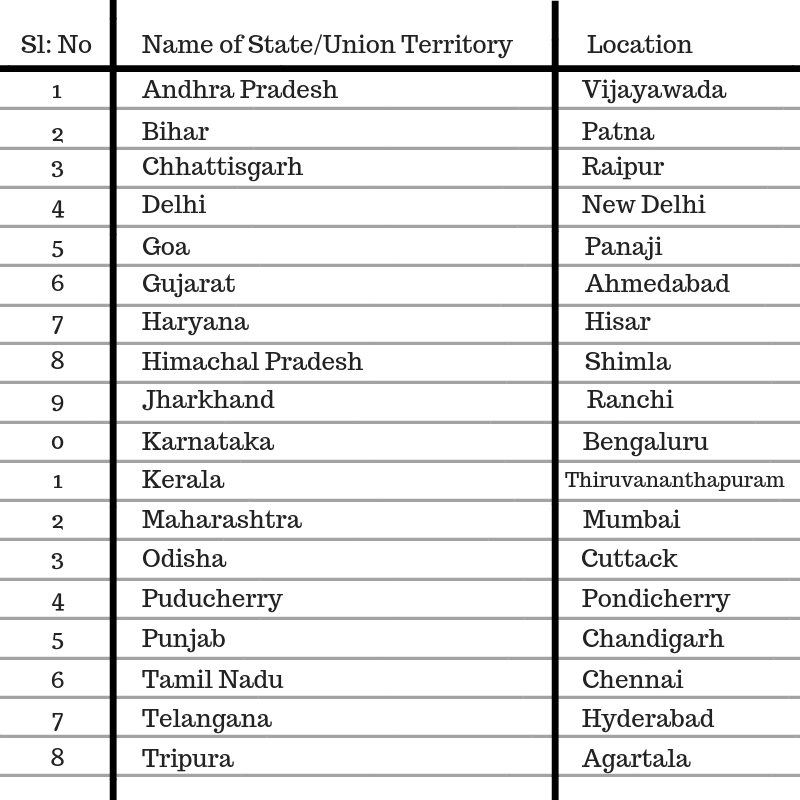

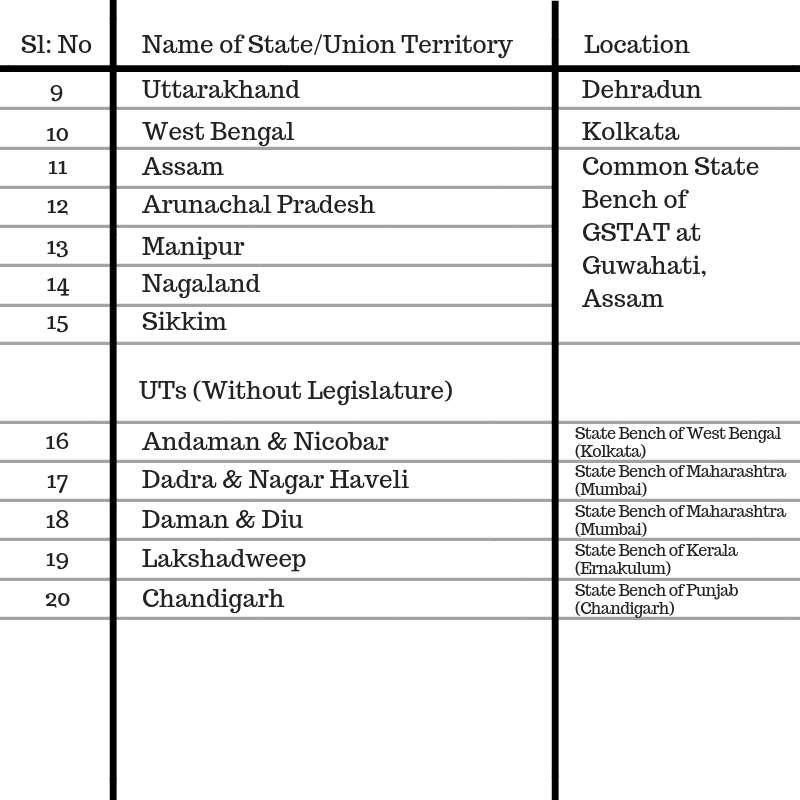

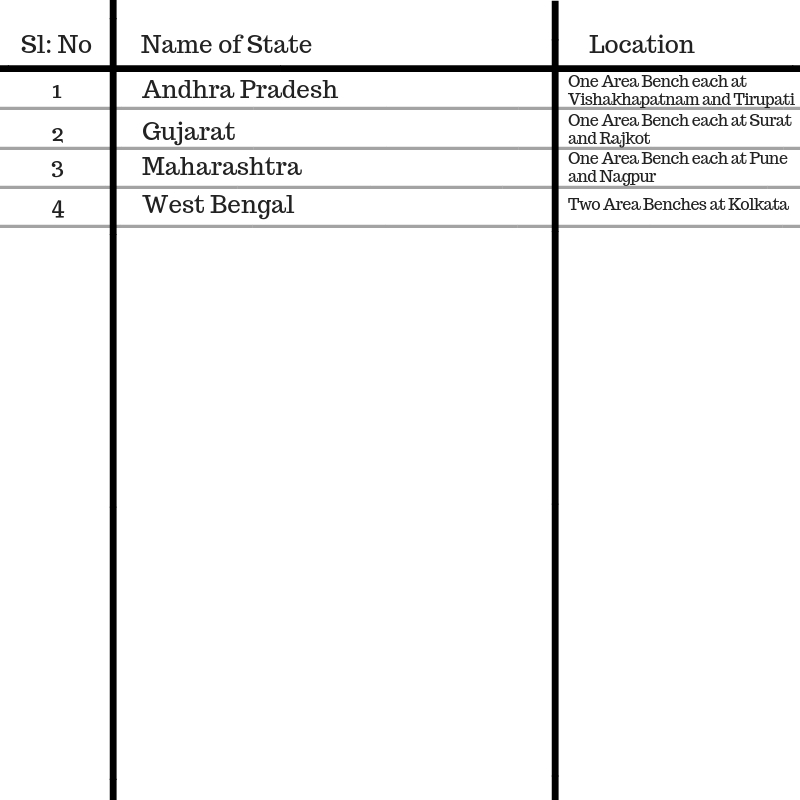

- The Ministry of Finance vide notification S.O. 3009(E) dated 21st August 2019 has notified the creation of the State Benches of the Goods and Services Tax Appellate Tribunal (GSTAT). Kerala’s State Bench will be located at Thiruvananthapuram. Detailed notification available here

- The Companies (Amendment) Bill, 2019 received the President’s approval on 31st July, 2019 and was notified as the Companies (Amendment) Act, 2019. The Companies (Amendment) Act, 2019 notified 43 sections out of which 31 sections were effective retrospectively from 2nd November, 2018. Other Sections are to be notified by the Ministry by way of separate commencement notification. Accordingly, the Ministry, on 14th of August, 2019 further notified 10 Sections to be effective from the date of notification. However, the Ministry of Corporate Affairs (MCA) has refrained from putting into effect the controversial CSR amendments in the recently enacted Companies (amendment) Act 2019 while going ahead with implementation of all other provisions in the amendment law. Brief summary of the changes available here

Tax and Regulatory Updates from PricewaterhouseCoopers

Direct Tax

CBDT extends the due date of filing income-tax return from 31 July to 31 August 2019

The Central Board of Direct Taxes, vide its order under section 119 of the Income-tax Act, 1961 (the Act), extended the due date of filing income tax returns for the financial year 2018-19 from 31 July to 31 August 2019. This will apply to all taxpayers who were required to file their returns by 31 July 2019.

PwC comments: This is a welcome step that will provide adequate time to the taxpayers to comply with the filing requirement. Taxpayers were facing difficulties in meeting the 31 July deadline due to multiple reasons, namely, collating details to meet up with additional disclosure requirements introduced in the income-tax return forms, late receipt of Form 16 due to extension of the due date for the issuance of Form 16 by the employer to 10 July 2019, multiple revision in the tax filing software (utility) etc. The extension also provides relief to the taxpayers from late filing fees of INR 5000 and also interest under section 234A of the Act (at 1% per month), if they file their returns by 31 August 2019. However, taxpayers should be careful in paying up the tax due, if any, by 31 July 2019 to avoid any additional monthly interest (at 1% per month) under section 234B of the Act if the same is paid in August 2019 at the time of filing the return

Even if additional Floor Space Index (FSI) assumed to be transferred in a redevelopment agreement, no capital gains arise absent any cost of acquisition

Recently , the Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) held that no capital gains tax should be applicable on transfer of additional floor space index (FSI) created due to the operation of “Land Development Control Rules, 1991” (DCR). The key reason being the absence of an element of cost in acquiring it. Furthermore, section 50C of the Income-tax Act, 1961 (Act) is applicable only on the transfer of land or building or both.

PwC comments: This decision re-emphasizes the principle that right to additional construction on acquisition of additional FSI by operation of the DCR, having no cost of acquisition to the taxpayer, should not be charged to tax as capital gains. Further, in case of transfer of TDR, since it has an element of cost (e.g. cost of land surrendered), the chargeability of capital gains may have to be evaluated. The provisions of section 50C of the Act should not be applicable for “rights in Development Agreement”. However, in the current context, the interplay of section 56(2)(x) of the Act should be evaluated

Even if additional Floor Space Index (FSI) assumed to be transferred in a redevelopment agreement, no capital gains arise absent any cost of acquisition

Recently , the Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) held that no capital gains tax should be applicable on transfer of additional floor space index (FSI) created due to the operation of “Land Development Control Rules, 1991” (DCR). The key reason being the absence of an element of cost in acquiring it. Furthermore, section 50C of the Income-tax Act, 1961 (Act) is applicable only on the transfer of land or building or both.

PwC comments: This decision re-emphasizes the principle that right to additional construction on acquisition of additional FSI by operation of the DCR, having no cost of acquisition to the taxpayer, should not be charged to tax as capital gains. Further, in case of transfer of TDR, since it has an element of cost (e.g. cost of land surrendered), the chargeability of capital gains may have to be evaluated. The provisions of section 50C of the Act should not be applicable for “rights in Development Agreement”. However, in the current context, the interplay of section 56(2)(x) of the Act should be evaluated.

Tribunal holds that Tax Officer (TO) cannot tinker with prescribed valuation method adopted by taxpayer for computation under section 56(2) (viib) of the Act and question commercial prudence

The Delhi Bench of the Income-tax Appellate Tribunal (Tribunal) held that the TO cannot reject the valuation report obtained from a prescribed valuer under a method of valuation prescribed under section 56(2)(vii)(b) of the Income-tax Act, 1961 (Act). There are no express provisions under the Act or the Income-tax Rule, 1962 (Rule) where the TO can adopt his own valuation under the discounted cash flow (DCF) method or obtain a valuation from a different valuer. The Tribunal further ruled that the TO cannot challenge the commercial prudence and wisdom of the taxpayer or the investors.

PwC comments: The judgement provides relief for genuine business transactions, wherein investments are based on future projections and prospects of the company. It has clearly noted that the TO cannot question the choice of method of valuation, as long as it can be justified by the taxpayer and a report to that effect has been obtained from a prescribed expert.

Conversion of firm into a company does not amount to distribution of assets – firm not liable to capital gains tax

In a recent ruling, the Ahmedabad Bench of the Income-tax Appellate Tribunal (Tribunal), held as follows:

- Revaluation of assets could not be treated as transfer within the meaning of section 2(47) of the Income-tax Act, 1961 (the Act).

- When converted into a company, the properties of the erstwhile firm vest into the company. Such vesting could not be equated to the distribution of assets as stipulated under section 45(4) of the Act.

- No justification found to hold that there was any transfer of asset and thus, the question of liability to pay tax on capital gains by the firm does not and cannot arise at all.

PwC comments: The decision reaffirms the position that for invoking section 45(4) of the Act, a distribution of capital asset of the firm on dissolution thereof is necessary, which is missing in the conversion of a firm into a company. It impliedly confirms that the conversion of a firm into a company only results in vesting of property and may not tantamount to transfer, and thus, is not liable for capital gains tax.

Tribunal holds that long-term capital loss, on STT paid sale of listed shares, is eligible for carry forward and set-off

The Kolkata bench of the Income-tax Appellate Tribunal (Tribunal) in the case of the taxpayer held that long-term capital loss (LTCL) on sale of listed shares [securities transaction tax (STT) paid] is eligible to be carried forward notwithstanding that gains on sale of such shares are exempt under section 10(38) of the Income-tax Act, 1961 (the Act) as per the erstwhile law.

PwC comments: The judgement reaffirms the position that LTCL on listed securities (which if income will be exempt under section 10(38) of the Act) should be allowed to be set-off against other capital gains and/ or to be carried forward. The Tribunal reiterates the principle that if a source of income is completely exempt from tax, the set-off and carry forward of loss shall not be available. However, if the exemption applies only to a part of the source of income and/ or is subject to fulfilment of some conditions, the loss from such source of income will be allowed to be set-off and carried forward

Transfer Pricing

Penalty proceedings can be initiated even if dispute resolved by enforcement of MAP

Recently, the High Court (HC) of Karnataka ruled on the constitutional validity of penalty proceedings to h0ld that the provisions of section 271(1)(c) of the Income-tax Act, 1961 (the Act) would continue to apply to cases resolved under a Mutual Agreement Procedure (MAP), unless the Double Tax Avoidance Agreement (tax treaty) or the MAP specifically waives the penalty

PwC comments: The HC ruled on the constitutional validity of the penalty proceedings in case of MAP resolutions, wherein the Transfer Pricing (TP) adjustment is only reduced and has not annulled the assessment proceedings. The onus lies on the taxpayer to prove that there is no concealment of income or furnishing of inaccurate particulars and to maintain the TP documentation in respect of such transactions in good faith and due diligence while determining the Arms’ Length Price (ALP). Considering that in a MAP resolution, the tax liability is determined merely on the basis of negotiation/ compromise and where the taxpayer does not even have the opportunity to be present during such negotiations, there should not be any question of concealing the particulars of income since the dispute was settled under a mutual understanding. The taxability of income determined under MAP takes precedence over the earlier determination by the TO, and there cannot be concealing or furnishing of inaccurate particulars. Additionally, a resolution accepted by the taxpayer in the MAP has the effect of substituting the originally returned income with the further additional income as accepted under the MAP. Therefore, since the MAP resolution has the effect of going back to the originally returned income, there cannot be a question of levying penalty

Draft assessment order issued erroneously in the name of the amalgamating entity invalidates final assessment on the amalgamated entity

Recently, the Mumbai bench of the Income-tax Appellate Tribunal (Tribunal) quashed the entire assessment as the draft of the proposed order of assessment (draft assessment order) was passed incorrectly in the name of a non-existent entity, although the final assessment order was framed in the correct entity’s name. The Tribunal ruled that since the Transfer Pricing Officer’s (TPO’s) order was made in the name of a non-existent entity, the “eligible assessee” did not exist as per section 144C of the Income-tax Act, 1961 (the Act). A draft assessment order passed in absence of an “eligible assessee” is a jurisdictional defect and not a procedural irregularity, thus the assessment was bad in law.

PwC comments: This ruling is the first of its kind, wherein the entire assessment has been quashed because the draft assessment order was issued in the name of an entity that did not exist on the date of the order, although the final assessment order was issued in the correct name. This ruling reaffirms the principle that violation of mandatory procedures laid down in the scheme of assessment under section 144C of the Act by the income-tax authorities, leads to a jurisdictional defect and cannot be termed a procedural irregularity. It is imperative that the taxpayer intimates the income-tax authorities about the fact of amalgamation, winding up, death of taxpayer, etc., before the income-tax authorities pass the assessment order, to succeed in challenging the validity of assessment made upon a non-existent person.

Issue of notice and assessment order in the name of the amalgamating company, which ceased to exist, is invalid: not a defect curable under section 292B

Recently, the Supreme Court (SC) held that the issuance of jurisdictional notice, and thereafter, passing of assessment order by the Tax Officer (TO) in the name of a non-existent entity would render the assessment proceeding non est. Furthermore, profound importance was given to the rule of certainty, consistency and uniformity.

PwC comments: The jurisdictional notice issued by the TO as well as the order passed in the name of a non-existent person would render the assessment proceeding non est. Further, the ambiguity over the conflict arising between the decisions of Skylight Hospitality LLP and Spice Enfotainment has been put to rest. It has been specifically noted that the decision of Sky Light Hospitality LLP was in view of the peculiar facts of the case, whereas, Spice Enfotainment continues to apply when a jurisdictional notice/ order is issued on a non-existent person. Furthermore, profound importance has been given to the rule of consistency and uniformity.

Regulatory

The Companies (Amendment) Bill, 2019 receives President’s assent

The President of India has given its assent to the Companies (Amendment) Bill, 2019, which further amends the Companies Act, 2013 (the Act). The Companies (Amendment) Bill, 2019 has been now published in the Official Gazette on 31 July 2019 as the Companies (Amendment) Act, 2019 (the Amendment Act). The Amendment Act has taken into consideration the amendments that were originally notified in the Companies (Amendment) Ordinance, 2018 which was promulgated by the President on 2 November 2018, and then retained in effect through the Companies (Amendment) Ordinance Act, 2019 and the Companies (Amendment) Second Ordinance, 2019 promulgated by the President on 12 January 2019 and 21 February 2019, respectively. Further, the Amendment Act has brought about other key changes enumerated in the succeeding paras. While the amendments implemented through the ordinances1 have already been in effect since 2 November 2018, the new amendments introduced by the Amendment Act will come into force from the date on which it’s prescribed by the Central Government by way of a notification in the Official Gazette. The key amendments other than those that were bought in through the ordinances, are analysed below

- Prospectus for public offer

The previous provision required a company to deliver a copy of the prospectus to the registrar for registration. However, with the amendment, the requirement has been changed from “registration” to “filing”

- Dematerialisation of securities

The Central Government can now prescribe and mandate even private limited companies to issue and hold securities in DEMAT form.

- Significant Beneficial Owners

The responsibility of the company to identify an individual who is a SBO and cause such individual to make a declaration was previously included in the Companies (Significant Beneficial Owners) Amendment Rules, 2019 notified on 8 February 2019. The Act has now been amended to also echo the same intention, as it casts responsibility on a company to take necessary steps to identify the SBO and cause the SBO to comply with the SBO provisions under the Act.

- Corporate Social Responsibility

- For the companies who have not completed three years, the amount of CSR contribution shall be calculated on the average of net profits for the years since incorporation.

- The unspent CSR amount, except for the amount that relates to any ongoing projects, is required to be transferred to any of the funds mentioned in Schedule VII of the Act, within a period of six months from the end of the financial year (FY).

- The unspent amounts in relation to ongoing projects should now be transferred to a separate bank account within 30 days from the end of FY, and such amount should be spent within a period of three FYs from the date of such transfer. In case such amount remains unspent after completion of three FYs, the said amount is then required to be transferred to any of the funds mentioned in Schedule VII, within a period of 30 days from the date of completion of the third FY.

- Penalty provisions for non-compliance of the CSR provisions has been introduced. As per the new provision, the failure to comply with the CSR provisions makes the company liable to a fine ranging from INR 0.05m to INR 2.5m, and every officer in default can be punished with imprisonment that may extend to three years or with a fine ranging from INR 0.05m to INR 0.5m or both.

- Powers of the Central Government and NCLT in case of oppression and mismanagement

- The Central Government is now empowered to initiate a case against unfit and improper persons (i.e. persons concerned in the conduct and management of a company, who have been found guilty of fraud, misfeasance, not conducting the business in accordance with sound business principles or practices, etc.) and refer the same to the National Company Law Tribunal (NCLT) to make inquiry and record a decision to declare if such a person is fit and proper to hold office of director or any other office connected with the company.

- NCLT is now empowered to determine, in case of oppression and mismanagement, if a person connected with any conduct or management of the company, is fit and proper. In case the NCLT reaches a conclusion that such a person is not fit and proper, then such a person can be debarred from holding an office of a director or any other office connected with a company for a period of five years from date of NCLT’s order. Further, such person shall not be entitled to be paid any compensation for the loss of office

PwC comments: PwC Comments: The Central Government, with the Amendment Act, is further trying to strengthen the governance framework for companies. It has also provided a key thrust to the CSR agenda, indirectly mandating all companies to spend towards CSR activities, against the initial stance of “comply or explain” to now “comply or explain and comply”.

Indirect Tax

Gujarat High Court (HC) issues decision on last date for claiming ITC for invoices from July 2017 to March 2018

Facts of the Case

The taxpayer, via a writ petition, challenged the press release dated 18 October 2018, which clarified that input tax credit (ITC) for invoices issued during July 2017 to March 2018 can be availed until the last date of filing Form GSTR-3B for September 2018, i.e., until 20 October 2018. The taxpayer contended that the clarification is contrary to section 16(4) of the Central Goods and Services Tax Act, 2017 (CGST Act, 2017), as the return prescribed under section 39 of the CGST Act, 2017 is a return required to be furnished in Form GSTR-3 and not Form GSTR-3B. Further, the taxpayer submitted that Form GSTR-3B has been notified in terms of Rule 61(5) and not section 39 of CGST Act, 2017.

High Court's decision

The Gujarat High Court (HC) answered in favour of the taxpayer and observed as follows:

- It was the Government’s decision, factoring the technical glitches and difficulties faced by taxpayers in filing Forms GSTR-2 and GSTR-3, both which are in abeyance. Thereafter, the eighteenth GST Council meeting decided to allow filing of a shorter return in Form GSTR-3B for an initial rollout period.

- Form GSTR-3B was not introduced as a return in lieu of return required to be filed in Form GSTR-3. The return in Form GSTR-3B was only a temporary stopgap arrangement until the due date of filing return in Form GSTR-3 was notified.

- Subsequently, through notification no. 10/ 2017 – Central Tax dated 28 June 2017, the Government introduced mandatory filing of return Form GSTR-3B, stating that it is a return in lieu of Form GSTR-3. Thereafter, the Government omitted such reference retrospectively, vide notification no. 17/2017 –Central Tax dated 27 July 2017.

Therefore, para 3 of the press release dated 18 October 2018, clarifying that the last date for availing ITC relating to invoices issued during July 2017 to March 2018, as the last date for filing return in Form GSTR-3B, is illegal and contrary to section 16(4) read with section 39(1) and Rule 61 of the CGST Rules.

PwC comments: This is a welcome decision by the Gujarat HC, which addresses the dilemma prevailing over the industry qua the last date for availment of ITC for invoices issued during the first nine months of the GST regime. It may be noted that the industry continues to face “mismatch” or “unmatched” invoices for this period. If not further litigated, the taxpayer can now avail ITC for the period 2017-2018 until 31 August 2019, as the current due date for furnishing annual return.

Delhi HC allows interim relief on widened anti-profiteering investigation prior to completion of initial investigation by National Anti-Profiteering Authority (NAA)

Facts of the Case

The applicant filed a writ against a notice issued by the Director General of Anti-Profiteering (DGAP) seeking information on all products of the company, although the National Anti-Profiteering Authority (NAA) had ordered an inquiry only on one product. The notice drew reference to the recent amendment in the Central GST Rules, 2017 (CGST Rules), which ostensibly allowed such widened investigation. The amendment allowed the NAA, if it had reasons to believe that a contravention had occurred in the report issued by the DGAP, to direct it to investigate into the goods or services not covered in its report.

High Court's decision

The Delhi High Court (HC) allowed interim relief to the company and held that at this stage, the company should not be required to furnish information to the DGAP other than in relation to the [one] product that was the subject of complaint, since the primary investigation was not yet completed. Additionally, the HC clarified that the NAA’s current inquiry on the subject product can proceed in accordance with law.

PwC comments: There were recent amendments to the CGST Rules granting powers to the DGAP to conduct investigations that may now possibly extend inquiries to situations outside the original complaints. Although this is an interim decision, the HC’s decision is a relief in the current circumstances, as the widening of the investigation must follow an initial investigation, which must be completed. This also underscores the industry’s demand from the Government seeking the issuance of definitive guidelines on anti-profiteering proceedings.

Patna HC holds that no recovery proceedings under section 73 of the Bihar Goods and Services Tax (BGST) Act can be initiated against Input Tax Credit (ITC) availed but not utilized

Facts of the Case

The assessee inadvertently failed to carry forward ITC for the financial years (FYs) 2007-08 and 2011-12 in the value added tax returns for the said period. On detection of omission in FY 2017-18, the assessee filed a refund application, which the Tax Officer (TO) rejected because it was time barred. The adjudication of the refund application for the period FY 2011-12 is currently pending.

Thereafter, the assessee opted to take the benefit of section 140 of the BGST Act, and include the transitional ITC pertaining to FYs 2007-08 and 2011-12 in its electronic credit ledger through TRAN-1. The transitional credit for the FYs 2007-08 and 2011-12, as carried forward into GST, has not been utilised against payment of output liability until date.

The TO rejected the carry forward of credit under section 140 of the BGST Act, and initiated recovery of taxes with interest and penalty under section 73 of the BGST Act. The assessee challenged this action before the Patna High Court (HC) via a writ.

High Court's decision

The HC categorically stated that it expressed no opinion on the rejection of transitional credit carried forward, as the assessee had not sought any relief in that respect. The HC restricted its examination to the legality of proceedings initiated under section 73 read with section 50 of the BGST Act.

Upon examination, the HC set aside the recovery proceedings and put forth as follows:

- Mere reflection of credit in the electronic credit ledger cannot be termed as equivalent to availment of credit or utilisation of credit, unless it is actually utilised for payment of tax liability at the time of filing returns.

- A claim for transitional credit can at best, only be rejected. No statutory jurisdiction is bestowed upon the assessing authority to create a tax liability, in the absence of an existing/ outstanding liability or on actual utilisation of transitional credit.

PwC comments: This is welcome relief granted by the Patna HC, which addresses the dilemma in the industry regarding the applicability of interest on transitional and other credit availed but not yet utilised on account of prevailing uncertainty in creditable duties. This is in line with jurisprudence emanating from judgements issued by the HCs of Madras and Kerala under service tax regulations.

Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019

In continuation of various Amnesty schemes introduced by States such as Gujarat, Kerala, Karnataka, Maharashtra, Madhya Pradesh, Haryana and Rajasthan, the Central Government, to “unload the baggage of more than INR 3.75 lakh crores (3750bn) blocked in litigations in service tax and excise and allow the business to move on” has proposed to introduce a legacy dispute resolution scheme (scheme). This will allow quick closure of pre-GST litigations.

The salient features of the scheme are as follows:

Some points to be noted

- No outer time limit is prescribed for the operation of the scheme.

- The scheme does not cover cases in which interest alone is in dispute.

- More clarity is required on the manner in which “voluntary disclosure” operates under the scheme.

- It is unclear whether CENVAT credit reversal issues (specifically for service tax assesses) is covered under the scheme

PwC Comments: As new litigations surface under GST, it is important that the Government resolve past tax disputes as early as possible. This onetime dispute resolution scheme is a welcome step towards addressing long-pending litigations. With complete waiver of interest, penalty and prosecution, and part waiver of tax dues, this would be an opportune moment for assessees to review their old tax disputes for early closure

Central Board of Indirect and Customs (CBIC) issues clarification on supply of ITeS qualifying as “export of services”

The CBIC has issued a clarification illustrating three scenarios when a supplier of Information Technology enabled Services (ITeS) such as call centres, business process outsourcing services, etc. located in India, will qualify as export or intermediary for determining GST liabilities on such services. The CBIC has contextualised its comments on the categories of ITeS listed in Rule 10TA (e) of the Income-tax Rules, 1962.

The scenarios discussed are summarised as follows:

Scenario - I: Supply on own account

Services in the form of back-end services to the client on its own account or even the client’s customer, have been clarified to not qualify as an “intermediary.” This will apply when “A” supplies services on its own account to his client “B” or to B’s customer “C.” This would not be categorised as an intermediary under section 2(13) of the Integrated Goods and Service Tax Act, 2017 (IGST Act), and the place of supply will be determined basis the location of the recipient of service.

Scenario - II: Supply by arrangement or facilitation

When the supplier arranges or facilitates the supply of goods or services between two or more persons, such services will be considered as intermediary services under section 2(13) of the IGST Act. The circular has provided an illustration for back-end support services in the nature of pre-delivery, delivery and post-delivery support (such as order placement, delivery and logistical support, obtaining relevant Government clearances, transportation of goods, post-sales support and other services, etc.). Because of such services qualifying as an intermediary, the zero-rated status as “export” will not be available.

For example, supplier “A” located in India arranges or facilitates back-end services such as delivery, logistical support and post-sales support, etc. to customer “C” on behalf of his client “B” located abroad would be an intermediary. Consequently, the place of provision of service shall be India and such services will attract GST.

Scenario - III: Supply on own account along with arrangement or facilitation

The supplier is providing a combination of services described in Scenarios I & II, i.e., two sets of services, namely, services on its own account and other back-end facilitation services. In this case, the circular prescribes that the supplier of such services may fall under the purview of intermediary services depending on the facts and circumstances of each case, and the set of services determined as the principal/ main supply.

PwC Comments: The circular is a partial relief to the industry, as it clearly states the principle that unless a clear arrangement or facilitation of goods/ services exists, ITeS will not be considered as intermediary services, when the provision of service is on its own account. However, the circular is silent on the criteria for qualifying as a service rendered on one’s own account. However, for other services potentially falling under Scenario II, will result in a debate. This is because the Appellate Authority for Advance Ruling in Maharashtra, while examining similar facts, held that back-office support services such as post-transaction support do not qualify as “export of service,” as they are in the nature of arranging or facilitating supply of goods between overseas companies and customers. However, the Authority for Advance Ruling ruling in Karnataka has approved the position that post-transaction support will qualify as export. Going forward, the application of this circular could unsettle export positions under GST by treating pre or post-sale support services as an “intermediary,” as the general understanding has been that only sale origination and execution roles (performed by commission agents and brokers, etc.) are covered in this category. This challenge could apply to both GST and the erstwhile service tax law, since the definition of intermediary is largely unaltered in the IGST Act

Non-Tax and Tax Updates

Budget - Corporate Update

Budget - DT update

Corporate Updates - August 2019

GST Council notifies creation of State Benches of GSTAT

NOTIFICATION

Table-1

Table-1

Table 2

Finer Points

NOTIFICATION

Chamber in the Newspapers

Forthcoming Events

9th CEO FORUM Breakfast Meeting 2019 | Cross Border Mergers and Tax Due-Diligence Impact Areas

Friday, 6th September 2019 | Taj Gateway Hotel, Ernakulam

With Cross-Border mergers now being a reality, this presents Indian companies with additional avenues to explore international expansion or engage in strategic consolidation to optimize group operations. This session will provide a conceptual understanding of the regulations relating to cross border mergers from various aspects, such as tax exchange regulations, and accounting, and it will also include case studies of practical instances of cross border mergers being undertaken by Indian Companies.

An effective due-diligence is a critical step for any successful merger, acquisition or investment deal. This session will help in understanding the key impact areas while undertaking a tax due-diligence. We will specifically focus on the technical and practical considerations to be borne in mind, while investigating and analyzing the tax aspects of a potential target company”

The Session will be handled by Mr. Alwar Rajkumar, Director in PwC ‘s Mergers & Acquisitions Tax Practice.

Delegate Fee:

Member: Rs. 1,500/- (incl. 18% GST)

Non-Member: Rs.1,750/- (incl. 18% GST)

Kindly click here to register for the session.

Workshop on Challenge the Status Quo

Friday, 20th September 2019 | Hotel Park Central, Kaloor, Ernakulam

The Cochin Chamber of Commerce & Industry is organising a One Day Interactive Workshop on “Challenge the Status Quo” on Friday, 20th September 2019 at Hotel Park Central, Kaloor, Cochin. The Session is scheduled from 9 am to 5 pm.

About the Workshop

Among the most well-known phrases in today’s work environment is ‘thinking outside the box’. It means thinking creatively, freely, and off the beaten path. It’s the kind of thinking that — in an age of increasingly powerful algorithms and neural networks — garners significant attention. The Workshop is designed to empower the participants to dispense with constraints and generate original and innovative solutions.

Cmde. S Sreeram and Cdr. Ninad Phatarphekar, Founders of Transformavens Training & Consulting LLP, Mumbai will be the Speakers at the Workshop.

Participant Profile

Leaders across all experience and hierarchical levels will benefit from the programme.

Registration Fee

Member fee – ₹1500/- (Inclusive of GST)

Non Member fee – ₹2000/- (Inclusive of GST)

Schedule

The Workshop will be conducted over a day with 4 sessions of 90 mins each with two tea breaks and a lunch break in between.

Click Here to register

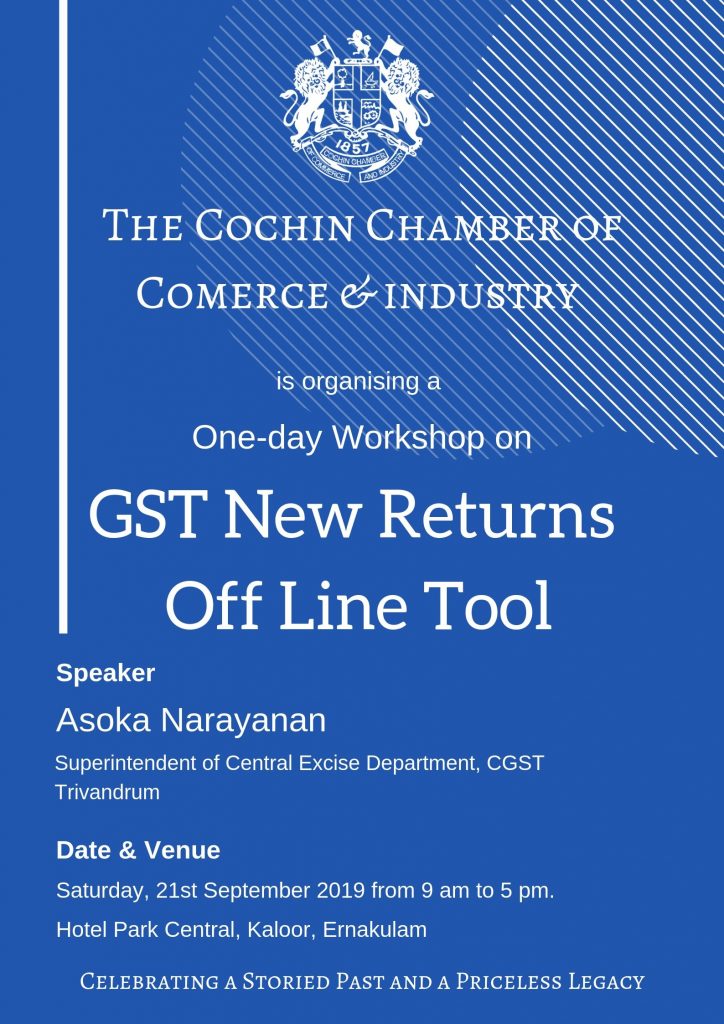

One day Workshop on GST New Returns Off-Line Tool

Saturday, 21st September 2019 | Hotel Park Central, Kaloor, Ernakulam

For further details contact

Manu Varghese: 9895676827

Archana A.K: 8921193442

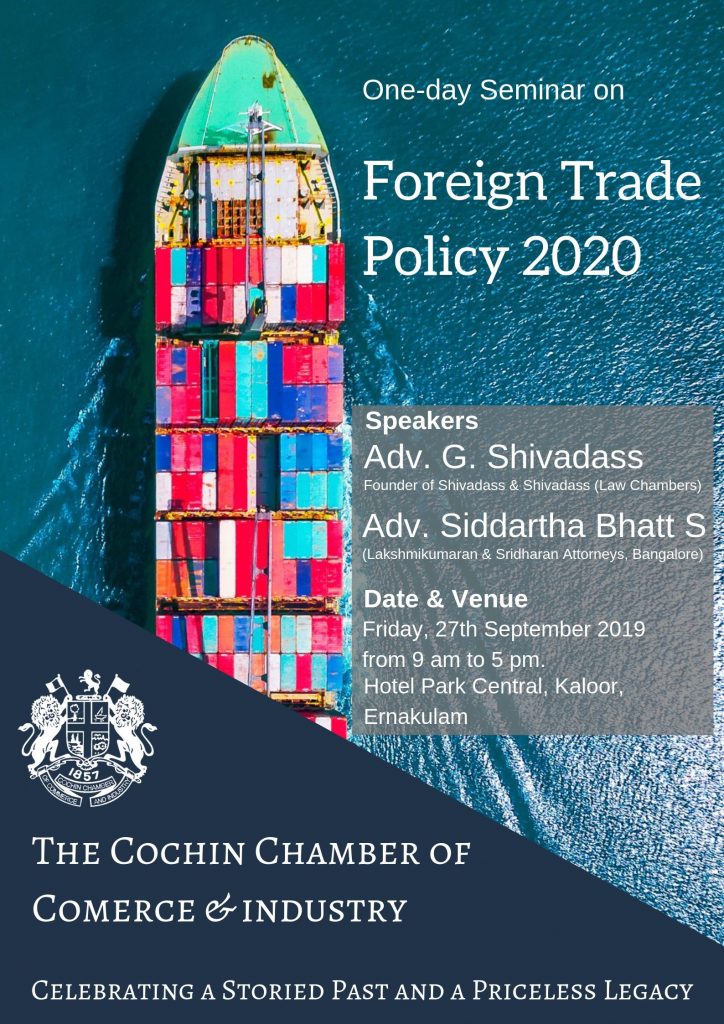

One-day Seminar on the Foreign Trade Policy 2020

Friday, 27th September 2019 | Hotel Park Central, Kaloor, Ernakulam

For further details contact

Manu Varghese: 9895676827

Archana A.K: 8921193442